|

市場調査レポート

商品コード

1685889

輸液ポンプ・付属品-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Infusion Pumps And Accessories - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 輸液ポンプ・付属品-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

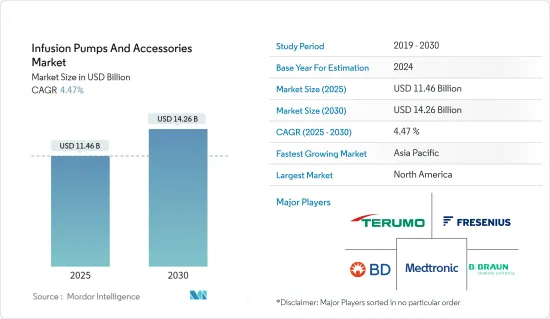

輸液ポンプ・付属品市場規模は、2025年に114億6,000万米ドルと推定され、予測期間(2025年~2030年)のCAGRは4.47%で、2030年には142億6,000万米ドルに達すると予測されます。

COVID-19のパンデミックは輸液ポンプを前面に押し出しました。COVID-19の封鎖期間中に輸液ポンプの需要が大幅に急増し、COVID-19の症例数が入院患者数の増加とともに急速に増加したためです。パンデミックの第一波では、集中治療室(ICU)にいる敗血症患者に必要な栄養素を供給するため、点滴療法の需要が高まりました。例えば、2022年5月にPubMedに掲載された論文によると、COVID-19による入院患者の32.5%に敗血症がみられ、そのうち70.8%はSARS-CoV-2のみによるもので、26.2%はSARS-CoV-2と非SARS-CoV-2の両方によるものでした。そのため、輸液ポンプは敗血症患者の輸液に頻繁に使用され、パンデミック時の市場拡大をさらに後押ししました。

このように、全体としてパンデミックは、ヘルスケア環境における患者数の増加により、市場に健全な成長をもたらしました。しかし、次世代輸液システムの利用増加、輸液バッグの進歩、慢性疾患、事故、輸血の増加は、今後数年間の市場成長を後押しすると予想されます。

輸液ポンプ・付属品市場は、主にがんなどの慢性疾患の罹患率の上昇と輸液デバイスの採用率の上昇によって牽引されています。輸液ポンプは化学療法、糖尿病管理、その他多くの用途で広く使用されています。これらの疾患の有病率が世界的に上昇していることは、市場成長のための十分な機会を生み出しています。がん患者は、過剰な体液喪失(嘔吐や下痢など)や体液摂取不足により、細胞外腔に水分がない状態である体液減少症になりやすいです。

がん患者の増加は、加圧注入バッグの需要を高め、市場の成長を後押しすると予想されます。例えば、米国がん協会の2023年がん統計によると、2023年に米国で新たに発生するがん患者は193万人と推定されています。この推定には、男性101万人、女性94万8,000人の症例が含まれます。がん罹患率の高さが輸液ポンプ・付属品の需要を増大させ、予測期間中の市場成長を後押ししています。

さらに、輸液関連のドラッグデリバリーを含む臨床研究活動の増加が、予測期間中の市場成長を後押しすると予想されます。例えば、2022年11月、がん治療薬のTriSalus Life Sciences, Inc.は、原発性および転移性肝腫瘍を対象とした進行中のPressure-Enabled Regional Immuno-Oncology('PERIO 01')および('PERIO 02')臨床試験に関する追加情報を公開しました。TriSalusプラットフォームは、TriNav注入システムとクラスCトール様受容体9(TLR9)アゴニストであるSD-101で構成されています。TriNavはFDAの認可を受けた装置で、確立された治療薬や新たな治療薬を投与するために設計されています。

さらに、デバイス技術の技術的進歩や主要企業による革新的な製品の発売は、市場の成長を促進すると思われます。例えば、ユナイテッド・セラピューティクスは2021年2月、肺動脈性肺高血圧症(PAH)患者の生活改善に役立つリモデリング薬物デリバリー用ポンプ「Remunity Pump」を発売しました。同様に、2021年2月、Mindray Medicalは、製品ポートフォリオを拡大するための新しい輸液システムであるBeneFusion Eシリーズ-ESP、EVP、EDSを発売しました。

したがって、慢性疾患の増加と輸液ポンプの急速な進歩に加え、主要企業による製品の発売により、市場は予測期間中に大きく成長すると予想されます。しかし、輸液ポンプの高価格とそれに伴う安全性の問題が、予測期間中の市場成長を抑制すると予想されます。

輸液ポンプ・付属品の市場動向

容積式輸液ポンプ分野は予測期間中に大幅な成長が見込まれる

容積式輸液ポンプは、疾病管理および非経口栄養において多くの用途があります。容積式輸液ポンプの安全性、正確性、簡便性は、多くの治療領域の治療に貢献し、これらのポンプの高い需要に寄与しています。容積式輸液ポンプ分野は、輸血症例や薬剤輸液症例の増加、主要企業による戦略的製品上市の増加により、大きな成長が見込まれています。

怪我や外傷の増加により、薬剤輸液の需要が高まると予想され、調査期間中の同分野の成長を牽引すると期待されています。例えば、2022年2月に発表された交通安全観測所の報告書によると、2022年1月にフランスの警察が記録した傷害事故件数は3,728件で、2021年(3,508件)を上回りました。交通事故の負担増は失血につながり、緊急輸血の必要性を生み出し、予測期間中の同分野の成長をさらに押し上げると予測されています。

さらに、革新的な容積式ポンプの進歩や出現は、規制当局の承認の増加とともに、セグメントの成長を後押しすると予想されます。例えば、2022年3月、フレゼニウス・カビは、Agilia容積ポンプとAgiliaシリンジポンプにVigilantソフトウェアスイートVigilant Master Med技術を搭載したワイヤレスAgiliaコネクト輸液システムの規制当局認可をFDAから取得しました。アジリアコネクトポンプとシリンジポンプは、2021年に医療機器開発協会(AAMI)が策定したTIR101基準に従って認可された最初のもの1つです。

さらに、大手企業は研究開発活動に注力しており、市場セグメントの成長を後押しすると期待されています。例えば、2021年11月、Zealand PharmaとDEKA Research &Development Corp.は、先天性高インスリン血症(CHI)の治療にグルカゴンと併用できる輸液ポンプの開発を進める契約を締結しました。

このように、慢性疾患の有病率の上昇や技術の進歩などの前述の要因により、調査対象セグメントは調査期間中に健全な成長を示すことが期待されています。

北米は予測期間中に大きな市場シェアを占めると予測される

北米は、慢性疾患の急増、高いヘルスケア支出、慢性疾患に対する外科的治療の増加、研究開発支出の増加、同地域における主要企業の存在などにより、輸液ポンプ・付属品市場で大きな市場シェアを占めると予測されています。例えば、CDCが2022年7月に発表したデータによると、米国の帝王切開分娩率は前年の31.8%から2021年には32.1%に上昇しました。従って、帝王切開手術件数の増加は、血液やその他のドラッグデリバリー目的の輸液バッグや付属品の使用量を押し上げ、市場成長を促進すると予想されます。

さらに、輸血は健康な血液細胞を体内に取り込むのを助けるため、がんの治療において極めて重要です。さらに、特定の悪性腫瘍(特に消化器系のもの)は内出血を引き起こし、貧血や患者の状態を悪化させる。このように、がん患者の負担が大きいため、輸液ポンプや関連付属品が利用されると予想されます。例えば、カナダがん協会が発表した2022年の統計によると、2022年にカナダで診断されたがん患者は約233,900人です。したがって、がん患者の負担が大きいため、輸液ポンプ・付属品の需要が急増し、調査期間中の市場成長につながると予想されます。

さらに、北米地域における製品発売、契約、提携などの主要企業による戦略的活動の高まりが、予測期間中の市場成長を後押しすると予想されます。例えば、2022年11月、Medtronic plc社は、米国で最大7日間装着可能と表示された最初の輸液セットの1つである拡張輸液セットを発売しました。Medtronic Extended infusion setは、インスリン保存液の損失を減らし、インスリンの流れと安定性を維持するのに役立つ高度な材料を利用して、輸液セットの装着時間を2倍にします。同様に、2021年5月、スミスメディカルはIvenix, Inc.と提携し、米国のヘルスケアニーズに対応した輸液管理ソリューションの包括的なスイートを提供しています。

このように、慢性疾患の高い有病率や主要企業による戦略的な製品投入により、北米は調査期間中に大きな市場成長が見込まれます。

輸液ポンプ・付属品産業の概要

輸液ポンプ・付属品市場は、多数の世界およびローカル企業の存在により、競争が激しく断片化しています。多くの主要企業は、世界中で存在感を高めるために、製品の発売、提携、協力などの様々な戦略的活動に注力しています。輸液ポンプ・付属品市場における主な世界的企業には、Baxter International Inc.、Becton, Dickinson and Company、Braun SE、Eli Lilly and Company、F. Hoffmann-la Roche Ltd.、Fresenius(Fresenius Kabi)などがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 輸液ポンプの普及率の増加

- 慢性疾患の増加

- 市場抑制要因

- 輸液ポンプの高価格と輸液ポンプの安全性問題

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 製品タイプ別

- 輸液ポンプタイプ

- シリンジ型輸液ポンプ

- 容積式輸液ポンプ

- エラストマー輸液ポンプ

- インスリン注入ポンプ

- 経腸用輸液ポンプ

- その他の製品タイプ

- 付属品ー/消耗品

- 輸液ポンプタイプ

- 用途別

- 消化器

- 糖尿病管理

- 血液学

- その他の用途

- エンドユーザー別

- 病院

- 外来手術センター

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Baxter

- Becton, Dickinson and Company

- Braun SE

- Eli Lilly and Company

- Merit Medical

- Fresenius(Fresenius Kabi)

- ICU Medical Inc.

- Eitan Medical Ltd.

- Medtronic Inc.

- Nipro Corporation

- Option Care Health Inc.

- Terumo Corporation

第7章 市場機会と今後の動向

The Infusion Pumps And Accessories Market size is estimated at USD 11.46 billion in 2025, and is expected to reach USD 14.26 billion by 2030, at a CAGR of 4.47% during the forecast period (2025-2030).

The COVID-19 pandemic brought infusion pumps to the forefront since the demand for infusion pumps surged considerably during the COVID-19 lockdown, as the number of COVID-19 cases increased faster with growing hospital admissions. The demand for intravenous infusion therapies was higher during the first wave of the pandemic to provide essential nutrients to sepsis patients in the intensive care unit (ICU). For instance, an article published in May 2022 in PubMed stated that sepsis was present in 32.5% of total COVID-19 hospitalizations, of which 70.8% of sepsis were due to SARS-CoV-2 alone and 26.2% were due to both SARS-CoV-2 and non-SARS-CoV-2 infections. Infusion pumps were, therefore, frequently employed for IV fluid delivery for sepsis-affected patients, which further propelled the market expansion during the pandemic.

Thus, overall, the pandemic offered healthy growth for the market due to the increase in the patient pool in healthcare settings. However, the increase in the utilization of next-generation infusion systems, advancements in infusion bags, and the rise in chronic diseases, accidents, and blood transfusions are expected to bolster the market growth in the coming years.

The infusion pumps and accessories market is primarily driven by the rising incidence of chronic diseases, such as cancer and others, coupled with the rising adoption of infusion devices. Infusion pumps are widely used in chemotherapy, diabetes management, and many other applications. The rising prevalence of these diseases worldwide creates ample opportunities for the market to grow. Patients with cancer are more prone to hypovolemia, which is the absence of water in the extracellular space due to excessive fluid loss (such as vomiting and diarrhea) or insufficient fluid intake.

An increase in cancer cases is expected to raise the demand for pressure infusion bags, bolstering market growth. For instance, according to the American Cancer Society 2023 Cancer Statistics, the new cancer cases are estimated to be 1.93 million in the United States in 2023. This estimation includes 1.01 million males and 948,000 cases of females. The high burden of cancer is augmenting the demand for infusion pumps and accessories, thereby boosting market growth over the forecast period.

Moreover, increased clinical research activities involving infusion-related drug delivery are expected to bolster market growth over the forecast period. For instance, in November 2022, TriSalus Life Sciences, Inc., an oncology therapeutics company, publicized the additional information regarding its ongoing Pressure-Enabled Regional Immuno-Oncology ('PERIO 01') and ('PERIO 02') clinical studies for primary and metastatic liver tumors. The TriSalus platform comprises the TriNav Infusion System and SD-101, a class C toll-like receptor 9 (TLR9) agonist. TriNav is an FDA-cleared device designed to administer established and emerging therapeutics.

Additionally, technological advancements in device technology and innovative product launches by the key players are likely to fuel market growth. For instance, in February 2021, United Therapeutics launched the Remunity Pump for remodeling drug delivery, which helps to improve the lives of patients with pulmonary arterial hypertension (PAH). Similarly, in February 2021, Mindray Medical launched BeneFusion E series-ESP, EVP, and EDS, new infusion systems for expanding its product portfolio.

Hence, owing to the rise in chronic diseases and rapid advancements in infusion pumps coupled with product launches by the key players, the market is anticipated to grow significantly over the forecast period. However, the higher cost of infusion pumps and the associated safety issues are expected to restrain the market growth over the forecast period.

Infusion Pumps and Accessories Market Trends

Volumetric Infusion Pumps Segment Is Expected to Witness a Significant Growth Over the Forecast Period

Volumetric infusion pumps have many applications in disease management and parenteral nutrition. The safety, accuracy, and simplicity of volumetric infusion pumps in treating many therapeutic areas contribute to the high demand for these pumps. The volumetric infusion pump segment is expected to witness significant growth owing to the rise in blood and drug transfusion cases and the increase in strategic product launches by the key players.

The increasing number of injuries and trauma cases is expected to raise the demand for drug infusions, which is anticipated to drive the growth of the segment over the study period. For instance, the Road Safety Observatory report published in February 2022 stated that the number of injury accidents recorded by police forces in France was 3,728 in January 2022, which was higher than that of 2021 (3,508). The rising burden of road accidents leads to blood loss and creates the need for emergency transfusion, further projected to boost the segment growth over the forecast period.

Furthermore, the advancements and the emergence of innovative volumetric pumps, along with the increase in regulatory approvals, are expected to bolster segment growth. For instance, in March 2022, Fresenius Kabi received regulatory clearance from the FDA for its wireless Agilia connect infusion system, which includes the Agilia volumetric pump and the Agilia syringe pump with the vigilant software suite Vigilant Master Med technology. The Agilia Connect volumetric pump and syringe pump is one of the first to be cleared by following TIR101 standards developed by the Association for the Advancement of Medical Instrumentation (AAMI) in 2021.

Additionally, the major players are focusing on research and development activities, which is expected to boost the growth of the market segment. For instance, in November 2021, Zealand Pharma and DEKA Research & Development Corp. signed an agreement to advance the development of an infusion pump that can be used with glucagon for the treatment of congenital hyperinsulinism (CHI).

Thus, due to the aforementioned factors, such as the rising prevalence of chronic diseases and technological advancement, the studied segment is expected to witness healthy growth over the study period.

North America is Anticipated to Hold a Significant Market Share Over the Forecast Period

North America is expected to hold a significant market share in the infusion pumps and accessories market owing to the surge in chronic disorders, high healthcare expenditures, the increasing surgical treatments for chronic diseases, the increased R&D expenditure, and the presence of key players in the region. For instance, according to the data published by the CDC in July 2022, the cesarean delivery rate in the United States increased to 32.1% in 2021 from 31.8% in the previous year. Thus, the rising number of cesarean section surgeries is expected to boost the usage of infusion bags and accessories for blood and other drug delivery purposes, fueling market growth.

Moreover, blood transfusions are crucial in the treatment of cancer because they assist the body in getting healthy blood cells. Additionally, certain malignancies (particularly those of the digestive system) result in internal bleeding, which worsens anemia and the patient's condition. Thus, a high burden of cancer cases is expected to utilize infusion pumps and related accessories. For instance, according to the 2022 statistics published by the Canadian Cancer Society, about 233,900 cancer cases were diagnosed in Canada in 2022. Therefore, the high burden of cancer cases is expected to surge the demand for infusion pumps and accessories, leading to market growth over the study period.

Furthermore, the rising strategic activities by the key players, such as product launches, agreements, and collaboration in the North American region, are expected to bolster market growth over the forecast period. For instance, in November 2022, Medtronic plc launched an extended infusion set, one of the first infusion sets labeled for up to 7-day wear in the United States. The Medtronic Extended infusion set utilizes advanced materials that help reduce insulin preservative loss and maintain insulin flow and stability to double the wear time of an infusion set. Similarly, in May 2021, Smiths Medical partnered with Ivenix, Inc. to offer a comprehensive suite of infusion management solutions for healthcare needs in the United States.

Thus, due to the high prevalence of chronic diseases and strategic product launches by the key players, North America is expected to witness significant market growth over the study period.

Infusion Pumps and Accessories Industry Overview

The infusion pumps and accessories market is highly competitive and fragmented due to the presence of a large number of global and local players. Many key players are concentrating on various strategic activities like product launches, partnerships and collaborations to increase their presence across the globe. Some of the key global players in the infusion pumps and accessories market are Baxter International Inc., Becton, Dickinson and Company, Braun SE, Eli Lilly and Company, F. Hoffmann-la Roche Ltd, and Fresenius (Fresenius Kabi) among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Adoption Rate of Infusion Pumps

- 4.2.2 Rising Incidences of Chronic Disease

- 4.3 Market Restraints

- 4.3.1 High Price of Infusion Pumps and Safety Issues Associated with Infusion Pumps

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Product Type

- 5.1.1 Infusion Pump Types

- 5.1.1.1 Syringe Infusion Pumps

- 5.1.1.2 Volumetric Infusion Pumps

- 5.1.1.3 Elastomeric Infusion Pumps

- 5.1.1.4 Insulin Infusion Pumps

- 5.1.1.5 Enteral Infusion Pumps

- 5.1.1.6 Other Product Types

- 5.1.2 Accessories/Disposables

- 5.1.1 Infusion Pump Types

- 5.2 By Application

- 5.2.1 Gastroenterology

- 5.2.2 Diabetes Management

- 5.2.3 Hematology

- 5.2.4 Other Applications

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgery Center

- 5.3.3 Other End Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Baxter

- 6.1.2 Becton, Dickinson and Company

- 6.1.3 Braun SE

- 6.1.4 Eli Lilly and Company

- 6.1.5 Merit Medical

- 6.1.6 Fresenius (Fresenius Kabi)

- 6.1.7 ICU Medical Inc.

- 6.1.8 Eitan Medical Ltd.

- 6.1.9 Medtronic Inc.

- 6.1.10 Nipro Corporation

- 6.1.11 Option Care Health Inc.

- 6.1.12 Terumo Corporation