|

市場調査レポート

商品コード

1852027

糖尿病薬:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Diabetes Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 糖尿病薬:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年08月06日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

概要

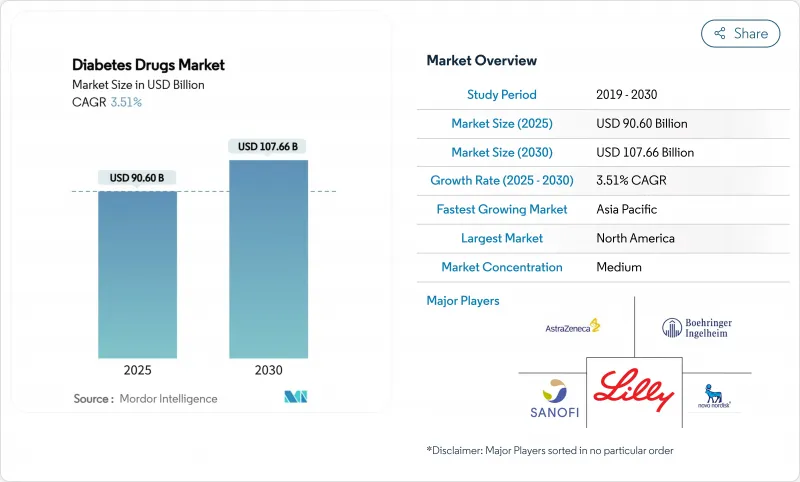

糖尿病薬市場規模は2025年に906億米ドルと推定され、予測期間(2025-2030年)のCAGRは3.51%で、2030年には1,076億6,000万米ドルに達すると予測されます。

持続的な成長の背景には、世界的な糖尿病負担の加速化、診断の早期化、血糖コントロールと体重管理効果を併せ持つ革新的治療法の急速な普及があります。インスリンは依然として不可欠であるが、需要はGLP-1受容体作動薬やその他の非インスリン注射剤に傾きつつあります。経口ペプチド技術、バイオシミラー基礎インスリン、デジタル化されたケアモデルは、コストを抑えつつ患者アクセスを拡大しています。競争環境は激化しており、既存企業は製造とデジタルエコシステムの規模を拡大し、価値主導の環境下でシェアを守ろうとしています。

世界の糖尿病薬市場の動向と洞察

世界的な糖尿病有病率の上昇と早期診断

2024年には8億2,800万人以上の成人が糖尿病を患い、1990年の4倍となります。低所得地域における早期スクリーニング・プログラムは、治療対象者を拡大し、治療期間を延長しています。GLP-1アゴニストの早期使用を支持するWHOの新しいガイダンスは、第一選択治療への高度な注射薬の統合を強化するものです。肥満と糖尿病の重複は、多くのGLP-1製剤が二重適応を持つようになったことから、需要をさらに増大させています。このようなシフトが、糖尿病薬市場の長期的な数量成長を支えています。

ヘルスケア支出の増加

糖尿病に対する医薬品支出は2023年に19%上昇し、医療全体のインフレを上回る。糖尿病市場調査によると、合併症の発生率が低下することで目先の支出が相殺されるため、支払者はより高額な治療薬に資金を提供しています。雇用主の医療保険制度は、利用管理を強化しながらも価値の高い医薬品へのアクセスを維持するという、大きな圧力に直面しています。このような支出の勢いは、単価が精査されるようになっても価格実現を維持し、臨床的・経済的リターンが明確な革新的製品に利益をもたらしています。

GLP-1関連膵炎に関する安全性への懸念

膵炎の報告は、ファーマコビジランスの強化と保守的な患者選択を促しています。膵炎の発生率は依然として低いもの、処方者による注意喚起が高リスク群での服用を遅らせ、GLP-1の急激な売上増加を抑制する可能性があります。メーカー各社は、ベネフィット・リスク・プロファイルを保護するための教育や市販後調査を支援しています。

セグメント分析

2024年の糖尿病薬市場におけるインスリンのシェアは55%を維持し、1型および進行2型の管理におけるインスリンの中心的役割が強調されました。しかし、GLP-1受容体作動薬のCAGRは4.5%で拡大しており、これは従来の血糖コントロール以外にも処方の幅を広げる減量効果に後押しされています。GLP-1製剤の市場規模は2030年までに1,500億米ドルに達すると予測されており、これはGLP-1製剤の二重適応の魅力を反映しています。経口SGLT-2阻害薬は、糖尿病治療市場における注射薬の貴重な補助薬または代替薬として位置づけられる臓器保護データに支えられ、引き続き支持を集めています。

このセグメントにおける競合の動きは激しいです。現在、ノボ・ノルディスクとイーライリリーがほぼ全シェアを占めていると推定されるが、デュアルアゴニストとトリプルアゴニストのパイプラインが新たな競争を約束しています。インスリンデグルデク/リラグルチドペンのような合剤は、投与方法の革新がいかにアドヒアランスの利点を確保し、製品ライフサイクルを延長できるかを示すものです。

地域分析

北米が2024年の売上高に42%寄与し、リーダーシップを維持。幅広い保険適用範囲、強力な専門医療インフラ、GLP-1製剤の早期導入がこの地域の優位性を支えています。インスリンの低価格化に関する法律も、価格拡大を抑制しつつも、患者のコスト負担を軽減することで需要を刺激しています。雇用主はGLP-1の成長を管理するために事前承認プロトコルを改良しているが、持続的な臨床的価値が幅広いアクセスを維持しています。

アジア太平洋地域は最も急成長している地域で、2025~2030年のCAGRは5.3%と予測されています。都市化の進展、食生活の変化、高齢化が2型糖尿病有病率の急上昇を促しています。中国とインドでは保険給付の拡大により、ブランドインスリン製剤や新規注射剤へのアクセスが拡大しています。デジタルヘルスツールやモバイルイルプラットフォームがケア提供のギャップを埋め、遠隔地の患者のアドヒアランスと継続性を支えています。そのため、アジア太平洋地域の糖尿病薬市場規模は、2030年までに欧米市場とのギャップの一部を埋めることが予想されます。

欧州は、強固なバイオシミラーフレームワークと、費用対効果を精査する価値評価機関によって形成された、成熟しつつも進化しつつある状況を示しています。バイオシミラー医薬品の高い普及率がオリジネーターの価格設定を圧迫しているが、配合剤や先進的なGLP-1製剤の普及が収益の底堅さを支えています。中東とラテンアメリカの新興市場は、糖尿病有病率の上昇に対処するために政府が資金を投入し、多国籍企業が製造と販売を現地化することで、新たなビジネスチャンスをもたらしています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 世界の糖尿病有病率の上昇と早期診断

- 医療費の増加

- アドヒアランスを高める合剤ペンの台頭

- 革新的な薬効分類に対する強力なアウトカムベースの臨床エビデンスとガイドラインの承認

- バイオシミラー基礎インスリンの採用拡大

- デジタル治療バンドル(アプリ+医薬品)が処方更新を促進する

- 市場抑制要因

- GLP-1関連膵炎に関する安全性の懸念

- インスリンアナログ製剤の公的価格キャップ

- 普及を阻むコールドチェーン・インフラストラクチャーのギャップi

- 新興国における医薬品の値ごろ感

- バリュー/サプライチェーン分析

- 規制の見通し

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 薬物別

- 経口糖尿病薬

- ビグアナイド薬

- メトホルミン

- αーグルコシダーゼ阻害薬

- ドパミンD2受容体作動薬

- シクロセット(ブロモクリプチン)

- SGLT-2阻害薬

- インボカーナ(カナグリフロジン)

- ジャーディアンス(エンパグリフロジン)

- ファルキシガ/フォルキシガ(ダパグリフロジン)

- スグラット(イプラグリフロジン)

- DPP-4阻害薬

- ジャヌビア(シタグリプチン)

- オングリザ(サキサグリプチン)

- トラジェンタ(リナグリプチン)

- ビピディア/ネシーナ(アログリプチン)

- ガルバス(ビルダグリプチン)

- スルホニル尿素

- メグリチニド

- インスリン製剤

- 基礎/長時間作用型

- ランタス(インスリングラルギン)

- レベミル(インスリンデテミル)

- トウジオ(インスリングラルギン)

- トレシーバ(インスリンデグルデク)

- バサグラ(インスリングラルギン)

- ボーラス/速効型

- ノボラピッド/ノボログ(インスリンアスパルト)

- ヒューマログ(インスリンリスプロ)

- アピドラ(インスリングルリジン)

- 従来のヒトインスリン

- ノボリン/アクトラピッド/インスラタード

- ヒュムリン

- インスマン

- バイオシミラーインスリン

- インスリングラルギンバイオシミラー

- ヒトインスリンバイオシミラー

- 非インスリン注射剤

- GLP-1受容体作動薬

- ビクトーザ(リラグルチド)

- バイエッタ(エキセナチド)

- ビデュロン(エキセナチド)

- トルリシティ(デュラグルチド)

- リクスミア(リクセナチド)

- アミリンアナログ

- シムリン(プラムリンチド)

- 配合剤

- 併用インスリン製剤

- ノボミックス(二相性インスリンアスパルト)

- ライゾデグ(インスリンデグルデク+アスパルト)

- ゾルトファイ(インスリンデグルデク+リラグルチド)

- 経口配合剤

- ジャヌメット(シタグリプチン+メトホルミン)

- 経口糖尿病薬

- 投与経路別

- 経口

- 皮下

- 静脈内投与

- 流通チャネル別

- オンライン薬局

- オフライン(病院・小売薬局)

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 中東

- GCC

- 南アフリカ

- その他中東

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 市場指標

- 1型糖尿病人口

- 2型糖尿病人口

第7章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 会社概要

- Novo Nordisk

- Eli Lilly and Company

- Sanofi

- AstraZeneca

- Merck & Co.

- Bristol Myers Squibb

- Boehringer Ingelheim

- Pfizer

- Johnson & Johnson(Janssen)

- Novartis

- Biocon

- Teva Pharmaceuticals

- Mylan(Viatris)

- Hualan Biologicals

- Tonghua Dongbao

- Wockhardt

- Gan & Lee Pharmaceuticals

- Hanmi Pharmaceutical

- Mitsubishi Tanabe Pharma

- Sun Pharma

第8章 市場機会と将来の展望

- ホワイトスペースとアンメットニーズ評価