|

|

市場調査レポート

商品コード

1441592

自動車内装:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Automotive Interior - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 自動車内装:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

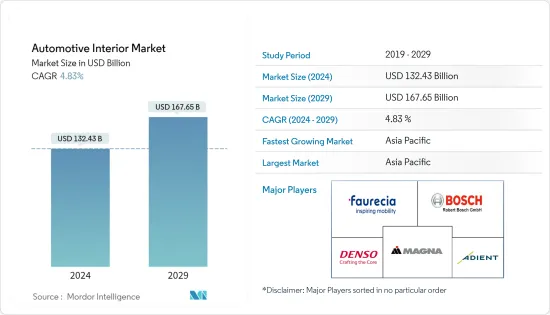

自動車内装市場規模は2024年に1,324億3,000万米ドルと推定され、2029年までに1,676億5,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に4.83%のCAGRで成長します。

新型コロナウイルス感染症(COVID-19)のパンデミックは、車両生産への影響により、自動車内装市場の成長を妨げています。ただし、2020年以降の自動車生産の着実な回復は、今後数年間でこの市場の発展を支えるでしょう。たとえば、マレリは、2020年の最初の2四半期にCOVID-19により生産全体に重大な影響を及ぼしました。同社は、2020年3月に始まった全国的なロックダウンの後、国内の施設を約2週間閉鎖しなければなりませんでした。、同社は必要な措置を講じた上で2020年4月に営業を再開しました。

車載インフォテインメントシステムに続くいくつかの技術的優位性があり、自動車内装市場の成長を大きく後押ししてきました。例えば:

主なハイライト

- 車載インフォテインメントシステムにスマートフォン機能が搭載されるケースが増えています。北米と欧州では、成人の90%以上が携帯電話を通じてインターネットにアクセスしており、これは他の地域の中でも最も高い水準にあります。携帯電話の利用が増えるにつれ、同じ目的で車内にスマートフォンを置く人も増えてきました。

- メーカーはタッチスクリーンのインフォテインメントシステムを導入しており、これにより社内の客室体験が完全に変わりました。現在、タッチスクリーンインフォテインメントシステムにいくつかの新たな進歩が見られ、メーカーは実際に画面に触れずに指示に従う予測タッチスクリーン機能を導入しています。これにより 促進要因の快適性と操作性が向上し、勢いが増しました。

消費者の安全性への懸念の高まり、技術の進歩の高まり、高級車の需要の急増が市場の成長を促進すると予想されます。軽量で安全な車両に対する政府の支援により、市場の成長が急速に進む可能性があります。

自動車内装材市場では、アジア太平洋が消費量で最大のシェアを占めました。日本と中国がこの地域の増大する需要を主に支えることになります。さらに、インドにおける製品需要の見通しの改善も、潜在的な成長要因となります。自動車メーカーの大規模なOEM基盤を持つ欧州も、内装材市場での受注をさらに増やすと思われます。

自動車内装市場の動向

自動車内装市場を独占すると予想されるインフォテインメントシステム

インフォテインメントシステムは、自動車内装市場で最大のセグメントです。以前は、自動車に提供されるインフォテイメントスクリーンは1つだけでしたが、技術の進歩に伴い、インフォテイメントスクリーンの数と寸法も増加しています。

そのため、インフォテインメントスクリーンはすべての自動車メーカーにとって主な焦点となっており、これらのスクリーンには最新のテクノロジー機能が満載されています。2022年にメルセデスベンツがインド市場向けにSクラスフリート、つまりS350dおよびS450を発売したためです。 150台の新車を輸入。車内のインフォテインメントシステムは消費者を驚かせます。 64色のアンビエントライトと後部座席のインフォテインメントスクリーンを備えたこの車は、究極の快適さと高級感を提供します。

自動車メーカーは、顧客に最高の機能とテクノロジーを提供するために、インフォテインメントシステムを常にアップグレードしています。最近の発売とモデルの一部は次のとおりです。

- ジープはまた、2022年に、ジープ・グランドチェロキー2022年モデルの後部座席に2つのインフォテインメント・スクリーンを搭載し、前席乗員が 促進要因のナビゲーション・システムと対話できるようにダッシュボードにスクリーンを搭載する可能性があると提案しました。

- 2022年、トヨタは3.5リッターV6ツインターボハイブリッドエンジンを搭載した新セグメントのタンドラTRDトラックを発売しました。消費者の観点から見ると、ピックアップトラックのインテリアは有望に思えます。自然光を変化させずに明るさをランダムに変化させるインダッシュインフォテインメントシステムを搭載。

- 2022年、リビアンは重要な消費者のあらゆる要件を考慮して、新しい電動ピックアップトラックを発売しました。この新発売のピックアップトラックには、ダッシュインフォテインメントシステムボードに装飾されたアッシュウッドが装備されています。このシステムは、車のHVAC通気口のすぐ上に組み込まれた12.3枚の横長スクリーンで構成されています。

自動車がより多くのコネクテッド機能を搭載するにつれて、通信およびテクノロジー企業は主要な自動車企業と提携して、顧客に最適な接続およびインフォテインメントソリューションを開発しています。

上記のすべての要因と車載インフォテインメントシステムの開発を考慮すると、自動車内装市場は予測期間に繁栄すると予想されます。

アジア太平洋が自動車内装市場をリード

アジア太平洋市場は小型/経済車セグメントによって牽引されており、内装部品の採用率が高くなります。トヨタ、ホンダ、ヒュンダイなど、この地域の大手自動車メーカーは、先進的なシートシステム、照明、エレクトロニクス、さまざまな安全システムの利点を活用し、自社の車種全体に不可欠な機能となっています。日本、中国、インドなどの主要経済国での電気自動車の台頭が市場価値をさらに支えています。

2022年4月、中国の乗用車生産は99万6,000台に達し、販売台数は96万5,000台に達しました。これは、前年比で生産量と売上高がそれぞれ41.9%、43.4%減少したことを示しています。 2022年の1月から4月までの乗用車生産台数は前年比2.6%減の64億9,400万台となった。

中国では、地元企業が協力して最高のインテリア製品を生産しています。たとえば、BAIC Yunxiang AutomobileはADAYOと協力して車両インフォテインメントシステムを開発しました。このパートナーシップは、北汽銀翔の新しいプラットフォームを構築し、インテリジェントな車両製造のためのプラットフォーム生産モードの再構築に役立ちます。中国企業は、市場に成長をもたらすという新たなビジョンを持って市場に参入しています。たとえば、2021年11月、中国の大手自動車内装部品サプライヤーである延豊汽車内装(YFAI)は、TCLおよびその子会社であるTCL CSOTと共同開発した業界初のパネルアンダーパネルオンボードインテリジェントスクリーンカメラを導入しました。

高級インテリア、快適性、ヘッドアップディスプレイやナビゲーションシステムなどの新しく革新的な機能に対する需要が、安全基準を満たすことへの注目の高まりとともに、この地域の市場を牽引しています。中国、日本、インド、韓国などのこの地域の主要国では、新しい技術が急速に導入されることが予想されます。中国はその高い自動車生産能力により、アジア太平洋地域の市場成長に大きく貢献すると期待されています。

アジア太平洋地域では、各国の補助金や税制優遇などの政府の取り組みにより、自動車OEMが地域の製造工場を建設するよう誘致されています。

自動車内装業界の概要

主要な自動車内装市場参入企業は、Continental AG、Magna International Inc.、Denso Corporation、Faurecia、Adientなどです。自動車内装市場は、競争上の優位性を獲得するための重要な製品メーカーによる集中的な研究開発活動、新製品開発、買収などのさまざまな戦略により、今後数年間で競合が予想されます。例えば、

- 2022年5月、自動車技術のLear Corporationは、シートヒーター、アクティブクーリング、シートセンサー、その他の内装部品のサプライヤーであるIG Bauerhinを買収すると発表しました。

- 2021年 9月に、Adientはカルディオンの使用を開始します。コベストロによると、コベストロのCO2技術を使用して製造されたポリオールは、2021年11月に熱硬化成型ポリウレタンフォームを製造するための持続可能な原料として使用されます。これらのフォームは、Adientの最先端の自動車シートシステムのクッションとして使用されています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション(市場規模、金額)

- 車種別

- 乗用車

- 商用車

- コンポーネントタイプ別

- インストルメントパネル

- インフォテイメントシステム

- インテリア照明

- ボディパネル

- その他のコンポーネントタイプ

- 地域別

- 北米

- 米国

- カナダ

- 北米のその他の地域

- 欧州

- ドイツ

- 英国

- フランス

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東とアフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- その他中東およびアフリカ

- 北米

第6章 競合情勢

- ベンダーの市場シェア

- 企業プロファイル

- Adient PLC

- Grupo Antolin

- Panasonic Corp.

- Faurecia

- Magna International

- Toyota Boshuku Corporation

- Hyundai Mobis Co.

- Pioneer Corporation

- JVCKENWOOD Corporation

- Robert Bosch GmbH

第7章 市場機会と将来の動向

The Automotive Interior Market size is estimated at USD 132.43 billion in 2024, and is expected to reach USD 167.65 billion by 2029, growing at a CAGR of 4.83% during the forecast period (2024-2029).

The COVID-19 pandemic has hindered the growth of the automotive interior market due to its impact on vehicle production. However, a steady recovery post-2020 in vehicle production will support the development of this market in the coming years. For instance, Marelli had a significant impact on COVID-19 on its overall production in the first two quarters of 2020. The company had to shut its facilities for around two weeks in the country after the nationwide lockdown, which started in March 2020. However, the company resumed its operations in April 2020 with the necessary measures.

There have been several technological dominance followed in-vehicle infotainment systems, which has provided a significant boost to the automotive interiors market growth. For instance:

Key Highlights

- There is a rise in smartphone functions built into in-vehicle infotainment systems. In North America and Europe, over 90% of adults have access to the internet through their mobile phones, which is also among the highest among other regions. As mobile phone use has risen, smartphones for the same purposes in their cars have also increased.

- Manufacturers are introducing a touchscreen infotainment system, which has completely changed the in-house cabin experience. Today, after several new advancements seen by the touch screen infotainment system, manufacturers have introduced a predictive touchscreen feature that shall follow the instruction without actually touching the screen. This has improved drivers' comfort and ease, thus gaining momentum.

Increasing consumer safety concerns, rising technological advancements, and a surge in demand for luxurious vehicles are expected to boost the market growth. Government support for lightweight and safe vehicles will likely surge the market growth.

Asia-Pacific accounted for the largest share in terms of consumption in the automotive interior materials market. Japan and China will be the primary support for the region's increasing demand. Moreover, an improved outlook for product demand in India is another potential factor for growth. With its sizeable OEM base of automobile manufacturers, Europe will also add to the order in the interior material market.

Automotive Interior Market Trends

Infotainment System Expected to Dominate the Automotive Interiors Market

The infotainment system is the largest segment in the automotive interiors market. Earlier, cars were offered only one infotainment screen, but as technology advances, the number and dimension of infotainment screens are also increasing.

As such, the infotainment screens have become the main focal point for every automaker, and these screens are packed with the latest technology capabilities, as In 2022, Mercedes-Benz launched its S-class fleet for the Indian market, namely, S350d and S450 importing 150 new cars. The infotainment system in the vehicle amazes the consumer; with 64-colour ambient lighting and rear seat infotainment screens, the car offers ultimate comfort and luxury.

Automakers constantly upgrade their infotainment systems to provide their customers with the best features and technologies. Some of the recent launches and models are:

- In 2022, Jeep also proposed that Jeep Grand Cherokee 2022 model may have two rear seat infotainment screens with a screen in the dashboard for the front-seat passenger to interact with the driver's navigation system.

- In 2022, Toyota launched its new segment Tundra TRD truck, powered by the 3.5-liter V6 twin-turbo hybrid engine. The pickup truck's interior seems promising from a consumer's point of view. It is equipped with the in-dash infotainment system, which changes brightness randomly without a change in natural lighting.

- In 2022, Rivian launched its new electric pickup truck considering all the requirements of critical consumers. This newly launched pickup truck is equipped with decorated ash wood on the dash infotainment system board. The system comprises of 12.3 landscape-oriented screen inbuilt placed just above the HVAC vents of the car.

As the cars come with more connected features, the telecom and technology players are partnering with major automotive players to develop the best connectivity and infotainment solutions for the customers.

Considering all the factors above and the development of in-vehicle infotainment systems, the automotive interiors market is expected to witness prosperity in the forecast period.

Asia-Pacific is Leading the Automotive Interiors Market

The Asian-Pacific market is driven by the small/economy car segment, which accounts for higher adoption of interior components. Leading automakers in this region, such as Toyota, Honda, and Hyundai, are embracing the advantages of advanced seating systems, lighting, electronics, and various safety systems, making them essential features across their car models. The emergence of electric vehicles in major economies, including Japan, China, and India, further supports the market value.

In April 2022, Chinese passenger car production reached 996,000 units, with sales registering 965,000 units. This accounts for the downfall of 41.9% and 43.4% respectively in production and sales compared to the previous year. In 2022, from January to April, passenger car production decreased by 2.6% year-on-year, registering 6,494 million units.

In China, local players are collaborating to produce the best interior products. For instance, BAIC Yunxiang Automobile Co. Ltd collaborated with ADAYO to develop vehicle infotainment systems. This partnership will build new platforms for BAIC Yinxiang and helps to restructure the platform production mode for intelligent vehicle manufacturing. Chinese players are debuting in the market with a new vision to provide growth to the market. For instance, In November 2021, China's leading automotive supplier for interior components, Yanfeng Automotive Interiors (YFAI), introduced an industry-first camera under panel onboard intelligent screen, which is co-developed with TCL and its subsidiary TCL CSOT.

The demand for premium interiors, comfort, and new and innovative features, like head-up displays and navigation systems, along with the growing focus on sufficing the safety standards, is driving the market in the region. Major countries in this region, such as China, Japan, India, and South Korea, are anticipated to witness the rapid adoption of new technologies. Due to its high vehicle production capacity, China is expected to contribute to Asia-Pacific's market growth significantly.

In Asia-Pacific, government initiatives, such as subsidies and tax concessions, across various countries are attracting automotive OEMs to build their regional manufacturing plants.

Automotive Interior Industry Overview

Key automotive interior market participants are Continental AG, Magna International Inc., Denso Corporation, Faurecia, Adient, and Others. The automotive interiors market is likely to expect competition in the coming years, owing to various strategies, such as focused research and development activities, new product developments, acquisitions, etc., by significant product manufacturers to gain a competitive advantage. For instance,

- In May 2022, Lear Corporation, an automotive technology, announced that it is acquiring I.G. Bauerhin, a seat heating supplier, active cooling, seat sensor, and other interior components.

- In September 2021, Adient will begin using cardyon; a polyol made using Covestro's CO2 technology, as a sustainable feedstock for the production of hot cure molded polyurethane foam in November 2021, according to Covestro. These foams are used as cushioning in Adient's cutting-edge automotive seating systems.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value USD Billlion)

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Commercial Vehicles

- 5.2 By Component Type

- 5.2.1 Instrument Panels

- 5.2.2 Infotainment Systems

- 5.2.3 Interior Lighting

- 5.2.4 Body Panels

- 5.2.5 Other Component Types

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.1 North America

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Adient PLC

- 6.2.2 Grupo Antolin

- 6.2.3 Panasonic Corp.

- 6.2.4 Faurecia

- 6.2.5 Magna International

- 6.2.6 Toyota Boshuku Corporation

- 6.2.7 Hyundai Mobis Co.

- 6.2.8 Pioneer Corporation

- 6.2.9 JVCKENWOOD Corporation

- 6.2.10 Robert Bosch GmbH