|

市場調査レポート

商品コード

1693990

英国のドッグフード:市場シェア分析、産業動向、成長予測(2025~2030年)UK Dog Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国のドッグフード:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 265 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

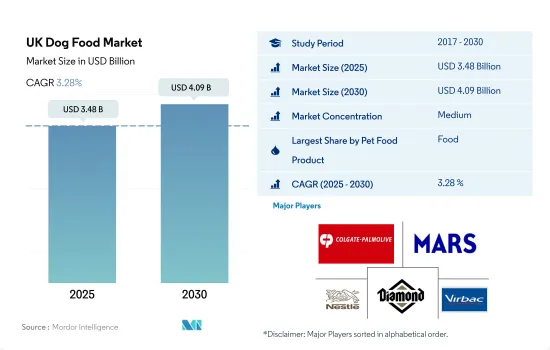

英国のドッグフード市場規模は2025年に34億8,000万米ドルと推定・予測され、2030年には40億9,000万米ドルに達し、予測期間(2025~2030年)のCAGRは3.28%で成長すると予測されています。

犬種の大きさや年齢に関係なく一次栄養源となるため、製品タイプ別ではフード部門が圧倒的に多い

- 英国のドッグフード市場は着実な成長を遂げており、2017~2021年にかけて約13.5%増加しています。このような市場の増加動向は、主に同国における愛犬の飼育数の増加によるもので、2022年時点で1,290万頭に達しています。ペットの人間化の進展が市場成長に寄与しています。

- フードセグメントは市場を独占し、2022年には68.4%を占めました。犬種の大きさや年齢に関係なく、同国のほとんどのペットオーナーにとってフードは主食であるためです。同国のドッグフード市場は、予測期間中にCAGR 2.7%を記録すると予測されています。

- 英国では犬用スナックが第2位の市場シェアを占め、2022年には市場の15.0%を占めます。犬は他のペットよりもスナックを好みます。これらのスナックは、しつけ、歯の健康維持、ご褒美の提供など、複数の目的を果たします。犬用スナック市場は予測期間中にCAGR 2.0%を記録すると予測されています。

- 犬の動物用食事は2022年に市場の12.8%を占めました。これらの食事は、尿路疾患、腎不全、消化過敏症など、ペットの特定の健康状態に対処するために特別に配合されます。犬用動物用飼料は、予測期間中にCAGR 3.7%を示すと予測されています。

- 犬の栄養補助食品またはサプリメントは、2022年の市場金額の3.8%を占めました。これらのペット用サプリメントは、全体的な健康と幸福をサポートするためにペットに与えられることが多いです。犬用サプリメント市場は予測期間中にCAGR 9.3%を記録すると予測されています。

- ペット数の増加動向と、幅広い市販のペット用製品によって提供される様々なメリットが、予測期間中の市場を牽引すると予測されます。

英国のドッグフード市場動向

アニマルシェルターやレスキュー団体からの採用、コンパニオンシップの提供が犬の飼育数を増加させている

- 英国では、犬はペットの親が採用する最も重要なペットの一つであり、2022年には33.8%を占めます。この高いシェアは、同国が犬への感謝と動物愛護の文化を強く持っているためで、同国の人々は犬の世話を楽しむ傾向が強く、可処分所得が高いことが描かれています。ラブラドール・レトリーバーは2022年に最も飼われた犬種で、4万頭が登録されました。

- 同国の犬の飼育数は2019~2022年の間に44.4%増加しました。COVID-19のパンデミックの間、動物保護施設やレスキュー団体からの犬の養子縁組が増加しました。より多くの人々が家で過ごすようになったため、交友関係を求める声が高まり、多くの人々がこれを犬を飼う機会と捉えました。国内のペット・ペアレントが犬を飼うようになり、2022年には犬の飼育世帯が1,000万世帯に達し、約34%がペットとして犬を飼っていることになります。2021~2022年にかけてペットの飼育率が1%上昇したのは、犬が忠誠心や愛情を与え、パンデミックのような困難な状況でもサポートしてくれるからです。

- 国内の犬の飼育数が増えたことで、養子縁組や里親探しのプログラムも増えています。その結果、企業はこの産業で新しいアイデアを模索する多くの機会を得ています。例えば、英国では、企業がペットの親に有給の「肉球休暇」を提供しています。そのため、ペットの親が複数の犬を飼うことを奨励しています。そのため、ペットの飼育数の増加、ペットの所有率の上昇、交友関係の提供といったメリットが、予測期間中の同国における犬の飼育数の増加に貢献すると予想されます。

ペットフード製品のプレミアム化の進展と高品質の天然ペットフードへの需要の高まりが、英国における犬の支出を促進しています。

- 英国では犬が最も人気のあるペットであり、ペットの飼い主は他のペットフードと比較してドッグフードに多くのお金を費やします。同国におけるペット用ドッグフードの支出は増加傾向にあり、2019~2022年の間に23.7%増加しています。このようなペット犬支出全体の増加は、同国におけるペット犬の飼育数が増加し、2019年の900万頭から2022年には1,300万頭に増加したことに起因しています。さらに、ペットの人間化の進展により、自然食や穀物不使用のペットフードなどのプレミアムドッグフード製品に対する需要が増加しています。

- 2019~2022年にかけての犬と猫に対する支出の増加は、国内の犬の飼育数が1,300万人、猫の人口が2022年時点で1,270万人と同程度であるため、ほぼ等しいです。しかし、ペットオーナーが犬にかける平均支出額は、猫にかける平均支出額より約9.7%高いです。これは主に、猫に比べて犬のサイズが大きく、より多くの量の餌を必要とするためです。さらに、ペットの飼い主はプレミアム犬用ブランド、特に犬のニーズに基づいた特別な栄養を提供するブランドへとシフトしています。

- 2022年の金融危機にもかかわらず、英国では58%という多くのペットオーナーが愛犬の誕生日プレゼントやクリスマスプレゼントを選んでおり、ペットの人間化の傾向が強まっていることを示しています。パンデミックの影響によりeコマースの人気が高まっているが、同国では依然としてスーパーマーケットがペットフードの購入に好ましい流通チャネルとなっています。高品質のペットフードの利点に対する意識の高まりとペットフードのプレミアム化は、今後も英国でのペット支出を促進すると予想されます。

英国のドッグフード産業概要

英国のドッグフード市場は適度に統合されており、上位5社で42.20%を占めています。この市場の主要企業は、Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)、Mars Incorporated、Nestle(Purina)、Schell & Kampeter Inc.(Diamond Pet Foods)、Virbacです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- ペット数

- ペット支出

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- ペットフード製品

- フード

- サブ製品別

- ドライペットフード

- サブ製品別ドライペットフード

- キブル

- その他のドライフード

- ウェットペットフード

- ペット用栄養補助食品サプリメント

- サブ製品別

- ミルクバイオアクティブ

- オメガ3脂肪酸

- プロバイオティクス

- タンパク質とペプチド

- ビタミンとミネラル

- その他の栄養補助食品

- ペット用スナック

- サブ製品別

- カリカリスナック

- デンタルトリーツ

- フリーズドライ&ジャーキートリーツ

- ソフト&モチートリーツ

- その他のスナック

- ペット用動物飼料

- サブ製品別

- 糖尿病

- 消化器過敏症用

- 経口ケア

- 腎臓

- 尿路疾患

- その他の動物用飼料

- フード

- 流通チャネル

- コンビニエンスストア

- オンラインチャネル

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他のチャネル

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Alltech

- Clearlake Capital Group, L.P.(Wellness Pet Company Inc.)

- Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)

- Dechra Pharmaceuticals PLC

- FARMINA PET FOODS

- General Mills Inc.

- Mars Incorporated

- Nestle(Purina)

- Schell & Kampeter Inc.(Diamond Pet Foods)

- Virbac

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

The UK Dog Food Market size is estimated at 3.48 billion USD in 2025, and is expected to reach 4.09 billion USD by 2030, growing at a CAGR of 3.28% during the forecast period (2025-2030).

The food segment dominated the product types as they are the primary sources of nutrition regardless of dog breed size and age

- The UK dog food market has been experiencing steady growth, increasing by about 13.5% between 2017 and 2021. This increasing trend in the market is mainly due to the growing pet dog population in the country, which reached 12.9 million as of 2022. Growing pet humanization has contributed to market growth.

- The food segment dominated the market and accounted for 68.4% in 2022, as food is a staple purchase for most pet owners in the country, regardless of their dog breed size or age. The dog food market in the country is estimated to register a CAGR of 2.7% during the forecast period.

- Dog treats hold the second-largest market share in the United Kingdom, accounting for 15.0% of the market in 2022. Dogs show a preference for treats over other pets. These treats serve multiple purposes, including training, maintaining dental health, and providing rewards. The dog treats market is projected to register a CAGR of 2.0% during the forecast period.

- Dog veterinary diets accounted for 12.8% of the market in 2022. These diets are specially formulated to address specific health conditions in pets, such as urinary tract diseases, renal failure, and digestive sensitivity. Dog veterinary diets are estimated to exhibit a CAGR of 3.7% during the forecast period.

- Dog nutraceuticals or supplements accounted for 3.8% of the market value in 2022. These pet supplements are often given to pets to support overall health and well-being. The market for dog supplements is projected to register a CAGR of 9.3% during the forecast period.

- The increasing trend in the pet population and the various benefits offered by the wide range of commercial pet products are anticipated to drive the market during the forecast period.

UK Dog Food Market Trends

Adoption from animal shelters and rescue organizations and providing companionship are increasing the dog population

- Dogs are one of the most important pets adopted by pet parents in the United Kingdom, accounting for 33.8% in 2022. The higher share is due to the country's strong culture of dog appreciation and animal welfare, portraying that people in the country are more likely to enjoy taking care of dogs and have higher disposable income. Labrador Retriever was the most adopted dog breed in 2022, with 40,000 registered, because of their friendly dispositions, intelligence, and ability to get along well.

- The dog population increased in the country by 44.4% between 2019 and 2022. During the COVID-19 pandemic, there was an increase in the adoption of dogs from animal shelters and rescue organizations. With more people spending time at home, there was an increased desire for companionship, and many saw this as an opportunity to adopt a dog. Pet parents in the country adopted a dog, which helped dog ownership to 10 million households in 2022, representing about 34% having a dog in their homes as pets. Pet ownership rose by 1% between 2021 and 2022 because they provide loyalty, love, and support during difficult situations, such as the pandemic.

- The increase in the dog population in the country has resulted in a rise in adoption and fostering programs. As a result, companies have many opportunities to explore new ideas in this industry. For instance, in the United Kingdom, companies offer paid "paw-ternity" leave for the pet parents. Therefore, encouraging pet parents to adopt more than one dog. Therefore, factors such as increasing pet adoption, rising pet ownership, and benefits such as providing companionship are anticipated to help in the growth of the dog population in the country during the forecast period.

The growing premiumization of pet food products and increasing demand for high-quality natural pet foods are driving dog expenditure in the United Kingdom

- Dogs are the most popular pets in the United Kingdom, and pet owners spend more money on dog food compared to any other pet food. Pet dog food expenditure in the country has been on the rise, growing by 23.7% between 2019 and 2022. This increase in overall pet dog expenditure can be attributed to the rising population of pet dogs in the country, which grew from 9.0 million in 2019 to 13.0 million in 2022. Additionally, the growing humanization of pets has led to an increased demand for premium dog food products, such as natural and grain-free pet foods.

- The increasing expenditure on dogs and cats between 2019 and 2022 was nearly equal as the population of dogs and cats in the country is similar, with 13 million and 12.7 million, respectively, as of 2022. However, the average spending by pet owners on dogs was about 9.7% higher than the average spending on cats. This is mainly due to the larger size of dogs, which require a higher quantity of food compared to cats. Additionally, pet owners are shifting toward premium dog brands, particularly those that provide specific nutrition based on the needs of dogs.

- Despite the financial crisis in 2022, a significant number of pet owners in the United Kingdom, amounting to 58%, still choose to purchase birthday and Christmas presents for their dogs, indicating the growing trend of pet humanization. Supermarkets remain the preferred distribution channels for buying pet food products in the country, although e-commerce has become increasingly popular due to the impact of the pandemic. The increasing awareness of the benefits of high-quality pet food and the premiumization of pet food are expected to continue driving pet expenditure in the United Kingdom.

UK Dog Food Industry Overview

The UK Dog Food Market is moderately consolidated, with the top five companies occupying 42.20%. The major players in this market are Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), Mars Incorporated, Nestle (Purina), Schell & Kampeter Inc. (Diamond Pet Foods) and Virbac (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Pet Food Product

- 5.1.1 Food

- 5.1.1.1 By Sub Product

- 5.1.1.1.1 Dry Pet Food

- 5.1.1.1.1.1 By Sub Dry Pet Food

- 5.1.1.1.1.1.1 Kibbles

- 5.1.1.1.1.1.2 Other Dry Pet Food

- 5.1.1.1.2 Wet Pet Food

- 5.1.2 Pet Nutraceuticals/Supplements

- 5.1.2.1 By Sub Product

- 5.1.2.1.1 Milk Bioactives

- 5.1.2.1.2 Omega-3 Fatty Acids

- 5.1.2.1.3 Probiotics

- 5.1.2.1.4 Proteins and Peptides

- 5.1.2.1.5 Vitamins and Minerals

- 5.1.2.1.6 Other Nutraceuticals

- 5.1.3 Pet Treats

- 5.1.3.1 By Sub Product

- 5.1.3.1.1 Crunchy Treats

- 5.1.3.1.2 Dental Treats

- 5.1.3.1.3 Freeze-dried and Jerky Treats

- 5.1.3.1.4 Soft & Chewy Treats

- 5.1.3.1.5 Other Treats

- 5.1.4 Pet Veterinary Diets

- 5.1.4.1 By Sub Product

- 5.1.4.1.1 Diabetes

- 5.1.4.1.2 Digestive Sensitivity

- 5.1.4.1.3 Oral Care Diets

- 5.1.4.1.4 Renal

- 5.1.4.1.5 Urinary tract disease

- 5.1.4.1.6 Other Veterinary Diets

- 5.1.1 Food

- 5.2 Distribution Channel

- 5.2.1 Convenience Stores

- 5.2.2 Online Channel

- 5.2.3 Specialty Stores

- 5.2.4 Supermarkets/Hypermarkets

- 5.2.5 Other Channels

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Alltech

- 6.4.2 Clearlake Capital Group, L.P. (Wellness Pet Company Inc.)

- 6.4.3 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 6.4.4 Dechra Pharmaceuticals PLC

- 6.4.5 FARMINA PET FOODS

- 6.4.6 General Mills Inc.

- 6.4.7 Mars Incorporated

- 6.4.8 Nestle (Purina)

- 6.4.9 Schell & Kampeter Inc. (Diamond Pet Foods)

- 6.4.10 Virbac

7 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms