|

市場調査レポート

商品コード

1693951

北米の衛星姿勢・軌道制御システム:市場シェア分析、産業動向、成長予測(2025年~2030年)North America Satellite Attitude and Orbit Control System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の衛星姿勢・軌道制御システム:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 157 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

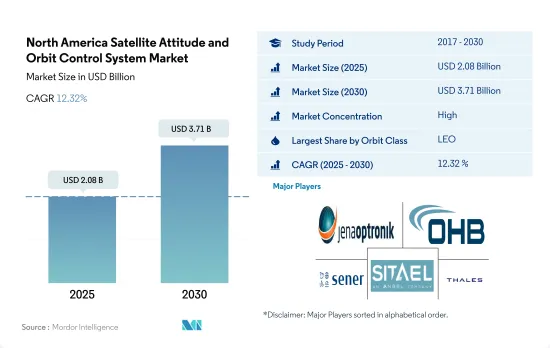

北米の衛星姿勢・軌道制御システム市場規模は2025年に20億8,000万米ドルと推定され、2030年には37億1,000万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは12.32%で成長する見込みです。

LEO衛星打ち上げの増加が市場需要を牽引

- 衛星AOCS市場は、通信、ナビゲーション、地球観測、軍事偵察、科学ミッションに使用されるLEO衛星の需要増に牽引され、力強い成長を遂げています。2017~2022年の間に、約3,021機の衛星がLEOに打ち上げられました。さらに、特に地方や遠隔地での高速インターネットアクセスの必要性が高まっているため、AOCSの需要が伸びています。このため、スペースX、ワンウェブ社、Amazonなどの主要企業は、何千もの衛星をLEOに打ち上げる計画を立てています。

- さらに、GEO衛星が適切に機能するように、AOCSは衛星の姿勢制御や位置の安定化など、さまざまなタスクを実行する必要があります。Honeywell・エアロスペースのようなメーカーは、モーメンタム・アティテュードコントロールシステム(MACS)やデジタルスター・トラッカー(DST)を含む、GEO衛星用のさまざまなAOCS製品とサービスを提供しています。2017~2022年にかけて、約33基の衛星がGEOに打ち上げられました。

- 近年では、信号強度の向上、通信データ転送能力の向上、カバーエリアの拡大など、さまざまな利点があることから、MEO衛星の軍事利用が拡大しています。例えば、レイセオン・ Technologiesのインテリジェンス&スペース社とBoeingのミレニアム・スペースシステムズ社は、軌道を維持するために様々なAOCSシステムを使用することが予想される米国宇宙軍のSSCのために、極超音速ミサイルを探知・追跡するための最初のプロトタイプのミサイル・トラック・カストディ(MTC)MEO OPIRペイロードを開発しています。2017~2022年にかけて、約7基の衛星がMEOに打ち上げられました。市場全体では、2023~2029年の間に14.77%の成長が見込まれています。

北米の衛星姿勢・軌道制御システム市場動向

小型衛星が市場の需要を創出する構え

- 宇宙船の質量による分類は、衛星を軌道に打ち上げるためのロケットのサイズとコストを決定する主要指標の1つです。衛星ミッションの成功は、飛行前の質量測定の正確さと、制限内の質量を得るための衛星の適切なバランスにかかっています。

- 衛星は質量によって分類されます。主要分類タイプは、1,000kgを超える大型衛星です。2017~2022年にかけて、打ち上げられた約45機以上の大型衛星は北米の組織が所有しています。中型衛星は質量が500~1,000kgの衛星。打ち上げられた80以上の衛星が北米の組織によって運用されました。同様に500kg以下の衛星は小型衛星と呼ばれ、この地域では約2,900機以上の小型衛星が打ち上げられています。

- 開発期間が短く、ミッション全体のコストを削減できることから、この地域では小型衛星への動向が高まっています。小型衛星によって、科学的技術的成果を得るために必要な時間を大幅に短縮することが可能になりました。小型衛星のミッションは柔軟性が高いため、新たな技術的機会やニーズへの対応も容易です。米国の小型衛星産業は、特定の用途に合わせた小型衛星を設計・製造するための強固な枠組みの存在に支えられています。北米で運用される衛星の数は、業務用と軍事用宇宙セグメントにおける需要の増加により、2023~2029年にかけて急増すると予想されます。

市場における投資機会

- 北米では、宇宙計画のための政府支出が2022年に約240億という記録を打ち立てた。この地域は、世界最大の宇宙機関であるNASAの存在により、宇宙イノベーションと研究の震源地となっています。2022年、米国政府は宇宙プログラムに620億米ドル近くを費やし、世界で最も宇宙開発費が多い国となります。調査と投資助成金に関しては、この地域の政府と民間部門は、宇宙セグメントの研究とイノベーションに専用の資金を投入しています。各機関は、義務と呼ばれる金銭的約束をすることで、利用可能な予算資源を費やしています。例えば、2023年2月まで、米航空宇宙局(NASA)は研究助成金として3億3,300万米ドルを分配しました。

- 2020年10月、宇宙開発庁(SDA)は、極超音速ミサイルの発射を追跡し、早期に警告することができる新しい軍事衛星の設計、製造、打ち上げに関して、スペースXに1億4,900万米ドルの契約を発注しました。同時期にL3ハリスにも1億9,300万米ドルの同様の契約が結ばれています。両社によって合計8基の衛星が製造される予定で、赤外線センサを使用して宇宙から国防総省にミサイル追跡を提供するために設計されたSDAのトラッキング・レイヤー・トランチ0の最初の重要な部分となります。カナダ政府によると、米国とは別に、カナダの宇宙部門はカナダのGDPに23億米ドルを上乗せし、1万人を雇用しています。カナダ政府の報告によると、カナダの宇宙関連企業の90%は中小企業です。カナダ宇宙庁(CSA)の予算は控えめで、2022~2023年の予算支出見込み額は3億2,900万米ドルです。

北米の衛星姿勢・軌道制御システム産業概要

北米の衛星姿勢・軌道制御システム市場はかなり統合されており、上位5社で82.65%を占めています。この市場の主要企業は、Jena-Optronik、OHB SE、SENER Group、Sitael S.p.A.、Thalesです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 衛星の小型化

- 衛星質量

- 宇宙開発への支出

- 規制の枠組み

- カナダ

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 用途

- 通信

- 地球観測

- ナビゲーション

- 宇宙観測

- その他

- 衛星質量

- 10~100kg

- 100~500kg

- 500~1,000kg

- 10kg以下

- 1,000kg以上

- 軌道クラス

- GEO

- LEO

- MEO

- エンドユーザー

- 商業

- 軍事・政府

- その他

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- AAC Clyde Space

- Innovative Solutions in Space BV

- Jena-Optronik

- NewSpace Systems

- OHB SE

- SENER Group

- Sitael S.p.A.

- Thales

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 50001265

The North America Satellite Attitude and Orbit Control System Market size is estimated at 2.08 billion USD in 2025, and is expected to reach 3.71 billion USD by 2030, growing at a CAGR of 12.32% during the forecast period (2025-2030).

Increasing launches of LEO satellites are driving the market demand

- The satellite AOCS market is experiencing strong growth, driven by the increasing demand for LEO satellites, which are used for communication, navigation, Earth observation, military reconnaissance, and scientific missions. Between 2017 and 2022, approximately 3,021 satellites were launched into LEO. In addition, the demand for AOCS is growing because of the increasing need for high-speed internet access, particularly in rural and remote areas. This has led companies such as SpaceX, OneWeb, and Amazon to plan the launch of thousands of satellites into LEO.

- Additionally, to ensure the proper functioning of GEO satellites, AOCS must perform a range of tasks, including controlling the satellite's orientation and stabilizing its position. Manufacturers like Honeywell Aerospace provide a range of AOCS products and services for GEO satellites, including the Momentum and Attitude Control System (MACS) and the Digital Star Tracker (DST). Between 2017 and 2022, approximately 33 satellites were launched into GEO.

- In recent years, the military's use of MEO satellites has grown due to their different advantages, including increased signal strength, improved communications and data transfer capabilities, and greater coverage area. For instance, Raytheon Technologies' Intelligence & Space and Boeing's Millennium Space Systems are developing the first prototype Missile Track Custody (MTC) MEO OPIR payloads to detect and track hypersonic missiles for the US Space Force's SSC that are expected to use various AOCS systems to maintain their orbit. Between 2017 and 2022, approximately seven satellites were launched into MEO. The overall market is expected to grow by 14.77% during 2023-2029.

North America Satellite Attitude and Orbit Control System Market Trends

Small satellites are poised to create demand in the market

- The classification of spacecraft by mass is one of the main metrics for determining the launch vehicle size and cost of launching satellites into orbit. The success of a satellite mission depends on the accuracy of measuring its mass prior to the flight and the proper balance of the satellite to yield the mass within limits.

- Satellites are classified according to mass. The major classification type is large satellites that are more than 1,000 kg. During 2017-2022, around 45+ large satellites launched were owned by North American organizations. A medium-sized satellite is a satellite with a mass between 500 and 1000 kg. More than 80 satellites launched were operated by North American organizations. Similarly, satellites with a mass of less than 500 kg are considered small satellites, and around 2900+ small satellites were launched in this region.

- There is a growing trend toward small satellites in the region because of their shorter development time which can reduce overall mission costs. They have made it possible to significantly reduce the time required to obtain scientific and technological results. Small spacecraft missions tend to be flexible and can therefore be more responsive to new technological opportunities or needs. The small satellite industry in the United States is supported by the presence of a robust framework for the design and manufacture of small satellites tailored to serve specific application profiles. The number of satellites operating in North America is expected to surge during 2023-2029 because of the growing demand in the commercial and military space segment.

Investment opportunities in the market

- In North America, government expenditure for space programs hit a record of approximately 24 billion in 2022. The region is the epicenter of space innovation and research, with the presence of the world's biggest space agency, NASA. In 2022, the US government spent nearly USD 62 billion on its space programs, making it the highest spender on space in the world. In terms of research and investment grant, the region's governments and the private sector have dedicated funds for research and innovation in the space sector. Agencies spend available budgetary resources by making financial promises called obligations. For instance, till February 2023, the National Aeronautics and Space Administration (NASA) distributed USD 333 million as research grants.

- In October 2020, the Space Development Agency (SDA) awarded a USD 149 million contract to SpaceX for the design, manufacture, and launch of a new military satellite capable of tracking and providing early warnings of hypersonic missile launches. A similar contract worth USD 193 million was awarded to L3Harris during the same timeframe. A total of eight satellites are scheduled to be manufactured by both companies and are meant to be the first crucial part of the SDA's Tracking Layer Tranche 0, which is designed to provide missile tracking for the Defense Department from space using infrared sensors. Apart from the United States, the Canadian space sector adds USD 2.3 billion to the Canadian GDP and employs 10,000 people, according to the Canadian government. The government reports that 90% of Canadian space firms are small and medium-sized businesses. The Canadian Space Agency (CSA) budget is modest, and the estimated budgetary spending for 2022-2023 is USD 329 million.

North America Satellite Attitude and Orbit Control System Industry Overview

The North America Satellite Attitude and Orbit Control System Market is fairly consolidated, with the top five companies occupying 82.65%. The major players in this market are Jena-Optronik, OHB SE, SENER Group, Sitael S.p.A. and Thales (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Satellite Miniaturization

- 4.2 Satellite Mass

- 4.3 Spending On Space Programs

- 4.4 Regulatory Framework

- 4.4.1 Canada

- 4.4.2 United States

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application

- 5.1.1 Communication

- 5.1.2 Earth Observation

- 5.1.3 Navigation

- 5.1.4 Space Observation

- 5.1.5 Others

- 5.2 Satellite Mass

- 5.2.1 10-100kg

- 5.2.2 100-500kg

- 5.2.3 500-1000kg

- 5.2.4 Below 10 Kg

- 5.2.5 above 1000kg

- 5.3 Orbit Class

- 5.3.1 GEO

- 5.3.2 LEO

- 5.3.3 MEO

- 5.4 End User

- 5.4.1 Commercial

- 5.4.2 Military & Government

- 5.4.3 Other

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 AAC Clyde Space

- 6.4.2 Innovative Solutions in Space BV

- 6.4.3 Jena-Optronik

- 6.4.4 NewSpace Systems

- 6.4.5 OHB SE

- 6.4.6 SENER Group

- 6.4.7 Sitael S.p.A.

- 6.4.8 Thales

7 KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms