|

市場調査レポート

商品コード

1687977

衛星姿勢軌道制御システム:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Satellite Attitude and Orbit Control System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 衛星姿勢軌道制御システム:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 193 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

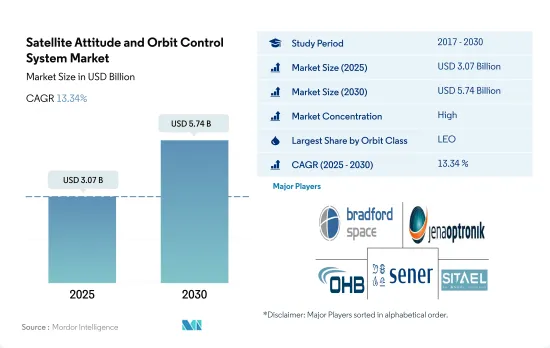

衛星姿勢軌道制御システム市場規模は2025年に30億7,000万米ドルと推計され、2030年には57億4,000万米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは13.34%で成長します。

LEO衛星の急速な配備拡大がAOCSの採用率を押し上げる

- 衛星AOCS市場は、通信、ナビゲーション、地球観測、軍事監視、科学ミッションに使用されるLEO衛星の需要増加に牽引され、力強い成長を遂げています。LEOセグメントは、3つの軌道クラスの中で最大かつ最も広く使用されています。他の2つの軌道クラスと比較すると、シェアの大半を占めています。2017年から2022年の間に、全地域で4,100機以上のLEO衛星が主に通信目的で製造・打ち上げられました。また、特に地方や遠隔地での高速インターネットアクセスのために通信衛星の採用が増加しているため、AOCSの需要が増加しています。このため、SpaceX社、OneWeb社、Amazon社などの主要企業は、LEOへの何千もの衛星打ち上げを計画しています。

- MEO衛星は2番目に大きなシェアを占めています。MEO衛星は、信号強度の向上、通信・データ転送能力の向上、カバーエリアの拡大などの利点があるため、軍事分野での利用が増加しています。

- さらに、GEO衛星に対するAOCSの必要性は低いもの、衛星の姿勢を制御し、位置を安定させ、太陽風、磁場、重力のような外的要因によって引き起こされるあらゆる外乱を修正するなど、さまざまなタスクを実行することによって、GEO衛星を正常に機能させる上で重要な役割を果たしています。AOCSシステム・メーカーは、革新的なスター・トラッカー、リアクション・ホイール、ジャイロスコープ、磁気トルクなど、GEO衛星プラットフォーム向けの先進的な製品を提供しています。

多数の衛星の開発と打ち上げが市場開拓の原動力

- 衛星AOCSは、宇宙空間における衛星の正確な位置、安定性、姿勢を維持する上で重要な役割を果たしています。これらのシステムは、衛星ミッションの成功を確実にし、正確なデータ収集、通信、地球観測を可能にするために極めて重要です。世界のAOCS市場は著しい成長を遂げており、北米、欧州、アジア太平洋がこの産業の発展を牽引する主要地域となっています。

- 北米は世界のAOCS市場をリードしており、米国が技術進歩の最前線にいます。この地域は、確立された航空宇宙企業、研究機関、政府機関からなる強固な宇宙産業を誇っています。北米のAOCS市場は、衛星ベースの通信、防衛、科学ミッションへの強い需要が牽引しています。

- 欧州のAOCS市場は、ESA加盟国と欧州連合の強力な協力関係から恩恵を受けています。フランス、ドイツ、英国といった欧州の主要国は衛星製造において強い存在感を示しており、AOCS市場の成長に貢献しています。この地域は、スター・トラッカー、リアクション・ホイール、スラスター・システムを含む先進的なAOCS技術の開発に重点を置いています。

- アジア太平洋地域は、宇宙産業の急速な拡大により、世界のAOCS市場における主要企業として浮上しています。中国、インド、日本などの国々は、宇宙探査、衛星技術、国産製造能力に多額の投資を行っています。通信、リモート・センシング、ナビゲーション・サービスに対する需要の高まりが、AOCSシステムの採用を後押ししています。

世界の衛星姿勢軌道制御システム市場動向

小型衛星が市場の需要を生み出す構え

- 宇宙船の質量による分類は、衛星を軌道に打ち上げるためのロケットのサイズとコストを決定する主な指標の1つです。北米では、2017~2022年の間に、45機以上の大型衛星(北米の組織が所有)、80機以上の中型衛星(北米の組織が運用)、2,900機以上の小型衛星(同地域で製造)が打ち上げられました。

- 欧州は近年著しい成長を遂げており、その主な要因は、異なる質量の衛星に対する需要の増加です。衛星質量は、欧州の衛星製造市場に影響を与える最も重要な要因の1つです。これは、衛星の種類によって異なる質量を必要とするためであり、ひいてはロケット市場に影響を与えます。2017年から2022年の間に、合計569機の衛星が軌道に投入されました。そのうち、小衛星が451機と最大のシェアを占め、次いで超小型衛星(44機)、大型衛星(37機)、中型衛星(16機)、超小型衛星(7機)と続きます。

- 近年、アジア太平洋地域では、高度な衛星能力に対する需要の高まりに対応する必要性から、衛星製造がますます重要な産業となっています。アジア太平洋地域で製造される衛星の質量範囲は大きく異なり、これが市場の成長に影響を与えています。2017年から2022年の間に、この地域では、130の超小型衛星、75の大型衛星、63の超小型衛星、60の中型衛星、42の小型衛星を含む合計370の衛星が打ち上げられました。

市場の成長を促す投資機会

- 北米では、宇宙計画のための政府支出が2021年に約1,030億米ドルと過去最高を記録しました。この地域は、世界最大の宇宙機関であるNASAの存在により、宇宙イノベーションと研究の震源地となっています。2022年、米国政府はその宇宙プログラムに約620億米ドルを支出し、世界で最も宇宙プログラムに予算を投じる国となりました。例えば、2023年2月まで、NASAは研究助成金として3億3,300万米ドルを分配しました。2022年、米国政府は宇宙プログラムに約620億米ドルを支出し、宇宙産業への支出額が世界一となりました。

- 欧州諸国は宇宙分野への投資の重要性を認識しており、世界の宇宙産業で競争力を維持するために、宇宙活動や技術革新への支出を増やしています。2022年11月、ESAは、地球観測における欧州のリードを維持し、航法サービスを拡大し、米国との探査におけるパートナーであり続けるために、今後3年間で宇宙予算を25%増額することを提案したと発表しました。ESAは22カ国に対し、2023年から2025年にかけての約185億ユーロの予算を支持するよう要請しました。ドイツ、フランス、イタリアが主な拠出国です。

- アジア太平洋地域での宇宙関連活動が増加しています。2022年の日本の予算案によると、宇宙予算は14億米ドルを超え、これにはH3ロケット、技術試験衛星9号、情報収集衛星(IGS)計画の開発が含まれます。22年度のインドの宇宙開発予算案は18億3,000万米ドルでした。2022年、韓国の科学情報通信省は、人工衛星、ロケット、その他の主要な宇宙機器の製造のために6億1,900万米ドルの宇宙予算を発表しました。

衛星姿勢軌道制御システム産業概要

衛星姿勢軌道制御システム市場はかなり統合されており、上位5社で98.09%を占めています。この市場の主要企業は以下の通りです。Bradford Engineering BV, Jena-Optronik, OHB SE, SENER Group and Sitael S.p.A.(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 衛星の小型化

- 衛星質量

- 宇宙開発への支出

- 規制の枠組み

- 世界

- オーストラリア

- ブラジル

- カナダ

- 中国

- フランス

- ドイツ

- インド

- イラン

- 日本

- ニュージーランド

- ロシア

- シンガポール

- 韓国

- アラブ首長国連邦

- 英国

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 用途

- 通信

- 地球観測

- ナビゲーション

- 宇宙観測

- その他

- 衛星質量

- 10-100kg

- 100-500kg

- 500-1000kg

- 10kg未満

- 1000kg以上

- 軌道クラス

- GEO

- LEO

- MEO

- エンドユーザー

- 商業

- 軍事・政府

- その他

- 地域

- アジア太平洋

- 欧州

- 北米

- 世界のその他の地域

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- AAC Clyde Space

- Bradford Engineering BV

- Innovative Solutions in Space BV

- Jena-Optronik

- NewSpace Systems

- OHB SE

- SENER Group

- Sitael S.p.A.

- Thales

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Satellite Attitude and Orbit Control System Market size is estimated at 3.07 billion USD in 2025, and is expected to reach 5.74 billion USD by 2030, growing at a CAGR of 13.34% during the forecast period (2025-2030).

Rapid or increased deployment of LEO satellites driving the adoption rate of AOCS

- The satellite AOCS market is experiencing strong growth, driven by the increasing demand for LEO satellites, which are used for communication, navigation, Earth observation, military surveillance, and scientific missions. The LEO segment is the largest and most widely used among the three orbit classes. It occupies the majority of the share when compared to the other two orbit classes. Between 2017 and 2022, more than 4,100 LEO satellites were manufactured and launched across all the regions, primarily for communication purposes. In addition, the demand for AOCS is increasing because of the increasing adoption of communication satellites for high-speed internet access, particularly in rural and remote areas. This has led companies such as SpaceX, OneWeb, and Amazon to plan the launch of thousands of satellites into LEO.

- MEO satellites constitute the second largest share. The usage of these satellites in the military has increased because of their added advantages, such as increased signal strength, improved communications and data transfer capabilities, and greater coverage area.

- In addition, though the requirement of AOCS for GEO satellites is less, it plays an important role in ensuring the proper functioning of GEO satellites by performing a range of tasks, including controlling the satellite's orientation, stabilizing its position, and correcting any disturbances caused by external factors like solar wind, magnetic fields, and gravity. AOCS system manufacturers provide advanced products for GEO satellite platforms, including innovative star trackers, reaction wheels, gyroscopes, and magnetic torques.

Development and launch of large number of satellites drives the growth of the market

- Satellite AOCS play a vital role in maintaining satellites' precise positioning, stability, and orientation in space. These systems are crucial for ensuring the success of satellite missions, enabling accurate data collection, communication, and Earth observation. The global AOCS market is witnessing significant growth, with North America, Europe, and Asia-Pacific emerging as key regions driving advancements in this industry.

- North America is a leading player in the global AOCS market, with the United States at the forefront of technological advancements. The region boasts a robust space industry comprising established aerospace companies, research institutions, and government agencies. The North American AOCS market is driven by strong demand for satellite-based communication, defense, and scientific missions.

- The European AOCS market benefits from strong collaborations between ESA member states and the European Union. Leading European countries such as France, Germany, and the United Kingdom have a strong presence in satellite manufacturing, contributing to the growth of the AOCS market. The region emphasizes the development of advanced AOCS technologies, including star trackers, reaction wheels, and thruster systems.

- The Asia-Pacific region has emerged as a key player in the global AOCS market, driven by the rapid expansion of its space industry. Countries like China, India, and Japan have invested substantially in space exploration, satellite technology, and indigenous manufacturing capabilities. The growing demand for communication, remote sensing, and navigation services fuels the adoption of AOCS systems.

Global Satellite Attitude and Orbit Control System Market Trends

Small satellites are poised to create demand in the market

- The classification of spacecraft by mass is one of the main metrics for determining the launch vehicle size and cost of launching satellites into orbit. In North America, during 2017-2022, over 45 large satellites (owned by North American organizations), more than 80 medium-sized satellites (operated by North American organizations), and over 2,900 small satellites (manufactured in the region) were launched.

- Europe has witnessed significant growth in recent years, primarily driven by the increasing demand for different satellite masses. Satellite mass is one of the most critical factors influencing the European satellite manufacturing market. This is because different types of satellites require different masses, which, in turn, affects the launch vehicle market. During 2017-2022, a total of 569 satellites were deployed in orbit. Of that, minisatellites accounted for the largest share, with 451, followed by nanosatellites (44), large satellites (37), medium-sized satellites (16), and microsatellites (7).

- Satellite manufacturing has become an increasingly important industry in the Asia-Pacific region in recent years, driven by the need to meet the growing demand for advanced satellite capabilities. The range of satellite mass manufactured in the Asia-Pacific region varies significantly, which affects the growth of the market. During 2017-2022, a total of 370 satellites were launched in the region, including 130 microsatellites, 75 large satellites, 63 nanosatellites, 60 medium-sized satellites, and 42 minisatellites.

Investment opportunities in the market driving growth

- In North America, government expenditure for space programs hit a record of approximately USD 103 billion in 2021. The region is the epicenter of space innovation and research, with the presence of the world's biggest space agency, NASA. In 2022, the US government spent nearly USD 62 billion on its space programs, making it the highest spender on space programs in the world. For instance, till February 2023, NASA distributed USD 333 million as research grants. In 2022, the US government spent nearly USD 62 billion on its space programs, making it the highest spender in the space industry in the world.

- European countries are recognizing the importance of investments in the space domain and are increasing their spending on space activities and innovation to stay competitive in the global space industry. In November 2022, ESA announced that it had proposed a 25% boost in space funding over the next three years to maintain Europe's lead in Earth observation, expand navigation services, and remain a partner in exploration with the United States. ESA asked its 22 nations to back a budget of around EUR 18.5 billion for the period of 2023-2025. Germany, France, and Italy are the major contributors.

- There has been an increase in space-related activities in the Asia-Pacific region. In 2022, according to the draft budget for Japan, the space budget amounted to over USD 1.4 billion, which included the development of the H3 rocket, Engineering Test Satellite-9, and the nation's Information Gathering Satellite (IGS) program. The proposed budget for India's space programs in FY22 was USD 1.83 billion. In 2022, South Korea's Ministry of Science and ICT announced a space budget of USD 619 million for manufacturing satellites, rockets, and other key space equipment.

Satellite Attitude and Orbit Control System Industry Overview

The Satellite Attitude and Orbit Control System Market is fairly consolidated, with the top five companies occupying 98.09%. The major players in this market are Bradford Engineering BV, Jena-Optronik, OHB SE, SENER Group and Sitael S.p.A. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Satellite Miniaturization

- 4.2 Satellite Mass

- 4.3 Spending On Space Programs

- 4.4 Regulatory Framework

- 4.4.1 Global

- 4.4.2 Australia

- 4.4.3 Brazil

- 4.4.4 Canada

- 4.4.5 China

- 4.4.6 France

- 4.4.7 Germany

- 4.4.8 India

- 4.4.9 Iran

- 4.4.10 Japan

- 4.4.11 New Zealand

- 4.4.12 Russia

- 4.4.13 Singapore

- 4.4.14 South Korea

- 4.4.15 United Arab Emirates

- 4.4.16 United Kingdom

- 4.4.17 United States

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application

- 5.1.1 Communication

- 5.1.2 Earth Observation

- 5.1.3 Navigation

- 5.1.4 Space Observation

- 5.1.5 Others

- 5.2 Satellite Mass

- 5.2.1 10-100kg

- 5.2.2 100-500kg

- 5.2.3 500-1000kg

- 5.2.4 Below 10 Kg

- 5.2.5 above 1000kg

- 5.3 Orbit Class

- 5.3.1 GEO

- 5.3.2 LEO

- 5.3.3 MEO

- 5.4 End User

- 5.4.1 Commercial

- 5.4.2 Military & Government

- 5.4.3 Other

- 5.5 Region

- 5.5.1 Asia-Pacific

- 5.5.2 Europe

- 5.5.3 North America

- 5.5.4 Rest of World

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 AAC Clyde Space

- 6.4.2 Bradford Engineering BV

- 6.4.3 Innovative Solutions in Space BV

- 6.4.4 Jena-Optronik

- 6.4.5 NewSpace Systems

- 6.4.6 OHB SE

- 6.4.7 SENER Group

- 6.4.8 Sitael S.p.A.

- 6.4.9 Thales

7 KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms