欧州のリモートセンシング衛星- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Europe Remote Sensing Satellites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 169 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693935

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

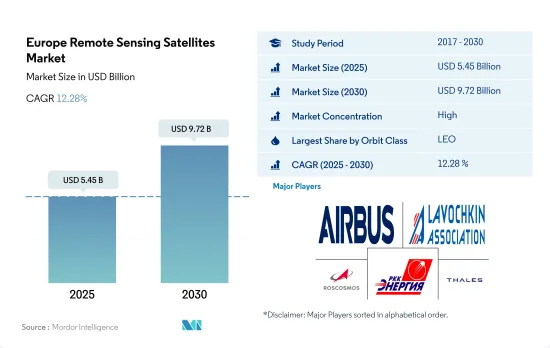

欧州のリモートセンシング衛星市場規模は2025年に54億5,000万米ドル、2030年には97億2,000万米ドルに達すると推定・予測され、予測期間(2025~2030年)のCAGRは12.28%で成長する見込み。

LEO衛星数の急増が予測期間の成長を牽引

- 民間企業は、マイクロエレクトロニクスの進歩、小型衛星、軌道投入コストの低さを組み合わせて、成長著しい地球低軌道(LEO)センシングコンステレーション(迅速なレビューを容易にし、低解像度から高解像度まで幅広い画像を提供する複数の軌道面にある多数の衛星)を作り始めています。

- これらの商業的進歩と、合成開口レーダー(SAR)や無線周波数(RF)マッピングを使用して可視と赤外(IR)スペクトル外を検出する能力との組み合わせは、移動対象の表示から高速妨害ジオロケーションまで、新たな商業とセキュリティアプリケーションを生成します。これらのコミットメントは、国家安全保障だけでなく、他の用途にも活用されています。

- 製造業者は災害対応の可能性に気づき、道路貨物、世界規模の鉄道、海上、陸上の動きをライブで観察することで、市場環境の変化に対する認識を高めています。

- 気象衛星や通信衛星の多くは、地表から最も遠い高軌道を周回する傾向があります。地球中周回軌道にある衛星には、特定の地域をモニタリングするために設計された航法衛星や特殊衛星があります。この地域で製造・打ち上げられる衛星は用途が異なります。例えば、2017~2022年にかけて、MEO軌道に打ち上げられた16基の衛星のうち、ほとんどが全地球測位/ナビゲーション目的で製造されたものです。同様に、GEO軌道に投入された15基の衛星のうち、ほとんどが地球観測と通信目的で配備されました。製造・打ち上げられた約500機以上のLEO衛星は、欧州の機関に属しています。同市場は予測期間中に69%の成長が見込まれています。

欧州のリモートセンシング衛星市場動向

衛星の小型化に対する世界の需要の高まりが市場を牽引

- 小型衛星は、先進的ミッション能力を生み出すために、計算、小型化エレクトロニクス、包装の進歩を活用しています。超小型衛星は他のミッションと宇宙空間を共有できるため、打ち上げコストを大幅に削減できます。欧州の需要は、主にドイツ、フランス、ロシア、英国が牽引しており、毎年最も多くの小型衛星を製造しています。新興企業や超小型衛星開発プロジェクトへの継続的な投資も、この地域の収益成長を押し上げると予想されています。この点、2017~2022年の間に、この地域の様々な参入企業によって50機以上の超小型・超小型衛星が軌道に投入されました。

- 企業は、増大する需要に対応するため、これらの衛星を大規模に生産するコスト効率の良いアプローチに注力しています。このアプローチには、開発と設計検証の段階で、低コストの工業用定格受動素子を使用することが含まれます。電子部品と電子システムの小型化と商業化が市場参入企業を牽引し、その結果、現在の市場シナリオを活用し、強化することを目指す新たな市場参入企業が出現しています。例えば、英国を拠点とする新興企業Open CosmosはESAと提携し、約90%の競争コスト削減を実現しながら、エンドユーザーに業務用超小型衛星打ち上げサービスを提供しています。同様に、2021年8月、フランスはBRO衛星をLEO軌道に打ち上げました。この超小型衛星は世界中の船舶の位置と識別が可能で、海上事業者に追跡サービスを提供し、治安部隊を支援します。同社は2025年までに20~25機の超小型衛星のフリートを構築する計画です。

市場への投資機会

- 欧州諸国は宇宙領域における様々な投資の重要性を認識しており、世界の宇宙産業において競合と革新性を維持するために、地球観測、衛星航法、接続性、宇宙研究、技術革新などのセグメントへの支出を増やしています。例えば、2022年11月、ESAは、地球観測における欧州のリードを維持し、航法サービスを拡大し、米国との探査パートナーであり続けるために、次の3年間で宇宙資金を25%増額することを提案したと発表しました。ESAは22カ国に対し、2023~2025年の予算を約185億ユーロとするよう要請しました。同様に、2022年9月、フランス政府は、宇宙活動に90億米ドル以上を割り当てる計画を発表しました。さらに2022年11月、ドイツはESAプログラムに約23億7,000万ユーロを割り当てると発表しました。その内訳は、地球観測に約6億6,900万ユーロ、通信に約3億6,500万ユーロ、技術プログラムに5,000万ユーロ、宇宙状況認識と宇宙セキュリティに1億5,500万ユーロ、宇宙輸送と運用に3億6,800万ユーロです。

- 英国宇宙庁は、英国の宇宙産業を後押しする18のプロジェクトを支援するために650万ユーロの資金を提供すると発表しました。この資金は、インパクトのある地元主導の計画や宇宙クラスター開発マネージャーを支援することで、英国の宇宙セグメントの成長を刺激します。これら18のプロジェクトは、地球観測データの活用など、地域の問題に立ち向かうためのさまざまな革新的宇宙技術を開拓し、公共サービスを強化することが期待されています。2023年4月、英国政府は宇宙関連活動に31億米ドルを割り当てる見込みであると発表しました。

欧州のリモートセンシング衛星産業概要

欧州のリモートセンシング衛星市場はかなり統合されており、上位5社で99.97%を占めています。この市場の主要企業は、Airbus SE、NPO Lavochkin、ROSCOSMOS、RSC Energia、Thalesです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 衛星の質量

- 衛星の小型化

- 宇宙開発への支出

- 規制の枠組み

- フランス

- ドイツ

- ロシア

- 英国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 衛星質量

- 10~100kg

- 100~500kg

- 500~1,000kg

- 10kg以下

- 1,000kg以上

- 軌道クラス

- GEO

- LEO

- MEO

- 衛星サブシステム

- 推進ハードウェアと推進剤

- 衛星バスとサブシステム

- 太陽電池アレイと電源ハードウェア

- 構造、ハーネス、機構

- エンドユーザー

- 商業

- 軍事・政府

- その他

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Airbus SE

- Esri

- GomSpaceApS

- ImageSat International

- Lockheed Martin Corporation

- Maxar Technologies Inc.

- Northrop Grumman Corporation

- NPO Lavochkin

- Planet Labs Inc.

- ROSCOSMOS

- RSC Energia

- Spire Global, Inc.

- Thales

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 50001247

The Europe Remote Sensing Satellites Market size is estimated at 5.45 billion USD in 2025, and is expected to reach 9.72 billion USD by 2030, growing at a CAGR of 12.28% during the forecast period (2025-2030).

The surge in the number of LEO satellites is driving the growth in the forecast period

- Commercial companies have begun to combine advances in microelectronics, small satellites, and low costs to orbit to create growing low Earth orbit (LEO) sensing constellations: a large number of satellites in multiple orbital planes that facilitate quick review and provide a wide range of low to high-resolution images.

- These commercial advances, combined with the ability to detect outside the visible and infrared (IR) spectrum using synthetic aperture radar (SAR) and radio frequency (RF) mapping, generate new commercial and security applications, from moving target indication to fast jamming geolocation. These commitments are also utilized for other applications and not only for national security.

- Manufacturers have realized the potential of disaster response and have even increased their awareness of changing market conditions by observing the live movement of road freight, global rail, sea, and land.

- Many weather and communication satellites tend to have high Earth orbits farthest from the surface. Satellites in mid Earth orbit include navigational and specialized satellites, which are designed to monitor a specific area. The different satellites produced and launched in this region have different applications. For instance, from 2017 to 2022, of the 16 satellites launched into MEO orbit, most were built for global positioning/navigation purposes. Similarly, of the 15 satellites in GEO orbit, most were deployed for Earth observation and communication purposes. Approximately more than 500 LEO satellites produced and launched belong to European organizations. The market is expected to grow by 69% during the forecast period.

Europe Remote Sensing Satellites Market Trends

Global rising demand for satellite miniaturization is driving the market

- Miniature satellites leverage advances in computation, miniaturized electronics, and packaging to produce sophisticated mission capabilities. As microsatellites can share the ride to space with other missions, they offer a considerable reduction in launch costs. The demand in Europe is primarily driven by Germany, France, Russia, and the United Kingdom, which manufacture the largest number of small satellites each year. The ongoing investments in start-ups and nano and microsatellite development projects are also expected to boost the revenue growth of the region. On this note, during 2017-2022, more than 50 nano and microsatellites were placed into orbit by various players in the region.

- Companies are focusing on cost-effective approaches to produce these satellites on a large scale to meet the growing demand. The approach involves the use of low-cost industrial-rated passives at the development and design validation stages. The miniaturization and commercialization of electronic components and systems have driven market participation, resulting in the emergence of new market players who aim to capitalize on and enhance the current market scenario. For instance, a UK-based start-up, Open Cosmos, partnered with ESA to provide commercial nanosatellite launch services to end users while ensuring competitive cost-savings of around 90%. Similarly, in August 2021, France launched the BRO satellite into LEO orbit. This nanosatellite is able to locate and identify ships around the world, providing tracking services for maritime operators and helping security forces. The company plans to build a fleet of 20 to 25 nanosatellites by 2025.

Investment opportunities in the market

- European countries are recognizing the importance of various investments in the space domain and are increasing their spending in areas such as Earth observation, satellite navigation, connectivity, space research, and innovation to stay competitive and innovative in the global space industry. For instance, in November 2022, ESA announced that it had proposed a 25% boost in space funding over the following three years, designed to maintain Europe's lead in Earth observation, expand navigation services and remain a partner in exploration with the United States. The ESA asked its 22 nations to back a budget of around EUR 18.5 billion for 2023-2025. Similarly, in September 2022, the French government announced that it was planning to allocate more than USD 9 billion to space activities, an increase of about 25% over the previous three years. Additionally, in November 2022, Germany announced that about EUR 2.37 billion was allocated for ESA programs, including about EUR 669 million for Earth observation, about EUR 365 million for telecommunications, EUR 50 million for technology programs, EUR 155 million for space situational awareness and space security, and EUR 368 million for space transport and operations.

- The UK Space Agency announced that it would be funding EUR 6.5 million to support 18 projects to boost the UK space industry. The funding will stimulate growth in the UK space sector by supporting high-impact and locally-led schemes and space cluster development managers. These 18 projects are expected to pioneer a range of innovative space technologies to combat local issues, such as utilizing Earth observation data, to enhance public services. In April 2023, the UK government announced that it expects to allocate USD 3.1 billion for space-related activities.

Europe Remote Sensing Satellites Industry Overview

The Europe Remote Sensing Satellites Market is fairly consolidated, with the top five companies occupying 99.97%. The major players in this market are Airbus SE, NPO Lavochkin, ROSCOSMOS, RSC Energia and Thales (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Satellite Mass

- 4.2 Satellite Miniaturization

- 4.3 Spending On Space Programs

- 4.4 Regulatory Framework

- 4.4.1 France

- 4.4.2 Germany

- 4.4.3 Russia

- 4.4.4 United Kingdom

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Satellite Mass

- 5.1.1 10-100kg

- 5.1.2 100-500kg

- 5.1.3 500-1000kg

- 5.1.4 Below 10 Kg

- 5.1.5 above 1000kg

- 5.2 Orbit Class

- 5.2.1 GEO

- 5.2.2 LEO

- 5.2.3 MEO

- 5.3 Satellite Subsystem

- 5.3.1 Propulsion Hardware and Propellant

- 5.3.2 Satellite Bus & Subsystems

- 5.3.3 Solar Array & Power Hardware

- 5.3.4 Structures, Harness & Mechanisms

- 5.4 End User

- 5.4.1 Commercial

- 5.4.2 Military & Government

- 5.4.3 Other

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Airbus SE

- 6.4.2 Esri

- 6.4.3 GomSpaceApS

- 6.4.4 ImageSat International

- 6.4.5 Lockheed Martin Corporation

- 6.4.6 Maxar Technologies Inc.

- 6.4.7 Northrop Grumman Corporation

- 6.4.8 NPO Lavochkin

- 6.4.9 Planet Labs Inc.

- 6.4.10 ROSCOSMOS

- 6.4.11 RSC Energia

- 6.4.12 Spire Global, Inc.

- 6.4.13 Thales

7 KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

欧州のリモートセンシング衛星- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 169 Pages

- 納期

- 2~3営業日