|

市場調査レポート

商品コード

1693922

日本のデータセンター用サーバ市場:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Japan Data Center Server - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 日本のデータセンター用サーバ市場:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 105 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

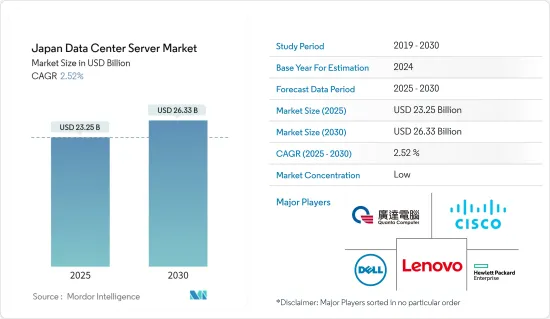

日本のデータセンター用サーバ市場規模は、2025年に232億5,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは2.52%で、2030年には263億3,000万米ドルに達すると予測されます。

日本のデータセンター需要は急増し、ビジネス市場としての魅力も高まっています。環境問題への取り組み、地方データセンターに対する政府の支援、産業構造の変化、技術の進歩によるライフスタイルの変化などが、日本のデータセンター市場において重要な役割を果たしており、その結果、サーバ市場の需要が大きくなっています。

主要ハイライト

- 市場成長の主要促進要因は、日本地域におけるハイパースケール構築需要の拡大です。大阪の強みは、環境、新エネルギー、製薬、製造業など多様な産業が集積している点にあります。この活気あるエコシステムは、ハイパースケールデータセンターと、世界の持続可能性と技術進歩を推進する産業とのユニークな連携を育んでいます。人口880万人の大阪府のGDPは3,600億米ドルで、ノルウェーの経済規模に匹敵します。

- 日本は、インターネットの普及という点で、最も先進的な経済国のひとつと広くみなされています。2023年現在、日本のインターネット利用率(個人)は82.9%、光ファイバーの開発率は99.3%です。ブロードバンド加入者数は4,380万人で、その内訳はFTTH加入者3,660万人、CATVインターネット加入者650万人、モバイルブロードバンド加入者数(4Gと5G)は1億8,400万人です。

- クラウドデータセンターのエネルギー効率は、2050年までに炭素排出量を正味ゼロにするという日本政府の目標を達成するため、日本の二酸化炭素排出量を削減する上で重要な役割を果たすことができます。

- クラウド技術が日本にもたらすメリットと、イノベーションの促進や従来とは異なるビジネスモデルの育成にプラスの効果をもたらすことを認識した日本政府は、国をさらにデジタル化する広範な計画の一環として、クラウドを推進するための数多くのイニシアチブを打ち出しています。

- サーバを構築するには、まず個々の部品を購入しなければならないです。サーバを組み立て、必要なソフトウェアをインストールしなければならないです。サーバをカスタマイズし、所有し、維持するには、リソースが必要です。長期的なプロジェクトや社内での知識蓄積に適しています。

日本のデータセンター用サーバ市場動向

ブレードサーバのフォームファクタセグメントが大幅な成長を遂げる見込み

- ブレードサーバは、コンピューターやシステムのネットワーク内でデータをホストし、配信するために使用される小型コンピューターです。コンピュータ、アプリケーション、プログラム、システム間のリンクとして機能します。Cloudsceneによると、2023年9月現在、日本には218のデータセンターがあります。ブレードサーバは通常、スペースと電力を最大限に活用し効率化する必要があるため、大規模なデータセンターで使用されます。

- 日本には、大規模なデータセンター施設として確認されているデータセンターが40近くあり、今後数年で増加すると予想されています。日本政府は、海底ケーブルの陸揚げ基地を分散させ、陸揚げ地点を多様化することで、全国に複数の新しいデータセンターを建設することを計画しています。海底ケーブルは主に日本の東太平洋側に敷設されており、その多くは東京や志摩など特定の地域に集中しています。政府は他の地域に陸揚げ基地を分散させ、経済的な安全性を強化する方針です。このため、新たな集中地域における大型DCセグメントが大きく成長し、ブレードサーバの需要を押し上げる可能性があります。

- 首都圏では土地と電力に制約があるため、建設コストが上昇し、新規開発が遅れる可能性があり、国内外の参入企業との競争が激化しています。DC建設会社は、日本の乏しい土地に新しいデータセンターを建設するために投資しているが、需要が高いため、これらのデータセンターは高いコンピューティングパワーを持つ可能性が高いです。このような状況におけるブレードサーバの利点は、ブレードサーバの限られたコンピューティングコンポーネントにより、顧客はより多くのサーバをより小さなラック面積に収め、密度を高めることができることです。

- 日本のような一部のアジア諸国は、110V電源インフラをサポートしていません。その結果、米国で享受されている電力密度を達成することができないです。例えば、米国の3相220V電源のデータセンターでは、15kWのラックをサポートすることができます。しかし、この電力密度をサポートするには、特別な冷却ソリューションが必要です。電源が110Vに制限されている場合、ベンダーを問わず、ブレードは実行可能なソリューションではないです。この例外は、HP BladeSystem C3,000やIBM BladeCenter Sのような部門ソリューションです。

- さらに、ブレードサーバは高性能処理用に設計されています。ラックサーバとは異なり、ブレードサーバはホットスワップが可能です。つまり、クラスタ全体の電源を落とすことなく、クラスタ内のブレードサーバを取り外し、交換することができます。このため、管理者がブレードサーバを交換したり、メンテナンスのためにブレードサーバをクラスタから移動したりする必要がある場合のダウンタイムが大幅に短縮されます。

- ブレードサーバ技術の過去、現在、未来を理解することは、日本のあらゆる規模の組織にとって、ITインフラに関して十分な情報に基づいた意思決定を行うために不可欠です。ブレードサーバは、そのコンパクトな設計、高い性能、拡大性により、進化し続ける技術の世界とともに、長年にわたってそのインフラの重要なコンポーネントであり続けることが期待されています。

IT・通信はエンドユーザー産業として急成長へ

- 日本の情報通信技術(ICT)部門はイノベーションの最前線にあり、目覚ましい進歩を推進し、将来を見据えた環境を作り出しています。ICTセグメントは、その成長を規定する課題に立ち向かいながら、最先端技術を活用することで可能性の世界を切り開いています。

- 日本のICT市場の成長は主に、民生用電子機器、軍事、農業、建設など様々なセグメントにおけるモノのインターネット(IoT)機器の利用拡大によって牽引されています。日本には、Sony、Panasonic、Fujitsu、NEC、Toshiba Corporationといった世界有数のICT企業があり、ICTハブとしての日本の成長に重要な役割を果たしています。最高級かつ先進的なインフラを維持するための政府支出の増加や、多くの近代化・改善プロジェクトの適切な実施は、市場の拡大に寄与しています。

- 日本のICT市場は、市民参加、自己評価、オンライン政府サービスに関するフィードバックなど、地域電子政府プロジェクトに焦点を当てたE-日本戦略の急速な拡大により成長すると予想されます。

- 日本は、ICTインフラ、通信技術、教育、医療など、質の高いインフラやサービスに加え、ビジネスや社会の安定性が高いです。日本政府は、民間セクタのデジタルトランスフォーメーションと中小企業(SME)の台頭を支援するための措置を講じています。

- スマートシティは、ソサエティ5.0を実現するための日本政府の主要イニシアチブの一つです。第6次戦略的技術基盤整備(STI)計画では、地方自治体、地域団体、民間企業など1,000以上の組織が参加し、2025年までに100の取り組み10を実施する目標を設定しました。スマートシティ官民パートナーシッププラットフォーム」は、官民パートナーシップを促進し、地域プロジェクトを開発するために、地方に分散したデジタル環境に取って代わるものです。具体的な取り組みとしては、2030年までにマイナンバー(市民ID)システムを一元化し、データベース登録標準を開発することが含まれます。

- さらに、日本の通信会社は6Gに投資しています。6Gシステムは5Gを上回るだけでなく、高速、大容量、低遅延、新たな高周波数帯(100GHz以上)、空・海・宇宙への通信範囲の拡大、超低消費電力・超低コストの通信を記載しています。総務省によると、2023年3月時点で日本国内の5G契約数は約6,980万件を数えます。2022年6月、NEC、Fujitsu、Nokiaの3社は、2030年までに6Gサービスを商用化するため、新たな移動通信技術のテストに共同で取り組みました。

- このように、ハイテク企業による全体的な投資の増加に伴い、IT産業の開発を改善するための政府の取り組みや国内のデータセンターの成長が、日本のサーバ市場を押し上げると考えられます。

日本のデータセンター用サーバ産業概要

日本のデータセンター用サーバ市場は、Dell Technologies Inc.、Hewlett Packard Enterprise、Cisco Systems Inc.、Lenovo Group Limited、Quanta Computer Inc.などの大手企業が存在し、非常にセグメント化されています。同市場の参入企業は、製品ラインナップを強化し、サステイナブル競争優位性を獲得するために、提携や買収などの戦略を採用しています。

- 2023年12月-Fujitsuは、主にサーバとストレージソリューションを中心とするハードウェア事業の経営をさらに強化するため、この戦略に沿ったハードウェア事業の専門会社を日本で立ち上げると発表しました。

- 2023年8月-Hewlett Packard Enterpriseは、phoenixNAPがAmpere Computingのエネルギー効率に優れたプロセッサを採用したクラウドネイティブなHPE ProLiant RL300 Gen11サーバでベアメタルクラウドプラットフォームを拡大すると発表。拡大されたサービスは、AI推論、クラウドゲーム、その他のクラウドネイティブなワークロードを、強化されたパフォーマンスとエネルギー効率でサポートします。

- 2023年7月-Fujitsuは新サーバBS2,000 SE730/SE730Bを発表。最新のSE世代のサーバは、大容量のデータを管理するためのハイエンド性能のプラットフォームとして評価されています。極めて高い可用性を実現し、ミッションクリティカルなアプリケーションに最適なプラットフォームです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 産業バリューチェーン分析

第5章 市場力学

- 市場の促進要因

- 新規データセンター建設の増加、インターネットインフラの開発

- クラウドとIoTサービスの採用増加

- 市場課題

- 高額な初期投資

- COVID-19の影響評価

第6章 市場セグメンテーション

- フォームファクタ別

- ブレードサーバ

- ラックサーバ

- タワー用サーバ

- エンドユーザー別

- IT・通信

- BFSI

- 政府機関

- メディアエンターテイメント

- その他

第7章 競合情勢

- 企業プロファイル

- Dell Technologies Inc.

- Hewlett Packard Enterprise

- Cisco Systems Inc.

- Lenovo Group Limited

- Quanta Computer Inc.

- Super Micro Computer Inc.

- Huawei Technologies Co. Ltd

- Fujitsu Limited

- NEC Corporation

- IBM Corporation

第8章 投資分析

第9章 市場機会と今後の動向

The Japan Data Center Server Market size is estimated at USD 23.25 billion in 2025, and is expected to reach USD 26.33 billion by 2030, at a CAGR of 2.52% during the forecast period (2025-2030).

Japan's demand for data centers is proliferating and becoming more attractive as a business market. Environmental initiatives, government support for local data centers, changes in industrial structure, and changing lifestyles due to technological advancements all play a significant role in the Japanese data center market, resulting in major demand for the server market.

Key Highlights

- The major driver for the market growth is the growing demand for hyperscale construction in the Japanese region. Osaka's strength lies in its diverse concentration of industries, encompassing environmental, new energies, pharmaceuticals, and manufacturing sectors. This vibrant ecosystem fosters a unique coaction between hyperscale data centers and industries driving global sustainability and technological advancement. With a population of 8.8 million, Osaka Prefecture has a GDP of USD 360 billion, similar to the size of Norway's economy.

- Japan is widely regarded as one of the most advanced economies in terms of Internet penetration. As of 2023, Japan's Internet usage rate (individuals) was 82.9%, and the development rate of optical fiber was 99.3%. The number of broadband subscribers was 43.8 million, which includes 36.6 million FTTH subscribers and 6.5 million CATV Internet subscribers, while the number of mobile broadband subscribers (4G and 5G) was 184 million.

- The energy efficiency of cloud data centers can play a crucial role in reducing Japan's carbon footprint to achieve the Japanese government's goal of net-zero carbon emissions by 2050.

- Having recognized the benefits cloud technologies can provide to the country and their positive effect on encouraging innovation and fostering non-conventional business models, the Japanese government has been launching numerous initiatives to promote the cloud as part of the broader plans to digitalize the country further.

- To build a server, one must buy individual components first. They have to assemble the server and install the necessary software. It is resource-intensive to customize, own, and maintain a server. It is well-suited for long-term projects and knowledge-building within the company.

Japan Data Center Server Market Trends

Blade Server Form Factor Segment is Expected to Witness Significant Growth

- A blade server is a small computer used to host and distribute data within a network of computers and systems. It acts as a link between computers, applications, programs, and systems. According to Cloudscene, as of September 2023, there were 218 data centers in Japan. A blade server is typically used in larger data centers due to the need to maximize space and power utilization and efficiency, have high computing needs, and support higher thermal and electrical loads.

- There are close to 40 data centers in Japan that are identified as extensive data center facilities and are expected to increase in the coming years. The Japanese government plans to build several new data centers nationwide by decentralizing landing bases for submarine cables to diversify landing points. Submarine cables are laid mainly on Japan's eastern Pacific Ocean side, with many concentrated in certain areas, such as Tokyo and Shima. The government intends to disperse landing bases in other areas and strengthen economic security. This may lead to significant growth in the large DC segments in newer concentrated areas, boosting the demand for blade servers.

- Constraints on land and power in the greater Tokyo area result in higher construction costs, possible delays for new developments, and fierce competition from domestic and foreign players. DC construction companies are investing in new data centers to build new data centers on scarce land in Japan, but as the demand is high, these data centers are likely to have high computing power. The advantage of blade servers in this situation is that, due to the limited computing components of blade servers, customers can fit more servers into a smaller rack area to increase the density.

- Some Asian countries, such as Japan, do not support 110 V power infrastructure. As a result, they are unable to achieve the power density enjoyed in the United States. For example, a 3-phase 220V power data center in the United States can support a 15 kW rack. However, special cooling solutions are needed to support this power density. Blades are not a viable solution in cases where power is restricted to 110V, no matter the vendor. An exception to this would be a departmental solution, such as the HP BladeSystem C3000 or IBM BladeCenter S.

- Further, blade servers are designed for high-performance processing. Unlike rack servers, blade servers can be hot-swapped. This means that one can remove and replace a blade server in a cluster without powering down the whole cluster. This significantly reduces downtime when an administrator needs to swap out a blade server or move a blade server out of the cluster for maintenance.

- Understanding blade server technology's past, present, and future is essential for organizations of all sizes in Japan to make informed decisions regarding their IT infrastructure. Due to their compact design, high performance, and scalability, blade servers are expected to remain a key component of that infrastructure for many years as they continue to evolve and evolve with the ever-evolving world of technology.

IT and Telecommunication to be the Fastest Growing End-user Industry

- Japan's Information and Communications Technology (ICT) sector is at the forefront of innovation, driving remarkable progress and creating a future-proof environment. The ICT sector opens up a world of possibilities by utilizing state-of-the-art technologies while facing the challenges that define its growth.

- The growth of the Japanese ICT market is mainly driven by the growing use of Internet of Things (IoT) devices across various sectors, such as consumer electronics, military, agriculture, and construction. Japan is home to some of the most prominent ICT organizations in the world, such as Sony, Panasonic, Fujitsu, NEC, and Toshiba (Toshiba), which are playing an important role in the growth of Japan as an ICT hub. The increasing government spending on maintaining the top-of-the-line and advanced infrastructure and the proper implementation of many modernization and improvement projects contribute to the market's expansion.

- Japan's ICT market is expected to grow due to the rapid expansion of E-Japan's strategy, which focuses on local e-government projects, such as citizen participation, self-assessment, and feedback on online government services.

- Japan has a high level of stability in business and society, as well as high-quality infrastructure and services such as ICT infrastructure, communication technology, education, healthcare, and more. The Japanese government is taking steps to support the private sector's digital transformation and the emergence of small and medium-sized enterprises (SMEs).

- Smart Cities are one of the Japanese government's key initiatives to bring Society 5.0 to life. The 6th Strategic Technology Infrastructure (STI) plan set a goal of 100 initiatives10 to be implemented by 2025 with the participation of 1000+ organizations from local government, regional organizations, and private enterprises. The "Smart City Public-Private Partnership platform" will replace the local and dispersed digital landscape to promote public-private partnerships and develop regional projects. Specific initiatives include centralizing the MyNumber (citizens ID) system and developing database registry standards by 2030.

- Further, the telecom companies in Japan are investing in 6G. The 6G system will not only outperform 5G, but it will also offer high speed, high capacity, low latency, new high-frequency bands (above 100 GHz), extend communication coverage to the sky, sea, and space, and provide ultra-low power consumption and ultra-low-cost communications. According to the Ministry of Internal Affairs and Communications, about 69.8 million 5G subscriptions were counted in Japan as of March 2023. In June 2022, NEC (NEC), Fujitsu (Fujitsu), and Nokia (Nokia) joined forces to test new mobile communication technologies to launch 6G services commercially by 2030.

- Thus, with the overall increase in investment by tech companies, government initiatives to improve the IT industry development and growth in data centers in the country would boost the server market in Japan.

Japan Data Center Server Industry Overview

The Japan data center server market is highly fragmented with the presence of major players like Dell Technologies Inc., Hewlett Packard Enterprise, Cisco Systems Inc., Lenovo Group Limited, and Quanta Computer Inc. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- December 2023 - Fujitsu announced the launch of a dedicated company for the hardware business in Japan in alignment with this strategy and to further strengthen the management of its hardware business, which primarily focuses on servers and storage solutions.

- August 2023 - Hewlett Packard Enterprise announced that phoenixNAP is expanding its Bare Metal Cloud platform with cloud-native HPE ProLiant RL300 Gen11 servers, using energy-efficient processors from Ampere Computing. The expanded services support AI inferencing, cloud gaming, and other cloud-native workloads with enhanced performance and energy efficiency.

- July 2023 - Fujitsu announced a new server, BS2000 SE730/SE730B. The servers of the latest SE generation are a valued platform in the high-end performance range for managing the largest data volumes. The servers offer extremely high availability and serve as an ideal platform for mission-critical applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increase in Construction of New Data Centers, Development of Internet Infrastructure

- 5.1.2 Increasing Adoption of Cloud and IoT Services

- 5.2 Market Challenge

- 5.2.1 High Initial Investments

- 5.3 Assessment of COVID-19 Impact

6 MARKET SEGMENTATION

- 6.1 By Form Factor

- 6.1.1 Blade Server

- 6.1.2 Rack Server

- 6.1.3 Tower Server

- 6.2 By End User

- 6.2.1 IT and Telecommunication

- 6.2.2 BFSI

- 6.2.3 Government

- 6.2.4 Media and Entertainment

- 6.2.5 Other End Users

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Dell Technologies Inc.

- 7.1.2 Hewlett Packard Enterprise

- 7.1.3 Cisco Systems Inc.

- 7.1.4 Lenovo Group Limited

- 7.1.5 Quanta Computer Inc.

- 7.1.6 Super Micro Computer Inc.

- 7.1.7 Huawei Technologies Co. Ltd

- 7.1.8 Fujitsu Limited

- 7.1.9 NEC Corporation

- 7.1.10 IBM Corporation