デジタルサイネージメディアプレーヤー:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Digital Signage Media Player - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1689961

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

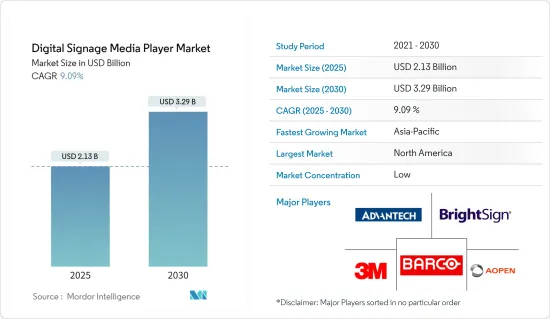

デジタルサイネージメディアプレーヤーの市場規模は、2025年に21億3,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは9.09%で、2030年には32億9,000万米ドルに達すると予測されます。

主なハイライト

- デジタルサイネージディスプレイは、製品、サービス、イベント、セールなどのプロモーションを効果的に表示します。単にグラフィックを回転させるだけでなく、これらのマルチメディア・スクリーンにはビデオやアニメーションが組み込まれており、広告主は静的な広告、製品デモ、ビデオによる体験談を提示することができます。

- デジタルサイネージでは、コンテンツやメッセージは、物理的な看板を変更することなく、電子スクリーン上で迅速に更新することができます。この動向は、今後数年間にいくつかの新興経済国で予想される力強い成長と同期しています。技術の進歩とコストの低下に伴い、デジタルサイネージの採用は増加傾向にあります。

- 多くの業界プレーヤーが提携し、最先端のソリューションを提供しています。例えば、クリックシェアとシグナジェライブは、職場のコラボレーションとコミュニケーションを変革するために提携しました。この提携により、企業はSignageliveとClickShare Conferenceをシームレスに統合し、即座に投資を強化することができます。クリックシェアのワイヤレス・ルーム・システムを導入することで、企業は情報豊富で魅力的なコラボレーション・スペースを作り出し、施設全体でスクリーンがダイナミックで生産的な状態を維持できるようになります。

- バーやレストランなど、顧客体験の向上を目的としたサイネージ・ソリューションの導入が増加していることから、今後数年間はデジタルサイネージメディアプレーヤーの需要が高まることが予想されます。従来のメニューカードに代わるこれらのデバイスは、人目を引く広告を表示するために電源付きスクリーンで使用されており、大きな市場機会をもたらしています。また、小売業界では、ブランドの認知度を高めるためにこれらのデバイスを採用するケースが増えており、デジタルサイネージメディアプレーヤー市場をさらに活性化させています。

- しかし、デジタル・サイネージの状況をナビゲートすることは、独立したインフラ開発と展開を試みるエンドユーザーにとって困難なことです。その複雑さを考えると、この取り組みには、IT、オーディオビジュアル、ソフトウェア、機械、ディスプレイ技術など、さまざまな領域にわたる専門知識が要求されます。付加価値小売業者の包括的なソリューションを選択し、パートナー・ベンダーの製品を統合するには、技術的な容易さと標準化されたプロトコルが必要です。これにより、設置が合理化されるだけでなく、アップグレードが簡素化され、メンテナンスが軽減されます。

- コンテンツ・セキュリティ、プラットフォームの互換性、標準化の要請といった課題がハードルとなる一方で、デジタル・サイネージ分野の大手企業は、インタラクティブでパーソナライズされたソリューションにますます注力するようになっており、世界市場の大幅な成長への道を開いています。

- パンデミック後、企業は先進技術やデジタルコンテンツの人気上昇を活用し、顧客を惹きつける斬新な方法を模索しています。また、パンデミックの後、企業はデジタル・コミュニケーションにシフトし、印刷された看板や対面での対応から脱却しています。このシフトは今後も続くと予想され、企業が物理的な資料への依存を減らし、容量制限の低下に適応するにつれて、デジタルサイネージの重要性が増しています。

デジタルサイネージメディアプレーヤー市場動向

小売セグメントが大きなシェアを占める見込み

- 小売販売にはパーソナライゼーションが必要であり、これが行動ベース広告の成功の礎となっています。コンテクスト広告は従来、コンテンツとの関連性に重点を置いてきたが、より直接的な顧客コミュニケーションを必要としています。しかし、人工知能(AI)が統合されたことで、状況は大きく変化しようとしており、コンテキスト広告にパーソナライゼーションを注入することが期待され、市場の成長を後押ししています。

- 小売業界では、消費者とのエンゲージメントを強化し、新たな顧客を獲得することを目的として、デジタルサイネージメディアプレーヤーの導入が増加しています。小売業者は、店舗での体験を向上させ、顧客基盤を拡大するために、先進的な技術ソリューションに軸足を移しています。さらに、タッチスクリーンのようなインタラクティブ機能の強化を誇るこれらのデバイスの急増が、業界内の需要の高まりに拍車をかけています。

- 従来の広告の大半は印刷されたサイネージであったが、長期的な費用対効果による集客と顧客満足を目指し、デジタルサイネージに取って代わられました。印刷されたサイネージは、ビルボードやポスターのような単一用途のメッセージであり、今日のコンテンツ・マーケティングのダイナミックな性質のために頻繁に廃棄されています。

- 小売業は、広告のためのデジタルサイネージへの投資が最も高い、広く採用されているセグメントです。大きな課題の1つは、さまざまな場所の個別のニーズに対応しながら、マーケティング・キャンペーンを調整することです。堅牢なデジタル・サイネージ・システムを採用することで、小売業の利害関係者を引き込むことが非常に容易になります。

- ラジオ、テレビ、印刷物などのさまざまな広告チャネルの中でも、デジタルは依然として世界の広告市場成長の主要な原動力であり、上昇基調にあります。このようなデジタル広告支出の増加は、デジタル化に向けて企業が割り当てた予算とともに、商業セグメントにおけるこれらのデバイスの高い採用率の主な理由です。特に、BluetoothやBLEと組み合わせたデジタルサイネージは、コンテクスチュアル・マーケティングに効果的な組み合わせです。ビーコン対応モバイルアプリは、顧客データを収集し、パーソナライズされたメッセージの送信に利用します。同じ理由で、メディア・プレーヤー・プロバイダーは、必要なコネクティビティを組み込む必要があります。

- 最新の電通世界広告費予測レポートによると、世界の広告投資は2023年に3.3%増加すると予測されています。同レポートは、年末までに全世界で約7,279億米ドルが支出され、業界の支出が大幅に増加すると予測しています。デジタルサイネージのためのデジタル広告費は、デジタル広告費(インターネット)に対する世界ブランドの親和性とともに増加すると予想され、OOH(アウトオブホーム)広告とともにデジタル広告費を組み込む道が開かれます。予測によると、前年比広告費の増加は、アウトオブホーム(+3.8%)、シネマ(+2.1%)、オーディオ(+0.8%)で記録されました。現在の動向は、市場の見通しを楽観的にしています。

北米が大きなシェアを占める

- 米国は最大のデジタルサイネージマーケットプレースの一つです。小売店、交通システム、屋外広告、レストラン、博物館、企業ビル、公共スペースなど、数多くの用途におけるディスプレイ、接続性、監視スペースの最近の技術進歩により、米国ではデジタルサイネージの人気が高まっています。また、普及に伴いディスプレイパネルの価格も急落しています。

- 米国の小売業は、店舗内でのユーザー体験を提供するため、かなりの市場シェアを獲得すると予測されています。OBERLOの推計によると、米国の小売売上高は2023年に0.6%、2024年に1.3%拡大する計画で、2022年第3四半期には1兆9,000億米ドルに達します。企業はオンラインとオフラインのショッピングを組み合わせ、シームレスなマルチチャネル体験を実現しています。これにより、価格、機能、販促方法など、多くのことが変化しています。

- Scala Digital Signageによると、購入の42%はオンライン、モバイル、ソーシャルコマースのウェブサイトからもたらされると予想されています。これに対し、米国の小売業者の74%は、魅力的な店舗での消費者体験を創造することが重要だと考えています。その結果、新興企業も既存企業も研究開発能力に多額の投資を行い、新製品を発表したり、旧製品を開発したり、可能な限り大きな市場シェアを獲得するためにパートナーシップを結んだりしています。

- カナダは、人口わずか3,900万人の世界有数の経済大国であるにもかかわらず、経済・産業分野で抜きん出ていることで有名です。これはデジタル・サイネージにも当てはまり、成熟したインフラと、オンライン・ショッピングよりも対面でのショッピングを好む国民性が、ネットワーク・オペレーターに大きなチャンスをもたらしています。

- パンデミックはカナダの小売業に大きな変化をもたらしたが、eコマースの成長は力強く、長く続いています。当然のことながら、オンライン情報、インスピレーション、購買はすべてデジタルによって促進されており、デジタルは今やすべての商取引の入り口であり、オンライン、オフラインを問わず、カナダのショッピング体験を牽引しています。このため、カナダのデジタルサイネージ小売市場は成長する可能性が高いです。

デジタルサイネージメディアプレーヤー産業の概要

デジタルサイネージメディアプレーヤー市場は、ハードウェアやソフトウェアなど、得意とする多様な分野から構成されています。市場の両分野で激しい競争が繰り広げられています。この業界における競争企業間の敵対関係は、3M、シスコ、デル、アドバンテックなどの大手企業が支配しています。業界の収益性は、プレーヤーの活動を著しく増加させています。そのため、新規参入企業や既存の大手企業は、市場での競争力を維持するために強力な戦略を採用しています。そのため、市場における競争企業間の敵対関係は高いです。

2024年4月、サービス・オートメーション・ソリューション・プロバイダーであるアドバンテックは、最新のイノベーションであるUBX-110Kを発表しました。このUHDファンレス・ミニボックス・コンピューター・プラットフォームは、特に小売店やホスピタリティ・サイネージ・プレーヤー市場向けにカスタマイズされています。第12世代Intel Embedded N97プロセッサーまたはIntel Embedded Core i3-N305プロセッサーを搭載したUBX-110Kは、3系統のビデオ出力で際立っています。UBX-110Kは、3系統のビデオ出力を備えており、そのソフトウェアは、シームレスなリアルタイム制御を可能にする、容易なリモート管理のために設計されています。これらの特長により、UBX-110Kはさまざまなデジタルサイネージ用途のトップチョイスとなり、その汎用性の高さを示しています。

2023年6月、デジタルサイネージ企業のBrightSignとTCLの子会社であるMOKA Technologyは、コンテンツプレーヤーを統合したディスプレイの開発で提携しました。この提携は、BrightSign Built-In Platformを顕著に特徴とするMOKA BS60を筆頭とする一連のディスプレイに焦点を当てています。このデバイスの特筆すべき特徴は、4K対応、横向きと縦向きの両方、超狭額ベゼル、25%ヘイズ、3H表面硬化、2インチ以下の薄型、500nitsの輝度、90%の広色域、卓越したコントラストレベルなどです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 産業バリューチェーン分析

- 主要マクロ経済動向の影響評価

第5章 市場力学

- 市場促進要因

- コンテクストを意識した広告と豊かな顧客体験の成長を促進する動向

- DOOH支出の着実な増加

- 市場の課題

- 技術および標準化の複雑さ

第6章 市場セグメンテーション

- コンポーネント別

- ハードウェア

- ソフトウェア

- 製品別

- エントリーレベル

- アドバンストレベル

- エンタープライズレベル

- 用途別

- 小売

- ホスピタリティ

- 企業

- 輸送機関

- その他の用途(教育、政府機関など)

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- アジア

- インド

- 中国

- 日本

- オーストラリア・ニュージーランド

- ラテンアメリカ

- ブラジル

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 北米

第7章 競合情勢

- 企業プロファイル

- 3M Company

- Advantech Co. Ltd

- AOPEN Inc.(Acer Group)

- Barco

- BrightSign LLC

- Broadsign

- Cisco Systems Inc.

- ClearOne Communications Inc.

- Dell Technologies Inc.

- Gefen

- HaiVision Inc.

- Hewlett Packard Enterprise

- ONELAN(Uniguest)

- Disguise Technologies Limited

- Dataton AB

- AV Stumpfl GmbH

- Green-Hippo(tvOne NCSA)

- Modulo Pi

- Christie Digital Systems USA Inc.

- 7thSense

第8章 ベンダーランキング

第9章 投資分析

第10章 市場の将来

目次

The Digital Signage Media Player Market size is estimated at USD 2.13 billion in 2025, and is expected to reach USD 3.29 billion by 2030, at a CAGR of 9.09% during the forecast period (2025-2030).

Key Highlights

- Digital signage displays effectively showcase promotions for products, services, events, or sales. Beyond just rotating graphics, these multimedia screens incorporate video and animation, allowing advertisers to present static ads, product demos, and video testimonials.

- With digital signage, content, and messages can be swiftly updated on electronic screens without altering physical signs. This trend is in sync with the robust growth anticipated in several emerging economies in the coming years. As technology advances and costs decrease, the adoption of digital signage is on the rise.

- Many industry players are teaming up to offer cutting-edge solutions. For example, ClickShare and Signagelive have partnered to transform workplace collaboration and communication. Businesses can seamlessly integrate Signagelive with ClickShare Conference through this collaboration, instantly enhancing their investments. By deploying ClickShare's wireless room systems, companies can create informative, engaging, and collaborative spaces, ensuring their screens remain dynamic and productive throughout their facilities.

- The increasing deployment of signage solutions in bars, restaurants, and similar establishments aimed at elevating the customer experience is set to drive demand for digital signage media players in the coming years. These devices, replacing traditional menu cards, are being used on powered screens to showcase eye-catching advertisements, presenting significant market opportunities. The retail sector also increasingly adopts these devices to boost brand visibility, further fueling the digital signage media player market.

- However, navigating the digital signage landscape can be daunting for end-users venturing into independent infrastructure development and deployment. Given its complexity, this endeavor demands expertise across various domains, including IT, audiovisuals, software, mechanics, and display technologies. Opting for comprehensive solutions from value-added retailers and integrating products from partner vendors necessitates technical ease and standardized protocols. This not only streamlines installations but also simplifies upgrades and reduces maintenance.

- While challenges like content security, platform compatibility, and the call for standardization pose hurdles, leading players in the digital signage realm are increasingly focusing on interactive and personalized solutions, paving the way for substantial global market growth.

- Post-pandemic, businesses are exploring novel ways to engage customers, leveraging advanced technologies and the rising popularity of digital content. Also, in the wake of the pandemic, businesses have shifted toward digital communications, moving away from printed signage and in-person interactions. This shift is expected to persist, with digital signage taking on added significance as companies reduce their reliance on physical materials and adapt to lower capacity limits.

Digital Signage Media Player Market Trends

The Retail Segment is Expected to Hold a Significant Share

- Retail sales require personalization, which has been the cornerstone of the success of behavior-based ads. While contextual ads have traditionally focused on content relevance, they need more direct customer communication. However, the landscape is poised for a significant shift with the integration of artificial intelligence (AI), promising to infuse personalization into contextual advertising, which propels the market toward growth.

- The retail sector's adoption of digital signage media players is on the rise, aimed at bolstering consumer engagement and drawing in fresh clientele. Retailers are pivoting towards advanced tech solutions to elevate their in-store experiences and widen their customer base. Moreover, the surge in these devices, boasting enhanced interactive features like touch screens, is fueling a heightened demand within the industry.

- The majority of traditional advertising is printed signage, which has been replaced with digital signage, aiming at customer attraction and satisfaction through cost-effectiveness in the long run. Printed signages were single-use messages such as billboards and posters, frequently discarded due to the dynamic nature of content marketing today.

- The retail sector is a widely adopted segment with the highest investment in digital signage for advertising. One major challenge is coordinating marketing campaigns while accommodating the individual needs of various locations. Adopting a robust digital signage system is making engaging retail stakeholders much easier.

- Among the different advertising channels, such as radio, television, and print, digital remains a key driver of global advertising market growth and is on an upward trajectory. Such increased digital advertising spending, along with allocated budgets by the companies toward digitization, is the major reason for the high adoption rate of these devices in the commercial segment. In particular, digital signage, coupled with Bluetooth or BLE, offers an effective combination for contextual marketing. Beacon-enabled mobile apps collect customer data and use it to send personalized messages. For the same reason, media player providers must embed the required connectivity.

- According to the latest Dentsu Global Ad Spend Forecasts report, global advertising investment was expected to increase by 3.3% in 2023. The report predicted that by the year's end, approximately USD 727.9 billion will have been spent worldwide, marking a significant growth in the industry's expenditure. Digital ad spending for digital signage is expected to increase along with global brands' affinity toward digital ad spending (internet), opening paths to incorporate digital spending along with OOH (out-of-home) ads. As per forecasts, the incremental increase in the Y-o-Y advertisement spending was recorded for out-of-home (+3.8%), cinema (+2.1%), and audio (+0.8%). The current trends are contributing to a optimistic market outlook.

North America Holds Major Market Share

- The United States is one of the largest digital signage marketplaces. Due to recent technological advancements in display, connectivity, and monitoring spaces in numerous applications, including retail stores, transportation systems, outdoor advertising, restaurants, museums, corporate buildings, and public spaces, digital signage is becoming increasingly popular in the United States. In addition, the widespread usage has led to a sharp decline in the cost of display panels.

- The retail sector in the United States is predicted to gain a considerable market share to provide a distinct in-store user experience. The OBERLO estimates that US retail sales were planned to expand by 0.6% in 2023 and 1.3% in 2024, accounting for USD 1.9 trillion in the third quarter of 2022. Businesses combine online and offline shopping to make a seamless multi-channel experience. This has changed a lot of things, like prices, features, and ways to promote.

- According to Scala Digital Signage, 42% of purchases are anticipated to come from online, mobile, and social commerce websites. In comparison, 74% of US retailers believe creating an engaging in-store consumer experience is crucial. As a result, new and established firms heavily invest in their R&D capabilities, release new products or develop old ones, and form partnerships to gain the largest possible market share.

- Canada is renowned for punching above its weight in the economic and industrial realms despite having a population of only 39 million and one of the largest economies in the world. This is also true for digital signage, where a mature infrastructure and a populace that prefers in-person to online shopping present network operators with enormous opportunities.

- The pandemic permanently altered Canadian retail, yet the growth of e-commerce has been robust and long-lasting. Unsurprisingly, online information, inspiration, and purchasing are all facilitated by digital, which is now the doorway to all commerce and is driving the Canadian shopping experience online and offline. Because of this, the Canadian retail market for digital signage is likely to grow since businesses need a solid digital presence to meet customer needs.

Digital Signage Media Player Industry Overview

The digital signage media player market comprises diverse areas in which to excel, such as hardware and software. There has been intense competition in both sectors of the market. Competitive rivalry in this industry is governed by significant players, such as 3M, Cisco, Dell, and Advantech. Profitability in the industry is significantly increasing player activity. Thus, the new players and the existing giants are adopting powerful strategies to maintain a competitive edge in the market. Therefore, the competitive rivalry in the market is high.

In April 2024, Advantech, a service automation solutions provider, introduced the UBX-110K, its latest innovation. This UHD fanless mini box computer platform is tailored specifically for the retail and hospitality signage player markets. Equipped with either the 12th-generation Intel Embedded N97 or Intel Embedded Core i3-N305 processors, the UBX-110K stands out with its three video outputs. Its software is crafted for effortless remote management, granting users seamless real-time control. These attributes collectively position the UBX-110K as the top choice for various digital signage applications, showcasing its versatility.

In June 2023, BrightSign, a digital signage firm, and MOKA Technology, a subsidiary of TCL, teamed up to develop displays with integrated content players. The collaboration focuses on a series of displays led by the MOKA BS60, which prominently features the BrightSign Built-In Platform. Notable features of the device include 4K support, both landscape and portrait orientations, an ultra-narrow bezel, 25% haze, 3H surface hardening, a slim profile under two inches, 500 nits brightness, a wide 90% color gamut, and exceptional contrast levels.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 An Assessment of the Impact of Key Macroeconomic Trends

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Trends Favoring the Growth of Context-aware Advertising and Enrich Customer Experience

- 5.1.2 Steady Increase in DOOH Spending

- 5.2 Market Challenges

- 5.2.1 Technical and Standardization Complexity

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Hardware

- 6.1.2 Software

- 6.2 By Product

- 6.2.1 Entry Level

- 6.2.2 Advanced Level

- 6.2.3 Enterprise Level

- 6.3 By Application

- 6.3.1 Retail

- 6.3.2 Hospitality

- 6.3.3 Corporate

- 6.3.4 Transportation

- 6.3.5 Other Applications (Education, Government, etc.)

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 United Kingdom

- 6.4.2.3 France

- 6.4.3 Asia

- 6.4.3.1 India

- 6.4.3.2 China

- 6.4.3.3 Japan

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.5.1 Brazil

- 6.4.5.2 Argentina

- 6.4.6 Middle East and Africa

- 6.4.6.1 United Arab Emirates

- 6.4.6.2 Saudi Arabia

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 3M Company

- 7.1.2 Advantech Co. Ltd

- 7.1.3 AOPEN Inc. (Acer Group)

- 7.1.4 Barco

- 7.1.5 BrightSign LLC

- 7.1.6 Broadsign

- 7.1.7 Cisco Systems Inc.

- 7.1.8 ClearOne Communications Inc.

- 7.1.9 Dell Technologies Inc.

- 7.1.10 Gefen

- 7.1.11 HaiVision Inc.

- 7.1.12 Hewlett Packard Enterprise

- 7.1.13 ONELAN (Uniguest)

- 7.1.14 Disguise Technologies Limited

- 7.1.15 Dataton AB

- 7.1.16 AV Stumpfl GmbH

- 7.1.17 Green-Hippo (tvOne NCSA)

- 7.1.18 Modulo Pi

- 7.1.19 Christie Digital Systems USA Inc.

- 7.1.20 7thSense

8 VENDOR RANKING

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日