アフリカの生物農薬:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Africa Biopesticides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 149 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693782

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

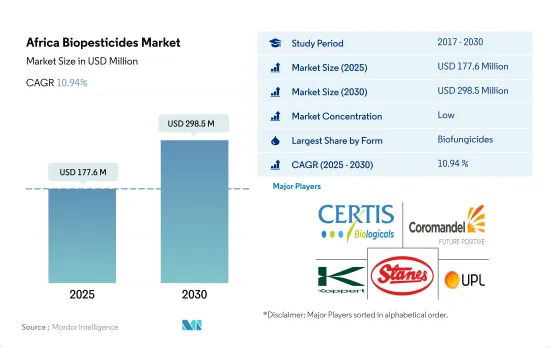

アフリカの生物農薬市場規模は2025年に1億7,760万米ドルと推定され、2030年には2億9,850万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは10.94%で成長する見込みです。

- 生物農薬は、動物、植物、昆虫、細菌や真菌を含む微生物に由来する天然由来の物質または薬剤であり、農業害虫や感染症の管理に使用されます。アフリカの生物農薬市場は2017~2022年にかけて23.4%成長しました。

- この地域では、連作作物における生物農薬消費が他の作物よりも高く、2022年には73.8%を占めます。園芸作物は19.7%を占め、換金作物は同年の消費量全体の6.5%を占めています。

- アフリカの生物農薬市場では、総合的有害生物管理(IPM)の概念が重要です。IPM1.0は、農薬の過剰使用を減らすために数十年前に確立されました。IPM2.0では、生物的防除や生息地管理といった農業生態学的原則が徐々に取り入れられました。しかしこの間、零細農業従事者は意思決定能力を向上させることなく、危険な農薬を第一の防御線として頼り続けた。アフリカ地域では、統合的病害虫管理3.0(IPM3.0)も実施されました。このIPM3.0には、3つの新機能、すなわち、農業従事者によるリアルタイムの意思決定へのアクセス、科学と自然による病害虫管理の選択肢、ゲノムアプローチ、生物農薬、生息地管理の実践の統合が含まれています。こうしたIPMの実践がアフリカにおける生物農薬市場を牽引する可能性があります。

- リアルIPMと共同で、国際昆虫生理生態センターは2種類の生物農薬、キャンペーン(icipe69)とアチーブ(icipe78)を商品化しました。キャンペーン(icipe69)は、キュウリ、マンゴー、パパイヤ、バラ、トマトなどの作物で、メアリ、アザミウマ、ミバエに対して使用されています。IPM実践の採用と生物農薬の研究開発活動の増加は、2023~2029年の間に市場規模を84.7%押し上げる可能性があります。

- アフリカの生物農薬市場は、2017~2021年の間に15.8%の成長率を示しており、この成長は2029年までに約84.7%の拡大が予測され、継続すると予想されます。

- この成長は主に、アフリカにおける総合的害虫管理3.0(IPM 3.0)の立ち上げに起因しています。この害虫管理戦略は、農業従事者によるリアルタイムの意思決定へのアクセス、科学的根拠による害虫管理の選択肢、遺伝的手法、生物農薬、生息地管理戦略の組み合わせという3つの柱に基づいています。これらのIPM手法は、アフリカの生物農薬市場の成長を促進する上で重要な役割を果たすと予想されます。

- バイオ殺菌剤は、アフリカ以外の地域の生物農薬市場の主要セグメントであり、2022年の市場規模は4,560万米ドルでした。トリコデルマは他の真菌を酵素的に破壊し、病原性真菌を死滅させる抗微生物物質を生産するため、バイオ殺菌剤として広く使用されています。

- エジプト、南アフリカ、その他のアフリカ地域は、有機農業の作付面積に関するアフリカ地域の主要セグメントです。2022年には、アフリカの有機農地総面積の95.0%を残りのアフリカ地域が占め、120万ヘクタールでした。エジプトは3.5%で4万5,100ヘクタール、南アフリカは1.0%で1万2,600ヘクタールでした。これらの国々では有機農産物の栽培面積が多いため、大きな市場機会があります。

- 有機製品に対する消費者の関心の高まり、農業従事者の意識の高まり、生物農薬を使用することによる経済的利点が、アフリカにおける生物農薬の需要を促進すると予想され、市場は2023~2029年の間にCAGR 9.2%を記録すると予測されます。

アフリカの生物農薬市場動向

この地域の有機セクタには83万4,000の有機生産者がおり、チュニジアの方が有機農地が多いです。

- 2022年、アフリカ地域の有機農地面積は120万ヘクタールを超え、世界の有機農地面積の9.0%を占めました。

- 2020年、アフリカは2019年より14万9,000ヘクタール多い有機栽培地を報告し、約83万4,000人の生産者の存在に伴い、前年比7.7%増を記録しました。チュニジアの有機栽培地が最も多く(2020年には29万ヘクタール以上)、エチオピアの有機生産者数が最も多かった(約22万人)。サントメ・プリンシペの島国は、この地域で有機農業に最も多くの土地を投入しており、農地面積の20.7%が有機作物です。

- アフリカ地域では、換金作物が有機農地に占める割合が大きく、有機農地面積の63.2%を占める81万7,400ヘクタールとなっています。畑作物はアフリカの有機農地で2番目に大きなシェアを占めており、有機農地全体の約25.6%、合計33万1,200ヘクタールにのぼります。園芸作物はアフリカの有機農地総面積の11.2%を占め、2022年には14万4,900ヘクタールとなります。

- 有機農作物の栽培面積が大きいアフリカ諸国には、その他のアフリカ地域セグメント、エジプト、南アフリカが含まれます。2022年には、アフリカ残りの地域が120万ヘクタールでアフリカの有機農業総面積の95.0%を占め、エジプトが4万5,100ヘクタールで3.5%のシェアを占め、南アフリカが1万2,600ヘクタールで1.0%のシェアを占めます。

- アフリカでは2017~2022年の間に有機農業の作付面積が6.9%増加しました。2029年には約52.2%増加し、200万米ドルに達すると予想されます。

一人当たりのオーガニック製品への支出はエジプト、南アフリカ、ナイジェリア諸国が優勢

- アフリカの1人当たり所得は長年にわたって一貫して増加しており、人々は栄養価の高い食品により多くの支出をするようになっています。アフリカ地域では、有機食品と飲食品がより多くの棚に並ぶようになっています。オーガニック認証を受けた農産物の国内消費量は比較的少ないため、オーガニック製品のほとんどは輸出用に生産されています。

- アフリカでは、特にエジプト、南アフリカ、ナイジェリアで有機製品の消費が大幅に増加しています。2021年の有機製品の1人当たり消費額は、エジプトが55.5米ドル、次いで南アフリカが7.1米ドルでした。オーガニック生産者数が最も多い国は、エチオピア(ほぼ22万2,000人)、タンザニア(ほぼ14万9,000人)、ウガンダ(13万9,000人以上)でした。

- アフリカ地域で一般的に消費されている有機製品には、新鮮野菜や果物が含まれます。アフリカでは、有機農業を施策、国の改良普及システム、マーケティング、バリューチェーン開拓の主流に据えるための多大な努力がなされてきました。これらすべての要因が消費者の関心を集めています。

- フルーツジュースを中心とする飲料の1人当たり消費量の増加、健康意識の高まり、化学成分を含まない有機飲料・食品への消費者のシフトに伴い、アフリカの有機食品市場の需要は2023~2029年にかけて拡大すると予想されます。

- しかし、低所得層が多く、有機基準や現地市場認証のためのその他のインフラが整っていないことが、同地域の有機市場成長の主要抑制要因となっています。

アフリカの生物農薬産業概要

アフリカの生物農薬市場はセグメント化されており、上位5社で14.93%を占めています。この市場の主要企業は、Certis USA LLC、Coromandel International Ltd、Koppert Biological Systems Inc.、T. Stanes、Company Limited、UPLなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 有機栽培面積

- 一人当たりのオーガニック製品への支出

- 規制の枠組み

- エジプト

- イラン

- ナイジェリア

- 南アフリカ

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 形態

- バイオ殺菌剤

- バイオ除草剤

- バイオ殺虫剤

- その他の生物農薬

- 作物タイプ

- 換金作物

- 園芸作物

- 耕作作物

- 生産国

- エジプト

- ナイジェリア

- 南アフリカ

- その他のアフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Andermatt Group AG

- Atlantica Agricola

- Biolchim SPA

- Certis USA LLC

- Coromandel International Ltd

- IPL Biologicals Limited

- Koppert Biological Systems Inc.

- T. Stanes and Company Limited

- UPL

- Valent Biosciences LLC

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 500042

The Africa Biopesticides Market size is estimated at 177.6 million USD in 2025, and is expected to reach 298.5 million USD by 2030, growing at a CAGR of 10.94% during the forecast period (2025-2030).

- Biopesticides are naturally occurring substances or agents derived from animals, plants, insects, and microorganisms, including bacteria and fungi, used to manage agricultural pests and infections. The African biopesticides market grew by 23.4% from 2017 to 2022.

- Biopesticide consumption in row crops is higher than other crops in the region, accounting for 73.8% in 2022. Horticultural crops accounted for 19.7%, while cash crops accounted for 6.5% of the overall consumption in the same year.

- The Integrated Pest Management (IPM) concept is important in the African biopesticides market. IPM 1.0 was established decades ago to reduce the overuse of agricultural pesticides. IPM 2.0 gradually incorporated agroecological principles such as biological control and habitat management. However, throughout this period, smallholder farmers did not improve their decision-making skills and continued to rely on hazardous pesticides as their first line of defense. The African region also implemented Integrated Pest Management 3.0 (IPM 3.0), which includes three new features, i.e., real-time farmer decision-making access, pest-management options based on science and nature, and the integration of genomic approaches, biopesticides, and habitat-management practices. These IPM practices may drive the biopesticides market in Africa.

- In collaboration with Real IPM Ltd, the International Centre of Insect Physiology and Ecology commercialized two biopesticides, Campaign (icipe69) and Achieve (icipe78). Campaign (icipe69) is being used against mealybugs, thrips, and fruit flies, in crops such as cucumber, mango, papaya, rose, and tomato. Adoption of IPM practices and increased R&D activities of biopesticides may boost the market value by 84.7% between 2023 and 2029.

- The African biopesticides market has exhibited a growth rate of 15.8% between 2017 and 2021, and this growth is expected to continue with a projected expansion of about 84.7% by 2029.

- This growth is primarily attributed to the launch of Integrated Pest Management 3.0 (IPM 3.0) in Africa. This pest management strategy is based on three pillars: real-time farmer decision-making access, science-based pest-management alternatives, and the combination of genetic methods, biopesticides, and habitat-management strategies. These IPM methods are expected to play a critical role in driving the growth of the African biopesticides market.

- Biofungicides are the dominant segment of the biopesticides market in the Rest of Africa segment, and it was valued at USD 45.6 million in 2022. Trichoderma is widely used as a biofungicide as it destroys other fungi enzymatically and produces anti-microbial substances that kill pathogenic fungi.

- Egypt, South Africa, and the Rest of Africa are the primary segments in the African region regarding organic agriculture acreage. In 2022, the Rest of Africa accounted for 95.0% of total organic agricultural land in Africa, with 1.2 million hectares. Egypt contributed 3.5% with 45.1 thousand hectares, while South Africa accounted for 1.0% with 12.6 thousand hectares. The high organic agricultural acreage in these countries provides significant market opportunities.

- The increasing consumer interest in organic products, growing awareness among farmers, and the economic advantages of using biopesticides are anticipated to drive the demand for biopesticides in Africa, and the market is expected to record a CAGR of 9.2% between 2023 and 2029.

Africa Biopesticides Market Trends

8,34,000 organic producers are in the region's organic sector with Tunisia is having more organic land

- In 2022, the area of organic agricultural land in the African region amounted to over 1.2 million hectares, representing 9.0% of the global organic agricultural area.

- In 2020, Africa reported 149,000 hectares more in organic cultivation land than in 2019, recording a 7.7% increase Y-o-Y in line with the presence of nearly 834,000 producers. Tunisia had the largest amount of organic land (more than 290,000 hectares in 2020), whereas Ethiopia had the highest number of organic producers (almost 220,000). The island states of Sao Tome and Principe have the most significant amount of land committed to organic farming in the region, with 20.7% of their agricultural area dedicated to organic crops.

- In the African region, cash crops account for a significant share of organic agricultural land, amounting to 63.2% of the total organic acreage with 817.4 thousand hectares. Row crops hold the second-largest share of organic acreage in Africa, which amounts to about 25.6% of the total organic acreage, totaling 331.2 thousand hectares. Horticultural crops account for 11.2% of the total organic acreage in Africa, with 144.9 thousand hectares in 2022.

- The African countries with significant organic agricultural acreage include the Rest of Africa regional segment, Egypt, and South Africa. In 2022, the Rest of Africa accounted for 95.0% of the total organic agricultural acreage in Africa, with 1.2 million hectares, Egypt accounted for a 3.5% share with 45.1 thousand hectares, and South Africa accounted for a 1.0% share with 12.6 thousand hectares.

- Organic agricultural acreage rose by 6.9% between 2017 and 2022 in Africa. It is anticipated to increase by about 52.2% and reach USD 2.0 million by 2029.

Per capita spending on organic product predominant in Egypt, South Africa, and Nigeria countries

- Africa's per capita income has consistently increased throughout the years, encouraging people to spend more money on nutritious food. Organic foods and beverages are gaining more shelf space in the African region. Since the domestic consumption of certified organic produce is relatively small, most organic goods are produced for export.

- In Africa, consumption of organic products has increased significantly, especially in Egypt, South Africa, and Nigeria. In 2021, the per capita consumption of organic products was USD 55.5 in Egypt, followed by South Africa with USD 7.1. The countries with the highest number of organic producers were Ethiopia (almost 222,000), Tanzania (nearly 149,000), and Uganda (over 139,000).

- In the African region, commonly consumed organic products include fresh vegetables and fruits. In Africa, significant efforts have been made to mainstream organic agriculture into policy, national extension systems, marketing, and value chain development. All these factors have gained the attention of consumers.

- With the increasing per capita consumption of beverages, primarily fruit juices, growing health awareness, and consumers shifting toward organic drinks and food that do not contain chemical ingredients, the demand for the African organic food market is expected to grow between 2023 and 2029.

- However, low-income levels and a lack of organic standards and other infrastructure for local market certification are the major restraining factors for the growth of the organic market in the region.

Africa Biopesticides Industry Overview

The Africa Biopesticides Market is fragmented, with the top five companies occupying 14.93%. The major players in this market are Certis USA LLC, Coromandel International Ltd, Koppert Biological Systems Inc., T. Stanes and Company Limited and UPL (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 Egypt

- 4.3.2 Iran

- 4.3.3 Nigeria

- 4.3.4 South Africa

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Form

- 5.1.1 Biofungicides

- 5.1.2 Bioherbicides

- 5.1.3 Bioinsecticides

- 5.1.4 Other Biopesticides

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

- 5.3 Country

- 5.3.1 Egypt

- 5.3.2 Nigeria

- 5.3.3 South Africa

- 5.3.4 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Andermatt Group AG

- 6.4.2 Atlantica Agricola

- 6.4.3 Biolchim SPA

- 6.4.4 Certis USA LLC

- 6.4.5 Coromandel International Ltd

- 6.4.6 IPL Biologicals Limited

- 6.4.7 Koppert Biological Systems Inc.

- 6.4.8 T. Stanes and Company Limited

- 6.4.9 UPL

- 6.4.10 Valent Biosciences LLC

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

アフリカの生物農薬:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 149 Pages

- 納期

- 2~3営業日