|

市場調査レポート

商品コード

1693764

中国の生物農薬:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)China Biopesticides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国の生物農薬:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 123 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

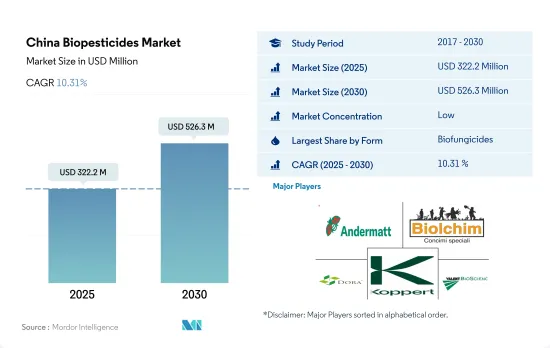

中国の生物農薬市場規模は2025年に3億2,220万米ドルと推定・予測され、2030年には5億2,630万米ドルに達し、予測期間(2025~2030年)のCAGRは10.31%で成長すると予測されます。

- 生物農薬は、動物、植物、昆虫、細菌や真菌を含む微生物に由来する天然由来の物質または薬剤であり、農業害虫や感染症の管理に使用されます。2022年、中国の生物農薬は作物保護市場全体の約47.1%を占めました。

- 中国の生物農薬市場では、生物殺菌剤が最も消費され、55.0%の数量シェアで市場を独占し、次いで生物殺虫剤、その他の生物農薬、生物除草剤が続き、2022年の市場シェアはそれぞれ31.0%、11.5%、2.4%でした。

- 同国では連作作物の栽培が支配的であり、その生物農薬消費量は2022年に約2億480万米ドルと評価されました。これは、同国の主食とされる畑作物の栽培面積が大きいためです。

- 微生物農薬は、細菌、真菌、ウイルス、原生動物、遺伝子組み換えを受けた微生物など、生きた生物を有効成分として含む農薬です。バチルス・チューリンゲンシス、枯草菌、ヘリコベルパ・アルミゲラ核多角体病ウイルス、メタリジウム・アニソプリアエ、パエニバチルス・ポリミキサが、中国における微生物農薬の生産高上位5です。

- 植物農薬は、植物から直接有効成分を抽出した農薬です。現在登録されている植物農薬には、マトリン、ロテノン、アザジラクチン、ベラトラミン、ピレトリンなどがあります。

- 中国では有機食品の需要が高まるにつれて、有機農業も拡大しています。2017~2022年にかけて、有機栽培面積の29.6%が増加しました。有機栽培面積の増加と政府の取り組みにより、2023~2029年にかけて生物農薬の市場規模は増加し、CAGRは10.1%と予測されます。

中国の生物農薬市場動向

農薬使用量のゼロ成長と有機製品輸出の増加が有機栽培を促進

- FiBLとIFOAMの最新報告によると、中国の有機食品市場は年率25.0%で成長しています。プラクティス農法から有機農法への移行は、中国から毎年29億1,000万米ドルの農産食品が輸出されていることを考えると、中国国内におけるよりサステイナブル食糧システムへの変革です。

- 中国で有機農地の面積が急増したのは、所得の増加と食品安全の重要性の高まりにより、より多くの人々が有機製品を購入するようになったためです。過去3年間で、中国の有機栽培面積は10%増加し、2020年には240万haに達します。さらに、有機生産を促進するための国家施策が採択され、「清冽な水と緑豊かな山はかけがえのない資産である」「グリーン開発」というスローガンが提唱されています。

- 中国の有機農業は主に輸出志向です。輸出品目も輸入品目も穀物、大豆、果物、野菜などです。中国の東北3省(遼寧省、吉林省、黒龍江省)は、生産量、数量、面積の面で全国最大の有機生産を支えています。中国北部(山東省や遼寧省など)にある有機農園のほとんどは、有機野菜や果物を近隣の都市に供給しています。さらに、日本、韓国、欧州、米国に輸出する製品もあります。

- 土壌汚染につながる合成肥料や農薬の過剰使用による土壌毒性への懸念が高まるなか、中国ではサステイナブル農業プラクティスや有機食品生産への需要が高まっています。このような栽培方法の変化は緩やかではあるが増加傾向にあり、農作物の栄養・保護製品に対する需要も増加しています。

有機製品に対する需要の高まりにより、中国の消費者の約73%が有機食品を希望しています。

- 中国の有機食品市場は急速に開拓されており、中国の消費者の有機食品に対する潜在需要は莫大です。その背景には、より裕福な中間層の増加と、健康への影響に対する意識の高まりがあります。2021年には、中国の有機食品の売上高は約775億4,000万米ドルに達しました。

- 食品の安全性よりも有機食品を優遇する政府の様々な法律や、従来の食品よりも有機食品を好む顧客の嗜好により、有機食品の需要はかなり拡大しています。中国の有機野菜の価格はプラクティス農産物の3倍から15倍であるのに対し、有機野菜の価格は一般にプラクティス農産物の5倍から10倍です。しかし、価格要因が障壁となっているにもかかわらず、裕福な家庭や健康に問題のある個人は予算を増やしたがっており、中国の消費者の約73%が有機食品に追加料金を支払うことを望んでいます。

- 中国政府は、有機食品セグメントでの自立を徐々に目指しています。例えば、農業従事者が化学肥料の使用を減らし、バイオベースの代替品に切り替えるよう奨励することで、経済は徐々にグリーン農業へと向かっています。2020年に行われた中国チェーンストア・フランチャイズ協会(CCFA)の調査では、サステイナブル食品生産の概念を理解している先進都市の中国人の有機意識は83%に達していると発表されました。中国の有機食品部門はまだかなり小さく、国内外の消費者の需要を満たすにはほど遠いもの、2021年の国内売上が4.01%増加することを考えると、中国の有機食品は国内市場でも海外市場でも大きな可能性を秘めていると言えます。

中国の生物農薬産業概要

中国の生物農薬市場はセグメント化されており、上位5社で0.78%を占めています。この市場の主要企業は、Andermatt Group AG、Biolchim SPA、Dora Agri-Tech、Koppert Biological Systems Inc.、Valent Biosciences LLCなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 有機栽培面積

- 一人当たりのオーガニック製品への支出

- 規制の枠組み

- 中国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 形態

- バイオ殺菌剤

- バイオ除草剤

- バイオ殺虫剤

- その他の生物農薬

- 作物タイプ

- 換金作物

- 園芸作物

- 耕作作物

第6章 競争情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Andermatt Group AG

- Biobest Group NV

- Biolchim SPA

- Dora Agri-Tech

- Henan Jiyuan Baiyun Industry Co. Ltd

- King BIoTec Corp.

- Koppert Biological Systems Inc.

- Valent Biosciences LLC

- Wuhan Taixin Biological Technology Co. Ltd

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 500024

The China Biopesticides Market size is estimated at 322.2 million USD in 2025, and is expected to reach 526.3 million USD by 2030, growing at a CAGR of 10.31% during the forecast period (2025-2030).

- Biopesticides are naturally occurring substances or agents derived from animals, plants, insects, and microorganisms, including bacteria and fungi, used to manage agricultural pests and infections. In 2022, Chinese biopesticides accounted for about 47.1% of the entire crop protection market value.

- In the Chinese biopesticides market, biofungicide was the most consumed biopesticide, dominating the market with a volume share of 55.0%, followed by bioinsecticides, other biopesticides, and bioherbicides, with market shares of 31.0%, 11.5%, 2.4%, respectively, in 2022.

- Row crop cultivation is dominant in the country, and its biopesticides consumption was valued at about USD 204.8 million in 2022. This is due to the large area under cultivation of field crops, which are considered the country's staple food.

- Microbial pesticides are pesticides that contain live organisms as active components, such as bacteria, fungi, viruses, protozoa, or microorganisms that have undergone genetic modification. Bacillus thuringiensis, Bacillus subtilis, Helicoverpa armigera nuclear polyhedrosis virus, Metarhizium anisopliae, and Paenibacillus polymyxa are the top five microbial pesticides in China in terms of manufacturing output.

- Botanical pesticides are pesticides with active components extracted directly from plants. The currently registered botanical pesticides include matrine, rotenone, azadirachtin, veratramine, and pyrethrin.

- Organic farming also expands in China as the demand for organic food rises. From 2017 to 2022, 29.6% of organic acreage increased. Increasing organic acreage and government initiatives are expected to increase the market value of biopesticides between 2023 and 2029, with a projected CAGR of 10.1%.

China Biopesticides Market Trends

Country's zero growth in pesticides use and increasing exports under organic products driving the organic cultivation.

- According to the latest reports by FiBL and the IFOAM, the market for organic food in China is growing at an annual rate of 25.0%. The shift from conventional to organic is a transformation toward a more sustainable food system within China, given the USD 2.91 billion of agri-food commodities exported from China each year.

- The size of organic farmland increased rapidly in China because more people started buying organic products due to increased incomes and the increasing importance of food safety. In the last three years, China's organic planting area increased by 10%, reaching 2.4 million ha in 2020. In addition, national policies have been adopted to promote organic production, advocating the slogans that state, "lucid waters and lush mountains are invaluable assets" and "green development".

- Organic farming in China is majorly export-oriented. The products that are both exported and imported include cereals, soybeans, fruits, and vegetables. China's three northeastern provinces (Liaoning, Jilin, and Heilongjiang) support the largest organic production nationally in terms of output, volume, and area. Most organic farms located in the northern part of China (e.g., Shandong and Liaoning) supply organic vegetables and fruits to nearby cities. In addition, they export some products to Japan, South Korea, Europe, and the United States.

- With the increasing concerns of soil toxicity due to the overuse of synthetic fertilizers and pesticides that lead to soil contamination, the demand for sustainable agriculture practices and organic food production is on the rise in China. This moderately slow yet increasing shift in cultivation practices has also subsequently increased the demand for crop nutrition and protection products.

The growing demand for organic products, approximately 73% of Chinese consumers are willing to have organic food

- China's organic food market is developing rapidly, and the potential demand for organic food among Chinese consumers is enormous. This is due to the growth of the wealthier middle classes and a greater awareness of the health implications. In 2021, organic food sales in China amounted to about USD 77.54 billion.

- Due to various government laws that favor organic food over food safety and customer preferences for organic food over conventional food, the demand for organic food items has considerably expanded. While prices of organic vegetables in China range from 3 to 15 times the cost of conventional produce, prices for organic vegetables are generally between 5 and 10 times that of their conventional counterparts. However, despite the price factor being a barrier, wealthy families and individuals with health problems are eager to increase their budget, with approximately 73% of Chinese consumers willing to pay extra for organic foods.

- The Chinese government is slowly aiming to become self-reliant in the organic food sector. For instance, the economy is slowly moving toward a green agriculture practice by encouraging farmers to scale back the use of chemical fertilizers and switch to bio-based alternatives. The China Chain Store and Franchise Association (CCFA) research in 2020 declared that organic awareness among the Chinese population in developed cities was at 83% when it came to an understanding of the concept of sustainable food production. Although China's organic food sector is still quite small and falls far short of satisfying domestic and international consumer demand, it can be stated that organic food in China has enormous potential in both the domestic and foreign markets, considering the rise in domestic sales by 4.01% in 2021.

China Biopesticides Industry Overview

The China Biopesticides Market is fragmented, with the top five companies occupying 0.78%. The major players in this market are Andermatt Group AG, Biolchim SPA, Dora Agri-Tech, Koppert Biological Systems Inc. and Valent Biosciences LLC (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 China

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Form

- 5.1.1 Biofungicides

- 5.1.2 Bioherbicides

- 5.1.3 Bioinsecticides

- 5.1.4 Other Biopesticides

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Andermatt Group AG

- 6.4.2 Biobest Group NV

- 6.4.3 Biolchim SPA

- 6.4.4 Dora Agri-Tech

- 6.4.5 Henan Jiyuan Baiyun Industry Co. Ltd

- 6.4.6 King Biotec Corp.

- 6.4.7 Koppert Biological Systems Inc.

- 6.4.8 Valent Biosciences LLC

- 6.4.9 Wuhan Taixin Biological Technology Co. Ltd

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms