|

市場調査レポート

商品コード

1693636

欧州の小型商用車電動化:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Electric Light Commercial Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の小型商用車電動化:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 258 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

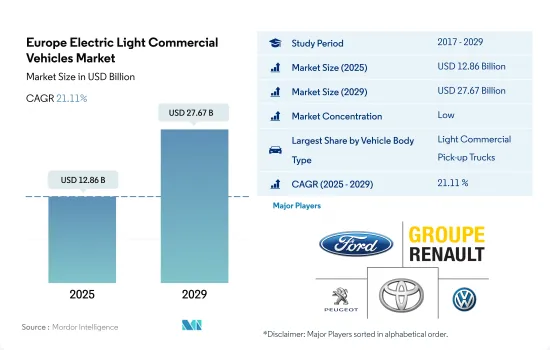

欧州の小型商用車市場規模は2025年に128億6,000万米ドルと推定・予測され、2029年には276億7,000万米ドルに達し、予測期間中(2025-2029年)のCAGRは21.11%で成長すると予測されます。

欧州は、さまざまなビジネスニーズに適した構成を持つ小型商用車の電動化を推進する先駆的な役割を担っています。

- 貨物トラックとバンを特徴とする欧州の小型商用車(ELCV)市場は、持続可能性と電動化へのシフトに牽引され、大きな変革期を迎えています。特にバンセグメントでは、ゼロエミッション車に対する需要の高まりに対応するため、大手自動車メーカーが電気自動車を投入しています。例えば、日産自動車の新型タウンスター・バンのイントロダクションは、e-NV200に代わる戦略的な動きであり、ゼロエミッション車への移行を加速させるよう設計された完全な電気自動車オプションを提供するものです。

- 欧州市場力学は、技術の進歩、規制の枠組み、効率的なラストワンマイル配送ソリューションの需要を高めているeコマースの成長など、さまざまな要因の影響を受けています。しかし市場は、商用車登録台数の全体的な減少や、パンデミックの経済的影響や排出量削減を目的とした規制状況の変化も一因とされるバン販売台数の具体的な落ち込みといった課題に直面しています。

- 欧州のELCV市場には、温室効果ガスの排出削減と都市部の大気質改善への関心の高まりに支えられたいくつかの機会があります。2030年までに欧州全域に6つのバッテリー工場を設立するというフォルクスワーゲンの計画のような取り組みは、電気自動車のエコシステム拡大に対する業界のコミットメントを強調するものです。さらに、持続可能なELCVを開発するためにパンチパワートレインがグルアウと合意したような、この分野での協力や革新は、電気バンや電気トラックが商業輸送の中心的役割を果たす未来を示唆しています。

欧州の小型商用車市場における新興諸国の開発は、電動化への取り組みにおける欧州大陸のリーダーシップを示すものです。

- 世界全体では、商用車の年間販売台数は1,770万台に達しました。290万台以上のバン、トラック、バスの新車登録台数で、欧州は世界の16.4%を占めています。消費者の購買習慣は、環境問題への関心の高まり、2030年までに内燃機関を禁止するという政府の計画、燃費効率やゼロエミッションといった環境に優しい自動車の利点に対する一般的な理解により、電気自動車を支持する方向にシフトしています。

- COVID-19の大流行は、文化と経済に比類なき影響を及ぼしています。自動車産業も大きな影響を受けており、復興にはまだ時間がかかりそうで、課題も山積しています。にもかかわらず、イタリア政府は2025年から電気自動車の普及が大幅に拡大すると予測し続けています。さらに、欧州委員会は2019年12月、汎欧州的な研究・革新プロジェクトに対し、加盟7カ国から32億ユーロの公的資金を拠出することを承認しました。これは、リチウムイオン電池の高度に革新的で持続可能な技術開発を促進するもので、電池のバリューチェーン全体に沿った最初の産業展開に至るまでの研究開発活動を含みます。

- 政府は、今後数年間で電気自動車の普及を加速させるため、バッテリー、車両、充電ステーション、デジタルモビリティアプリ、ICT、スマートモビリティ、エネルギーサービスの開発を優先しています。電気商用車の需要は、eコマースと物流活動の成長により増加すると予想されます。

欧州の小型商用車市場の動向

環境問題、政府支援、脱炭素目標が欧州の電気自動車需要と販売に拍車

- 欧州諸国における電気自動車の需要と販売は、過去数年間で大きく伸びています。ドイツは2022年に電気自動車の販売台数が2021年比で22%増加し、次いで英国が2022年に2021年比で18.40%増加しました。環境問題への関心の高まり、政府の厳しい規範、燃費の良さ、サービスコストの低さ、二酸化炭素排出量の少なさといった電気自動車の利点、政府による補助金などが、欧州諸国における電気自動車の成長に寄与している要因のひとつです。

- 電気商用車、特に小型トラックの需要は、欧州諸国で徐々に伸びています。さらに、各国の政府も電気自動車の導入を支援しています。2021年11月、英国政府は2040年までにすべての大型車をゼロ・エミッションにするという公約を発表しました。このような要因により、英国における2022年の電気商用車販売台数は2021年比で23.17%増加し、各国における同様の慣行が欧州全体の電気商用車需要を高めています。

- 欧州諸国における車両の電動化は、今後数年間で飛躍的に成長すると予測されています。脱炭素化に向けた各国政府の取り組みが、欧州の電気商用車市場を牽引すると予想されます。例えば、2022年1月、ドイツの運輸大臣は、2030年までに1,500万台の電気自動車を走らせるという目標を発表しました。このような要因により、欧州諸国では2024年から2030年にかけて電気自動車の販売が増加すると予想されます。

欧州の小型商用車産業の概要

欧州の小型商用車市場は細分化されており、上位5社で32.16%を占めています。この市場の主要企業は以下の通り。 Ford Motor Company, Groupe Renault, Peugeot S.A., Toyota Motor Corporation and Volkswagen AG(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 人口

- 一人当たりGDP

- 自動車購入のための消費者支出(cvp)

- インフレ率

- 自動車ローン金利

- 電化の影響

- EV充電ステーション

- バッテリーパック価格

- Xev新モデル発表

- 物流性能指数

- 燃料価格

- OEM生産統計

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 車両構成

- 小型商用車

- 燃料カテゴリー

- BEV

- FCEV

- HEV

- PHEV

- 国名

- オーストリア

- ベルギー

- チェコ共和国

- デンマーク

- エストニア

- フランス

- ドイツ

- アイルランド

- イタリア

- ラトビア

- リトアニア

- ノルウェー

- ポーランド

- ロシア

- スペイン

- スウェーデン

- 英国

- その他欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADDAX MOTORS NV.

- ARRIVAL LTD.

- Daimler AG(Mercedes-Benz AG)

- Fiat Chrysler Automobiles N.V

- Ford Motor Company

- Groupe Renault

- Maxus

- Nissan Motor Co. Ltd.

- Peugeot S.A.

- Toyota Motor Corporation

- Volkswagen AG

- Volvo Group

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Europe Electric Light Commercial Vehicles Market size is estimated at 12.86 billion USD in 2025, and is expected to reach 27.67 billion USD by 2029, growing at a CAGR of 21.11% during the forecast period (2025-2029).

Europe has a pioneering role in driving the adoption of electric light commercial vehicles with configurations suited to various business needs

- The European electric light commercial vehicles (ELCVs) market, characterized by cargo trucks and vans, is undergoing significant transformations driven by a shift toward sustainability and electrification. The van segment, in particular, has seen notable activity, with major automotive players introducing electric variants to cater to the rising demand for zero-emission vehicles. For example, Nissan's introduction of the all-new Townstar van represents a strategic move to replace the e-NV200, offering a fully electric option designed to accelerate the transition to zero-emission motoring.

- The European market's dynamics are influenced by various factors, including technological advancements, regulatory frameworks, and the growth of e-commerce, which has increased the demand for efficient last-mile delivery solutions. However, the market has faced challenges, such as the overall decline in commercial vehicle registrations and the specific downturn in van sales, attributed partly to the economic impact of the pandemic and the changing regulatory landscape aimed at reducing emissions.

- The ELCV market in Europe presents several opportunities, underpinned by the growing emphasis on reducing greenhouse gas emissions and improving urban air quality. Initiatives like Volkswagen's plan to set up six battery factories across Europe by 2030 underscore the industry's commitment to expanding the electric vehicle ecosystem. Additionally, collaborations and innovations in the sector, such as Punch Powertrain's agreement with Gruau to develop sustainable ELCVs, signal a future where electric vans and trucks play a central role in commercial transportation.

Country-specific developments in the European electric light commercial vehicles market are showcasing the continent's leadership in electrification efforts

- Globally, sales of commercial vehicles reached a total of 17.7 million each year. With more than 2.9 million new vans, trucks, and buses, Europe accounts for 16.4% of global registrations. Consumer purchasing habits have shifted in favor of electric vehicles due to increasing environmental concerns, the government's plan to ban internal combustion engines by 2030, and a general understanding of the benefits of eco-friendly vehicles, such as fuel efficiency and zero emissions.

- The COVID-19 pandemic has had unparalleled repercussions on culture and the economy. The automobile industry has experienced significant effects, and the recovery process is still expected to be drawn out and challenging. Despite this, the Italian government continues to predict that starting in 2025, the use of electric vehicles will significantly expand. Additionally, the European Commission approved public financing of EUR 3.2 billion in December 2019 from seven Member States for pan-European research and innovation projects. This promotes the development of highly innovative and sustainable technologies for lithium-ion batteries, involving R&I activities up to the first industrial deployment along the entire battery value chain.

- The government has prioritized the development of batteries, vehicles, charging stations, digital mobility apps, ICT, smart mobility, and energy services to accelerate the adoption of electric vehicles in the coming years. The demand for electric commercial vehicles is anticipated to increase due to the growth of e-commerce and logistical activities.

Europe Electric Light Commercial Vehicles Market Trends

Environmental concerns, government support, and decarbonization goals fuel European electric vehicle demand and sales

- The demand and sales of electric vehicles in European countries have grown significantly over the past few years. Germany witnessed a growth in the sales of electric cars by 22% in 2022 over 2021, followed by the United Kingdom with an 18.40% increase in 2022 over 2021. Growing environmental concerns, stringent governmental norms, advantages of electric vehicles such as fuel efficiency, low service cost, no carbon emissions, and subsidies by the government are some of the factors contributing to the growth of electric vehicles in European countries.

- The demand for electric commercial vehicles, especially light trucks, is growing gradually in European countries. Moreover, the governments of various countries are also supporting the adoption of electric vehicles. In November 2021, the government of the United Kingdom announced a pledge that all heavy-duty vehicles would be zero-emission by the year 2040. Such factors have increased the sales of electric commercial vehicles in the United Kingdom by 23.17% in 2022 over 2021, and similar practices in various countries are enhancing the demand for electric commercial vehicles across Europe.

- It is projected that the electrification of vehicles in European countries is expected to grow tremendously in the next few years. The efforts of the governments in the regions for decarbonization are expected to drive the electric commercial vehicle market in Europe. For instance, in January 2022, the transport minister of Germany announced a goal to put 15 million electric vehicles on the road by 2030. Such factors are expected to increase the sales of electric vehicles during the 2024-2030 period in European countries.

Europe Electric Light Commercial Vehicles Industry Overview

The Europe Electric Light Commercial Vehicles Market is fragmented, with the top five companies occupying 32.16%. The major players in this market are Ford Motor Company, Groupe Renault, Peugeot S.A., Toyota Motor Corporation and Volkswagen AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.2 GDP Per Capita

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.4 Inflation

- 4.5 Interest Rate For Auto Loans

- 4.6 Impact Of Electrification

- 4.7 EV Charging Station

- 4.8 Battery Pack Price

- 4.9 New Xev Models Announced

- 4.10 Logistics Performance Index

- 4.11 Fuel Price

- 4.12 Oem-wise Production Statistics

- 4.13 Regulatory Framework

- 4.14 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Configuration

- 5.1.1 Light Commercial Vehicles

- 5.2 Fuel Category

- 5.2.1 BEV

- 5.2.2 FCEV

- 5.2.3 HEV

- 5.2.4 PHEV

- 5.3 Country

- 5.3.1 Austria

- 5.3.2 Belgium

- 5.3.3 Czech Republic

- 5.3.4 Denmark

- 5.3.5 Estonia

- 5.3.6 France

- 5.3.7 Germany

- 5.3.8 Ireland

- 5.3.9 Italy

- 5.3.10 Latvia

- 5.3.11 Lithuania

- 5.3.12 Norway

- 5.3.13 Poland

- 5.3.14 Russia

- 5.3.15 Spain

- 5.3.16 Sweden

- 5.3.17 UK

- 5.3.18 Rest-of-Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 ADDAX MOTORS NV.

- 6.4.2 ARRIVAL LTD.

- 6.4.3 Daimler AG (Mercedes-Benz AG)

- 6.4.4 Fiat Chrysler Automobiles N.V

- 6.4.5 Ford Motor Company

- 6.4.6 Groupe Renault

- 6.4.7 Maxus

- 6.4.8 Nissan Motor Co. Ltd.

- 6.4.9 Peugeot S.A.

- 6.4.10 Toyota Motor Corporation

- 6.4.11 Volkswagen AG

- 6.4.12 Volvo Group

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms