|

市場調査レポート

商品コード

1693642

アジア太平洋の電気商用車市場:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Asia Pacific Electric Commercial Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋の電気商用車市場:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 240 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

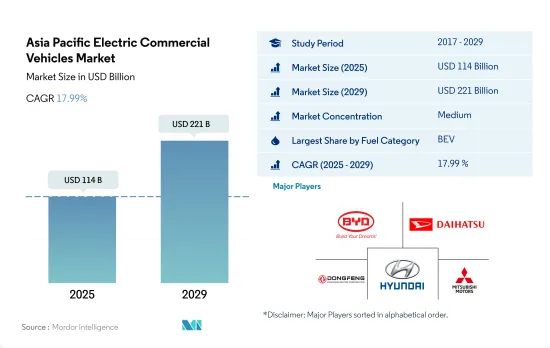

アジア太平洋の電気商用車市場規模は、2025年に1,140億米ドルと推定され、2029年には2,210億米ドルに達すると予測され、予測期間中(2025~2029年)のCAGRは17.99%で成長する見込みです。

アジア太平洋におけるハイブリッドと電気商用車の普及は、2030年までに3倍以上になると予想される

- よりエコフレンドリー輸送ソリューションへのアジア太平洋の移行は、2022~2023年にかけてハイブリッドと電気商用車(CV)セグメントで顕著に表れています。ハイブリッド車と電気自動車の登録台数は大幅に増加し、2021年の264,007台から2022年には490,958台に達しました。この数字は、以前の低迷からの回復を意味するだけでなく、環境問題への関心が高まり、政府の施策が進歩する中で、これらのクリーンな技術への強い嗜好を裏付けています。

- 過去のデータが興味深い背景を示しています。2017~2019年にかけて、ハイブリッド車と電気自動車を合わせた登録台数は、260,519台から188,118台へと緩やかな減少傾向にありました。この落ち込みは、インフラの準備状況、車両の価格帯、初期のためらいといった要因によるもの可能性があります。しかし、その後の数年間、特に2022年には、数字が劇的に復活し、よりクリーンなCVソリューションを通じて排出ガスと闘うという、この地域の迅速な適応姿勢が強調されました。

- 将来を予測すると、アジア太平洋におけるハイブリッド車と電気自動車は、驚くほど楽観的な上昇軌道を描いています。2025年までに、その数は926,761台を超えると推定されています。2030年には、総登録台数は1,677,598台に達すると予想されています。この予測は、技術的躍進、成熟した充電インフラ、総所有コストの削減、持続可能性目標の達成において電気商用車が果たす重要な役割の認識によるものです。

アジア太平洋の電気商用車市場は、厳しい排ガス規制と、よりエコフレンドリー公共・物流輸送ソリューションの強力な推進に後押しされ、急速に拡大する態勢にあります。

- アジア太平洋は、多様な経済、急速に進む都市化、二酸化炭素排出量削減への関心の高まりにより、電気商用車にとって最もダイナミックな市場の一つとなっています。市場情勢は国によって大きく異なり、経済発展、政府の施策、インフラの整備状況、産業の採用率の違いを反映しています。電気自動車技術の世界的リーダーである中国は、積極的な政府施策、充電インフラへの多額の投資、幅広い国内メーカーの恩恵を受けて、アジア太平洋のECV市場を独占しています。

- 日本や韓国など、この地域の他の国々も電気商用車市場で大きく前進しています。自動車産業が確立している日本は、BEVと並ぶECVの広範な戦略の一環として、水素燃料電池車に注力しています。水素社会」の実現に向けた日本のコミットメントは、商用車セグメントの電動化への取り組みを補完するものです。一方、韓国はバッテリー技術とインフラ開発を急速に進めています。

- 対照的に、インド、インドネシア、タイなど、この地域の新興国はECV導入の初期段階にあり、限られたインフラや高い初期費用といった課題に直面しています。しかし、これらの国々は、都市化の進展、環境問題に対する意識の高まり、電気自動車の利用促進を目的とした政府の取り組みにより、ECV市場成長の大きな可能性を秘めています。例えばインドは、インフラ整備と購入者への補助金支給の両方に重点を置き、電気自動車の普及を促進するために複数のイニシアチブを打ち出しています。

アジア太平洋の電気商用車市場動向

アジア太平洋の急速な電気自動車需要と販売増は、政府のイニシアティブと商用車の電動化が原動力

- アジア太平洋では近年、電気自動車(EV)の需要と販売が急増しています。主要市場である中国は、2022年の電気自動車販売台数が2021年比で2.90%増加し、日本は同期間に11.11%増加しました。この動向を後押ししている要因には、環境問題への関心の高まり、厳しい規制、燃費効率、維持費の削減、二酸化炭素排出ゼロといったEVの利点などがあります。政府の補助金は、アジア諸国におけるEVの採用をさらに後押ししています。

- 従来型の燃料を使用する商用車、特にトラックやバスは、アジア太平洋諸国の汚染レベル上昇の一因となっています。これに対し、この地域の多くの国々は、二酸化炭素排出量の抑制を目指し、内燃機関(ICE)車を電気自動車に移行させるために多額の投資を行っています。例えば、2020年12月、インドネシアで自治体バスを運行するトランスジャカルタは、2030年までに電気バス(Eバス)車両を10,000台に拡大するという野心的な計画を発表しました。このような地域全体の取り組みが、商用車の電動化を推進しています。

- アジア太平洋各国の政府機関は、化石燃料自動車を段階的に廃止する措置を積極的に提案しており、この動きは電気商用車市場を強化する構えです。注目すべき開発では、2022年5月、タタ・モーターズがインドで、FAME 2スキームの下で5,450台、500億インドルピー相当の電気バスを供給する政府契約を獲得しました。さらに同社は、大手eコマース企業6社に小型電気トラック2万台を納入する計画を発表しました。EVセグメントにおけるこうした進歩は、2024~2030年にかけて、アジア太平洋における電気商用車の需要をさらに促進すると予想されます。

アジア太平洋の電気商用車産業概要

アジア太平洋の電気商用車市場は適度に統合されており、上位5社で48.55%を占めています。この市場の主要企業は、BYD Auto、Daihatsu Motor、Dongfeng Motor Corporation、Hyundai Motor Company、Mitsubishi Motors Corporationなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 人口

- 一人当たりGDP

- 自動車購入のための消費者支出(cvp)

- インフレ率

- 自動車ローン金利

- 電化の影響

- EV充電ステーション

- バッテリーパック価格

- Xev新モデル発表

- 物流性能指数

- 燃料価格

- OEM生産統計

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 車体タイプ

- バス

- 大型商用トラック

- 小型商用ピックアップトラック

- 小型商用バン

- 中型商用トラック

- 燃料カテゴリー

- BEV

- FCEV

- HEV

- PHEV

- 国名

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- 韓国

- タイ

- その他のアジア太平洋

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- BYD Auto Co. Ltd.

- Daihatsu Motor Co. Ltd.

- Dongfeng Motor Corporation

- Higer Bus Company Ltd.

- Hino Motors Ltd.

- Hyundai Motor Company

- Mahindra & Mahindra Limited

- Mitsubishi Motors Corporation

- Tata Motors Limited

- Zhengzhou Yutong Bus Co. Ltd.

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

The Asia Pacific Electric Commercial Vehicles Market size is estimated at 114 billion USD in 2025, and is expected to reach 221 billion USD by 2029, growing at a CAGR of 17.99% during the forecast period (2025-2029).

The adoption of hybrid and electric commercial vehicles in Asia-Pacific is expected to be more than triple by 2030

- Asia-Pacific's transition toward greener transportation solutions has been pronouncedly evident in the hybrid and electric commercial vehicle (CV) sector between 2022 and 2023. The collective figures for hybrid and electric CV registrations rose significantly, reaching 490,958 units in 2022 from the previous 264,007 units in 2021. These numbers signify not only a rebound from the prior slump but also underline a strong preference for these cleaner technologies amid escalating environmental concerns and progressive governmental policies.

- Historical data provides an intriguing context. From 2017 to 2019, the combined registrations for hybrid and electric CVs experienced a gentle downward trend, from 260,519 units to 188,118 units. This dip might be attributed to factors like infrastructure readiness, vehicle price points, and initial hesitations. However, the next few years, especially 2022, saw a dramatic resurrection in the numbers, emphasizing the region's fast-adapting stance to combat emissions through cleaner CV solutions.

- Projecting into the future, the upward trajectory for hybrid and electric CVs in Asia-Pacific is remarkably optimistic. By 2025, it is estimated the numbers will cross the 926,761 units mark. By 2030, the total registrations are anticipated to reach an impressive 1,677,598 units. This forecasted upswing can be attributed to technological breakthroughs, a matured charging infrastructure, reduced total cost of ownership, and the realization of the critical role these vehicles play in achieving sustainability goals.

The Asia-Pacific electric commercial vehicles market is poised for rapid expansion, fueled by stringent emission regulations and a robust push for greener public and logistic transport solutions

- Asia-Pacific represents one of the most dynamic markets for electric commercial vehicles due to its diverse economies, rapidly growing urbanization, and increasing focus on reducing carbon emissions. The market landscape varies significantly by country, reflecting differences in economic development, government policies, infrastructure readiness, and industry adoption rates. China, as a global leader in electric vehicle technology, dominates the ECV market in Asia Pacific, benefiting from aggressive government policies, substantial investments in charging infrastructure, and a wide range of domestic manufacturers.

- Other countries in the region, such as Japan and South Korea, are also making significant strides in the electric commercial vehicle market. Japan, with its well-established automotive industry, is focusing on hydrogen fuel cell vehicles as part of its broader strategy for ECVs alongside BEVs. The country's commitment to creating a 'hydrogen society' complements its efforts in electrifying its commercial vehicle segment. South Korea, on the other hand, is rapidly advancing in battery technology and infrastructure development.

- In contrast, emerging economies in the region, such as India, Indonesia, and Thailand, are in the earlier stages of ECV adoption, facing challenges such as limited infrastructure and higher upfront costs. However, these countries hold significant potential for growth in the ECV market due to increasing urbanization, rising awareness of environmental issues, and government initiatives aimed at encouraging the use of electric vehicles. India, for example, has launched multiple initiatives to boost EV adoption, focusing on both improving infrastructure and offering subsidies to buyers.

Asia Pacific Electric Commercial Vehicles Market Trends

APAC's rapid electric vehicle demand and sales growth are driven by government initiatives and commercial vehicle electrification

- Electric vehicle (EV) demand and sales have surged in the APAC region in recent years. China, the dominant market, saw a 2.90% rise in electric car sales in 2022 compared to 2021, while Japan experienced an 11.11% increase during the same period. Factors driving this trend include mounting environmental concerns, stringent regulations, and the advantages of EVs, such as fuel efficiency, lower maintenance costs, and zero carbon emissions. Government subsidies further bolster the adoption of EVs in Asian nations.

- Conventional fuel-powered commercial vehicles, notably trucks and buses, are contributing to the escalating pollution levels in several Asia-Pacific countries. In response, many nations in the region are making substantial investments to transition their internal combustion engine (ICE) vehicles to electric ones, aiming to curb carbon emissions. For instance, in December 2020, TransJakarta, a city-owned bus operator in Indonesia, unveiled an ambitious plan to expand its electric bus (e-bus) fleet to 10,000 units by 2030. Such initiatives across the region are propelling the electrification of commercial vehicles.

- Government bodies in various APAC countries are actively proposing measures to phase out fossil fuel vehicles, a move that is poised to bolster the market for electric commercial vehicles. In a notable development, in May 2022, Tata Motors secured a government contract in India to supply 5,450 electric buses worth INR 5,000 crore under the FAME 2 scheme. Additionally, the company announced plans to deliver 20,000 light electric trucks to six major e-commerce players. These advancements in the EV space are anticipated to further fuel the demand for electric commercial vehicles in the APAC region from 2024 to 2030.

Asia Pacific Electric Commercial Vehicles Industry Overview

The Asia Pacific Electric Commercial Vehicles Market is moderately consolidated, with the top five companies occupying 48.55%. The major players in this market are BYD Auto Co. Ltd., Daihatsu Motor Co. Ltd., Dongfeng Motor Corporation, Hyundai Motor Company and Mitsubishi Motors Corporation (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.2 GDP Per Capita

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.4 Inflation

- 4.5 Interest Rate For Auto Loans

- 4.6 Impact Of Electrification

- 4.7 EV Charging Station

- 4.8 Battery Pack Price

- 4.9 New Xev Models Announced

- 4.10 Logistics Performance Index

- 4.11 Fuel Price

- 4.12 Oem-wise Production Statistics

- 4.13 Regulatory Framework

- 4.14 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Body Type

- 5.1.1 Buses

- 5.1.2 Heavy-duty Commercial Trucks

- 5.1.3 Light Commercial Pick-up Trucks

- 5.1.4 Light Commercial Vans

- 5.1.5 Medium-duty Commercial Trucks

- 5.2 Fuel Category

- 5.2.1 BEV

- 5.2.2 FCEV

- 5.2.3 HEV

- 5.2.4 PHEV

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Malaysia

- 5.3.7 South Korea

- 5.3.8 Thailand

- 5.3.9 Rest-of-APAC

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 BYD Auto Co. Ltd.

- 6.4.2 Daihatsu Motor Co. Ltd.

- 6.4.3 Dongfeng Motor Corporation

- 6.4.4 Higer Bus Company Ltd.

- 6.4.5 Hino Motors Ltd.

- 6.4.6 Hyundai Motor Company

- 6.4.7 Mahindra & Mahindra Limited

- 6.4.8 Mitsubishi Motors Corporation

- 6.4.9 Tata Motors Limited

- 6.4.10 Zhengzhou Yutong Bus Co. Ltd.

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms