電気商用車:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Electric Commercial Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1689817

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

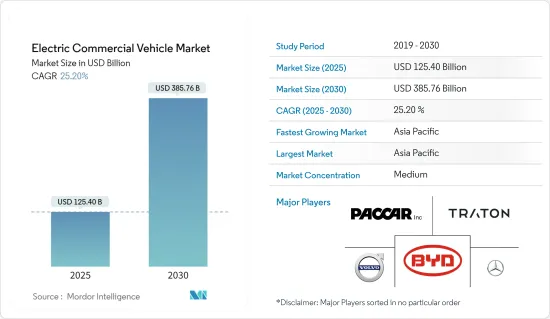

電気商用車の市場規模は2025年に1,254億米ドルと推定され、予測期間(2025-2030年)のCAGRは25.2%で、2030年には3,857億6,000万米ドルに達すると予測されます。

中期的には、多くの新興諸国、特にロジスティクスとサプライ・チェーン分野で電気自動車の利用が普及すると予想されます。世界の厳しい環境規制により、多くの企業が電気自動車への切り替えを余儀なくされており、市場の成長をさらに後押ししています。

自動車メーカー各社は、温室効果ガスの排出に取り組むよう、世界各国の政府から圧力をかけられています。これには、ディーゼル燃料の燃焼による炭素排出を削減し、電気自動車の進歩に投資することが含まれます。

環境に優しい輸送やよりクリーンなエネルギーに対する世界の関心の高まりにより、電気商用車の魅力が急上昇しています。しかし消費者は、航続距離の制限、高価格、利用可能なモデルの不足、知識不足といった課題に直面しています。これらの問題は、販促キャンペーンや政府の規制を通じて徐々に解決されつつあります。

電気商用車市場の主な原動力は、都市部の公害と化石燃料への依存を減らす必要性です。電気商用車市場は現在、世界最大の市場です。中国、インド、日本は、今後数年間で電気商用車市場に貢献する主要国です。

電気商用車市場の動向

バスが大きな市場シェアを占める

燃料費はどの車両にとっても大きな出費です。燃料価格が上昇を続ける中、公共交通機関用に電気バスを選択することで、燃料費が減少し、初期費用と全体的な所有費用が削減されます。2030年までに、電気バスの価格はディーゼル燃料バスの価格まで下がると予想されています。電気バスは、ディーゼルエンジンバスと比較して、維持・運行コストを81~83%削減できます。

大気汚染と気候変動に対する市民の意識の高まりとディーゼル燃料価格の着実な上昇が、多くの州や市の交通当局を動かし、クリーンな公共交通ソリューションを地域開発戦略に組み込むことを優先させています。

電気バスは、ガソリン・バスやディーゼル・バスに比べて、乗客に優れた快適性を提供します。従来のディーゼル・バスとは異なり、電気バスは騒音、振動、ハーシュネス(NVH)のレベルを最小限に抑え、乗客の全体的な移動体験を向上させる。

米国では、環境保護庁(EPA)と高速道路交通安全局(NHTSA)がSAFE(Safer Affordable Fuel-Efficient Vehicles)規則を導入しました。この規則は、乗用車と商用車の平均燃費と温室効果ガスの排出に関する要件を定めたものです。

ゼロ・エミッション車(ZEV)プログラムは、自動車メーカーに対し、電気自動車、ハイブリッド車、燃料電池車を搭載した商用車や乗用車など、環境に優しいゼロ・エミッション車を一定台数販売することを義務付けるものです。ZEVプログラムの目標は、2030年までにバスを含む1,200万台のゼロ・エミッション車を国内の道路を走らせることです。

世界の自動車メーカーは、顧客の多様なニーズに応えるため、革新的な自動車を生み出してきました。例えば

- 2023年9月、インドと米国は共同で、インドで最大1万台の電気バスを発売し、同国の公共交通システムに大きな変革をもたらしました。

以上のような世界各地での開発により、電気バスの需要は今後数年間で拡大する可能性が高いです。

アジア太平洋が市場をリードする見込み

中国政府は電気自動車の利用を促進しており、トラクターや建設機械に使用されるディーゼル燃料を段階的に廃止する計画を発表しています。2035年までに、中国で販売される新車はすべて新エネルギーを動力源としなければならないです。その半分は電気自動車、燃料電池車、プラグイン・ハイブリッド車でなければならないです。

中国全土でEV充電ステーションの設置が進んでいることから、主要地域では電気バスの需要が高まる可能性があります。全国的な電気バスメーカーの拡大が、予測期間中の市場を牽引する可能性が高いです。

中国では、BYDやSAICなどの商用車メーカーが全国に強力な研究開発施設を持ち、大きな存在感を示しています。この動向は、予測期間中に有利な市場機会を生み出す可能性が高いです。例えば

- 2023年10月、Starship Chinaコンセプト・トラックが一汽集団有限公司とシェル・チャイナ社によって共同開発され、正式に発売されました。

インドの州政府は、ICEバスを転換して運用コストを削減すると同時に、二酸化炭素排出量を削減し、大気の質を改善するために、電気バスを車両に含めています。例えば

- 2024年5月、インド政府は、国全体でゼロ・エミッション交通を促進するため、都市間および州間の移動に電気バスを導入するインセンティブを与える計画を発表しました。

日本には、地球上で最も進んだ電気自動車のエコシステムがあります。トヨタや日産のような大手企業は、国内で電気自動車を開発・製造するために目覚しい措置を講じています。

EV充電ステーションの多さは、ガソリン・ディーゼル・コンセントの数を上回っており、ハイブリッド車・電気自動車市場の進展を示しています。こうした好条件は、日本の商用電気自動車市場と需要に拍車をかけると予想されます。さらに、政府の資金援助も日本の商用電気自動車市場の成長を支えています。

このような地域全体の開発により、電気商用車の需要は今後数年で拡大する可能性が高いです。

電気商用車産業の概要

電気商用車市場は、BYD Motors Inc.、AB Volvo、Daimler Truck AG、Paccar Inc.など複数の主要企業によって支配されています。電気商用車メーカーの全国的な急拡大と主要国での新モデルの導入により、予測期間中に市場が大きく成長することが期待されます。例えば

- 2024年4月、Daimler Truck AGのブランドであるRizonは、カナダでクラス4-5の電気トラックを導入しました。同社はe16L、e16M、e18L、e18Mの4種類のバッテリー電気トラックを提供し、GVWは7.25トンから8.55トンです。

- 2023年10月、湖南省長沙市で開催されたブランド刷新・新製品発表会で、次世代小型トラック「オーマーク」と次世代マイクロトラック「ワンダー」を発表。

- 2023年6月、バイエルン州政府はMANトラック・バスの5つの資金調達プロジェクトのうち4つを承認しました。この資金援助は、電気トラック・バス用の高電圧バッテリーの開発を支援するものです。ニュルンベルクの拠点では、2,684万米ドルの政府補助金が支給されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 厳しい排ガス規制が市場成長を促進

- 市場抑制要因

- 電気商用車の高コストが成長を妨げる可能性

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(金額ベース)

- 車両タイプ別

- バス

- トラック

- ピックアップトラック

- バン

- 推進別

- バッテリー電気自動車

- プラグイン・ハイブリッド電気自動車

- 燃料電池電気自動車

- 出力別

- 150kW未満

- 150~250 kW

- 250kW以上

- 地域別

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- 韓国

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- BYD Motors Inc.

- AB Volvo

- Traton SE

- Daimler Truck AG

- Zhengzhou Yutong Bus Co. Ltd

- Ford Motor Company

- Tesla Inc.

- Proterra Inc.

- Rivian Automotive Inc.

- Tata Motor Limited

- Olectra Greentech Limited

- Paccar Inc.

第7章 市場機会と今後の動向

第8章 各地域における電気自動車充電インフラ開発の概要

目次

The Electric Commercial Vehicle Market size is estimated at USD 125.40 billion in 2025, and is expected to reach USD 385.76 billion by 2030, at a CAGR of 25.2% during the forecast period (2025-2030).

Over the medium term, the use of electric vehicles is expected to become more popular in many developing countries, especially in the logistics and supply chain sectors. Strict environmental regulations worldwide are compelling many companies to switch to electric vehicles, further driving the market's growth.

Automakers face growing pressure from governments worldwide to tackle greenhouse gas emissions. This involves cutting carbon emissions from diesel fuel combustion and investing in the advancement of electric vehicles.

The growing worldwide interest in eco-friendly transportation and cleaner energy has caused a surge in the appeal of electric commercial vehicles. However, consumers have encountered challenges such as limited vehicle range, high prices, a lack of available models, and insufficient knowledge. These issues are slowly being addressed through promotional campaigns and government regulations.

The electric commercial vehicle market is mainly driven by the need to reduce urban pollution and dependence on fossil fuels. It is currently the world's largest market for such vehicles. China, India, and Japan are the leading countries contributing to the electric commercial vehicle market in the years to come.

Electric Commercial Vehicle Market Trends

Buses Hold a Major Market Share

The cost of fuel is a significant expense for any vehicle. As fuel prices continue to rise, opting for an electric bus for public transportation decreases fuel expenses and reduces initial costs and overall ownership expenses. By 2030, the prices for electric buses are expected to come down to that of diesel fuel buses. Electric buses help reduce 81-83% of the maintenance and operating costs compared to a diesel-engine bus.

The growing public consciousness of air pollution and climate change, along with the steady rise in diesel prices, has motivated many state and city transportation authorities to prioritize the integration of clean public transportation solutions into their regional development strategies.

Electric buses provide a superior level of comfort for passengers compared to gasoline or diesel buses. Unlike traditional diesel buses, electric buses have minimal levels of noise, vibration, and harshness (NVH), enhancing the overall travel experience for passengers.

In the United States, the Environmental Protection Agency (EPA) and the National Highway Traffic Safety Administration (NHTSA) introduced the Safer Affordable Fuel-Efficient (SAFE) vehicles rule. This regulation establishes the requirements for the average fuel efficiency and emissions of greenhouse gases for both passenger and commercial vehicles.

The Zero-emission Vehicles (ZEV) Program mandates that vehicle manufacturers must sell a certain number of eco-friendly and zero-emission vehicles, which include electric, hybrid, and fuel cell-powered commercial and passenger vehicles. The ZEV program's goal is to have 12 million zero-emission vehicles, including buses, on the roads in the country by 2030.

Worldwide, automobile manufacturers have created innovative vehicles to meet the diverse needs of their customers. For instance:

- In September 2023, India and the United States joined forces to launch up to 10,000 electric buses in India, creating a significant transformation in the country's public transportation system.

With the above-mentioned developments across the world, the demand for electric buses is likely to grow in the coming years.

Asia-Pacific is Expected to Lead the Market

The Chinese government is promoting the use of electric vehicles and has announced plans to phase out diesel fuel used in tractors and construction equipment. By 2035, all new vehicles sold in China must be powered by new energy. Half of these vehicles must be electric, fuel cell, or plug-in hybrid, with the other half being hybrid vehicles.

The increasing installation of EV charging stations throughout China may lead to a higher demand for electric buses in major regions. The expansion of electric bus manufacturers across the country will likely drive the market during the forecast period.

China has a major presence of commercial vehicle manufacturers, such as BYD Co. Ltd and SAIC, with strong R&D facilities nationwide. This trend will likely create lucrative market opportunities during the forecast period. For instance:

- In October 2023, the Starship China concept truck was co-developed and officially launched by FAW Jiefang Group Co. and Shell China Ltd.

The state governments in India are including electric buses in their fleets to convert their ICE fleet of buses and reduce operational costs while reducing carbon emissions and improving air quality. For instance:

- In May 2024, the government of India announced its plans to incentivize the adoption of electric buses for intercity and interstate travel to promote zero-emission transportation across the country.

Japan is home to one of the planet's most cutting-edge electric vehicle ecosystems. Major companies like Toyota and Nissan are taking impressive steps to develop and manufacture electric vehicles within the country.

The abundance of EV charging stations, surpassing the number of petrol and diesel outlets, indicates progress in the hybrid and electric vehicle market. These favorable conditions are expected to fuel Japan's market and demand for commercial electric vehicles. Additionally, government funding supports the growth of Japan's electric commercial vehicle market.

With such developments across the region, the demand for electric commercial vehicles will likely grow in the coming years.

Electric Commercial Vehicle Industry Overview

The electric commercial vehicle market is dominated by several key players, including BYD Motors Inc., AB Volvo, Daimler Truck AG, and Paccar Inc. The rapid expansion of electric commercial vehicle manufacturers across the country and the introduction of new models across major countries are expected to witness major growth for the market during the forecast period. For instance:

- In April 2024, Rizon, a brand of Daimler Truck AG, introduced class 4-5 electric trucks in Canada. The company will offer four variants of its battery-electric trucks, including the e16L, e16M, e18L, and the e18M, with GVW ratings ranging from 7.25 tons to 8.55 tons.

- In October 2023, Foton Motor introduced the Aumark next-generation light-duty truck and the Wonder next-generation micro-truck during a brand renewal and new product launch in Changsha, Hunan.

- In June 2023, the Bavarian State Government approved four out of five funding projects of MAN Truck & Bus. This funding supports the advancement of high-voltage batteries for electric trucks and buses. The government subsidy of USD 26.84 million at the Nuremberg site.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Stringent Emission Regulations are Fueling Market Growth

- 4.2 Market Restraints

- 4.2.1 High Cost of Electric Commercial Vehicles May Hamper Growth

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Value in USD)

- 5.1 By Vehicle Type

- 5.1.1 Bus

- 5.1.2 Trucks

- 5.1.3 Pick-up Trucks

- 5.1.4 Vans

- 5.2 By Propulsion

- 5.2.1 Battery Electric Vehicles

- 5.2.2 Plug-in Hybrid Electric Vehicles

- 5.2.3 Fuel Cell Electric Vehicles

- 5.3 By Power Output

- 5.3.1 Less than 150 kW

- 5.3.2 150-250 kW

- 5.3.3 Above 250 kW

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 BYD Motors Inc.

- 6.2.2 AB Volvo

- 6.2.3 Traton SE

- 6.2.4 Daimler Truck AG

- 6.2.5 Zhengzhou Yutong Bus Co. Ltd

- 6.2.6 Ford Motor Company

- 6.2.7 Tesla Inc.

- 6.2.8 Proterra Inc.

- 6.2.9 Rivian Automotive Inc.

- 6.2.10 Tata Motor Limited

- 6.2.11 Olectra Greentech Limited

- 6.2.12 Paccar Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

8 An Overview of Electric Vehicle Charging Infrastructure Development Across the Region**

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日