インドの電気車両:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

India Electric Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 246 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693623

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

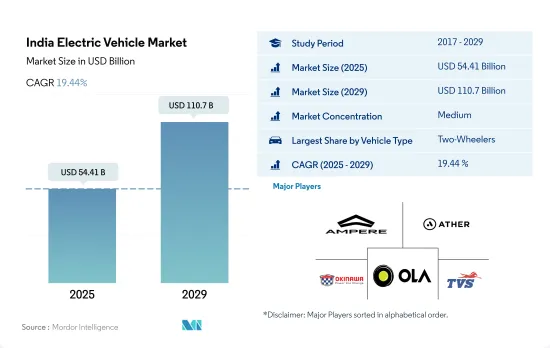

インドの電気車両市場規模は2025年に544億1,000万米ドルと推定され、2029年には1,107億米ドルに達すると予測され、予測期間中(2025-2029年)のCAGRは19.44%で成長する見込みです。

さまざまな車両カテゴリーで電気車両(EV)を採用するインドの包括的戦略が、持続可能なモビリティへの移行を推進しています。

- インドの電気車両(EV)市場は、車種別に乗用車、商用車、二輪車に区分され、クリーンエネルギーの導入と二酸化炭素排出量削減に対する国のコミットメントを反映して、大きな変革期を迎えています。各セグメントは、それぞれ異なる市場力学、ユーザーニーズ、成長の可能性に対応しており、電動モビリティに向けたインドの歩みを包括的に描き出しています。

- 電気乗用車は、消費者の意識の高まり、政府の好意的な政策、国内外のメーカーの存在感の高まりに後押しされ、インド市場で着実に普及しつつあります。現在は従来型自動車に比べれば小規模だが、大衆市場向けの手頃なモデルから高級セグメント向けのプレミアム電気車両まで、このセグメントは急速に拡大しています。

- 電気商用車部門は、まだ初期段階にあるとはいえ、大きな成長を示すことになると思われます。この成長の原動力となっているのは、ロジスティクスと輸送部門における持続可能性とコスト効率の重視の高まりです。電気バス、トラック、バンは、公害を削減し、公共交通機関や商品配送における電動モビリティを促進することを目的とした政府のイニシアティブに支えられて、徐々に都市部の車両に導入されつつあります。電気商用車の運用コスト面での利点は、州や中央政府の様々な優遇措置と相まって、フリートオペレーターや企業に電気オプションへの移行を促しています。このセグメントの成長は、インドの野心的な環境目標を達成し、都市の大気の質を改善するために不可欠です。

インドの電気車両市場動向

政府のイニシアティブと厳しい規範がインドの電気車両市場の急成長を牽引

- インドの電気車両(EV)市場は成長段階にあり、政府が公害対策戦略を積極的に策定しています。2015年に開始されたFame Indiaスキームは、自動車の電動化を推進する上で極めて重要な役割を果たしました。その成功を受けて、2022年4月まで実施されるフェイム・フェーズ2は、特に2021年のEV販売をさらに強化し、政府はバッテリー容量が15kWhまでの電気車両に1万インドルピー(約1,000万円)の補助金を提供しています。

- インド全土の州政府は、内燃機関(ICE)バスからの移行を目指し、電気バスを導入するケースが増えています。この動きは、運行コストを削減するだけでなく、二酸化炭素排出を抑制し、大気の質を改善します。注目すべき動きとして、デリー政府は2021年3月に300台の新型低床電気(AC)バスの調達を許可し、そのうち100台は2022年1月に道路に投入されました。こうした取り組みにより、2022年のインドにおける電気商用車の需要は2021年比で62.58%と大幅に急増しました。

- 電気車両の需要は、政府の厳しい基準導入に後押しされ、ここ最近急増しています。2021年8月、インド政府は車両スクラップ政策を発表し、年式に関係なく汚染車両や不適合車両を段階的に廃止することを目標としました。この政策は2024年までに実施されることになっており、消費者を電気車両に誘導しています。さらに政府は、2030年までにインドの全自動車の30%を電動化するという野心的な目標を掲げています。こうした取り組みにより、インドでは2024年から2030年にかけて電気車両の販売が促進される見込みです。

インドの電気車両産業の概要

インドの電気車両市場は適度に統合されており、上位5社で43.74%を占めています。この市場の主要企業は以下の通り。 Ampere Vehicle Private Limited, Ather Energy Pvt. Ltd., Okinawa Autotech Pvt. Ltd., Ola Electric Mobility Pvt. Ltd. and TVS Motor Company Limited(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 人口

- 一人当たりGDP

- 自動車購入のための消費者支出(cvp)

- インフレ率

- 自動車ローン金利

- シェアライド

- 電化の影響

- EV充電ステーション

- バッテリーパック価格

- Xev新モデル発表

- 中古車販売

- 燃料価格

- OEM生産統計

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 車両タイプ

- 商用車

- バス

- 大型商用トラック

- 小型商用ピックアップトラック

- 小型商用バン

- 中型商用トラック

- 乗用車

- ハッチバック

- 多目的車

- セダン

- SUV

- 二輪車

- 商用車

- 燃料カテゴリー

- FCEV

- HEV

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Ampere Vehicle Private Limited

- Ather Energy Pvt. Ltd.

- BYD India Private Limited

- Hero Electric Vehicles Pvt. Ltd.

- Hyundai Motor India Limited

- JBM Auto Limited

- Mahindra & Mahindra Limited

- MG Motor India Private Limited

- Okinawa Autotech Pvt. Ltd.

- Ola Electric Mobility Pvt. Ltd.

- Olectra Greentech Ltd.

- Switch Mobility(Ashok Leyland Limited)

- Tata Motors Limited

- Toyota Kirloskar Motor Pvt. Ltd.

- TVS Motor Company Limited

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The India Electric Vehicle Market size is estimated at 54.41 billion USD in 2025, and is expected to reach 110.7 billion USD by 2029, growing at a CAGR of 19.44% during the forecast period (2025-2029).

India's comprehensive strategy to adopt electric vehicles (EVs) across various vehicle categories is driving the nation's transition toward sustainable mobility

- India's electric vehicle (EV) market, segmented by vehicle type into passenger cars, commercial vehicles, and two-wheelers, is undergoing a significant transformation, reflecting the country's commitment to embracing clean energy and reducing carbon emissions. Each segment caters to distinct market dynamics, user needs, and growth potential, painting a comprehensive picture of India's journey toward electric mobility.

- Electric passenger cars are steadily gaining traction in the Indian market, driven by increasing consumer awareness, favorable government policies, and the growing presence of both international and local manufacturers. Although currently small compared to conventional vehicles, the segment is witnessing a rapid expansion in offerings, ranging from affordable models aimed at the mass market to premium electric cars catering to the luxury segment.

- The electric commercial vehicle sector, though still in its early stages, is set to witness significant growth. This growth is being driven by a rising emphasis on sustainability and cost-effectiveness within the logistics and transportation sectors. Electric buses, trucks, and vans are gradually making their way into urban fleets, supported by government initiatives aimed at reducing pollution and promoting electric mobility in public transportation and goods delivery. The operational cost benefits of electric commercial vehicles, coupled with various state and central government incentives, are encouraging fleet operators and businesses to transition toward electric options. This segment's growth is critical for achieving India's ambitious environmental targets and improving urban air quality.

India Electric Vehicle Market Trends

Government initiatives and stringent norms drive rapid growth in the electric vehicle market in India

- India's electric vehicle (EV) market is in a growth phase, with the government actively formulating strategies to combat pollution. The Fame India scheme, launched in 2015, has played a pivotal role in driving vehicle electrification. Building on its success, Fame Phase 2, active till April 2022, further bolstered EV sales, especially in 2021, with the government offering subsidies like INR 10,000 grants for electric cars with battery capacities up to 15 kWh.

- State governments across India are increasingly incorporating electric buses into their fleets, aiming to transition from internal combustion engine (ICE) buses. This move not only cuts operational costs but also curbs carbon emissions and improves air quality. In a notable move, the Delhi government greenlit the procurement of 300 new low-floor electric (AC) buses in March 2021, with 100 of them hitting the roads in January 2022. These initiatives contributed to a significant 62.58% surge in demand for electric commercial vehicles in India in 2022 over 2021.

- The demand for electric cars has surged in recent times, driven by the government's introduction of stringent norms. In August 2021, the Indian government unveiled the Vehicle Scrappage Policy, targeting the phasing out of polluting and unfit vehicles, irrespective of their age. This policy, set to be implemented by 2024, is steering consumers toward electric cars. Additionally, the government has set an ambitious target of having 30% of all cars in India electrified by 2030. These initiatives are poised to propel electric car sales during the 2024-2030 period in India.

India Electric Vehicle Industry Overview

The India Electric Vehicle Market is moderately consolidated, with the top five companies occupying 43.74%. The major players in this market are Ampere Vehicle Private Limited, Ather Energy Pvt. Ltd., Okinawa Autotech Pvt. Ltd., Ola Electric Mobility Pvt. Ltd. and TVS Motor Company Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.2 GDP Per Capita

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.4 Inflation

- 4.5 Interest Rate For Auto Loans

- 4.6 Shared Rides

- 4.7 Impact Of Electrification

- 4.8 EV Charging Station

- 4.9 Battery Pack Price

- 4.10 New Xev Models Announced

- 4.11 Used Car Sales

- 4.12 Fuel Price

- 4.13 Oem-wise Production Statistics

- 4.14 Regulatory Framework

- 4.15 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Type

- 5.1.1 Commercial Vehicles

- 5.1.1.1 Buses

- 5.1.1.2 Heavy-duty Commercial Trucks

- 5.1.1.3 Light Commercial Pick-up Trucks

- 5.1.1.4 Light Commercial Vans

- 5.1.1.5 Medium-duty Commercial Trucks

- 5.1.2 Passenger Vehicles

- 5.1.2.1 Hatchback

- 5.1.2.2 Multi-purpose Vehicle

- 5.1.2.3 Sedan

- 5.1.2.4 Sports Utility Vehicle

- 5.1.3 Two-Wheelers

- 5.1.1 Commercial Vehicles

- 5.2 Fuel Category

- 5.2.1 FCEV

- 5.2.2 HEV

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Ampere Vehicle Private Limited

- 6.4.2 Ather Energy Pvt. Ltd.

- 6.4.3 BYD India Private Limited

- 6.4.4 Hero Electric Vehicles Pvt. Ltd.

- 6.4.5 Hyundai Motor India Limited

- 6.4.6 JBM Auto Limited

- 6.4.7 Mahindra & Mahindra Limited

- 6.4.8 MG Motor India Private Limited

- 6.4.9 Okinawa Autotech Pvt. Ltd.

- 6.4.10 Ola Electric Mobility Pvt. Ltd.

- 6.4.11 Olectra Greentech Ltd.

- 6.4.12 Switch Mobility (Ashok Leyland Limited)

- 6.4.13 Tata Motors Limited

- 6.4.14 Toyota Kirloskar Motor Pvt. Ltd.

- 6.4.15 TVS Motor Company Limited

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 246 Pages

- 納期

- 2~3営業日