民間航空- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Commercial Aviation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 338 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693589

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

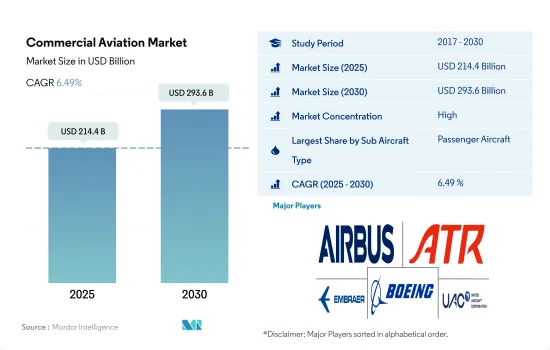

民間航空市場規模は2025年に2,144億米ドルと推定・予測され、2030年には2,936億米ドルに達し、予測期間中(2025~2030年)のCAGRは6.49%で成長すると予測されます。

航空旅客輸送量の伸びと、燃費が良く最新式の航空機に対する需要の高まりが、世界的に民間航空産業を押し上げると予想されます。

- 国連世界観光機関(UNWTO)によると、観光業は世界のGDPの10%に寄与しており、現代世界における主要な収入源のひとつとなっています。過去15年間で、民間航空の旅客数は倍増しています。予測期間中、合計1万4,080機の民間航空機が納入される見込みであり、その一部は、現在の機体のより老朽化した航空機を置き換える可能性があります。COVID-19パンデミックは、2020年の世界の航空旅客輸送量に影響を与え、フライト活動を減少させ、航空会社のキャッシュフローに影響を与えました。その結果、ほとんどの航空会社が航空機発注のキャンセルまたは延期を決定しました。

- しかし、民間航空産業は2022年に徐々に回復し、その結果、航空機納入数は2021年に比べて大幅に増加しました。航空会社は、より優れた燃料効率と航続距離を持つ航空機を求めており、より新しい航空機の開発は、OEMが今後数年間、より多くの航空会社の顧客を引き付けるのに役立つ可能性があります。2017~2022年にかけての納入機数では、合計2,049機が世界の様々な航空会社によって調達されました。これら合計2,049機のうち、旅客機が96%を占め、貨物機が4%を占めました。

- 国内旅客需要は国際旅客需要よりも早くCOVID-19以前の水準に戻ると予想されるため、ナローボディ機の市場はワイドボディ機の需要よりも早く回復すると予想されます。737MAXが2020年後半に運航を再開することも、ナローボディ機セグメントの拡大を後押しする可能性があります。このような開発は、市場の需要を牽引すると予想されます。予測期間中、世界全体で旅客機13,812機、貨物機268機の納入が見込まれます。

アジア太平洋が民間航空市場で最も有利な市場となる展望

- 北米は、アジア太平洋に次いで2番目に高い成長が見込まれる地域です。航空機納入数では、北米の民間航空機は2017~2022年にかけて世界の民間航空機全体のほぼ29%を占めます。2023~2030年にかけて、航空機納入数は57%増加すると予想されています。北米は予測期間中、航空機納入総数の27%を占める可能性があります。欧州の民間航空機は、2017~2022年にかけて世界の民間航空機総数の17%を占めます。

- 南米の航空旅客数は、2020年の2億1,073万人に対し、2021年には1億9,915万人に縮小しました。予測期間中、欧州、中東・アフリカ、南米は、それぞれ航空機納入総数の約20%、9%、3%を占める可能性があります。

- COVID-19パンデミックは、世界の輸送の停止により民間航空機市場に大きな影響を与えました。また、世界中で実施された厳格な閉鎖措置も、民間航空機市場の経済状況に大きな影響を与えました。そのため、2021年の国際旅客需要は2019年に比べて75.5%減少しました。アジア太平洋は、2023~2030年にかけて健全な成長を遂げると予測されています。

- アジア太平洋では、パンデミックが同地域の航空産業に大きな影響を与えたもの、国内旅客輸送量は着実に増加しています。2022年には、アジア太平洋の航空旅客輸送量は世界全体の38%に達しました。

- 同地域の経済成長とインフラ整備による一人当たり所得の増加は、航空旅客数の増加に寄与し、地域航空会社や国内航空会社の機材拡大を支えました。ナローボディ型航空機は、同期間中の納入総数の約83%を占めました。

世界の民間航空市場の動向

渡航制限の緩和と旅客数の増加が需要を牽引

- 国境を越えた旅行が徐々に回復するにつれて、アジア太平洋の航空会社は、旅行に対する欲求の高まりと、COVID-19による2年間の鎖国期間中に蓄積された貯蓄に刺激されて、駆け込み需要に対応するために便の投入を急いです。その結果、2022年には、この地域の航空旅客輸送量は、他の地域よりもパンデミックから急速に回復しました。例えば、2022年、アジア太平洋の航空旅客輸送量は22億人を記録し、2021年比で10%の伸びを示しました。さらに、同地域の航空会社は、同地域の主要国における航空旅客輸送量の増加に対応するため、機材の拡大計画を実施しています。中国、インド、日本、インドネシアは、アジア太平洋の総旅客輸送量の70%を占めており、同地域の他の国々と比べて新型航空機に対する需要が高まると予想されます。

- アジア太平洋の航空会社は、世界的に経済状況が厳しさを増しているにもかかわらず、潜在的な旅行需要が成長を促進し続けたため、国際航空旅客市場の顕著な回復を目の当たりにしました。同地域の航空会社の搭乗率も改善し、前年同期比で17.9pts上昇し、78.8%に達しました。このようなASK総計と搭乗率の開発は非常に心強いものであり、当地域における航空需要の増加を裏付けるものです。さらに、国際線旅客数の健全な伸びは、ビジネスとレジャー部門からの旅行需要が旺盛であることを示しています。同地域における航空旅客輸送量の急速な増加は、将来の航空輸送産業を牽引するものと期待されます。

民間航空産業概要

民間航空市場はかなり統合されており、上位5社で90.21%を占めています。この市場の主要企業は、Airbus SE、ATR、Embraer、The Boeing Company、United Aircraft Corporationなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 航空旅客輸送量

- アジア太平洋

- 欧州

- 中東・アフリカ

- 北米

- 南米

- 航空輸送貨物

- アジア太平洋

- 欧州

- 中東・アフリカ

- 北米

- 南米

- 国内総生産

- アジア太平洋

- 欧州

- 中東・アフリカ

- 北米

- 南米

- 収入旅客キロ(rpk)

- アジア太平洋

- 欧州

- 中東・アフリカ

- 北米

- 南米

- インフレ率

- アジア太平洋

- 欧州

- 中東・アフリカ

- 北米

- 南米

- 規制の枠組み

- バリューチェーン分析

第5章 市場セグメンテーション

- サブ航空機タイプ

- 貨物機

- 旅客機

- ナローボディ機

- ワイドボディ機

- 地域

- アジア太平洋

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- フィリピン

- シンガポール

- 韓国

- タイ

- その他のアジア太平洋

- 欧州

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- トルコ

- 英国

- その他の欧州

- 中東・アフリカ

- アルジェリア

- エジプト

- カタール

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他の中東・アフリカ

- 北米

- カナダ

- メキシコ

- 米国

- その他の北米地域

- 南米

- ブラジル

- チリ

- コロンビア

- その他の南米

- アジア太平洋

第6章 競合情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Airbus SE

- ATR

- COMAC

- De Havilland Aircraft of Canada Ltd.

- Embraer

- The Boeing Company

- United Aircraft Corporation

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92739

The Commercial Aviation Market size is estimated at 214.4 billion USD in 2025, and is expected to reach 293.6 billion USD by 2030, growing at a CAGR of 6.49% during the forecast period (2025-2030).

The Growth In Air Passenger Traffic And The Increasing Demand For Fuel-Efficient And Modern Aircraft Are Expected To Boost The Commercial Aviation Industry Globally

- According to the UNWTO, tourism contributes 10% of the world's GDP, making it one of the main sources of income in the modern world, with 57% of cross-border travelers using aircraft. In the last 15 years, the number of passengers in commercial aviation has doubled. During the forecast period, a total of 14,080 commercial aircraft are expected to be delivered, some of which may replace the current fleet's more aged aircraft. The COVID-19 pandemic affected air passenger traffic globally in 2020, reducing flight activity and impacting airline cash flows. As a result, most airlines decided to cancel or defer their aircraft orders.

- However, the commercial aviation industry recovered gradually in 2022, which led to a significant increase in aircraft deliveries compared to 2021. Airlines are looking for aircraft with better fuel efficiency and range, and the development of newer aircraft may help OEMs attract more airline customers in the coming years. In terms of deliveries during 2017-2022, a total of 2,049 aircraft were procured by various airlines globally. Of these total 2,049 aircraft, passenger aircraft accounted for 96%, and freighter aircraft accounted for 4%.

- Since the domestic passenger demand is anticipated to return to pre-COVID-19 levels earlier than the international passenger demand, the market for narrowbody aircraft is anticipated to rebound faster than the demand for widebody aircraft. The 737 MAX's return to service in late 2020 may also support the expansion of the narrowbody segment. Such developments are expected to drive the demand in the market. A total of 13,812 passenger aircraft and 268 freighter aircraft are expected to be delivered globally during the forecast period

Asia-Pacific Is Expected To Be The Most Lucrative Market In The Commercial Aviation

- North America is expected to be the second-highest-growing region after Asia-Pacific. In terms of aircraft deliveries, North America's commercial aircraft accounted for almost 29% of the total commercial aircraft worldwide from 2017 to 2022. Aircraft deliveries are expected to rise by 57% from 2023 to 2030. North America may be accountable for 27% of total aircraft deliveries during the forecast period. Europe's commercial aircraft accounted for 17% of the total commercial aircraft worldwide from 2017 to 2022.

- Air travel in South America contracted to 199.15 million air passengers in 2021 compared to 210.73 million passengers traveled in 2020. During the forecast period, Europe, Middle East & Africa, and South America may account for around 20%, 9%, and 3% of total aircraft deliveries, respectively.

- The COVID-19 pandemic greatly impacted the commercial aircraft market due to a halt in global transportation. The stringent lockdowns enforced worldwide also significantly impacted the economic conditions of the commercial aircraft market. Therefore, in 2021, international passenger demand was 75.5% lower than in 2019. Asia-Pacific (APAC) is projected to grow at a healthy rate between 2023 and 2030.

- Domestic passenger traffic has been steadily increasing in the APAC region, although the pandemic had a significant impact on the region's aviation industry. In 2022, the APAC region contributed 38% of total air passenger traffic worldwide.

- The region's rising per capita income due to economic and infrastructure growth contributed to the growth of air passenger numbers and supported the expansion of the regional and domestic airlines' fleets. Narrowbody aircraft accounted for approximately 83% of total deliveries during the period.

Global Commercial Aviation Market Trends

Ease of travel restrictions and the rising number of passengers are driving the demand

- As cross-border travel was progressively restored, the carriers in the Asia-Pacific have raced to put on flights to meet runaway demand, stimulated by the pent-up desire to travel and savings accumulated in the two years of isolation due to COVID-19. As a result, in 2022, air passenger traffic in the region recovered more rapidly from the pandemic than other regions. For instance, in 2022, air passenger traffic in Asia-Pacific was recorded at 2.2 billion, witnessing a growth of 10% compared to 2021. Moreover, airline companies in the region are implementing fleet expansion plans to cater to the growing air passenger traffic in the major countries in the region. China, India, Japan, and Indonesia account for 70% of the total air passenger traffic in Asia-Pacific and are expected to generate more demand for new aircraft compared to other countries in the region.

- Airlines in Asia-Pacific witnessed a notable recovery in international air passenger markets as pent-up travel demand continued to fuel growth despite increasingly challenging global economic conditions. The passenger load factor for the region's airlines also improved, showing a year-on-year increase of 17.9 ppts and reaching 78.8%. These developments in total ASK and passenger load factor are highly encouraging and support the increasing demand for air travel in the region. Moreover, the healthy growth in international passenger traffic shows strong travel demand from the business and leisure sectors. The rapid increase in air passenger traffic in the region is expected to drive the air transport industry in the future.

Commercial Aviation Industry Overview

The Commercial Aviation Market is fairly consolidated, with the top five companies occupying 90.21%. The major players in this market are Airbus SE, ATR, Embraer, The Boeing Company and United Aircraft Corporation (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Air Passenger Traffic

- 4.1.1 Asia-Pacific

- 4.1.2 Europe

- 4.1.3 Middle East and Africa

- 4.1.4 North America

- 4.1.5 South America

- 4.2 Air Transport Freight

- 4.2.1 Asia-Pacific

- 4.2.2 Europe

- 4.2.3 Middle East and Africa

- 4.2.4 North America

- 4.2.5 South America

- 4.3 Gross Domestic Product

- 4.3.1 Asia-Pacific

- 4.3.2 Europe

- 4.3.3 Middle East and Africa

- 4.3.4 North America

- 4.3.5 South America

- 4.4 Revenue Passenger Kilometers (rpk)

- 4.4.1 Asia-Pacific

- 4.4.2 Europe

- 4.4.3 Middle East and Africa

- 4.4.4 North America

- 4.4.5 South America

- 4.5 Inflation Rate

- 4.5.1 Asia-Pacific

- 4.5.2 Europe

- 4.5.3 Middle East and Africa

- 4.5.4 North America

- 4.5.5 South America

- 4.6 Regulatory Framework

- 4.7 Value Chain Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Sub Aircraft Type

- 5.1.1 Freighter Aircraft

- 5.1.2 Passenger Aircraft

- 5.1.2.1 Narrowbody Aircraft

- 5.1.2.2 Widebody Aircraft

- 5.2 Region

- 5.2.1 Asia-Pacific

- 5.2.1.1 Australia

- 5.2.1.2 China

- 5.2.1.3 India

- 5.2.1.4 Indonesia

- 5.2.1.5 Japan

- 5.2.1.6 Malaysia

- 5.2.1.7 Philippines

- 5.2.1.8 Singapore

- 5.2.1.9 South Korea

- 5.2.1.10 Thailand

- 5.2.1.11 Rest of Asia-Pacific

- 5.2.2 Europe

- 5.2.2.1 France

- 5.2.2.2 Germany

- 5.2.2.3 Italy

- 5.2.2.4 Netherlands

- 5.2.2.5 Russia

- 5.2.2.6 Spain

- 5.2.2.7 Turkey

- 5.2.2.8 UK

- 5.2.2.9 Rest of Europe

- 5.2.3 Middle East and Africa

- 5.2.3.1 Algeria

- 5.2.3.2 Egypt

- 5.2.3.3 Qatar

- 5.2.3.4 Saudi Arabia

- 5.2.3.5 South Africa

- 5.2.3.6 United Arab Emirates

- 5.2.3.7 Rest of Middle East and Africa

- 5.2.4 North America

- 5.2.4.1 Canada

- 5.2.4.2 Mexico

- 5.2.4.3 United States

- 5.2.4.4 Rest of North America

- 5.2.5 South America

- 5.2.5.1 Brazil

- 5.2.5.2 Chile

- 5.2.5.3 Colombia

- 5.2.5.4 Rest of South America

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Airbus SE

- 6.4.2 ATR

- 6.4.3 COMAC

- 6.4.4 De Havilland Aircraft of Canada Ltd.

- 6.4.5 Embraer

- 6.4.6 The Boeing Company

- 6.4.7 United Aircraft Corporation

7 KEY STRATEGIC QUESTIONS FOR AVIATION CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

民間航空- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 338 Pages

- 納期

- 2~3営業日