|

市場調査レポート

商品コード

1692479

北米の民間航空:市場シェア分析、産業動向、成長予測(2025年~2030年)North America Commercial Aviation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の民間航空:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 162 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

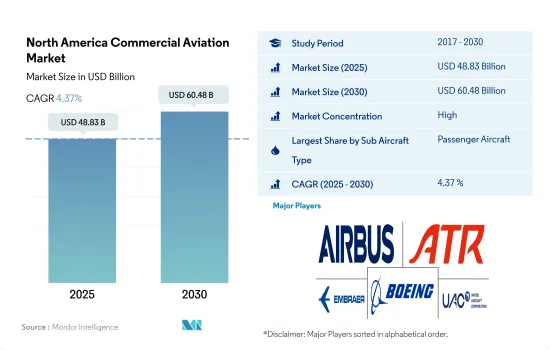

北米の民間航空市場規模は2025年に488億3,000万米ドルと推定され、2030年には604億8,000万米ドルに達し、予測期間(2025年~2030年)のCAGRは4.37%で成長すると予測されます。

航空会社の機体開発、燃費効率の高い航空機への需要の高まりが北米の民間航空機需要を牽引

- 北米の民間航空市場は、主に国内旅客数の増加による旅客機需要によって、予測期間中に大きな成長が見込まれます。

- 航空会社の機体開発、燃費効率の高い航空機に対する需要の増加、航空旅客数の増加、航空業界によるゼロエミッション2050年目標の検討が民間航空機の需要を促進しています。2023年8月現在、同地域には1,474機のボーイング機と986機のエアバス機の供給残があります。これらの航空機のうち、米国だけで2,405機の受注残があります。従って、同国はより大きな成長が見込まれます。

- さらに、北米では米国が最大の民間航空機保有国であり、世界最大の航空会社の本拠地でもあります。新しい航空機の納入に関しては、この地域では2017年から2022年の間に、合計2,065機の新しい民間航空機が様々な航空会社によって調達されました。これら2,065機のうち、旅客機が1,919機、貨物機が146機を占めています。航空需要が回復するなか、航空会社は調達計画を再構築し、運航コストを削減するために比較的若い機体を維持しようとしており、その結果、新型旅客機の需要が発生しています。

- さらに、航空貨物のキャパシティーの混乱は、貨物専用機がeコマース導入の加速に支えられ、取扱量と収益を増加させたことから、貨物機部門にとってプラスであることが証明されました。FedEx、UPS、Atlas Airは、予測期間中に新型貨物機による機材拡大を計画しています。

ナローボディ機が同地域の民間航空活動を牽引

- 北米の民間航空業界は、長きにわたり世界の航空市場において重要な役割を担ってきました。同地域の商業航空活動の需要は、年間航空旅客数の増加によって牽引されています。2022年、この地域の航空旅客数は60億人に達しました。米国が83%と最大のシェアを占め、次いでカナダが8%、メキシコが6%、その他の北米地域が2%となっています。

- 格安航空会社(LCC)や超低価格航空会社(ULCC)の台頭は、従来の航空会社のビジネスモデルを破壊しました。これらの航空会社は競争力のある運賃を提供することで、より多くの顧客層を獲得し、より多くの人々への航空旅行の利便性を拡大しています。2017年から2022年の間に納入された航空機に関しては、合計2,049機がこの地域の様々な航空会社によって調達されました。この2,049機のうち、旅客機が96%を占め、貨物機が4%を占めました。

- 787ドリームライナーの納入一時停止、777Xプログラムの遅延、認証問題によるA350の生産立ち上げの遅れ、さらにワイドボディ・ジェット機に対する需要の低迷が、予測期間前半のワイドボディ・セグメントの成長を妨げると予想されます。反対に、737MAX、A220、A321neo、A321XLRの生産増強計画は、今後10年間の同地域のナローボディセグメントの成長を支えると思われます。このような開発により、民間航空機の需要は増加し、2023年から2030年にかけて、合計2,997機の民間航空機が調達される予定です。

北米の民間航空市場の動向

国内旅行者の需要増加が市場を牽引

- 北米は古くから航空旅行のハブとなってきました。広大な国土と多様な目的地を有するため、何百万人もの旅客が国内外へのフライトを選択しています。経済の成長、航空券の値ごろ感、中産階級の台頭といった要因がすべて、航空旅客数の大幅な増加に寄与しています。米国の2022年の航空旅客数は10億4,000万人に達し、2021年比で7%、2019年比で12%増加しました。

- 2022年1月から12月までの通年で、米国の航空会社が運んだ旅客数は8億5,300万人で、2021年の6億5,800万人、2020年の3億8,800万人を上回りました。カナダの航空会社が運んだ旅客総数は2022年に1億700万人に達し、2021年の水準を6%上回りました。2022年のメキシコの航空旅客数は1億人で、2021年の水準と比較して7%の伸びを示しました。北米は、他の多くの国や地域よりも渡航制限が少なく、その期間も短いという恩恵を受けています。これは、海外旅行だけでなく、大きな自国市場の国内旅行も後押ししています。同地域の純利益は、2022年の99億米ドルから2023年には114億米ドルに増加すると予想されます。

- さらに、航空旅客輸送量による需要に対応するため、この地域のさまざまな航空会社が新しい航空機の調達を計画しています。例えば、2023年の世界の航空機納入数の約3分の1は、北米の航空会社によって納入されると予想されています。同地域の航空機納入は昨年すでに2019年の水準を上回っていたが、今年はさらに72機の増加が見込まれています。全体として、安定した航空旅行により、同地域の航空旅客数は、2022年に記録された12億人に対し、2030年には17億人の増加が見込まれています。

北米の民間航空産業の概要

北米の民間航空市場はかなり統合されており、上位5社が87.70%を占めています。この市場の主要企業は以下の通り。 Airbus SE, ATR, Embraer, The Boeing Company and United Aircraft Corporation(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 航空旅客輸送量

- 航空貨物輸送量

- 国内総生産

- 収入旅客キロ(rpk)

- インフレ率

- 規制の枠組み

- バリューチェーン分析

第5章 市場セグメンテーション

- サブ航空機タイプ

- 貨物機

- 旅客機

- ナローボディ機

- ワイドボディ機

- 国名

- カナダ

- メキシコ

- 米国

- その他の北米

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Airbus SE

- ATR

- COMAC

- De Havilland Aircraft of Canada Ltd.

- Embraer

- The Boeing Company

- United Aircraft Corporation

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 91466

The North America Commercial Aviation Market size is estimated at 48.83 billion USD in 2025, and is expected to reach 60.48 billion USD by 2030, growing at a CAGR of 4.37% during the forecast period (2025-2030).

Fleet development of the airlines, and increasing demand for fuel-efficient aircraft is driving the demand for the commercial aircraft in North America

- The commercial aircraft market in North America is expected to experience significant growth during the forecast period, primarily driven by the demand for passenger aircraft due to the growing number of domestic passengers traveling.

- Fleet development of the airlines, increase in demand for fuel-efficient aircraft, growth in the number of airline passengers, and the airline industry's consideration of the zero-emission 2050 goal fuel the demand for commercial aircraft. As of August 2023, the region has a backlog of 1,474 Boeing aircraft and 986 Airbus aircraft. Of these total aircraft, the US alone has 2,405 aircraft in backlog. Hence, the country is expected to witness larger growth.

- Additionally, in North America, the United States has the largest fleet of commercial aircraft and is home to some of the biggest carriers in the world. In terms of new aircraft deliveries, in the region during 2017-2022, a total of 2,065 new commercial aircraft were procured by various airlines. Of these 2,065 aircraft, passenger aircraft accounted for 1,919, and freighter aircraft accounted for 146 aircraft. With the demand for air travel recovering, the airlines are restructuring their procurement plans and trying to maintain a relatively younger fleet to reduce operational costs, thus generating demand for new passenger aircraft.

- Furthermore, disruption in air cargo capacity proved to be positive for the freighter segment, as dedicated freighter fleets experienced volume and revenue increases, supported by accelerated e-commerce adoption. FedEx, UPS, and Atlas Air have plans to expand their fleet with new freighter aircraft during the forecast period.

Narrowbody aircraft is driving the region's commercial aviation activity

- The commercial aviation industry in North America has long been a significant player in the global aviation market. The demand for commercial aviation activity in the region is driven by the rising number of passengers traveling by air annually. In 2022, the region's air passenger traffic stood at 6 billion. The US accounted for the largest share, which was 83%, followed by Canada, Mexico, and the Rest of North America at 8%, 6%, and 2%, respectively.

- The rise of low-cost carriers (LCCs) and ultra-low-cost carriers (ULCCs) has disrupted the traditional airline business model. These carriers offer competitive fares, enticing a larger customer base and expanding air travel accessibility to more people. In terms of deliveries during 2017-2022, a total of 2,049 aircraft were procured by various airlines in the region. Of these 2,049 aircraft, passenger aircraft accounted for 96% and freighter aircraft accounted for 4%.

- A temporary halt in delivery of the 787 Dreamliner, delay in the 777X program, and delay in production ramp-up of A350s due to certification problems, as well as weak demand for the widebody jet, are expected to hamper the growth of the widebody segment during the first half of the forecast period. On the contrary, production ramp-up plans for 737MAX, A220, A321neo, and A321XLR will support the growth of the narrowbody segment in the region over the next decade. Overall, with developments such as these, the demand for commercial aviation aircraft is expected to rise, and during 2023-2030, a total of 2,997 commercial aviation aircraft is scheduled to be procured.

North America Commercial Aviation Market Trends

The increase in demand from domestic travelers is driving the market

- North America has long been a hub for air travel. With a vast landmass and diverse destinations, millions of passengers choose to fly domestically and internationally. Factors such as a growing economy, increased affordability of air travel, and a rising middle class have all contributed to a significant uptick in air passenger traffic. The air passenger traffic in the US reached 1.04 billion in 2022, up by 7% compared to 2021 and 12% compared to 2019.

- For the full year 2022, January through December, US airlines carried 853 million passengers, up from 658 million in 2021 and 388 million in 2020. The total number of passengers carried by airlines in Canada reached 107 million in 2022, surpassing the levels in 2021 by 6%. In 2022, Mexico had 100 million air passenger traffic, representing a 7% growth compared to its 2021 traffic levels. North America has benefitted from fewer and shorter-lasting travel restrictions than many other countries and regions. This has boosted domestic travel in a large home market, as well as international travel. Net profits for the region are expected to rise from USD 9.9 billion in 2022 to USD 11.4 billion in 2023.

- Additionally, to cater to the demand driven by air passenger traffic, various airlines in the region are planning to procure new aircraft. For instance, around one-third of global aircraft deliveries for 2023 are anticipated to be received by various carriers in North America. Although the region's aircraft deliveries were already above 2019 levels last year, they are expected to grow by an additional 72 units this year. Overall, with consistent air travel, the region's air passenger traffic is expected to increase by 1.7 billion in 2030, compared to 1.2 billion recorded in 2022.

North America Commercial Aviation Industry Overview

The North America Commercial Aviation Market is fairly consolidated, with the top five companies occupying 87.70%. The major players in this market are Airbus SE, ATR, Embraer, The Boeing Company and United Aircraft Corporation (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Air Passenger Traffic

- 4.2 Air Transport Freight

- 4.3 Gross Domestic Product

- 4.4 Revenue Passenger Kilometers (rpk)

- 4.5 Inflation Rate

- 4.6 Regulatory Framework

- 4.7 Value Chain Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Sub Aircraft Type

- 5.1.1 Freighter Aircraft

- 5.1.2 Passenger Aircraft

- 5.1.2.1 Narrowbody Aircraft

- 5.1.2.2 Widebody Aircraft

- 5.2 Country

- 5.2.1 Canada

- 5.2.2 Mexico

- 5.2.3 United States

- 5.2.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Airbus SE

- 6.4.2 ATR

- 6.4.3 COMAC

- 6.4.4 De Havilland Aircraft of Canada Ltd.

- 6.4.5 Embraer

- 6.4.6 The Boeing Company

- 6.4.7 United Aircraft Corporation

7 KEY STRATEGIC QUESTIONS FOR AVIATION CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms