北米のEV用バッテリーパック:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

North America EV Battery Pack - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 292 Pages

- 納期

- 2~3営業日

- 商品コード

- 1692462

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

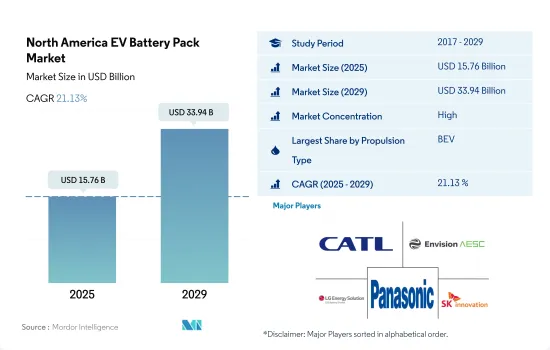

北米のEV用バッテリーパック市場規模は2025年に157億6,000万米ドルと推定・予測され、2029年には339億4,000万米ドルに達し、予測期間(2025-2029年)のCAGRは21.13%で成長すると予測されます。

バッテリー製造工場が北米電気自動車産業の成長を促進する見込み

- 2017年から2023年にかけて、北米では電気自動車の生産と導入が大幅に増加しています。2017年、北米で生産された電気自動車の総数は約20万台で、2022年には40万台以上に増加しました。この成長は、政府のインセンティブ、バッテリー価格の低下、消費者の意識向上など様々な要因によるものです。電気自動車産業における研究開発への取り組みも最近の動向で増加しています。

- 北米のEV用バッテリーパック市場は、政府の補助金やインセンティブ・プログラムに大きく後押しされ、大きな成長を遂げています。近年、環境に優しい交通手段の利用を促進することを目的としたこれらのプログラムにより、電気自動車の導入が顕著に増加しています。例えば、米国政府は電気自動車の購入に最大7,500米ドルの税額控除を導入し、電気自動車をより手頃な価格で、より多くの人々が利用できるようにしています。

- さらに、北米のEV市場の成長には、バッテリー製造工場の開拓が欠かせないです。現在、EV用バッテリーのほとんどはアジア、主に中国と韓国で製造されています。しかし、北米でもバッテリー製造工場の建設が計画されており、輸入バッテリーへの依存を減らし、北米のEV産業の成長を支えることになります。ブルームバーグ・ニュー・エナジー・ファイナンスの報告書によると、北米は二酸化炭素排出量を削減し、よりクリーンな輸送手段への移行を目指すため、2040年までにEVインフラに3,600億米ドルを投資すると予想されています。全体として、北米における電気自動車とバッテリーパックの将来は有望です。

米国とカナダにおける電気自動車普及の原動力となる政府の支援と投資

- 北米のEV用バッテリーパック市場は近年力強い成長を遂げており、米国とカナダではEVの導入が急増しています。この上昇には、政府のインセンティブ、排ガス規制の強化、消費者の環境意識の高まり、充電インフラの進歩など、いくつかの要因があります。

- 北米各地の政府は、さまざまなレベルでEVの普及を促進する政策やインセンティブを打ち出しています。こうした取り組みには、税額控除、補助金、リベート、充電インフラへの投資などが含まれます。こうした支援は消費者のEVへの関心を高め、バッテリーパックの需要を促進しています。注目すべきは、大手自動車メーカーやバッテリーメーカーが、この地域市場でEV用バッテリーパックの生産能力を増強していることです。例えば、テスラは米国ネバダ州でギガファクトリーを運営しており、バッテリー生産に特化しています。ゼネラルモーターズ、フォード、フォルクスワーゲンといった他の業界大手も、独自の国内バッテリー生産施設の設立計画を発表しています。

- バッテリー技術における継続的な研究開発努力は、エネルギー密度の向上、コスト削減、EVの航続距離の延長に焦点を当てています。ソリッドステートバッテリー、急速充電機能、バッテリー寿命の延長といった技術革新は、市場をさらに押し上げる構えです。さらに、主要な電池材料の入手可能性も重要な要素です。北米は、リチウム、ニッケル、コバルトのような重要な材料の埋蔵量を誇っており、今後数年間、現地生産とサプライチェーン活動を強化することができます。

北米のEV用バッテリーパック市場動向

北米電気自動車市場の主要企業は、テスラ、トヨタ、フォード、現代自動車、ホンダなど

- 北米の電気自動車市場は、2023年に市場の70%以上を占める5大プレイヤーによって大きく牽引されています。これらの有力企業には、テスラ、トヨタ・グループ、フォードグループ、現代自動車、ホンダが含まれます。テスラは、北米各国で電気自動車を最も多く販売しており、市場の約33%を占めています。同社は強力なイノベーション技術に注力しており、様々なEV部品(バッテリーなど)メーカーと強力な戦略的パートナーシップを結んでいます。米国を拠点とする企業であるため、北米の米国やカナダなどの主要国で優れた製品とサービスを提供し、強力な顧客基盤を持っています。

- トヨタグループは電気自動車販売台数第2位で、北米全体で約30.8%の市場シェアを占めています。同社は強力なサプライチェーンと流通網を持っています。トヨタは顧客の間で信頼できるブランドイメージを持っています。北米各国のEV販売台数では第3位。フォードグループが約9.9%の市場シェアで買収しました。強力なブランドイメージと多様な商品により、北米諸国で多くの顧客基盤を持っています。

- ヒュンダイは第4位で、北米全域でのEV販売で約5.48%の市場シェアを獲得しています。同社は強力な生産・サプライチェーン網を有し、リーズナブルな価格設定からプレミアムな価格設定まで、さまざまなタイプの顧客向けに革新的で多様な製品を幅広く提供しています。EV市場の第5位はホンダで、約5.22%の市場シェアを維持しています。北米でEVSを販売している他の企業には、ジープ、シボレー、BMW、ボルボなどがあります。

米国は莫大なEV需要を持つ最大の市場であり、2023年には地域全体のバッテリーパック市場の60%以上を占める。

- 2023年には、北米のいくつかの国で電気自動車の数が着実に増加したため、バッテリーの需要が急増しました。同地域では他にも多くのブランドやモデルが販売されているが、2023年の上位5モデル、テスラモデルY、テスラモデル3、トヨタRav 4、トヨタシエンタ、ホンダCRVが市場のかなりの部分を獲得しました。2023年の米国での販売台数は24万7,344台で、テスラモデルYがトップの座を維持しました。モデルYは、航続距離の長さ、座席数の多さ、荷物の積載量の多さなどから非常に人気が高いです。

- テスラモデル3は、2023年の米国での販売台数が21万5,500台で2位となりました。後輪駆動とパフォーマンス・バージョンがあります。その強力な性能特性により、モデル3は顧客を引きつけています。電気自動車販売では、トヨタRav4が米国および北米全域で14万9,938台を販売し、3位となりました。同車はプラグインハイブリッド技術と、Toyota Safety Senseを含む複数のADAS機能を搭載しています。

- トヨタ・シエンタは、米国で6万9,720台を販売し、電気自動車販売台数第4位を獲得しました。この車には、ハイブリッド・パワートレインを搭載した2.5 lエンジンのオプションがあります。7人乗りを求める大家族の消費者は、トヨタ・シエナに好意的な反応を示しています。5位はホンダCRVで、米国での2023年の販売台数は6万9,720台でした。その他の売れ筋モデルは、トヨタ・ハイランダー、ジープ・ラングラー、トヨタ・カムリ、ホンダ・アコード、フォード・マスタング・マッハEなどです。

北米のEV用バッテリーパック産業概要

北米のEV用バッテリーパック市場はかなり統合されており、上位5社で85.66%を占めています。この市場の主要企業は以下の通り。 Contemporary Amperex Technology(CATL), Envision AESC Japan, LG Energy Solution Ltd., Panasonic Holdings Corporation and SK Innovation(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 電気自動車販売台数

- OEM別電気自動車販売台数

- 売れ筋EVモデル

- 好ましいバッテリーケミストリーを持つOEM

- 電池パック価格

- 電池材料コスト

- 各電池化学の価格表

- 誰が誰に供給するか

- EVバッテリーの容量と効率

- EVの発売モデル数

- 規制の枠組み

- カナダ

- メキシコ

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- ボディタイプ

- バス

- LCV

- M&HDT

- 乗用車

- 推進タイプ

- BEV

- PHEV

- 電池化学

- LFP

- NCA

- NCM

- NMC

- その他

- 容量

- 15 kWh~40 kWh

- 40 kWh~80 kWh

- 80kWh以上

- 15kWh未満

- バッテリー形状

- 円筒形

- 袋

- 角型

- 方式

- レーザー

- ワイヤー

- コンポーネント

- 陽極

- カソード

- 電解液

- セパレーター

- 材料タイプ

- コバルト

- リチウム

- マンガン

- 天然黒鉛

- ニッケル

- その他の材料

- 国名

- カナダ

- 米国

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- A123 Systems LLC

- ACDELCO(Subsidiary Of General Motors)

- American Battery Solutions Inc.

- Clarios International Inc.

- Contemporary Amperex Technology Co. Ltd.(CATL)

- Electrovaya Inc.

- Envision AESC Japan Co. Ltd.

- LG Energy Solution Ltd.

- Nikola Corporation

- Panasonic Holdings Corporation

- QuantumScape Corp.

- SK Innovation Co. Ltd.

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The North America EV Battery Pack Market size is estimated at 15.76 billion USD in 2025, and is expected to reach 33.94 billion USD by 2029, growing at a CAGR of 21.13% during the forecast period (2025-2029).

Battery manufacturing plants are expected to fuel the growth of the North American electric vehicle industry

- From 2017 to 2023, there has been a significant increase in the production and adoption of electric vehicles in North America. In 2017, the total number of electric vehicles produced in North America was approximately 200,000, which increased to over 400,000 in 2022. This growth can be attributed to various factors, including government incentives, lower battery prices, and increased consumer awareness. Research and development efforts in the electric vehicle industry have also been increasing in recent years.

- The electric vehicle battery pack market in North America is experiencing significant growth, largely driven by government subsidies and incentive programs. In recent years, there has been a marked increase in the adoption of electric vehicles due to these programs, which aim to promote the use of environmentally friendly transportation. For instance, the US government has introduced tax credits of up to USD 7,500 for the purchase of electric vehicles, making them more affordable and accessible to a wider audience.

- Further, the development of battery manufacturing plants is critical to the growth of the EV market in North America. Currently, most EV batteries are manufactured in Asia, primarily in China and South Korea. However, there are plans to build more battery manufacturing plants in North America, which will help to reduce the region's reliance on imported batteries and support the growth of the local EV industry. According to a report by Bloomberg New Energy Finance, North America is expected to invest USD 360 billion in EV infrastructure by 2040 as the region seeks to reduce its carbon emissions and transition to cleaner transportation. Overall, the future of electric vehicles and battery packs in North America is promising.

Government support and investments driving electric vehicle adoption in the United States and Canada

- The North American electric vehicle (EV) battery pack market has witnessed robust growth in recent years, with both the United States and Canada seeing a surge in EV adoption. This uptick can be attributed to several factors, including government incentives, tightening emission regulations, growing environmental consciousness among consumers, and advancements in charging infrastructure.

- At various levels, governments across North America have been rolling out policies and incentives to spur EV adoption. These initiatives encompass tax credits, grants, rebates, and investments in charging infrastructure. Such support has bolstered consumer interest in EVs, thereby driving the demand for battery packs. Notably, major automakers and battery manufacturers are ramping up their production capacities for EV battery packs in the regional market. Tesla, for instance, operates its gigafactory in Nevada, United States, which is solely dedicated to battery production. Other industry giants like General Motors, Ford, and Volkswagen have also unveiled plans to establish their own domestic battery production facilities.

- Continued R&D endeavors in battery technology are focused on enhancing energy density, cost reduction, and extending the range of EVs. Innovations like solid-state batteries, rapid-charging capabilities, and prolonged battery life are poised to propel the market further. Additionally, the availability of key battery materials is a crucial factor. North America boasts substantial reserves of vital materials like lithium, nickel, and cobalt, which can bolster localized production and supply chain activities over the coming years.

North America EV Battery Pack Market Trends

The major players in the North American electric vehicle market include Tesla, Toyota, Ford, Hyundai, and Honda

- The North American electric vehicle market is majorly driven by the five major players, accounting for more than 70% of the market in 2023. These prominent players include Tesla, Toyota Group, Ford Group, Hyundai, and Honda. Tesla is the highest seller of electric vehicles in the various North American countries, accounting for around 33% of the market. The company focuses on strong innovation technologies and has strong strategic partnerships with various EV components (such as a battery) manufacturers. Being a US-based company, it has a strong customer base with great product and service offerings in major countries like the United States and Canada across North America.

- Toyota Group is the second largest seller of electric vehicles, accounting for around 30.8% market share across North America. The company has a strong supply chain and distribution network. Toyota has a reliable brand image among its customers. It ranks third in EV sales across various countries in North America. Ford Group acquired it with around 9.9% of the market share. The company has a large customer base in North American countries due to its strong brand image and diverse offerings.

- Hyundai is the fourth largest player, acquiring around 5.48% of the market share in EV sales across North America. The company has a strong production and supply chain network, with wide innovative and diverse products offered for various types of customers looking from reasonable to premium pricing. The fifth-largest player operating in the EV market is Honda, maintaining its market share at around 5.22%. Some of the other players selling EVS in North America include Jeep, Chevrolet, BMW, and Volvo.

The United States was the largest market with huge EV demand and captured more than 60% of the battery pack market across the region in 2023

- In 2023, the demand for batteries surged as the number of electric vehicles steadily climbed across several North American countries. Many other brands and models are sold in the region, but the top five models in 2023, the Tesla Model Y, Tesla Model 3, Toyota Rav 4, Toyota Sienna, and Honda CRV, acquired a significant portion of the market. With 247,344 units sold in the United States in 2023, the Tesla Model Y maintained its top spot. The Model Y is very well-liked because of its long range, strong seating capacity, and huge luggage capacity.

- The Tesla Model 3 took second place with 215,500 sales in the United States in 2023. The rear-wheel drive and performance versions of the vehicle are available. Due to its strong performance characteristics, Model 3 is drawing customers. The Toyota Rav4 took third position in electric car sales, with sales of 149,938 in the United States and throughout North America. The vehicle has plug-in hybrid technology and several ADAS features, including Toyota Safety Sense.

- The Toyota Sienna has acquired fourth place in the electric vehicle models' sales, with 69,720 in the United States. The car comes with the option of a 2.5 l engine with a hybrid powertrain. Consumers with big families looking for seven-seater cars have positively responded to the Toyota Sienna. The fifth place was acquired by the Honda CRV, selling 69,720 units in 2023 in the United States. Other top-selling models include Toyota Highlander, Jeep Wrangler, Toyota Camry, Honda Accord, and Ford Mustang Mach-E.

North America EV Battery Pack Industry Overview

The North America EV Battery Pack Market is fairly consolidated, with the top five companies occupying 85.66%. The major players in this market are Contemporary Amperex Technology Co. Ltd. (CATL), Envision AESC Japan Co. Ltd., LG Energy Solution Ltd., Panasonic Holdings Corporation and SK Innovation Co. Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Electric Vehicle Sales

- 4.2 Electric Vehicle Sales By OEMs

- 4.3 Best-selling EV Models

- 4.4 OEMs With Preferable Battery Chemistry

- 4.5 Battery Pack Price

- 4.6 Battery Material Cost

- 4.7 Price Chart Of Different Battery Chemistry

- 4.8 Who Supply Whom

- 4.9 EV Battery Capacity And Efficiency

- 4.10 Number Of EV Models Launched

- 4.11 Regulatory Framework

- 4.11.1 Canada

- 4.11.2 Mexico

- 4.11.3 US

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Body Type

- 5.1.1 Bus

- 5.1.2 LCV

- 5.1.3 M&HDT

- 5.1.4 Passenger Car

- 5.2 Propulsion Type

- 5.2.1 BEV

- 5.2.2 PHEV

- 5.3 Battery Chemistry

- 5.3.1 LFP

- 5.3.2 NCA

- 5.3.3 NCM

- 5.3.4 NMC

- 5.3.5 Others

- 5.4 Capacity

- 5.4.1 15 kWh to 40 kWh

- 5.4.2 40 kWh to 80 kWh

- 5.4.3 Above 80 kWh

- 5.4.4 Less than 15 kWh

- 5.5 Battery Form

- 5.5.1 Cylindrical

- 5.5.2 Pouch

- 5.5.3 Prismatic

- 5.6 Method

- 5.6.1 Laser

- 5.6.2 Wire

- 5.7 Component

- 5.7.1 Anode

- 5.7.2 Cathode

- 5.7.3 Electrolyte

- 5.7.4 Separator

- 5.8 Material Type

- 5.8.1 Cobalt

- 5.8.2 Lithium

- 5.8.3 Manganese

- 5.8.4 Natural Graphite

- 5.8.5 Nickel

- 5.8.6 Other Materials

- 5.9 Country

- 5.9.1 Canada

- 5.9.2 US

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 A123 Systems LLC

- 6.4.2 ACDELCO (Subsidiary Of General Motors)

- 6.4.3 American Battery Solutions Inc.

- 6.4.4 Clarios International Inc.

- 6.4.5 Contemporary Amperex Technology Co. Ltd. (CATL)

- 6.4.6 Electrovaya Inc.

- 6.4.7 Envision AESC Japan Co. Ltd.

- 6.4.8 LG Energy Solution Ltd.

- 6.4.9 Nikola Corporation

- 6.4.10 Panasonic Holdings Corporation

- 6.4.11 QuantumScape Corp.

- 6.4.12 SK Innovation Co. Ltd.

7 KEY STRATEGIC QUESTIONS FOR EV BATTERY PACK CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 292 Pages

- 納期

- 2~3営業日