中東・アフリカの軟包装:市場シェア分析、産業動向、成長予測(2025~2030年)

Middle East And Africa Flexible Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1692157

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

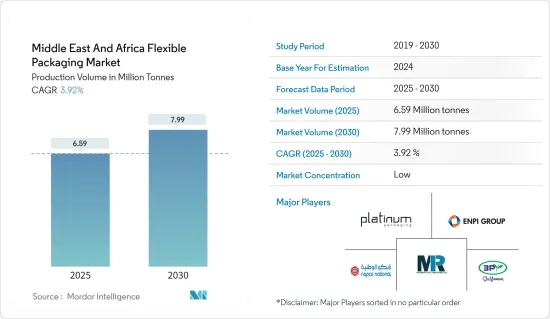

中東・アフリカの軟包装市場規模は、生産量ベースで2025年の659万トンから2030年には799万トンに拡大し、予測期間(2025~2030年)のCAGRは3.92%と予測されています。

軟包装は、より経済的でカスタマイズ可能な製品包装オプションを可能にします。飲食品、パーソナルケア、製薬業界など、汎用性の高い包装を必要とする業界では特に有用です。軟包装は、その高い効率性と費用対効果により人気が高まっています。

主なハイライト

- この地域の包装事業は、消費者の期待の変化と人口の増加により、過去10年間一貫した成長を遂げてきました。同地域では、包装材料における様々な技術革新が見られることから、持続可能性と環境的側面が引き続き重視される可能性があります。紙や段ボール、再生PET(rPET)、バイオプラスチックなど、リサイクル可能で持続可能な包装材料への需要の高まりが市場成長を後押ししています。

- さらに、アラブ首長国連邦における消費者の食の嗜好の変化は、特に飲食品業界にとって包装業界に大きな成長機会をもたらしています。アラブ首長国連邦の金融機関Alpen Capitalの報告書によると、中東・アフリカ地域の食品産業は、その戦略的立地と人口増加により成長すると推定されています。パンデミック後のオンライン食品宅配の急増は、ラップ、スリーブ、ラベルなどの軟包装の需要を高め、業界の成長を牽引しています。

- さらに、国内の消費者の間で欧米の食習慣の影響が強まっていることも、包装食品の需要を押し上げています。この動向はさらに、移民、旅行者、若い消費者が調理済み食品、加工食品、冷凍食品の需要を牽引しています。

- スタンドアップパウチは硬質包装よりも軽量で、材料使用量が少なく、輸送コストが低いため、包装食品メーカーに利益をもたらしています。同地域では飲料業界によるパウチの消費が増加しており、同市場からの需要は増加すると予想されます。

- 中東はリサイクルインフラが限られているため、軟包装業界では大きな課題に直面しています。この問題は、持続可能性への懸念が世界的に、そしてこの地域内でも高まるにつれて、ますます顕著になってきています。環境問題に対する認識が高まり、リサイクルと廃棄物削減を促進するためのさまざまな政府イニシアティブが実施されているにもかかわらず、適切なリサイクル施設とシステムの必要性が依然として大きな障害となっています。このような状況は、この地域のフレキシブル・パッケージング・メーカーとユーザーにとって複雑な力学を生み出し、市場の需要と新たな持続可能性要件とのバランスを取ろうと努力しています。

中東・アフリカの軟包装市場の動向

食品産業が最大のエンドユーザーに

- 中東のパッケージ食品市場は、食品加工技術の先進化と消費者のライフスタイルの変化により成長を遂げています。これらの要因は製品需要を増加させ、予測期間中の軟包装の成長を促進すると予想されます。

- さらに、中東の人口増加と肉、魚介類、鶏肉に対する食欲の高まりが、軟質プラスチック包装の需要を煽っています。メーカーが利便性と保存期間の延長を求める消費者の嗜好に応えようとしているため、包装材料とデザインの革新もこの動向に寄与しています。

- さらに、アラブ首長国連邦やサウジアラビアなどの中東諸国におけるeコマースの成長が、コンビニエンス・フード需要を促進しています。この動向は、食品の鮮度や保温性を長期間維持するのに役立つフィルム、ラップ、パウチ、袋などの軟包装を取り巻く環境を再構築しています。

- 中東・アフリカの主要な塊であるGCC地域の食品産業は、パンデミック後に回復しました。人口の増加に加え、社会人の増加や多くの海外駐在員の増加が、この地域の食品業界を牽引しています。高い栄養価を求めるこの地域の消費者の健康的な食習慣に対する意識の高まりが、生鮮食品や有機食品に対する需要の高まりにつながっています。パウチは重量と強度が低いため、食品包装にプラスチック袋やパウチを使用することが、軟質プラスチック包装の需要を牽引しています。

- アルペン・キャピタルの報告書によると、GCC諸国における食品消費量は、一人当たり所得の増加と人口の増加に牽引され、2027年には5,620万トンに成長すると推定されています。食料消費量ではサウジアラビアが同地域最大の国で、アラブ首長国連邦とバーレーンがこれに続くと推定されます。

サウジアラビアが主要市場シェアを占める

- サウジアラビアは3つの大陸が交差する戦略的な位置にあるため、中東・アフリカ、アジアの市場への重要なアクセスポイントとなっています。サウジアラビアの整備されたインフラ、効率的な交通網、先進的な物流施設は、世界な貿易と投資の機会に大きなメリットをもたらします。

- サウジアラビアは、新たな機会と成長を求める企業にとって魅力的な進出先として位置づけられています。サウジアラビアの野心的な経済改革、戦略的イニシアティブ、進化するビジネス環境は、サウジアラビアを潜在的な世界ビジネスの中心地へと変貌させています。この変貌は、国際市場におけるサウジアラビアの重要性の高まりを反映し、世界中の包装ビジネスからますます注目を集めています。

- 食品、小売、消費財、医薬品などの分野で軟包装ソリューションの需要が高まる中、サウジアラビアに注目する企業が増えています。サウジアラビアはその戦略的位置づけから、地域および国際貿易、投資、技術革新の形成において重要な役割を果たすことになります。

- 調理済み食品(Ready-to-Eat Meals)および冷凍食品(Frozen Food)分野は、消費前に最小限の準備しか必要としない、あるいは準備の必要がない調理済み食品を提供します。このセグメントは、ペースの速い都市のライフスタイルと多様な文化の影響により、中東諸国、特にサウジアラビアで人気を集めています。

- サウジアラビアの加工肉、シーフード、代替肉市場は成長を遂げています。2023年の市場規模は約1,499.10トンでした。2027年には約1,839.50トンに増加すると予測されているが、これは加工肉に対する消費者の嗜好の変化と増加を反映しています。

中東・アフリカの軟包装産業の概要

中東・アフリカの軟包装市場は断片化されており、複数の企業が地域ごとに事業を展開しています。競合の度合いは、ブランド・アイデンティティ、強力な競争戦略、透明性の度合い、企業集中率など、市場に影響を与える様々な要因によって決まる。市場の主なプレーヤーとしては、Napco National、3P Gulf Group、Platinum Packaging Ltd、Aalmir Plastic Industries LLC、ENPI Groupなどが挙げられます。

- 2024年6月- 持続可能なパッケージング・ソリューションの主要企業であるフルタマキは、アラブ首長国連邦(UAE)のフレキシブル・パッケージング製造事業を統合する計画を明らかにしました。この戦略では、ジェベル・アリの施設を維持する一方、ラスアルハイマの施設を大幅に拡張します。同社によると、この動きは業務を合理化し、競合力を高め、将来の地域拡大への足場を固めることを目的としています。

- 2024年5月-Napco Nationalはアラブ首長国連邦を拠点とするブランドAlsharq Plas LLCを戦略的に買収し、包装部門を拡大。買収後、Alsharq Plas LLCのブランドはNapco Sharq Plas LLCに変更されます。この動きは、GCC地域の顧客の高度化する需要に対応する両社の能力を強化するものです。さらに、この買収はNapco Nationalの市場での存在感を高めるものと期待されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヵ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界エコシステム分析サプライヤー、素材メーカーなど

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係の強さ

- 代替品の脅威

- 輸出入分析

第5章 市場力学

- 市場促進要因

- 加工食品需要の着実な増加

- 市場抑制要因

- 高い原材料コストと限られたリサイクルインフラ

- 市場機会

- 持続可能な包装ソリューションへの需要の高まり

第6章 市場セグメンテーション

- 材料タイプ別

- プラスチック

- ポリエチレン(PE)

- ポリプロピレン(PP)

- ポリエチレンテレフタレート(PET)

- その他プラスチック(PVC、PAなど)

- 紙類

- アルミニウム

- コンポスト可能素材(PLA、PBS、PHA、PBATなど)

- プラスチック

- 製品タイプ別

- パウチ・袋

- フィルム・ラップ

- 熱成形フィルム

- ストレッチフィルム

- シュリンクフィルム

- クリンプフィルム

- ラベルとスリーブ

- 蓋とライナー

- ブリスター包装

- エンドユーザー産業別

- 食品

- 飲料

- 医薬品

- 化粧品・パーソナルケア

- 家庭用品

- ペットケア

- タバコ

- その他のエンドユーザー産業(エレクトロニクス、化学、農業製品など)

- 国別

- サウジアラビア

- アラブ首長国連邦

- モロッコ

- エジプト

- 南アフリカ

第7章 競合情勢

- 企業プロファイル

- Napco National

- 3P Gulf Group

- Platinum Packaging Ltd

- Aalmir Plastic Industries LLC

- ENPI Group

- Amber Packaging Industries LLC

- Emirates Printing Press(LLC)

- Huhtamaki Flexibles UAE(Huhtamki Oyj)

- Gulf East Paper and Plastic Industries LLC

- Radiant Packaging Industry LLC

- Arabian Flexible Packaging LLC

- Integrated Plastics Packaging LLC

- Constantia Flexibles Afripack(Constantia Flexibles)

- SwissPac UAE

- Hotpack Packaging Industries LLC

- Falcon Pack

第8章 投資の展望

第9章 市場の将来展望

目次

The Middle East And Africa Flexible Packaging Market size in terms of production volume is expected to grow from 6.59 million tonnes in 2025 to 7.99 million tonnes by 2030, at a CAGR of 3.92% during the forecast period (2025-2030).

Flexible packaging allows more economical and customizable options for packaging products. It is particularly useful in industries requiring versatile packaging, including food and beverage, personal care, and pharmaceutical industries. Flexible packaging has grown popular due to its high efficiency and cost-effectiveness.

Key Highlights

- The packaging business in the region has experienced consistent growth over the last decade due to changing consumer expectations and a rising population. Sustainability and environmental aspects might continue to be emphasized in the region as the market is witnessing various innovations in packaging materials. Increased demand for recyclable and sustainable packaging materials, such as paper and cardboard, recycled PET (rPET), and bioplastics, are driving market growth.

- Moreover, the changing consumer food preferences in the United Arab Emirates have created significant growth opportunities in the packaging industry, especially for the food and beverage industry. According to a report by Alpen Capital, a financial institute in the United Arab Emirates, the food industry in the Middle East and African region is estimated to grow due to its strategic location and growing population. Post-pandemic, the surge in online food delivery has enhanced the demand for flexible packaging such as wraps, sleeves, labels, and others, driving industry growth.

- Additionally, the increasing influence of Western eating habits among domestic consumers has boosted the demand for packaged foods. This trend is further supported by immigrants, tourists, and young consumers driving the demand for ready-to-eat, processed, and frozen foods.

- The lighter weight, reduced material use, and lower shipping cost of stand-up pouches than the rigid packaging benefit the packaged food producers. With the beverage industry increasingly consuming pouches in the region, the demand from the market is expected to increase.

- The Middle East faces significant challenges in the flexible packaging industry due to its limited recycling infrastructure. This issue has become increasingly prominent as sustainability concerns gain traction globally and within the region. Despite growing awareness of the environmental problems and implementing various government initiatives to promote recycling and waste reduction, the need for adequate recycling facilities and systems continues to pose a substantial obstacle. This situation creates a complex dynamic for flexible packaging manufacturers and users in the region as they strive to balance market demands with emerging sustainability requirements.

Middle East and Africa Flexible Packaging Market Trends

Food Industry to be the Largest End User

- The Middle East packaged food market is experiencing growth due to advancements in food processing techniques and changing consumer lifestyles. These factors are expected to increase product demand, driving the growth of flexible packaging during the forecast period.

- Further, the rising Middle Eastern population and a growing appetite for meat, seafood, and poultry fuel the demand for flexible plastic packaging. Innovations in packaging materials and designs also contribute to this trend, as manufacturers seek to meet consumer preferences for convenience and extended shelf life.

- In addition, the growth of e-commerce in Middle Eastern countries, such as the United Arab Emirates and Saudi Arabia, is driving demand for convenience food. This trend is reshaping the flexible packaging landscape, including films, wraps, pouches, and bags, which help maintain food freshness and warmth for extended periods.

- The food industry in the GCC region, a major chunk of Middle East and Africa, recovered after the pandemic. The growing population, coupled with the increasing number of working professionals and many expatriates, is a major driver for the region's food industry. Growing awareness of healthy eating habits of consumers in the region seeking high nutritional value has led to rising demand for fresh and organic food items. The use of plastic bags and pouches for food packaging, as pouches are low in weight and strength, drives the demand for flexible plastic packaging.

- According to a report by Alpen Capital, food consumption in GCC countries is estimated to grow to 56.2 million metric tons in 2027, driven by the increase in per capita income and growing population. Saudi Arabia is estimated to be the largest country in the region in terms of food consumption, followed by the United Arab Emirates and Bahrain.

Saudi Arabia Holds Major Market Share

- Saudi Arabia's strategic location at the intersection of three continents positions it as a critical access point to markets in the Middle East, Africa, and Asia. The country's well-developed infrastructure, efficient transportation networks, and advanced logistics facilities provide significant advantages for global trade and investment opportunities.

- Saudi Arabia has positioned itself as an attractive destination for businesses seeking new opportunities and growth. The Kingdom's ambitious economic reforms, strategic initiatives, and evolving business landscape transform it into a potential global business center. This transformation has garnered increasing attention from packaging businesses worldwide, reflecting Saudi Arabia's growing importance in the international market.

- With the demand for flexible packaging solutions rising in sectors like food, retail, consumer goods, and pharmaceuticals, businesses are increasingly eyeing Saudi Arabia. The country's strategic positioning will make it a key player in shaping regional and international trade, investment, and innovation.

- The Ready-to-Eat Meals and Frozen Food segment offers prepared food that requires minimal or no preparation before consumption. This segment is gaining popularity in Middle Eastern countries, particularly in Saudi Arabia, due to the fast-paced urban lifestyle and diverse cultural influences.

- The Saudi Arabian market for processed meat, seafood, and meat alternatives is experiencing growth. In 2023, the market volume was approximately 1,499.10 metric tons. Projections indicate an increase to about 1,839.50 metric tons by 2027, reflecting the country's changing and growing consumer preferences for processed meat.

Middle East and Africa Flexible Packaging Industry Overview

The Middle East and Africa Flexible Packaging Market are fragmented, with multiple players in the market operating regionally. The degree of competition depends on various factors affecting the market, such as brand identity, powerful competitive strategy, degree of transparency, and firm concentration ratio. Some of the major players in the market are Napco National, 3P Gulf Group, Platinum Packaging Ltd, Aalmir Plastic Industries LLC, and ENPI Group, among others.

- June 2024 - Huhtamaki, a key player in sustainable packaging solutions, has revealed plans to consolidate its Flexible Packaging manufacturing operations in the United Arab Emirates (UAE). The strategy involves retaining its Jebel Ali facility while significantly enlarging its Ras Al Khaimah site. According to the company, this move aims to streamline operations, elevate competitiveness, and fortify its foothold for future regional expansion.

- May 2024 - Napco National expanded its packaging division by strategically acquiring Alsharq Plas LLC, a brand based in the United Arab Emirates. Post-acquisition, Alsharq Plas LLC will be rebranded as Napco Sharq Plas LLC. This move is poised to bolster both companies' capabilities in meeting the increasingly sophisticated demands of customers in the GCC region. Furthermore, the acquisition is expected to bolster Napco National's market presence.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Ecosystem Analysis Suppliers, Material Manufacturers, etc.

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitute Products

- 4.4 Import-Export Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Steady Rise in Demand for Processing Food

- 5.2 Market Restraints

- 5.2.1 High Raw Material Costs and Limited Recycling Infrastructure

- 5.3 Market Opportunities

- 5.3.1 Growing Demand for Sustainable Packaging Solution

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Plastics

- 6.1.1.1 Polyethene (PE)

- 6.1.1.2 Polypropylene (PP)

- 6.1.1.3 Polyethylene Terephthalate (PET )

- 6.1.1.4 Other Plastics (PVC, PA, etc.)

- 6.1.2 Paper

- 6.1.3 Aluminum

- 6.1.4 Compostable Materials (PLA, PBS, PHA, PBAT, etc.)

- 6.1.1 Plastics

- 6.2 By Product Type

- 6.2.1 Pouches And Bags

- 6.2.2 Films And Wraps

- 6.2.2.1 Thermoforming Film

- 6.2.2.2 Stretch Films

- 6.2.2.3 Shrink Film

- 6.2.2.4 Cling Film

- 6.2.3 Labels And Sleeves

- 6.2.4 Lidding And Liners

- 6.2.5 Blister Packaging

- 6.3 By End-user Industry

- 6.3.1 Food

- 6.3.2 Beverages

- 6.3.3 Pharmaceuticals

- 6.3.4 Cosmetics And Personal Care

- 6.3.5 Household Care

- 6.3.6 Pet Care

- 6.3.7 Tobacco

- 6.3.8 Other End-user Industries (Electronics, Chemicals, Agricultural Products etc.)

- 6.4 By Country

- 6.4.1 Saudi Arabia

- 6.4.2 United Arab Emirates

- 6.4.3 Morocco

- 6.4.4 Egypt

- 6.4.5 South Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Napco National

- 7.1.2 3P Gulf Group

- 7.1.3 Platinum Packaging Ltd

- 7.1.4 Aalmir Plastic Industries LLC

- 7.1.5 ENPI Group

- 7.1.6 Amber Packaging Industries LLC

- 7.1.7 Emirates Printing Press (LLC)

- 7.1.8 Huhtamaki Flexibles UAE (Huhtamki Oyj)

- 7.1.9 Gulf East Paper and Plastic Industries LLC

- 7.1.10 Radiant Packaging Industry LLC

- 7.1.11 Arabian Flexible Packaging LLC

- 7.1.12 Integrated Plastics Packaging LLC

- 7.1.13 Constantia Flexibles Afripack (Constantia Flexibles)

- 7.1.14 SwissPac UAE

- 7.1.15 Hotpack Packaging Industries LLC

- 7.1.16 Falcon Pack

8 INVESTMENT OUTLOOK

9 FUTURE OUTLOOK OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日