|

市場調査レポート

商品コード

1692018

アジア太平洋のミルクプロテイン:市場シェア分析、産業動向、成長予測(2025~2030年)Asia-Pacific Milk Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋のミルクプロテイン:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 228 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

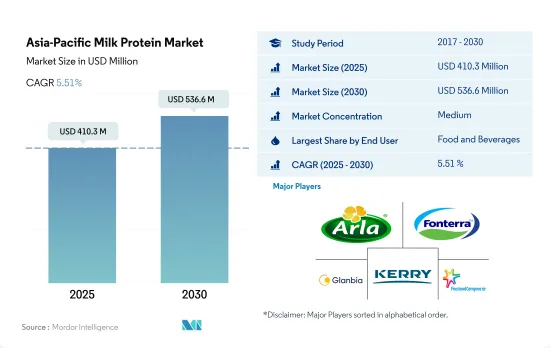

アジア太平洋のミルクプロテイン市場規模は2025年に4億1,030万米ドルと推定され、2030年には5億3,660万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは5.51%で成長する見込みです。

ミルクプロテインのスナック、飲食品、ベーカリー産業における多様な用途に支えられ、飲食品が84%の市場シェアで市場をリードしています。

- ミルクプロテインの高い機能性が、他のタンパク源との組み合わせによるF&Bセグメントでの応用を後押ししています。より健康志向の高い消費者に対応するため、メーカーは卵の代用品として様々な飲料、低脂肪スナックなどをベーカリーで製造しています。栄養強化食品は、ミルクプロテインセグメントにおける事業にとって大きな機会となります。飲食品全体のタンパク質の動向から、タンパク質強化は最重要の選択肢となっており、消費者は購入時にタンパク質と食物繊維の表示を求めるようになっています。2023年のミルクプロテイン市場は主にF&B部門が支配的であり、その用途の84%は金額ベースでスナック、飲料、ベーカリー産業が占めています。

- ミルクプロテインはサプリメント市場の大部分を占め、主にベビー用粉ミルクが予測期間中に金額ベースでCAGR 5.08%で上昇します。パック入りのベビーフードは、乳児に適切な栄養素を提供するため、都市部では一般的です。2021年のインドの女性労働力率は19.23%でした。働く母親の数が増加しているため、乳児用食品企業は、この地域で増大する手軽な栄養補給の需要に対応するために、ミルクタンパク質のサプリメントのような栄養豊富な製品を開発するようになりました。

- ミルクプロテインは卵の代替に高い効果を発揮し、ベーカリー産業での需要を押し上げています。2022年には数量ベースで53%の用途シェアがありました。鳥インフルエンザが懸念される中国のような国々では、卵の代替動向の中でミルクプロテインがさらに急増すると予想されます。乳タンパク材料は、パン、ケーキ、ペストリー、クッキー、クラッカー、アイシング、フィリング、グレーズなど幅広い用途で、より栄養価が高くおいしいベーカリー製品を求める消費者の需要の高まりに応えるのに役立ちます。

健康的でタンパク質を強化した飲料に対する国民の受け入れに変化が生じています。インドは中国、その他のアジア太平洋に次ぐ第3位

- 2022年、中国はトップの座を維持。新生児栄養、臨床食、スポーツ、ウェイトトレーニングといった専門的な製品カテゴリーにおいて、ミルクプロテインの魅力が高まっていることがその理由です。中国では最近、高タンパク商品が大きな注目を集めており、食品購入前にタンパク質が最も望まれる要素の1つであることが確認されています。2020年には、中国国民の36%以上が高タンパク食品の購入に関心を持っています。同国は予測期間を通じて最大の開発ポテンシャルを持つと予想され、金額ベースのCAGRは5.01%です。

- 中国に次いで、インドでも健康志向の消費者が増加の一途をたどっています。インド人の肥満率の着実な上昇により、健康的でタンパク質強化飲料に対する国民の受け入れ態勢が変化しています。2021年には、太りすぎの女性の割合が20.6%から24%に、男性では18.9%から22.9%に増加しました。ミルクプロテインは、全体的なカロリー摂取量を減らし、甘いものや高カロリー食品への欲求を減らすのに役立ちます。定期的な運動習慣と組み合わせれば、MPIやMPCは健康的かつ持続的な減量に役立ちます。したがって、予測期間中、同国のCAGRは4.62%で、2番目に速い成長が予測されます。

- ミルクプロテイン市場のサプリメントセグメントは、オーストラリアの予測期間において金額ベースでCAGR 2.90%を記録すると予測されています。薬用サプリメントやスポーツ栄養サプリメントのような主要用途セグメントの大幅な成長が、今後数年間の栄養補助食品用ミルクプロテイン市場を牽引すると予測されます。2021年には、オーストラリアの全年齢層のほぼ半数(46.6%)が1つ以上の慢性疾患を有し、ほぼ5人に1人(18.6%)が2つ以上の慢性疾患を有しています。

アジア太平洋のミルクプロテイン市場動向

ヘルス&フィットネスセンターの増加が市場を牽引

- 産業を牽引しているのは、健康に関する関心の高まりとヘルスクラブの会員数拡大です。フィットネスクラブ/ヘルスクラブの増加は、消費者の利用可能性とその関与率をさらに促進します。例えば、2020年には中国が2万7,000クラブと、この地域で最も多くのヘルスフィットネスクラブを有していました。韓国と日本のフィットネスクラブはそれぞれ6,590と4,950でした。

- フィットネスクラブはこの地域のスポーツ栄養製品の主要市場であるため、フィットネスクラブ数の増加は市場に大きな影響を与えます。International Health, Racquet, and Sportsclub Association(IHRSA)によると、この地域ではフィットネスフランチャイズが増加しており、スポーツ栄養セグメントの売上を牽引しています。IHRSAは、ヘルスクラブの再開から、COVID-19救済策にヘルス&フィットネス産業を含めるよう議員に促すことまで、国や州レベルの草の根キャンペーンを展開し、7万9,000人以上のフィットネス関係者や消費者がパンデミックに関連するIHRSAのキャンペーンで行動を起こしました。

- 健康的なライフスタイルを送ることの重要性が、スポーツ栄養市場を活性化。ここ数年、インドのスポーツ栄養市場が加速度的に成長しているのは、主にインドのスポーツ産業の大きな成長、アスリートやボディビルダーにおける各種健康サプリメントやエナジードリンクへの強い需要、高いレベルのフィットネスと栄養を必要とするスポーツや活動への若者の参加の増加によって拍車がかかっています。プロテインサプリメントは市場をリードしており、このセグメントにおける消費全体の70%のシェアを占めています。インドのスポーツ栄養市場は現在、未組織部門に属しており、市場規模は130億インドルピー以上、前年比成長率は約25%です。

インドのような発展途上国では、政府のイニシアティブが牛乳生産を支援しています。

- グラフは牛乳とヤギ乳の総生産量を表しています。この地域では、インドと中国が最も生乳生産量の多い国で、生産量の80%近くを占めています。過去10年間で最も力強い伸びを記録したのは東南アジアであり、生乳の伝統的消費の欠如と低関税が相まって、同地域では輸入乳製品が国内必要量の4分の1近くを占めるに至っています。アジアにおける生乳生産が世界生産の主要原動力となる可能性が高く、その原動力は引き続き、インドとパキスタンにおける乳牛頭数の増加と集乳効率の向上であり、中国の大規模農場における生産量の増加です。

- 2021年の中国の生乳生産量は4.5%増の3,450万トン超となります。これは生産性の向上によるもので、これにより中国の生乳生産量と消費量が急増しています。輸入も、消費者の需要と中国の製造業への要求により、プラス成長を示しています。ミルクプロテインの生産に主に使用される脱脂粉乳は、中国の食品産業が輸入脱脂粉乳に依存しているため増加しています。

- インドのような国では、州ごとに特定の規制を実施する政府当局によって生乳生産が高度にサポートされています。インドでは生乳生産量を増やすため、ウッタル・プラデーシュ州政府が生乳保存センターとグリーンフィールド酪農場を設立しています。国連食糧農業機関法人統計データベース(FAOSTAT)の生産データによると、インドは生乳生産量が最も多く、世界第1位で、2021~22年には世界の生乳生産量の24%を占めます。

アジア太平洋のミルクプロテイン産業概要

アジア太平洋のミルクプロテイン市場は適度に統合されており、上位5社で49.32%を占めています。この市場の主要企業は、 Arla Foods amba、Fonterra Co-operative Group Limited、Glanbia PLC、Kerry Group PLC、Koninklijke FrieslandCampina N.V.などです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- エンドユーザー市場規模

- ベビーフードと乳児用調製粉乳

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品と乳製品代替製品

- 高齢者栄養・医療栄養

- 肉・鶏肉・魚介類と肉代替製品

- RTE/RTC食品

- スナック

- スポーツ/パフォーマンス栄養

- 動物飼料

- パーソナルケアと化粧品

- タンパク質消費動向

- 動物

- 生産動向

- 動物

- 規制の枠組み

- オーストラリア

- 中国

- インド

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- 形態

- 濃縮物

- 単離液

- エンドユーザー

- 動物飼料

- 飲食品

- サブエンドユーザー別

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 乳製品及び乳製品代替製品

- RTE/RTC食品

- スナック

- パーソナルケアと化粧品

- サプリメント

- サブエンドユーザー別

- ベビーフードと乳児用調製粉乳

- 高齢者栄養と医療栄養

- スポーツ/パフォーマンス栄養

- 国別

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- ニュージーランド

- 韓国

- タイ

- ベトナム

- その他のアジア太平洋

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Arla Foods amba

- Fonterra Co-operative Group Limited

- Glanbia PLC

- Groupe LACTALIS

- Kerry Group PLC

- Koninklijke FrieslandCampina N.V.

- Milligans Food Group Limited

- Morinaga Milk Industry Co. Ltd

- Olam International Limited

第6章 CEOへの主要戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

The Asia-Pacific Milk Protein Market size is estimated at 410.3 million USD in 2025, and is expected to reach 536.6 million USD by 2030, growing at a CAGR of 5.51% during the forecast period (2025-2030).

Food and beverages leads the market with 84% market share, supported by the varied usage of milk protein in snacks, beverages, and bakery industries

- The higher functionality of milk proteins drives their application in the F&B segment in combination with other protein sources. To cater to more health-conscious consumers, manufacturers have produced a variety of beverages, reduced-fat snacks, and more in bakeries as egg replacements. Nutritionally fortified foods offer a significant opportunity for the business in the milk protein segment. The trend in protein across food and beverages makes protein fortification a top choice, and consumers are looking for protein and fiber claims while purchasing. The milk protein market is majorly dominated by the F&B sector in 2023, where 84% by value of its application is shared by the snacks, beverages, and bakery industries.

- Milk proteins account for a large portion of the supplements market, primarily rising in baby formula at a CAGR of 5.08% by value over the forecast period. Packaged baby foods are common in cities because they provide appropriate nutrients for infants. In 2021, the female labor force participation rate in India was 19.23%. An increase in the number of working mothers has encouraged infant food firms to create nutrient-rich products like milk protein supplements to meet the region's growing demand for easy nourishment.

- Milk protein's high efficacy in egg replacement is boosting its demand in the bakery industry. It had an application share of 53% by volume in 2022. For countries like China, where Avian flu is a budding concern, milk protein is expected to surge further amid egg replacement trends. Milk protein ingredients help formulators meet growing consumer demand for more nutritious and delicious bakery offerings across a wide range of applications such as bread, cakes, pastries, cookies, and crackers, as well as icings, fillings, and glazes.

With country's experiencing a shift in population's acceptance of healthy and protein-fortified drinks. India ranked 3rd behind China and Rest of Asia-Pacific countries

- In 2022, China maintained its top position. Milk protein's increased appeal in specialist product categories such as newborn nutrition, clinical diets, sports, and weight training was ascribed to this. High-protein goods have recently received significant public attention in China, identifying protein as one of the most desired elements before food purchase. In 2020, over 36% of Chinese citizens were interested in purchasing high-protein food products. The country is expected to have the biggest development potential throughout the forecast period, with a CAGR of 5.01% in terms of value.

- Next to China, India has been witnessing a constant rise in health-conscious consumers. The steady rise in obesity rates among Indians has shifted the population's acceptance of healthy and protein-fortified drinks. In 2021, the percentage of overweight women rose from 20.6% to 24%, while in men, the number increased from 18.9% to 22.9%. Milk proteins help reduce overall calorie intake and decrease the desire for sweet and high-calorie foods. When combined with a regular exercise routine, MPI or MPC can help people lose weight healthily and sustainably. Hence, the country is projected to have the second-fastest growth in the forecast period, with a CAGR of 4.62% by value.

- The supplement segment of the milk protein market is projected to register a CAGR of 2.90% by value in the forecasted period in Australia. The substantial growth of key application sectors like medicinal and sports nutrition supplements is anticipated to drive the milk protein market for dietary supplements in the coming years. In 2021, nearly half of Australians of all ages (46.6%) had one or more chronic conditions, and almost one in five (18.6%) had two or more chronic conditions.

Asia-Pacific Milk Protein Market Trends

Increasing number of health and fitness centers is driving the market

- The industry is driven by increased health-related concerns and expanding membership at health clubs. The increasing number of fitness clubs/health clubs further fosters the availability of consumers and their involvement rate. For instance, in 2020, China had the most health and fitness clubs in the region, with 27,000 clubs. South Korea and Japan had 6,590 and 4,950 fitness clubs, respectively.

- The increase in the number of health and fitness clubs majorly impacts the market as they are the major marketplace for sports nutrition products in the region. According to the International Health, Racquet, and Sportsclub Association (IHRSA), there is an increase in fitness franchises in the region, driving sales of the sports nutrition segment. The IHRSA launched national and state-level grassroots campaigns, ranging from reopening health clubs to urging lawmakers to include the health and fitness industry in any COVID-19 relief package, as more than 79,000 fitness professionals and consumers took action on IHRSA campaigns relating to the pandemic.

- The importance of leading a healthy lifestyle fuels the sports nutrition marketplace. The accelerated growth of the Indian sports nutrition market in the last few years has been spurred primarily by the huge growth in the Indian sports industry, strong demand for various health supplements and energy drinks among athletes and bodybuilders, and increasing youth participation in sports and activities that require a high level of fitness and nutrition. Protein supplements lead the market, accounting for a share of 70% of the overall consumption in this segment. The Indian sports nutrition market currently lies in the unorganized sector, with a market size of over INR 1,300 crore and a Y-o-Y growth of about 25%.

Government initiatives are supporting the milk production in developing countries such as India

- The graph given depicts the total production of cow milk and goat milk, as these are commonly used raw materials for milk proteins. In the region, India and China are the highest milk-producing countries, accounting for nearly 80% of production. The strongest gains over the past decade have been registered in Southeast Asia, where a lack of traditional consumption of fresh milk, combined with low tariffs, has led to imported milk products accounting for nearly one-quarter of domestic requirements in the subregion. Milk production in Asia is likely to be the primary driver of global output, which continues to be driven by rising dairy cattle numbers and increasing milk collection efficiency in India and Pakistan, with rising output in large-scale farms in China.

- China's milk production in the region increased by 4.5% to more than 34.5 MMT in 2021. This is due to improved productivity, which caused China's production and consumption of milk to grow rapidly. Imports are also showing positive growth due to consumer demand and requirements for the manufacturing industries in China. Skim milk powder, which is majorly used for milk protein production, has increased due to the Chinese food industry's dependence on imported skim milk powder.

- In countries like India, milk production is highly supported by government authorities implementing specific regulations in different states. To boost milk output in India, the Uttar Pradesh state government is establishing milk conservation centers and greenfield dairies. According to production data from the Food and Agriculture Organization Corporate Statistical Database (FAOSTAT), India is the highest milk producer and ranks first position in the world, contributing 24% of global milk production in the year 2021-22.

Asia-Pacific Milk Protein Industry Overview

The Asia-Pacific Milk Protein Market is moderately consolidated, with the top five companies occupying 49.32%. The major players in this market are Arla Foods amba, Fonterra Co-operative Group Limited, Glanbia PLC, Kerry Group PLC and Koninklijke FrieslandCampina N.V. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Animal

- 3.3 Production Trends

- 3.3.1 Animal

- 3.4 Regulatory Framework

- 3.4.1 Australia

- 3.4.2 China

- 3.4.3 India

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Form

- 4.1.1 Concentrates

- 4.1.2 Isolates

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Dairy and Dairy Alternative Products

- 4.2.2.1.6 RTE/RTC Food Products

- 4.2.2.1.7 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

- 4.3 Country

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 India

- 4.3.4 Indonesia

- 4.3.5 Japan

- 4.3.6 Malaysia

- 4.3.7 New Zealand

- 4.3.8 South Korea

- 4.3.9 Thailand

- 4.3.10 Vietnam

- 4.3.11 Rest of Asia-Pacific

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Arla Foods amba

- 5.4.2 Fonterra Co-operative Group Limited

- 5.4.3 Glanbia PLC

- 5.4.4 Groupe LACTALIS

- 5.4.5 Kerry Group PLC

- 5.4.6 Koninklijke FrieslandCampina N.V.

- 5.4.7 Milligans Food Group Limited

- 5.4.8 Morinaga Milk Industry Co. Ltd

- 5.4.9 Olam International Limited

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms