|

市場調査レポート

商品コード

1683506

乳たんぱく質:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Milk Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 乳たんぱく質:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 389 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

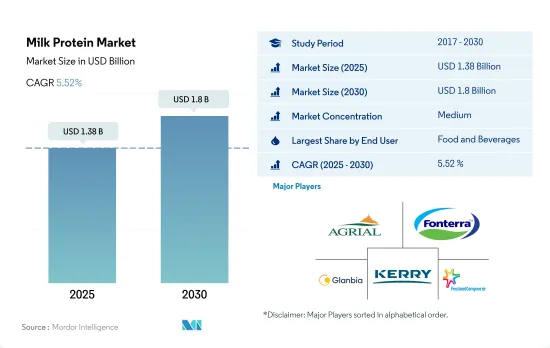

乳たんぱく質の市場規模は2025年に13億8,000万米ドルと推定され、2030年には18億米ドルに達すると予測され、予測期間中(2025-2030年)のCAGRは5.52%で成長する見込みです。

乳たんぱく質需要の85.67%がベーカリー、スナック、飲食品産業であり、飲食品分野が市場をリードしています。

- 用途別では、F&B分野がレビュー期間を通じて市場トップの座を維持しました。数量ベースでは、2022年にF&Bセグメントのミルクたんぱく質需要の85.67%がベーカリー、スナック、飲料産業によって牽引されました。乳たんぱく質は、その高い溶解性と熱安定性により、低酸性飲料で人気を集めています。同様に、乳たんぱく質の卵代替における高い有効性は、ベーカリー業界、特に鳥インフルエンザが懸念されている国々での需要を押し上げました。したがって、F&B分野での乳たんぱく質の使用は、予測期間中に数量ベースでCAGR 4.55%を記録すると予想されます。

- 一方、サプリメント分野も世界的に大きな需要を記録しました。これは、スポーツ・パフォーマンス栄養業界とベビーフード・乳児用調製粉乳業界の需要拡大に牽引されたもので、サプリメント分野ではそれぞれ数量ベースで33%と66%のシェアを占めています。スポーツ・パフォーマンス栄養は、すべてのサプリメント・サブセグメントの中で最も急成長し、予測期間中にCAGR 6.08%を記録すると予測されています。ホエイとカゼインの比率が20:80である乳たんぱく質は、ボディビルダーにとって優れた代替品です。アメリカ人の75%以上が毎年栄養補助食品を摂取しており、女性成人の79%、男性成人の74%が少なくとも1種類のサプリメントを食事と一緒に摂取していると回答しています。

- 2020年6月、FDAは乳たんぱく質濃縮物(MPC)、乳たんぱく質分離物(MPI)、およびいくつかの追加添加物を「高タンパク牛乳」としてブランド化された製品に含めることを許可することを決定しました。

肥満の蔓延やその他の健康問題で人口が増加するアジア太平洋地域は、乳たんぱく質の市場規模が最も大きいです。

- アジア太平洋、特に中国(2022年の地域市場シェア33.8%)は、明確なエンドユーザー層をターゲットとした絶え間ない技術革新に支えられ、乳たんぱく質の主要市場となっています。肥満の増加(人口の約27%、2020年には5億人以上)とフィットネス愛好家が高タンパク食品を選ぶことが、中国を市場リーダーに位置づけています。酪農産業は世界的に絶大な成長を記録しており、乳たんぱく質の生産を牽引しています。これらの蛋白質は、飲食品セグメントのベーカリー・サブセグメント、次いでサプリメント・セグメントで絶大な用途があります。

- 欧州は第2位の市場シェアを占め、トルコとEUの食品法の調和に伴い海外からの投資を引き付けています。その他の地域は莫大な市場開拓の可能性を秘めており、多国籍企業がアフリカ、南米、中東の乳たんぱく質市場に多額の投資を行っています。乳たんぱく質濃縮物を提供する主要ブランドである乳製品原料メーカーのDarigoldは、中東とアフリカの顧客とのサービス統合を改善するため、2019年にドバイに事務所を開設しました。

- 中東地域は、予測期間2023-2029年のCAGRが金額ベースで6.25%と、市場で最も急成長すると予測されています。栄養価に対する意識の高まりから、原料メーカーは中東市場に営業所を開設し、製品を販売しています。2021年には、サウジアラビア全土で約48.2%の人が週に30分以上身体活動やスポーツ活動を実践していました。サウジアラビアにおける2022年のサプリメント分野のたんぱく質消費量は8,234.4トンでした。

世界の乳たんぱく質市場動向

健康意識の高まりとミレニアル世代からの需要増が市場を牽引

- 健康意識の高まりとミレニアル世代からの需要の急増がスポーツ栄養セグメントを牽引しています。この分野では、筋肉の維持や成長といった利点を理由に、消費者がたんぱく質を強化した飲料や栄養補助食品を求める傾向が強まっています。例えば、2023年のCRN Consumer Survey on Dietary Supplements(栄養補助食品に関する消費者調査)によると、米国の成人の74%が栄養補助食品を摂取しており、そのうち55%が「常用者」であることが明らかになっています。

- スポーツドリンクは従来、激しい運動中の電解質補給を目的として販売されてきたが、炭水化物や塩分の増加、運動中のパフォーマンス向上といったメリットを強調するように進化してきました。この進化は、アクティブで健康的なライフスタイルへのシフトと一致しています。スポーツ栄養分野では、中高年層のスポーツ参加率の高まりが追い風となっています。例えば、2022年には、アジアの6~12歳の青少年の定期的なスポーツ参加率は、2019年の35%から42%に急増しました。

- 北米は、スポーツ動向の高まり、健康への関心、食生活に牽引され、スポーツ栄養セグメントの最前線に立っています。同市場は、健康上の利点を誇る風味革新の継続的動向から恩恵を受けると予想されます。一方、欧州は重要なプレーヤーとして台頭しており、英国、ドイツ、スペイン、フランスなどの主要市場が市場の主要シェアを占めています。2022年の統計によると、欧州連合(EU)の成人の38%が週に1回以上スポーツや運動を行っており、6%が週に5回行っています。

牛乳は主要な動物性たんぱく質源として貢献し続ける

- 牛乳は小規模農家にとって重要な収入源であり、比較的短期間で収益を上げることができます。この開発の大部分は、一頭当たりの生産量の増加よりも、乳生産動物の増加と収量の目に見える拡大によるものです。世界の生乳生産量は、1988年の5億3,000万トンから2018年には8億4,300万トンと、過去30年間で59%以上増加し、2022年の世界生乳生産量は2021年比1.0%増の9億3,700万トンに達すると予測されています。国連食糧農業機関法人統計データベース(FAOSTAT)の生産データによると、インドは世界で最も生乳生産量の多い国です。インドは2021年から2022年にかけて世界の生乳生産量の24%に貢献しました。

- インドとパキスタンの生乳集荷の効率化と中国の急成長する大規模農場に牽引されるアジアは、世界の生乳生産の要となる態勢を整えています。北米、中南米、カリブ海諸国では2022年の生乳生産量は、主に収量の増加に牽引されて緩やかな伸びを示したが、欧州、南米、オセアニアでは生産量の減少予測に直面しました。この減少は、乳牛の頭数の減少、熟練労働者の不足の深刻化、牧草の質の低下によるものです。

- フランスでは2021年1月のEUにおける生乳供給量が顕著に落ち込み、2020年の同月から3%以上減少し、20億リットル強に落ち着いた。これは2020年1月と比較して7,000万リットル以上生産量が減少したことになります。この減少は主に2021年初頭の厳しい天候に加え、飼料価格の高騰と標準以下のサイレージ品質に起因します。

乳たんぱく質業界の概要

乳たんぱく質市場は適度に統合されており、上位5社で41.38%を占めています。この市場の主要企業は以下の通り。 Agrial Enterprise, Fonterra Co-operative Group Limited, Glanbia PLC, Kerry Group PLC and Royal FrieslandCampina NV(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- エンドユーザー市場規模

- ベビーフードおよび乳児用調製乳

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品および乳製品代替製品

- 高齢者栄養・医療栄養

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- スポーツ/パフォーマンス栄養

- 動物飼料

- パーソナルケアと化粧品

- たんぱく質消費動向

- 動物

- 生産動向

- 動物

- 規制の枠組み

- オーストラリア

- カナダ

- 中国

- フランス

- ドイツ

- インド

- イタリア

- 英国

- 米国

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- 形態

- 濃縮物

- 加水分解物

- 分離物

- エンドユーザー

- 動物飼料

- 飲食品

- サブエンドユーザー別

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 乳製品及び乳製品代替製品

- RTE/RTC食品

- スナック

- パーソナルケアと化粧品

- サプリメント

- サブエンドユーザー別

- ベビーフードおよび乳児用調製粉乳

- 高齢者栄養と医療栄養

- スポーツ/パフォーマンス栄養

- 地域別

- アフリカ

- 形態別

- エンドユーザー別

- 国別

- ナイジェリア

- 南アフリカ

- その他のアフリカ

- アジア太平洋

- 形態別

- エンドユーザー別

- 国別

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- ニュージーランド

- 韓国

- タイ

- ベトナム

- その他アジア太平洋地域

- 欧州

- 形態別

- エンドユーザー別

- 国別

- ベルギー

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- トルコ

- 英国

- その他欧州

- 中東

- 形態別

- エンドユーザー別

- 国別

- イラン

- サウジアラビア

- アラブ首長国連邦

- その他中東

- 北米

- 形態別

- エンドユーザー別

- 国別

- カナダ

- メキシコ

- 米国

- その他北米

- 南米

- 形態別

- エンドユーザー別

- 国別

- アルゼンチン

- ブラジル

- その他南米地域

- アフリカ

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- Agrial Enterprise

- Fonterra Co-operative Group Limited

- Glanbia PLC

- Groupe LACTALIS

- Kerry Group PLC

- Morinaga Milk Industry Co., Ltd.

- Olam International Limited

- Royal FrieslandCampina NV

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Milk Protein Market size is estimated at 1.38 billion USD in 2025, and is expected to reach 1.8 billion USD by 2030, growing at a CAGR of 5.52% during the forecast period (2025-2030).

With 85.67% of milk protein demand in the bakery, snacks, and beverage industries, food and beverages segment has led the market

- By application, the F&B sector retained the top position in the market throughout the review period. By volume, 85.67% of milk protein demand in the F&B segment was driven by the bakery, snacks, and beverage industries in 2022. Milk proteins are gaining popularity in low-acid beverages due to their greater solubility and heat stability. Similarly, milk proteins' high efficacy in egg replacement boosted its demand in the bakery industry, especially in countries where avian flu is a budding concern. Hence, the use of milk proteins in the F&B segment is anticipated to register a CAGR of 4.55%, by volume, during the forecast period.

- On the other hand, the supplements sector also recorded a significant global demand. This was led by the growing demand for the sport and performance nutrition and baby food and infant formula industries, which accounted for shares of 33% and 66%, by volume, respectively, in the supplements segment. Sports and performance nutrition is projected to be the fastest-growing among all supplements sub-segments, recording a CAGR of 6.08% during the forecast period. Milk protein is an excellent alternative for bodybuilders due to its ability to offer a whey-to-casein ratio of 20:80. More than 75% of Americans take dietary supplements every year; with 79% of female adults and 74% of male adults claiming to consume at least one form of supplements with their diet.

- In June 2020, the FDA decided to allow the inclusion of milk protein concentrate (MPC), milk protein isolate (MPI), and a few additional additives in products branded as "high protein milk," which is further expected to propel the market segment during the forecast period.

Increasing population with rising prevalence of obesity and other health concerns, Asia-Pacific witnessed the highest market for milk protein

- Asia-Pacific, particularly China (with a 33.8% share in the regional market in 2022), is the leading market for milk protein, aided by constant innovations targeting distinct end-user segments. Increases in the prevalence of obesity (roughly 27% of the population, more than half a billion people in 2020) and fitness enthusiasts choosing high-protein foods have positioned China as the market leader. The dairy industry has recorded immense growth globally, driving milk protein production. These proteins have immense applications in the bakery sub-segment in the food and beverages segment, followed by the supplements segment.

- Europe holds the second-largest market share and has been attracting foreign investments in line with harmonization achieved by Turkish and EU Food Laws. Other regions hold enormous development potential, prompting multinational businesses to spend heavily in the milk protein market in Africa, South America, and the Middle East. Dairy ingredient maker Darigold, a major brand that offers milk protein concentrates, opened an office in Dubai in 2019 for improved service integration with customers in the Middle East and Africa.

- The Middle East region is projected to be the fastest-growing in the market, with a CAGR of 6.25% by value during the forecast period 2023-2029. Due to the growing awareness of its nutritional value, raw material manufacturers are opening sales offices and selling products in the Middle Eastern market. In 2021, around 48.2% of people across Saudi Arabia practiced physical and sporting activities at least 30 minutes a week. The protein consumption in the supplements segment accounted for a volume of 8,234.4 ton in 2022 in Saudi Arabia.

Global Milk Protein Market Trends

Rising health awareness and growing demand from millennials are driving the market

- Rising health awareness and a surge in demand from millennials are driving the sports nutrition segment. The segment is witnessing an upswing, with consumers increasingly seeking protein-enriched beverages and dietary supplements, citing benefits like muscle maintenance and growth. For instance, the 2023 CRN Consumer Survey on Dietary Supplements reveals that 74% of US adults consume dietary supplements, with 55% identified as "regular users".

- Sports drinks, traditionally marketed for their electrolyte-replenishing properties during intense physical activities, have evolved to emphasize benefits such as increased carbohydrates, salts, and enhanced performance during workouts. This evolution aligns with the shift toward active and healthier lifestyles. The sports nutrition segment has seen a boost from growing participation in sports among middle-aged and elderly populations. For example, in 2022, the rate of regular sports participation among Asian youth aged 6 to 12 years surged to 42%, up from 35% in 2019.

- North America stands at the forefront of the sports nutrition segment, driven by a rising athletic trend, health concerns, and dietary habits. The market is expected to benefit from the ongoing trend of flavor innovations that boast health advantages. Meanwhile, Europe is emerging as a significant player, with key markets like the United Kingdom, Germany, Spain, and France commanding a major share of the market. In 2022, statistics revealed that 38% of adults in the European Union engaged in sports or exercise at least once a week, with 6% committing to it five times weekly.

Milk continues to contribute as a major animal protein source

- Milk is a key source of financial revenue for small-scale farmers and offers relatively quick returns. This development is mostly due to an increase in the number of milk-producing animals and a tangible expansion in yield figures rather than an increase in production per head. Global milk production increased by more than 59% in the previous three decades, from 530 million tons in 1988 to 843 million tons in 2018, and global milk production in 2022 was projected to reach 937 million tons, up 1.0% from 2021. According to production data from the Food and Agriculture Organization Corporate Statistical Database (FAOSTAT), India is the highest milk producer in the world. India contributed 24% of global milk production from 2021 to 2022.

- Asia, led by India and Pakistan's efficiency in milk collection and China's burgeoning large-scale farms, is poised to be the linchpin of global milk production. While North America, Central America, and the Caribbean saw moderate growth in milk output in 2022, largely driven by enhanced yields, Europe, South America, and Oceania faced projections of declining production. This decline is attributed to diminishing dairy cattle numbers, a rising shortage of skilled labor, and subpar pasture quality.

- France experienced a notable dip in milk supply in the European Union in January 2021, down over 3% from the same month in 2020, settling at just over 2 billion liters. This translated to a production drop of more than 70 million liters compared to January 2020. The decline was primarily linked to harsh early 2021 weather, alongside elevated feed prices and substandard silage quality.

Milk Protein Industry Overview

The Milk Protein Market is moderately consolidated, with the top five companies occupying 41.38%. The major players in this market are Agrial Enterprise, Fonterra Co-operative Group Limited, Glanbia PLC, Kerry Group PLC and Royal FrieslandCampina NV (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Animal

- 3.3 Production Trends

- 3.3.1 Animal

- 3.4 Regulatory Framework

- 3.4.1 Australia

- 3.4.2 Canada

- 3.4.3 China

- 3.4.4 France

- 3.4.5 Germany

- 3.4.6 India

- 3.4.7 Italy

- 3.4.8 United Kingdom

- 3.4.9 United States

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Form

- 4.1.1 Concentrates

- 4.1.2 Hydrolyzed

- 4.1.3 Isolates

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Dairy and Dairy Alternative Products

- 4.2.2.1.6 RTE/RTC Food Products

- 4.2.2.1.7 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

- 4.3 Region

- 4.3.1 Africa

- 4.3.1.1 By Form

- 4.3.1.2 By End User

- 4.3.1.3 By Country

- 4.3.1.3.1 Nigeria

- 4.3.1.3.2 South Africa

- 4.3.1.3.3 Rest of Africa

- 4.3.2 Asia-Pacific

- 4.3.2.1 By Form

- 4.3.2.2 By End User

- 4.3.2.3 By Country

- 4.3.2.3.1 Australia

- 4.3.2.3.2 China

- 4.3.2.3.3 India

- 4.3.2.3.4 Indonesia

- 4.3.2.3.5 Japan

- 4.3.2.3.6 Malaysia

- 4.3.2.3.7 New Zealand

- 4.3.2.3.8 South Korea

- 4.3.2.3.9 Thailand

- 4.3.2.3.10 Vietnam

- 4.3.2.3.11 Rest of Asia-Pacific

- 4.3.3 Europe

- 4.3.3.1 By Form

- 4.3.3.2 By End User

- 4.3.3.3 By Country

- 4.3.3.3.1 Belgium

- 4.3.3.3.2 France

- 4.3.3.3.3 Germany

- 4.3.3.3.4 Italy

- 4.3.3.3.5 Netherlands

- 4.3.3.3.6 Russia

- 4.3.3.3.7 Spain

- 4.3.3.3.8 Turkey

- 4.3.3.3.9 United Kingdom

- 4.3.3.3.10 Rest of Europe

- 4.3.4 Middle East

- 4.3.4.1 By Form

- 4.3.4.2 By End User

- 4.3.4.3 By Country

- 4.3.4.3.1 Iran

- 4.3.4.3.2 Saudi Arabia

- 4.3.4.3.3 United Arab Emirates

- 4.3.4.3.4 Rest of Middle East

- 4.3.5 North America

- 4.3.5.1 By Form

- 4.3.5.2 By End User

- 4.3.5.3 By Country

- 4.3.5.3.1 Canada

- 4.3.5.3.2 Mexico

- 4.3.5.3.3 United States

- 4.3.5.3.4 Rest of North America

- 4.3.6 South America

- 4.3.6.1 By Form

- 4.3.6.2 By End User

- 4.3.6.3 By Country

- 4.3.6.3.1 Argentina

- 4.3.6.3.2 Brazil

- 4.3.6.3.3 Rest of South America

- 4.3.1 Africa

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Agrial Enterprise

- 5.4.2 Fonterra Co-operative Group Limited

- 5.4.3 Glanbia PLC

- 5.4.4 Groupe LACTALIS

- 5.4.5 Kerry Group PLC

- 5.4.6 Morinaga Milk Industry Co., Ltd.

- 5.4.7 Olam International Limited

- 5.4.8 Royal FrieslandCampina NV

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms