|

市場調査レポート

商品コード

1911285

中東・北アフリカ地域のフィンテック市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)MENA Fintech - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東・北アフリカ地域のフィンテック市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

概要

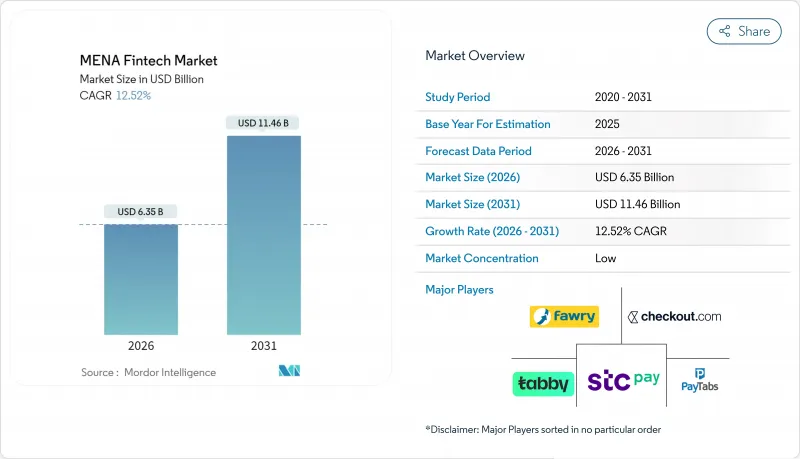

中東・北アフリカのフィンテック市場規模は、2026年に63億5,000万米ドルに達すると予測されています。

これは2025年の56億5,000万米ドルから成長した数値であり、2031年には114億6,000万米ドルに達すると見込まれています。2026~2031年にかけての年間平均成長率(CAGR)は12.52%と予測されています。

キャッシュレス施策の義務化拡大、スマートフォンの普及拡大、ベンチャーキャピタル流入の増加が、デジタル金融サービスの対象顧客基盤を拡大しています。GCCやエジプトにおける中央銀行デジタル通貨(CBDC)の検査運用は決済インフラを近代化させ、サウジアラビア、アラブ首長国連邦、ヨルダンにおける規制サンドボックスは製品投入サイクルを短縮しています。同時に、電子商取引、ギグエコノミー、送金ルートが組み込み金融の使用事例を促進しています。産業関係者は、新たな収益源を創出し、分散したポジションを統合するプラットフォームの多様化と越境パートナーシップを通じて対応しています。

中東・北アフリカのフィンテック市場動向と洞察

政府のキャッシュレス化・金融包摂施策がフィンテック需要を加速

サウジアラビアは2030年までに取引の70%をキャッシュレス化、エジプトは2025年までに成人の50%を銀行口座保有化、アラブ首長国連邦は2024年にライセンシング制度を簡素化することを目標としています。これらの目標は導入の明確な指標を提供し、民間事業者の市場参入障壁を低減します。ヨルダンのサンドボックスは規制リスクをさらに軽減し、スタートアップが法規制対応コストを抑えつつ事業拡大を支援します。政府が給与決済や福祉給付のデジタル化を進める中、消費者の電子財布への親和性が高まり、顧客獲得コストが低下しています。施策推進は小売業者に非接触決済の導入を促し、決済ネットワークを拡大。これらの施策が相まって好循環を生み出し、中東・北アフリカのフィンテック市場を拡大させています。

モバイルインターネット普及率の急伸がモバイルファースト金融アクセスを実現

GCCではスマートフォン普及率が80%を超え、モバイルが銀行取引のデフォルトチャネルとなりました。アラブ首長国連邦では既にデジタルウォレットがPOS支出の18%を占め、2027年までに33%に達する見込みです。エジプトとモロッコでは通信事業者ベース代理店モデルにより、支店インフラを迂回して事業コストを削減しつつサービス範囲を拡大しています。Z世代ユーザーはデジタルウォレット経由の地域eコマース支出の23%を占め、持続的な決済習慣を確立しています。北アフリカ地方における4G/5Gのカバー率拡大により、遠隔での本人確認(KYC)手続きが可能となり、新たな顧客層の開発が進んでいます。このようにモバイルファーストモデルは、あらゆる消費者層において急速なシェア拡大を推進しています。

管轄区域ごとの規制のセグメント化がコンプライアンス負担を増大

19の異なるライセンシング制度により、フィンテック企業は市場ごとに別法人を設立する必要があり、統一された枠組みと比較して間接費が15~25%増加します。資本規制やデータ現地化のルールがばらつき、パスポート制度の適用を妨げ、地域規模での事業拡大を遅らせています。大手既存企業はコストを吸収できますが、スタートアップはリソース不足に直面し、イノベーションの多様性が制限されます。相互承認の欠如は越境オープンAPI連携も阻害し、統合のデッドゾーンを生み出します。投資家はリスクを評価額に織り込み、複数国展開の回避策として統合を促しています。

セグメント分析

デジタル決済は2025年時点で中東・北アフリカ地域のフィンテック市場の54.12%を占め、ほぼ普遍的なスマートフォンウォレットと積極的な加盟店獲得インセンティブが基盤となっています。このサブセグメントではQRコード決済やトークン化ウォレット決済といった新たな決済チャネルが追加され、顧客定着率がさらに強化されました。デジタル融資は規模こそ小さいも、リアルタイムの代替データスコアリングの強みを背景に17.74%のCAGRで成長しています。ファウリー社が2025年に達成した10億EGPの融資急増は、決済から信用供与への隣接領域進出を示しています。

ロボアドバイザーとインシュアテックはAPIファーストの流通で拡大し、STC Bankのようなネオバンクはウォレット基盤をフルサービス口座へ転換しています。規制サンドボックスはパラメトリック保険や使用量ベース保険を可能にし、実験を促進しています。決済ブランドが同一アプリ内にクレジット、投資、保険タブを追加することでクロスセルの相乗効果が生まれ、ユーザーの生涯価値が拡大しています。この多様化の推進は、中東・北アフリカ地域のフィンテック市場全体でプラットフォームの収束が加速していることを示しています。

その他の特典

- エクセル形態の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 政府によるキャッシュレス化と金融包摂の義務付け

- モバイルインターネット普及率の急増

- ベンチャーキャピタル資金調達と規制サンドボックスの進展

- CBDCパイロットによる越境決済基盤の実現

- 電子商取引とギグプラットフォームからの組み込み金融需要

- 即時決済インフラが代替融資データの活用を可能にします

- 市場抑制要因

- 管轄区域間の規制の分断

- 現金中心の習慣が北アフリカにおける顧客獲得コスト(CAC)を押し上げている

- アラビア語対応のAI/MLリスクスコアリングデータセットの不足

- レガシーな中核銀行ITシステムのボトルネック

- バリュー/サプライチェーン分析

- 規制情勢

- 技術の展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- サービス提案別

- デジタル決済

- デジタル融資・資金調達

- デジタル投資

- インシュアテック

- ネオバンキング

- エンドユーザー別

- 小売

- 企業

- ユーザーインターフェース別

- モバイルアプリケーション

- ウェブ/ブラウザ

- POS/IoTデバイス

- 地域別

- GCC

- サウジアラビア

- アラブ首長国連邦

- カタール

- バーレーン

- クウェート

- オマーン

- 北アフリカ

- エジプト

- モロッコ

- アルジェリア

- チュニジア

- レバント地域

- ヨルダン

- レバノン

- GCC

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Fawry

- PayTabs

- Checkout.com

- Tabby

- Tamara

- STC Pay

- Paymob

- MNT-Halan

- Geidea

- Network International

- BenefitPay

- Careem Pay

- Lean Technologies

- HyperPay

- YAP

- Telda

- NymCard

- Sarwa

- OPay