大豆ベース食品:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Soy-based Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690874

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

大豆ベース食品の市場規模は2025年に301億5,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは6.45%で、2030年には412億1,000万米ドルに達すると予測されます。

消費者の間で従来の動物性食品・飲料製品の消費に対する懸念が高まっていることや、健康意識の高まりによるCOVID-19の大流行をきっかけにビーガン食が採用されたことが、大豆ベースの飲食品市場の成長にプラスの影響を与えました。COVID-19の流行は、多くの民間企業が市場に参入し、急増する需要に対応する機会を生み出すことにもなりました。また、大豆ベースのパッケージ入り食肉製品は安全だと考えられているため、その需要は常に高いです。植物性食品協会によると、コロナウイルスが発生した際、植物性食肉の小売売上は昨年より148%増加しました。4月以降の数週間も、植物性食肉の売上は61%の伸びを示し、これは同時期の動物性食肉の約2倍でした。

中期的には、大豆ベース食品の出現は、動物性食品から植物性食品への顧客需要のシフトを明確に示しており、大豆ベース食品が突出したシェアを占めています。このような植物ベースの食事への漸進的なシフトは、主に生態系への懸念、健康意識、倫理的または宗教的信条、環境問題や動物の権利に関する意識に影響されています。動物性タンパク質は必要なアミノ酸含有量を提供するもの、高コレステロール値やその他の関連問題と関連しています。そのため、先進諸国の消費者は、ビーガンベースのタンパク源を好むようになってきています。

さらに、植物性食生活への嗜好の高まりと、大手食肉加工業者や食肉メーカーが代替肉製品ラインアップを揃えてこの競合に参入する意向を表明していることが、植物性食品・飲食品の消費に大きなチャンスをもたらしています。健康志向と持続可能性志向の高まりは、菜食主義/柔軟主義への移行を促進し、消費者の間で大豆ベース食品への支持が高まっています。

大豆ベース食品の市場動向

乳糖不耐症人口の増加

アレルギーや不耐症は乳製品を摂らないようにする主な理由であり、特に牛乳アレルギーが乳幼児と小児における主要な食物アレルギーであるという食物アレルギー・イニシアチブの統計を考慮するとそうです。大豆ベースの代替乳製品は当然乳糖を含まず、一般的に動物性ミルクよりもコレステロールや脂肪分が低いと考えられています。さらに、タンパク質、ミネラル、ビタミンの含有量も同程度です。さらに、カッテージチーズ(4.62g/125ml)、クリームチーズ(1.60g/50g)、ヨーグルト(3.25g/125ml)などに含まれる相対的な乳糖含有量は、ラクターゼ欠乏症の人々の間で栄養素の吸収不良を引き起こし、革新的な大豆ベースの無乳糖ポートフォリオに道を開き、市場の需要を牽引しています。さらに、この市場は主に都市部で人気を集めており、人々は必須多量栄養素やアミノ酸、良質な脂肪酸プロファイル、重要なミネラル、ビタミン、複合炭水化物、多くの植物化学物質を含むプレミアム製品に消費しています。大豆の優れた栄養価に加え、科学者たちは、大豆関連製品の摂取が心臓病のリスク軽減に貢献することを発見しました。それゆえ、人口のかなりの割合が大豆ベースの飲食品にシフトしています。この動向を受け、メーカー各社は製品に微量栄養素を計画的に強化しており、これが市場を後押ししています。

アジア太平洋地域が最大のシェアを占める

アジア太平洋地域は、特に10代の若者やミレニアル世代が主導する菜食主義の拡大傾向を目の当たりにしています。アジアの消費者は現在、植物由来の肉製品という考え方に寛容で、健康的なライフスタイルに貢献しています。コロナウイルスやアフリカ豚熱のような疾病の発生に危機感を募らせる新世代の消費者の間で、植物性代替肉は徐々に地位を確立しつつあります。加えて、食品会社は、植物性食肉に対する消費者の需要に応え、消費者基盤を拡大するために、人工食肉を拡大するために提携しています。例えば、食肉総合企業のスターゼンは2021年5月、健康食品・飲料メーカーの大塚製薬と共同で「ZEROMEAT(ゼロミート)」というブランドを開発し、大豆タンパク質と卵白を原料とした植物性ソーセージ、ミートボール、ハンバーグパティを販売しています。食品メーカーに加え、小売・外食チェーンもこの大豆ミートの動向を牽引しています。2020年には、ローソン、セブンイレブン、ファミリーマートなど、ほぼすべてのコンビニエンスストア・チェーンや、いくつかの外食・カフェ・チェーンが大豆ベースの商品を発売しました。

大豆ベース食品産業の概要

世界の大豆ベース食品市場は非常に競争の激しい市場であり、地域的・地元的プレーヤーと国際的プレーヤーで構成されています。市場を独占しているのは、Kellogg, Gardein, Unilever, Conagra, Impossible foodsなどの企業です。これらのプレーヤーは、製品革新、合併、買収、パートナーシップ、生産と地理的拡大などの戦略にふけることで、順番に、市場で尊敬される地位を得るために活用されています。消費者の嗜好や好みの変化に伴い、市場の様々な主要企業による製品面でかなりの開発が行われています。製品レンジを革新するために、大手企業は製品レンジを強化しています。さらに、企業は市場での地位を維持し、さまざまな大豆ベース食品を提供するために、研究開発(R&D)やマーケティングへの投資を増やし、流通チャネルを拡大しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 製品タイプ別

- 肉の代替品

- テクスチャードベジタブルたんぱく質

- 豆腐

- テンペ

- 非乳製品アイスクリーム

- 非乳製品チーズ

- 乳製品不使用ヨーグルト

- 非乳製品スプレッド

- 肉の代替品

- 流通チャネル別

- ハイパーマーケット/スーパーマーケット

- コンビニエンスストア

- オンライン小売店

- その他の流通チャネル

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- 日本

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- その他中東とアフリカ

- 北米

第6章 競合情勢

- 最も活発な企業

- 最も採用されている戦略

- 市場ポジショニング分析

- 企業プロファイル

- Danone SA

- Good Catch Foods

- Monde Nissin Corporation

- Nestle SA

- Conagra Brands Inc

- Impossible Foods Inc

- Vitasoy International Holdings Ltd

- Hain Celestial Group

- Unilever PLC

- The Amy's Kitchen

第7章 市場機会と今後の動向

第8章 COVID-19が業界に与える影響

目次

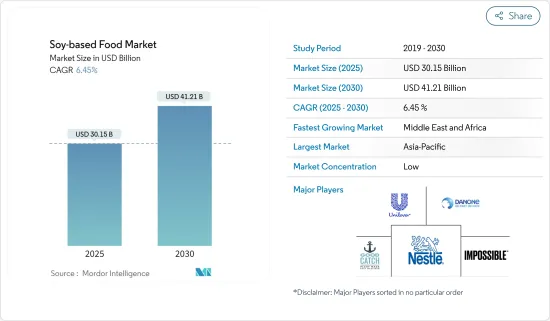

The Soy-based Food Market size is estimated at USD 30.15 billion in 2025, and is expected to reach USD 41.21 billion by 2030, at a CAGR of 6.45% during the forecast period (2025-2030).

The growing concerns among consumers about the consumption of conventional animal-based food and beverage products and the adoption of vegan diets in the wake of the COVID-19 outbreak due to rising health awareness positively impacted the soy-based growth of the food market. The COVID-19 pandemic has also resulted in the generation of opportunities for many private players to emerge in the market and cater to the inflated demand. Also, the demand for packaged soy-based meat products is consistently high because they are considered safe. According to the Plant-based Foods Association, during the coronavirus outbreak, plant-based meat retail sales increased by 148% more than last year. During the weeks following April, plant-based meat sales continued to grow at a rate of 61%, which was almost twice as high as animal-based meats during the same period.

Over the medium term, the emergence of soy-based food products clearly demonstrates a shift in customer demand from animal-based products to plant-based products, with soy-based foods holding a prominent share. This incremental shift toward a plant-based diet is primarily influenced by ecological concerns, health consciousness, ethical or religious beliefs, and awareness about environmental issues and animal rights.Though animal-based proteins provide the necessary amino acid content, they are associated with high cholesterol levels and other related issues. Thus, consumers in developed countries are increasingly preferring vegan-based protein sources.

Furthermore, the growing preference for plant-based diets and the major meat processors and manufacturers announcing their intentions to join this competition with their line of meat alternatives together present a massive opportunity for plant-based food and beverage consumption. Growing health and sustainability trends are fostering the shift toward vegan/flexitarian diet, which is increasingly favoring soy-based food among consumers, thereby driving the market studied.

Soy Based Foods Market Trends

Rising Prevalence of Lactose Intolerant Population

Allergies and intolerances are the major reasons for going dairy-free, especially considering the food allergy initiative's statistic stating that cow milk allergy is the leading food allergy in infants and children. Soy-based dairy alternatives are naturally lactose-free, and they are generally considered to be lower in cholesterol and fat than milk from animals. Moreover, they usually offer a similar protein, mineral, and vitamin content. Further, a relative amount of lactose content in cottage cheese (4.62g/125ml), cream cheese (1.60g/50g), and yogurt (3.25g/125 ml), among others, results in the malabsorption of nutrients among the lactase-deficient demographics, paying the way for innovative soy-based, lactose-free portfolios, driving the market demand. Additionally, the market studied is gaining popularity, mainly in urban areas, where people are spending on premium products that have essential macronutrients and amino acids, good quality fatty acid profiles, vital minerals, vitamins, complex carbohydrates, and many phytochemicals. In addition to the excellent nutritional value of soy, scientists have found that consumption of soy-associated products can contribute to reducing the risk of heart disease. Hence, a considerable percentage of the population is shifting toward soy-based food and beverages. Taking up the trend, the manufacturers are systematically fortifying micronutrients into the products, which is booting the market.

Asia-Pacific Accounting for the Largest Share

Asia-Pacific region is witnessing a growing trend of veganism led by young people, especially teens and millennials, who seem to be more invested in defending and spreading awareness about this trend. Asian consumers are now more open to the idea of plant-based meat products, contributing to a healthy lifestyle. Plant-based meat substitutes are slowly carving out a place for themselves among a new generation of consumers increasingly alarmed by outbreaks of diseases, such as Coronavirus and African swine fever. In addition, food companies are partnering to expand artificial meat to cater to consumer demand for plant-based meat and broaden their consumer bases. For instance, in May 2021, Starzen, a meat integrated company, together with health food and drink manufacturer Otsuka, developed a brand called 'ZEROMEAT' and is selling plant-based sausages, meatballs, and hamburg steak patties made from soy protein and egg whites. In addition to the food manufacturers, the retail and foodservice chains are also the main drivers of this soy-meat trend. In 2020, almost all convenience store chains, including Lawson, Seven Eleven, Family Mart, as well as several food services and cafe chains, released soy-based products

Soy Based Foods Industry Overview

The global soy-based food market is a highly competitive market and comprises regional/local and international players. The market is dominated by players like Kellogg, Gardein, Unilever, Conagra, and Impossible foods, among others. These players are indulging in strategies like product innovation, mergers, acquisitions, partnerships, and production and geographical expansions, which, in turn, has leveraged them to gain an esteemed position in the market. , There have been considerable developments in terms of products by various key players in the market owing to the changing tastes and preferences of consumers. In order to innovate product ranges, leading players are enhancing the product range. Furthermore, companies are also increasing their investments in research and development (R&D) and marketing and expanding their distribution channels to maintain their positions in the market and offer different soy-based food.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Product Type

- 5.1.1 Meat Substitutes

- 5.1.1.1 Textured Vegetable Protein

- 5.1.1.2 Tofu

- 5.1.1.3 Tempeh

- 5.1.2 Non-Dairy Ice Cream

- 5.1.3 Non-Dairy Cheese

- 5.1.4 Non-Dairy Yogurt

- 5.1.5 Non-Dairy Spread

- 5.1.1 Meat Substitutes

- 5.2 By Distribution Channel

- 5.2.1 Hypermarkets/Supermarkets

- 5.2.2 Convenience Stores

- 5.2.3 Online Retail Stores

- 5.2.4 Other Distribution Channel

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Active Companies

- 6.2 Most Adopted Strategies

- 6.3 Market Positioning Analysis

- 6.4 Company Profile

- 6.4.1 Danone SA

- 6.4.2 Good Catch Foods

- 6.4.3 Monde Nissin Corporation

- 6.4.4 Nestle SA

- 6.4.5 Conagra Brands Inc

- 6.4.6 Impossible Foods Inc

- 6.4.7 Vitasoy International Holdings Ltd

- 6.4.8 Hain Celestial Group

- 6.4.9 Unilever PLC

- 6.4.10 The Amy's Kitchen

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

8 IMPACT OF COVID-19 ON THE INDUSTRY

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日