|

市場調査レポート

商品コード

1690870

中東のゲーム:市場シェア分析、産業動向、成長予測(2025~2030年)Middle East Gaming - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東のゲーム:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

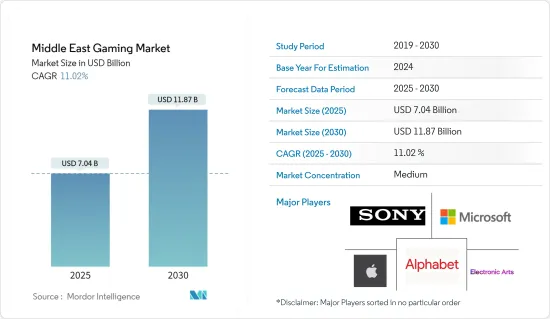

中東のゲーム市場規模は2025年に70億4,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは11.02%で、2030年には118億7,000万米ドルに達すると予測されます。

最近のCOVID-19の流行により、オンラインゲームサービスの利用が増加しているため、同地域のゲーム市場は大きな成長が見込まれます。市場のさまざまなゲームベンダーは、この期間中にユーザーベースを増やし、COVID-19シナリオ後のリターンを急増させることに注力すると予想され、そのためベンダーは特典やオファーを提供したり、サービスの利用料を免除したりしています。

アラブ首長国連邦ではゲーム産業が盛んで、地元で開発された人材やゲームへの関心や投資が高まっています。消費に関しては、非常に多様な地域です。同国の平均的なゲーマーの年間消費額は115米ドルと予想されています。

さらに、スマートフォンとオンラインゲームの普及が進んでいることも、市場の成長を促す重要な要因となっています。ARベースのアプリやゲームの開発が進んでいることから、予測期間中に市場機会が創出されると期待されています。

また、サウジアラビア政府は、テーマパークやアミューズメントスペースに数十億米ドルの巨額投資を行っています。そのため、サウジアラビアのエンターテインメント産業の利害関係者として、産業関係者は専用のカンファレンスに参加し、知識と豊富な経験を得て、革新的な最高の技術を実際に体験することができます。

サウジアラビアは、1,000万米ドルの賞金でCOVID-19の発生と闘う資金を集めるために、新しいチャリティeスポーツイベントを立ち上げました。競合は、COVID-19の流行によって人々が家に閉じこもり、ビジネスを停止し、旅行を最小限に制限する中で行われました。これは、COVID-19に対応するため、世界のゲームコミュニティを団結させ、結びつける可能性があります。中東の人口の約70%は30歳以下で、約2,000万人のゲーマーまたはゲーム愛好家がおり、予測期間中に市場は成長すると予想されます。

中東のゲーム市場動向

スマートフォンセグメントが大きな市場シェアを占める見込み

- 中東地域では近年、モバイルゲームがコンソールゲームやPCゲームを抜き、最も人気のあるゲーム形態となっています。モバイルゲームが成長した要因の1つとして、ほとんどの人がゲームをインストールしたスマートフォンを持っていることが挙げられます。さらに、AR、VR、クラウドゲーム、5Gなど、さまざまな技術の進歩や改善により、モバイルゲームの需要が増加しています。モバイルゲーム産業は主に新技術に依存しています。

- ARは、その没入的でインタラクティブな技術により、モバイルゲームに最適になりつつあります。さらに、モバイルゲームはアプリストアで最も有名なARカテゴリーです。ポケモンGOやイングレスなど、以前リリースされたARモバイルゲームは別として、今でも有名です。

- アラブ首長国連邦とその若年層は、石油に依存する同地域の経済を多角化し、ソフトウェア力を高めるため、近年、スポーツや技術などさまざまなセグメントに飛び込んでいます。

- 例えば、アブダビのMedia and Entertainment Free Zone Authority、twofour54、その他のメディアの報告によると、ゲームへの支出は2019年に約3億2,670万米ドルに達しました。2022年には約44億米ドルに達すると予測されています。

- 中東のゲーム市場を牽引する上で、スマートフォン契約数の増加が重要な役割を果たしています。スマートフォンの契約数が増えれば、モバイルゲームの潜在的なユーザー数も増えます。スマートフォンは従来のゲーム機やPCよりも身近で手頃なため、中東の多くの人々にとって主要なゲームプラットフォームとなっています。このような幅広い利用者層がモバイルゲームの需要を喚起し、市場成長の原動力となっています。Ericssonによると、2022年のGCC諸国のスマートフォン契約数は6,500万台で、今後5年間で7,300万台に増加すると予想されています。

サウジアラビアが大きな市場シェアを占める見込み

- サウジアラビアは「ビジョン2030」を掲げて石油依存からの脱却を図っており、デジタル化に大きく注力しています。サウジアラビアのVRゲームスペースは、国内のさまざまなモール内で形を整えつつあり、VRゲーム産業の最高峰を収容しようとしています。VRのコンセプトは、新たな破壊的技術の助けを借りて、モールの事業価値を高めることにもつながっています。

- さらに、VRの認知度は、国内のあらゆる年齢層のゲーマーの間で着実に高まっています。魅力的なVRヘッドセットの導入後、ゲーム産業ではダイナミックな変化が起きています。

- 社会開発銀行(SDB)によると、サウジアラビアのビデオゲーム市場は約10億米ドルと推定され、同国は2030年までに市場規模を25億米ドルまで押し上げることを目指しています。

- サウジアラビアの通信事業者はまた、ゲーマーに最高の体験を提供し、市場の透明性を高め、投資家や一般市民がこのセグメントのパフォーマンスに関する重要なデータや指標を入手できるようにすることを求められています。この取り組みには、ネットワークのパフォーマンスを示す重要な指標であるゲームのレスポンスタイムが最も優れたインターネットサービスプロバイダを四半期ごとに表彰することも含まれています。

- モバイルインターネットトラフィックは、サウジアラビアのゲーム市場を牽引する上で極めて重要な役割を果たしています。モバイルインターネットトラフィックが増加することで、オンラインゲームプラットフォームへのアクセスが広がり、サウジアラビアの個人はさまざまなゲームをダウンロードしてプレイできるようになります。モバイル機器の安定した高速インターネット接続により、ゲーマーはシームレスなゲーム体験を楽しみ、さまざまなゲームジャンルを探索し、世界のゲームコミュニティとつながることができます。Stacounterによると、サウジアラビアにおけるモバイルインターネットトラフィックのシェアは75.18%です。

中東のゲーム産業概要

中東のゲーム市場は適度にセグメント化されており、多くの世界と地域参入企業が存在します。主要参入企業としては、Sony Corporation、Microsoft Corporation、Apple Inc.、Google LLC(Alphabet Inc.)、Electronic Arts Inc.などが挙げられます。市場の参入企業は、製品ラインナップを強化し、サステイナブル競争優位性を獲得するために、提携や買収などの戦略を採用しています。

2023年5月、Appleは、200を超える非常に楽しいゲームに無制限にアクセスできる同社の定額制ゲームサービス「Apple Arcade」に、20の新タイトルをリリースすると発表しました。「WHAT THE CAR?」、「TMNT Splintered Fate」、「Disney SpellStruck」、「Cityscapes」などです。「Sim Builder」などが、Apple Arcadeで新たに提供されます。今回のアップデートには、「Temple Run+」、Playdeadの「LIMBO+」、「PPKP+」などのApp Storeの人気ゲームが含まれています。

2022年8月、サウジアラビアはMicrosoftによるゲーム会社Activision Blizzardの買収を承認しました。サウジアラビアの規制機関は、MicrosoftによるActivision Blizzardの買収を687億米ドルで承認しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- エコシステム分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響評価

第5章 市場力学

- 市場の促進要因

- 若者とミレニアル世代の消費者の存在

- eスポーツベッティングやファンタジーサイトなどのゲームプラットフォームの採用

- 市場抑制要因

- 違法コピー、法規制、ゲーム取引中の不正行為に関する懸念などの問題

第6章 中東におけるクラウドゲームの展望

- 現在の市場シナリオ

- 中東におけるクラウドゲームの市場分析

- 中東におけるクラウドゲームの主要利害関係者

- Etisalat

- PlayPod

- PlayKey

- Nvidia(GeForce)

- Google Stadia

- トルコにおけるクラウドゲームの導入に影響を与えると予想される主要因の評価

- 市場展望

第7章 市場セグメンテーション

- プラットフォーム別

- ブラウザPC

- スマートフォン

- タブレット

- ゲーム機

- ダウンロード/ボックスPC

- 国別

- アラブ首長国連邦

- サウジアラビア

- トルコ

- イラン

- クウェート

- その他の中東地域

第8章 競合情勢

- 企業プロファイル

- Sony Corporation

- Microsoft Corporation

- Apple Inc.

- Google LLC(Alphabet Inc.)

- Electronic Arts Inc.

- NetEase Inc.

第9章 投資分析

第10章 投資分析市場の将来

The Middle East Gaming Market size is estimated at USD 7.04 billion in 2025, and is expected to reach USD 11.87 billion by 2030, at a CAGR of 11.02% during the forecast period (2025-2030).

With the recent outbreak of COVID-19, the gaming market in the region is expected to witness significant growth due to an increased usage of online gaming services. Various gaming vendors in the market are expected to focus on increasing their user base during this period and surging returns post COVID-19 scenarios, owing to which vendors are offering benefits, offers, and waiving off their fees on the use of their services.

The gaming industry proliferates in the United Arab Emirates, with rising interest and investment in locally developing homegrown talent and games. In terms of spending, it is a very diverse region. It is expected that the average gamer in the country spends USD 115 per year.

Additionally, the growing penetration of smartphones and online gaming is a crucial factor driving the market's growth. The growing development of AR-based apps and games is expected to create market opportunities over the forecast period.

The Saudi Arabian government is also heavily investing billions of dollars in theme parks and amusement spaces. So, as Saudi entertainment industry stakeholders, trade visitors can attend dedicated conferences to gain knowledge and wealth of experience and get a hands-on technology experience at its innovative best.

Saudi Arabia set up a new charity e-sports event to raise money to fight the COVID-19 outbreak with a USD 10 million prize fund. The competition comes as the COVID-19 outbreak keeps people at home, shuts down businesses, and restricts travel to a minimum. This may unite and connect the global gaming community in response to COVID-19. With around 70% of the country's population under 30 years and approximately 20 million gamers or gaming enthusiasts, the market is expected to grow over the forecast period.

Middle East Gaming Market Trends

The Smartphones Segment is Expected to Hold the Significant Market Share

- In recent times mobile gaming has surpassed console and PC gaming as the most popular form of gaming in the Middle East region. One of several factors for the growth of mobile gaming is its availability, and almost everyone has a smartphone with games installed in it. Moreover, the increasing demand for mobile games results from various technological advancements and improvements such as AR, VR, cloud gaming, and 5G. Considering the mobile game industry mainly relies on new technology.

- AR is becoming perfect for mobile gaming owing to its immersive and interactive technology. Moreover, mobile games are the most famous AR category in app stores. Apart from previously released AR mobile games, which are still famous, such as Pokemon Go and Ingress.

- In a move to diversify the oil-dependent economy of the region and boost its software power, the United Arab Emirates (UAE) and its population of young individuals have jumped into a range of sectors, including sports and technology, in recent years.

- For instance, according to the reports by Abu Dhabi's Media and Entertainment Free Zone Authority, twofour54, and other media, expenditure on games reached around USD 326.7 million in 2019. It is anticipated to reach around USD 4.4 billion in 2022.

- Increasing smartphone subscriptions play a significant role in driving the gaming market in the Middle East. As smartphone subscriptions increase, so does the potential user base for mobile games. Smartphones are more accessible and affordable than traditional gaming consoles or PCs, making them the primary gaming platform for many people in the Middle East. This broader audience fuels the demand for mobile games and drives the market growth. According to Ericsson, in 2022, the smartphone subscription in GCC countries is 65 million, expected to increase to 73 million by the next five years.

Saudi Arabia is Expected to Hold Significant Market Share

- As the country has been moving away from its dependency on oil with its Vision 2030, the focus is significantly on digitization. Saudi Arabia's VR gaming space has been taking shape within various malls in the country, looking to house the best of the VR gaming industry. The VR concept is also increasing the business value of the malls with the help of new disruptive technology.

- Moreover, the awareness of VR is steadily growing among gamers of all age groups in the country. After the introduction of the engaging VR headsets, a dynamic shift has been taking place in the gaming industry.

- According to Social Development Bank (SDB), the video games market in Saudi Arabia is estimated to be around USD 1 billion, and the country aims to boost the market value up to USD 2.5 billion by 2030.

- Telcos in the country are also being pushed to provide the best experience for gamers, raising the transparency levels in the market and enabling investors and the public with crucial data and indicators on the sector's performance. The initiative also includes launching a quarterly award for the internet service provider with the best response time for gaming, which is a key indicator of the network's performance.

- Mobile internet traffic plays a crucial role in driving the gaming market in Saudi Arabia. Increasing mobile internet traffic provides wider access to online gaming platforms, allowing individuals in Saudi Arabia to download and play a variety of games. With a stable and fast internet connection on their mobile devices, gamers can enjoy a seamless gaming experience, explore different game genres, and connect with a global gaming community. According to Stacounter, the Share of mobile internet traffic in Saudi Arabia is 75.18%.

Middle East Gaming Industry Overview

The Middle Eastern Gaming Market is moderately fragmented and has many global and regional players. Some of the major players in the market are Sony Corporation, Microsoft Corporation, Apple Inc., Google LLC (Alphabet Inc.), and Electronic Arts Inc. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

In May 2023, Apple announced the release of 20 new titles on Apple Arcade, the company's gaming subscription service that provides unlimited access to over 200 significantly enjoyable games. WHAT THE CAR?, TMNT Splintered Fate, Disney SpellStruck, and Cityscapes: Sim Builder are among the new titles available on Apple Arcade. The update includes popular App Store games like Temple Run+, Playdead's LIMBO+, PPKP+, and others.

In August 2022, Saudi Arabia approved Microsoft's acquisition of Activision Blizzard, a video game company. Saudi Arabia's regulatory body approved Microsoft's acquisition of Activision Blizzard for USD 68.7 billion.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Ecosystem Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Presence of Young and Millennial Consumers

- 5.1.2 Adoption of Gaming Platforms, such as E-sports Betting and Fantasy Sites

- 5.2 Market Restraints

- 5.2.1 Issues like Piracy, Laws and Regulations, and Concerns Relating to Fraud During Gaming Transactions

6 CLOUD GAMING LANDSCAPE IN THE MIDDLE EAST

- 6.1 Current Market Scenario

- 6.2 Analysis of Addressable Market for Cloud Gaming in the Middle East

- 6.3 Major Cloud Gaming Stakeholders in the Middle East

- 6.3.1 Etisalat

- 6.3.2 PlayPod

- 6.3.3 PlayKey

- 6.3.4 Nvidia (GeForce)

- 6.3.5 Google Stadia

- 6.4 Assessment of Major Factors Expected to Influence the Adoption of Cloud Gaming in Turkey

- 6.5 Market Outlook

7 MARKET SEGMENTATION

- 7.1 By Platform

- 7.1.1 Browser PC

- 7.1.2 Smartphone

- 7.1.3 Tablets

- 7.1.4 Gaming Console

- 7.1.5 Downloaded/Box PC

- 7.2 By Country

- 7.2.1 United Arab Emirates

- 7.2.2 Saudi Arabia

- 7.2.3 Turkey

- 7.2.4 Iran

- 7.2.5 Kuwait

- 7.2.6 Rest of Middle East

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Sony Corporation

- 8.1.2 Microsoft Corporation

- 8.1.3 Apple Inc.

- 8.1.4 Google LLC (Alphabet Inc.)

- 8.1.5 Electronic Arts Inc.

- 8.1.6 NetEase Inc.