|

市場調査レポート

商品コード

1690755

英国の宅配・速達・小包(CEP)-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)United Kingdom Courier, Express, and Parcel (CEP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国の宅配・速達・小包(CEP)-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 306 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

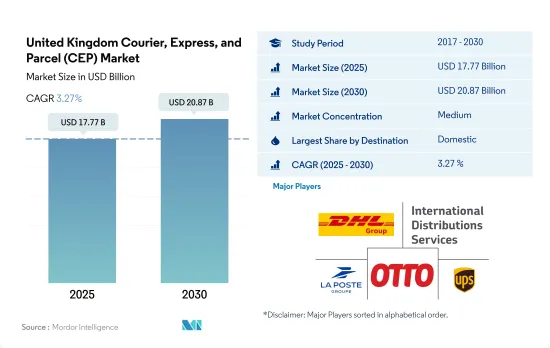

英国の宅配・速達・小包(CEP)市場規模は2025年に177億7,000万米ドルと推定・予測され、2030年には208億7,000万米ドルに達し、予測期間(2025~2030年)のCAGRは3.27%で成長すると予測されます。

eコマースCEP受注の増加に起因するカーボンフットプリント削減イニシアチブの高まりは、CEP産業にプラスの影響を与えると予想されます。

- eコマース産業は、国内外のCEPセグメントの成長を牽引しています。2022年に英国の消費者がオンラインで購入した最も一般的な商品はファッション商品で、衣料品が63%、靴が47%のシェアを占めています。次いで、民生用電子機器製品が35%、書籍・映画ゲームが33%です。これらの品目はすべて、英国のCEP需要を牽引しています。

- 最大の市場シェアを誇るCEP企業は、大量の小包を配達することで発生する二酸化炭素排出量を削減するために、重要な措置を講じています。例えば、ロイヤルメールは、9万人の郵便配達員に足による配達を許可しています。配達の3分の2は、純粋に徒歩で、あるいは「パーク・アンド・ループ」方式で行われており、そのほとんどが徒歩です。同社はまた、二酸化炭素排出量削減のさらなる取り組みとして、2023年までに5,500台の電気バンの導入を目指しています。Amazonも2022年にロンドンで徒歩と電動カーゴ二輪車による配送を開始しました。両社の取り組みは、2040年までにすべての貨物の炭素排出量を正味ゼロにするというコミットメントの一環です。

英国の宅配・速達・小包(CEP)市場動向

消費者向けフルフィルメントセンターの需要増加により、英国の倉庫数は2027年までに21万4,000に達すると予想されます。

- 2024年5月、DP Worldは顧客競合強化のための5,000万英ポンド(6,092万米ドル)の投資の一環として、コベントリーに59万8,000平方フィート(約8,000平方メートル)というこれまでで最大の倉庫を開設しました。これは、2023年9月にビスターに開設した27万平方フィートの音楽・ビデオ流通倉庫に続くもので、英国の物理的な音楽の70%、ホームエンターテイメント製品の35%を取り扱う。DPワールドはこれまで、バートン・アポン・トレントに7万5,000平方フィートの倉庫を、ロンドン・ゲートウェイの物流ハブに23万平方フィートのマルチユーザー倉庫を開設しています。サウサンプトンとロンドン・ゲートウェイのハブとともに、78カ国で事業を展開するDPワールドは、世界貿易の10%を管理しています。このようなイニシャティブは、このセクタからのGDP貢献を押し上げると期待されています。

- 英国の大型倉庫の数は急速に増加しています。2027年までに、世界全体で5万平方フィート以上の倉庫は約21万4,000棟になると予想されています。これらの倉庫の多くはeコマース・フルフィルメントセンターとして機能し、2027年までに全倉庫の約18%が消費者向けフルフィルメント用となります。この増加は、貿易物流ハブとして運営される倉庫の割合が消費者向けフルフィルメントセンターにシフトし始め、eコマースの世界の拡大を示唆しています。

英国政府は燃料価格に大きな影響を及ぼしており、燃料税と付加価値税(標準税率20%)がガソリンと軽油価格の大半を占めています。

- 2022年8月、原油価格は100米ドルを割り込み、1バレル90.63米ドルで1ヵ月を終えました。2023年にはさらに値下がりし、5月には1バレル72.50米ドルまで下がりました。2024年3月、英国のガソリン価格は1リットル当たり平均150.1ペソとなり、2023年11月以来の高値となりました。これは中東情勢の緊迫化による原油価格の上昇とポンド安ドル高によるものです。全体的なインフレ率は緩和しているもの、ガソリンと軽油の価格は3月に上昇しました。原油価格は、2024年4月のイスラエルによるイランへの報復攻撃で急騰した後、下落しました。

- 2024年6月、英国政府は2030年までにジェット燃料に少なくとも10%のサステイナブル航空燃料(SAF)を義務付ける計画を確認しました。現在、SAFは希少であり、従来の燃料よりも高価であるため、航空セグメントでの使用を増やすことは困難です。SAFは、世界のジェット燃料の0.1%以下です。政府によるSAFの義務化は、法制化の承認を経て、2025年1月に開始される予定です。これは、2050年までに航空機の排出量を正味ゼロにすることを目指す2022年の「ジェット・ゼロ」戦略に続くものです。

英国の宅配・速達・小包(CEP)産業概要

英国の宅配・速達・小包(CEP)市場は適度に統合されており、DHL Group、International Distributions Services(Royal Mailを含む)、La Poste Group、Otto Group(The Hermes Groupを含む)、United Parcel Service of America, Inc.(UPS)の5社が主要企業です(アルファベット順)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 人口動態

- 経済活動別GDP分布

- 経済活動別GDP成長率

- インフレ率

- 経済パフォーマンスとプロファイル

- eコマース産業の動向

- 製造業の動向

- 運輸・倉庫業のGDP

- 輸出動向

- 輸入動向

- 燃料価格

- 物流実績

- インフラ

- 規制の枠組み

- 英国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 販売先

- 国内

- 国際

- 配達スピード

- 速達

- 非速達

- モデル

- 企業間(B2B)

- B2C

- 消費者間(C2C)

- 出荷重量

- 重量貨物

- 軽量貨物

- 中量貨物

- 輸送形態

- 航空便

- 道路

- その他

- エンドユーザー

- eコマース

- 金融サービス(BFSI)

- 医療

- 製造業

- 第一次産業

- 卸売・小売業(オフライン)

- その他

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- APC Overnight

- DHL Group

- FedEx

- GEODIS

- International Distributions Services(Royal Mailを含む)

- La Poste Group

- Otto Group(including The Hermes Group)

- Rapid Parcel

- United Parcel Service of America, Inc.(UPS)

- Yodel

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 技術の進歩

- 情報源と参考文献

- 図表リスト

- 主要な洞察

- データパック

- 用語集

The United Kingdom Courier, Express, and Parcel (CEP) Market size is estimated at 17.77 billion USD in 2025, and is expected to reach 20.87 billion USD by 2030, growing at a CAGR of 3.27% during the forecast period (2025-2030).

Growing carbon footprint reduction initiatives owing to increasing e-commerce CEP orders are expected to positively impact CEP industry

- The e-commerce industry is a leading driver of growth in the domestic and international CEP segments. The most common goods purchased online by UK consumers in 2022 were fashion goods , with clothing accounting for a 63% share and shoes for a 47% share. These were followed by consumer electronics, with a 35% share, and books, movies, and games, with a 33% share in 2022. All these item deliveries collectively drove CEP demand in the United Kingdom.

- CEP companies with some of the biggest market shares are taking significant steps to reduce the carbon footprint generated by delivering huge volumes of parcels. For instance, Royal Mail has allowed 90,000 posties to make on-feet deliveries. Two-thirds of the deliveries are made purely by foot or through a 'park and loop' method, which is mostly on foot. The company is also aiming to have 5,500 electric vans by 2023 in a further effort to reduce carbon emissions. Amazon also started on-foot and electric cargo bike delivery in London in 2022. Initiatives by both companies are a part of their commitment toward all shipments having net-zero carbon emissions by 2040.

United Kingdom Courier, Express, and Parcel (CEP) Market Trends

The UK's warehouse count is expected to reach 214,000 by 2027 due to a rise in demand for consumer fulfillment centers

- In May 2024, DP World opened its largest warehouse yet, a 598,000 sq ft facility in Coventry, as part of a GBP 50 million (USD 60.92 million) investment to boost customer competitiveness. This follows the September 2023 opening of a 270,000 sq ft music and video distribution warehouse in Bicester, handling 70% of the UK's physical music and 35% of home entertainment products. Previously, DP World opened a 75,000 sq ft site in Burton upon Trent and a 230,000 sq ft multi-user warehouse at London Gateway's logistics hub. Alongside its hubs at Southampton and London Gateway, operating in 78 countries, DP World manages 10% of global trade. Such initiaves are expected to boost the GDP contribution from the sector.

- The number of large warehouses in the United Kingdom is rapidly increasing. By 2027, there are expected to be around 214,000 warehouses larger than 50,000 square feet globally. Many of these warehouses are to serve as e-commerce fulfillment centers, and approximately 18% of all warehouses will be for consumer fulfillment by 2027. This increase suggests the global expansion of e-commerce as the proportion of warehouses operating as trade distribution hubs begins to shift in favor of consumer fulfillment centers.

UK government has a major influence on fuel prices, and both fuel duty and VAT (standard 20% rate) make up majority of the petrol and diesel prices

- In August 2022, the oil price dropped under USD 100 and finished the month at USD 90.63 a barrel. Prices dropped further in 2023, and by May, a barrel of oil was down to USD 72.50. In March 2024, petrol prices in the UK averaged 150.1p per litre, the highest since November 2023. This is due to rising oil prices due to Middle East tensions and a weaker pound against the dollar. Although overall inflation has eased, petrol and diesel prices increased in March. Oil prices have since dropped after spiking following Israel's retaliatory attack on Iran in April 2024.

- In June 2024, the UK government confirmed it plans to require at least 10% sustainable aviation fuel (SAF) in jet fuel by 2030. Currently, SAF is scarce and more expensive than traditional fuels, making it challenging to increase its use in aviation. SAF represents less than 0.1% of jet fuel globally. The government's SAF mandate, pending legislative approval, is set to start in January 2025. This follows the 2022 "Jet Zero" strategy aiming for net-zero emissions in aviation by 2050.

United Kingdom Courier, Express, and Parcel (CEP) Industry Overview

The United Kingdom Courier, Express, and Parcel (CEP) Market is moderately consolidated, with the major five players in this market being DHL Group, International Distributions Services (including Royal Mail), La Poste Group, Otto Group (including The Hermes Group) and United Parcel Service of America, Inc. (UPS) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Demographics

- 4.2 GDP Distribution By Economic Activity

- 4.3 GDP Growth By Economic Activity

- 4.4 Inflation

- 4.5 Economic Performance And Profile

- 4.5.1 Trends in E-Commerce Industry

- 4.5.2 Trends in Manufacturing Industry

- 4.6 Transport And Storage Sector GDP

- 4.7 Export Trends

- 4.8 Import Trends

- 4.9 Fuel Price

- 4.10 Logistics Performance

- 4.11 Infrastructure

- 4.12 Regulatory Framework

- 4.12.1 United Kingdom

- 4.13 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes Market Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Destination

- 5.1.1 Domestic

- 5.1.2 International

- 5.2 Speed Of Delivery

- 5.2.1 Express

- 5.2.2 Non-Express

- 5.3 Model

- 5.3.1 Business-to-Business (B2B)

- 5.3.2 Business-to-Consumer (B2C)

- 5.3.3 Consumer-to-Consumer (C2C)

- 5.4 Shipment Weight

- 5.4.1 Heavy Weight Shipments

- 5.4.2 Light Weight Shipments

- 5.4.3 Medium Weight Shipments

- 5.5 Mode Of Transport

- 5.5.1 Air

- 5.5.2 Road

- 5.5.3 Others

- 5.6 End User Industry

- 5.6.1 E-Commerce

- 5.6.2 Financial Services (BFSI)

- 5.6.3 Healthcare

- 5.6.4 Manufacturing

- 5.6.5 Primary Industry

- 5.6.6 Wholesale and Retail Trade (Offline)

- 5.6.7 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 APC Overnight

- 6.4.2 DHL Group

- 6.4.3 FedEx

- 6.4.4 GEODIS

- 6.4.5 International Distributions Services (including Royal Mail)

- 6.4.6 La Poste Group

- 6.4.7 Otto Group (including The Hermes Group)

- 6.4.8 Rapid Parcel

- 6.4.9 United Parcel Service of America, Inc. (UPS)

- 6.4.10 Yodel

7 KEY STRATEGIC QUESTIONS FOR CEP CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.1.5 Technological Advancements

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms