ラテンアメリカの建設:市場シェア分析、産業動向、成長予測(2025年~2030年)

Latin America Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690180

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

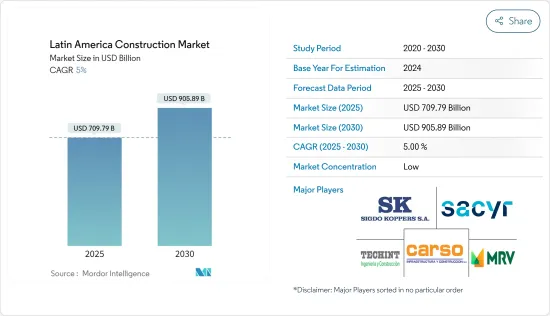

ラテンアメリカの建設市場規模は2025年に7,097億9,000万米ドルと推定され、予測期間(2025年~2030年)のCAGRは5%で、2030年には9,058億9,000万米ドルに達すると予測されます。

同地域では、不動産とインフラに対する需要の高まりが市場を牽引しています。さらに、建設生産高を緩和する政府プロジェクトや政策が市場を牽引しています。

主なハイライト

- ラテンアメリカでは建築セクターが急速に拡大しています。この地域にはさまざまな国があり、それぞれが異なる政治・経済情勢を有しています。このような違いがあるにもかかわらず、建設業界はいくつかの原動力によって地域全体で拡大しています。

- こうした拡大要因にもかかわらず、ラテンアメリカの建設業界はいくつかの障害に直面しています。建設プロジェクトの資金不足は大きな問題の一つです。大規模な建設プロジェクトは、多くの地域で資金調達が困難です。従来の金融機関から融資を受けることが困難な中小の建設会社は、特にその傾向が強いと思われます。

- 有能な労働力の不足も、ラテンアメリカの建設部門が直面している問題です。熟練労働者の不足は、特にエンジニアリングやアーキテクチャのような技術職において、この地域の多くの国々を悩ませています。有能な労働力の不足により、建設プロジェクトを予定通り予算内で完了させることは困難かもしれないです。

- 都市化は、ラテンアメリカの建設業界を活性化させる主な要因のひとつです。より大きな経済的展望を求めて都市に移住する人が増え、この地域は急速に都市化が進んでいます。新しい住宅、企業、道路、橋、公共交通システムなどのインフラ・プロジェクトに対する需要は、この動向に後押しされています。

- 2022年第2四半期、この地域のホスピタリティ関連の建設パイプラインは、555プロジェクト、90,496室となっています。パンデミック(世界的大流行)による2年近い不安の後、ラテンアメリカのホテル業界はようやく回復の兆しを見せています。国境規制や地域の検疫要件が緩和されたことで、消費者の信頼感は高まっています。ラテンアメリカ諸国への航空旅客数は、2021年第2四半期と比較して大幅に増加しています。同地域では、2022年上半期に40プロジェクト、合計8,481室が着工しました。2022年第2四半期の新規プロジェクト発表は前年同期比57%増の36プロジェクト/6,208室。

ラテンアメリカの建設市場動向

住宅建設の増加が市場を牽引

政府や業界の統計によると、コロンビアの都市部における住宅供給は増加傾向にあります。公式統計によると、コロンビアの住宅ストックは130万戸以上不足しています。政府は需要を満たすため、建設や住宅投資を奨励し、助成する政策を実施しています。コロンビアは、この地域で最も急成長している建設ブームを経験しています。

パナマは、その例外的なビジネス環境から、アメリカ、欧州、ラテンアメリカの投資家の注目を集めています。この小さな国がムンドのお気に入りのひとつであることは周知の事実です。パナマは、少し前にコンサルタント・グループがムンドの設立を決めた場所でもあります。ここ数十年、パナマは奇跡的な好景気に沸いています。軍事クーデター、高インフレ、無価値通貨に慣れ親しんだラテンアメリカでは珍しい安定性と低インフレ率から、私たちはこれをパナマ例外主義と呼びました。自由主義的な経済政策と政治的安定性により、不動産業界は繁栄しています。過去10年間、米国、コロンビア、アジアからの投資家が需要を満たすために殺到し、価格を年間5~10%押し上げました。

ブラジル経済は予想以上に堅調に回復し、指標は第1四半期を上回りました。取引量が減少し、まだ入居手続き中のスペースがいくつか空室となっているもの、当市場のAクラスオフィス市場の業績は、今上半期も堅調なペースで推移しています。空室率は35.37%と、前年同期の35.45%から低下し、安定しているもの高い水準にあります。低水準ながら、この重要な都市のほとんどの地区で、新規雇用の動きが失業率を上回りました。

ホスピタリティ・インフラの開発が市場を開拓

経済的圧力にもかかわらず、ラテンアメリカの宿泊市場は「著しい経済的変貌」を遂げつつある、と業界専門家の一人が報告しています。既存および新規のホスピタリティ・プロジェクトへの一貫した投資が、宿泊需要を牽引し、2年後の供給増を支えると思われます。既存のホテル供給比率(人口1,000人当たりのその国の推定関連ホテル客室数を示す指標)が2.6であるメキシコは、宿泊市場において最も先進的な国です。今後10年間で、一貫したビジネス、観光、インフラ投資により、ホテル供給比率は3.8まで上昇すると思われます。チリは、この地域で最も安定した経済の一つと広く見なされており、支持可能な供給が5.3%増加し、2年間で推定46,700室の質の高いホテルがもたらされると予想されています。

コロンビアでも、観光、一般的な経済成長、特別税制優遇措置により、供給が大幅に増加しています。石油部門は苦境に立たされているが、コロンビアは魅力的なビジネス・観光地として台頭し続けているため、今後10年間は安定した投資を呼び込むことが期待されます。ペルーは、既存ストックの基盤が比較的小さいにもかかわらず、今後10年間の質の高い宿泊施設供給の成長率が高く、プロファイル対象国の中で最も高い成長率を示しています。

ラテンアメリカ建設産業の概要

ラテンアメリカの建設市場はかなり細分化されており、主に地元や地域の企業で構成され、世界企業はほとんどいないです。主な企業は、Empresa i.C.A., S.A.B. de C.V., O.A.S. S.A., IDEAL, S.A.B. de C.V., Cyrela Brazil Realty S.A., Andrade Gutierrez S.A.などです。観光客の増加により、ホスピタリティ・インフラの建設・開発の機会が生まれています。また、この地域の新興政策に準拠する企業には、市場シェアを高めるチャンスがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場分析

- 現在の経済と建設市場のシナリオ

- 建設分野における技術革新

- 政府の規制と取り組みが業界に与える影響

- 建設資材の主要輸出入統計

- COVID-19の市場への影響

第5章 市場力学

- 促進要因

- 市場を牽引する住宅建設の増加

- ホスピタリティ・インフラの開発が市場を牽引

- 抑制要因

- 融資へのアクセス制限

- 熟練労働者の不足

- 機会

- 市場を牽引する新しいインフラの必要性

- 手頃な価格の住宅需要の増加

- バリューチェーン/サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者/買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第6章 市場セグメンテーション

- タイプ別

- 住宅用

- 商業用

- 産業用

- インフラ

- エネルギーと公益事業

第7章 競合情勢

- 市場集中度の概要

- 企業プロファイル

- Sigdo Koppers

- Sacyr

- MRV Engenharia

- Carso Infraestructura y Construcci-n

- Techint Ingenier-a y construcci-n

- Aenza(Gra-a y Montero)

- SalfaCorp

- Mota-Engil

- Besalco

- Echeverria Izquierdo

第8章 市場の将来

第9章 付録

目次

The Latin America Construction Market size is estimated at USD 709.79 billion in 2025, and is expected to reach USD 905.89 billion by 2030, at a CAGR of 5% during the forecast period (2025-2030).

The region's growing demand for real estate and infrastructure drives the market. Furthermore, government projects and policies easing the construction output drive the market.

Key Highlights

- The building sector is expanding quickly in Latin America. The area is home to various nations, each with a distinct political and economic climate. Despite this variation, the construction industry is expanding across the region due to several dynamics.

- Despite these factors encouraging expansion, Latin America's construction industry faces several obstacles. Lack of funding for construction projects is among the major problems. Large-scale construction projects are challenging to finance in many regions due to the lack of access to financing. Smaller construction companies, who may find it difficult to obtain finance from conventional lenders, may find this especially true.

- Lack of competenlaborur is another issue Latin America's construction sector is facing. A lack of skilled labor plagues many of the region's nations, especially in technical professions like engineering and architecture. It may be challenging to finish construction projects on schedule and within budget due to the lack of competent labor.

- Urbanization is one of the main factors boosting the Latin American construction industry. More people are relocating to cities for greater economic prospects, and the region is rapidly becoming more urbanized. Demand for new homes, businesses, and infrastructure projects like roads, bridges, and public transportation systems is being driven by this trend.

- In Q2 2022, the region's total hospitality construction pipeline includes 555 projects and 90,496 rooms. Following nearly two years of uncertainty caused by the pandemic, the Latin American hotel industry is finally showing signs of recovery. Consumer confidence has risen as border restrictions and regional quarantine requirementsn have been relaxed. Air passenger traffic to Latin American countries has increased significantly compared to the second quarter of 2021. In the region, 40 projects totaling 8,481 rooms began construction in the first half of 2022. In Q2 2022, new project announcements increased 57% year on year to 36 projects/6,208 rooms.

Latin America Construction Market Trends

Increase in residential construction driving the market

According to government and industry figures, Colombia's supply of urban housing has been increasing. However, it has not been sufficient to offset demand: according to official statistics, the country's housing stock is more than 1.3 million homes short. The government has implemented policies to meet the demand that encourages and subsidizes construction and housing investment. Colombia is experiencing the region's fastest-growing construction boom.

Because of its exceptional business conditions, Panama is on the minds of American, European, and Latin American investors. It's no secret that this tiny country is one of Mundo's favorites. It is the location where a group of consultants decided to establish Mundo some time ago. In recent decades, Panama has experienced a miraculous economic boom. We called it Panamanian Exceptionalism because of its stability and low inflation rates, unusual in Latin America, a region accustomed to military coups, high inflation, and worthless currencies. The real estate industry thrives due to liberal economic policies and political stability. Over the last decade, investors from the United States, Colombia, and Asia have rushed to meet demand, pushing prices up by 5 to 10% per year.

The Brazilian economy recovered more solidly than expected, with indicators higher than in the first quarter. Despite a decrease in the volume of transactions and the vacancy of some spaces still in process, the performance of the Class A office market in this market continues at a steady pace in this first semester. The availability rate is still stable but high at 35.37%, down from 35.45% in the year's first quarter. Despite being low, activity in new occupations outpaced unemployment in most corridors of this important city.

Development of hospitality infrastructure driving the market

Despite economic pressures, the Latin American lodging market is undergoing a "significant economic transformation," according to a report by one of the industry experts. Consistent investment in existing and new hospitality projects will drive lodging demand and support supply growth in two years. With an existing hotel supply ratio (a measure of the estimated relevant hotel rooms in a country per 1,000 inhabitants) of 2.6, Mexico is the most advanced country in its lodging market. Over the next decade, consistent business, tourism, and infrastructure investment will raise the hotel supply ratio to 3.8. Chile, widely regarded as one of the most stable economies in the region, is expected to see a 5.3% increase in supportable supply, bringing in an estimated 46,700 quality hotel rooms in two years.

Colombia has also seen significant supply increases due to tourism, general economic growth, and special tax incentives. While the petroleum sector has suffered, Colombia is expected to attract consistent investment over the next decade as it continues to emerge as an appealing business and tourist destination. Peru has the highest growth rate among the profiled countries, with a high growth rate in quality lodging supply over the next decade despite having a relatively small base of existing stock.

Latin America Construction Industry Overview

The Latin America Construction Market is fairly fragmented, comprising mainly local and regional players, with few global players. The major players are Empresa I.C.A., S.A.B. de C.V., O.A.S. S.A., IDEAL, S.A.B. de C.V., Cyrela Brazil Realty S.A., Andrade Gutierrez S.A., and many more. The rise in tourism creates opportunities for the construction and development of hospitality infrastructure. Also, companies complying with the emerging policies in the region have opportunities to gain a good market share.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Economic and Construction Market Scenario

- 4.2 Technological Innovations in the Construction Sector

- 4.3 Impact of Government Regulations and Initiatives on the Industry

- 4.4 Key Exports & import statistics of construction materials

- 4.5 Impact of COVID - 19 on the market

5 MARKET DYNAMICS

- 5.1 Drivers

- 5.1.1 Increase in residential construction driving the market

- 5.1.2 Development of hospitality infrastructure driving the market

- 5.2 Restraints

- 5.2.1 Limited access to financing

- 5.2.2 Shortage of skilled labor

- 5.3 Opportunitites

- 5.3.1 The need for new infrastructure driving the market

- 5.3.2 Increasing demand for affordable housing

- 5.4 Value Chain / Supply Chain Analysis

- 5.5 Porter's Five Forces Analysis

- 5.5.1 Bargaining Power of Suppliers

- 5.5.2 Bargaining Power of Consumers / Buyers

- 5.5.3 Threat of New Entrants

- 5.5.4 Threat of Substitute Products

- 5.5.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Residential

- 6.1.2 Commercial

- 6.1.3 Industrial

- 6.1.4 Infrastructure

- 6.1.5 Energy and Utilities

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 Sigdo Koppers

- 7.2.2 Sacyr

- 7.2.3 MRV Engenharia

- 7.2.4 Carso Infraestructura y Construcci-n

- 7.2.5 Techint Ingenier-a y construcci-n

- 7.2.6 Aenza (Gra-a y Montero)

- 7.2.7 SalfaCorp

- 7.2.8 Mota-Engil

- 7.2.9 Besalco

- 7.2.10 Echeverria Izquierdo

8 FUTURE OF THE MARKET

9 APPENDIX

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日