|

市場調査レポート

商品コード

1910842

インドネシアのフレキシブル包装市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Indonesia Flexible Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドネシアのフレキシブル包装市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

概要

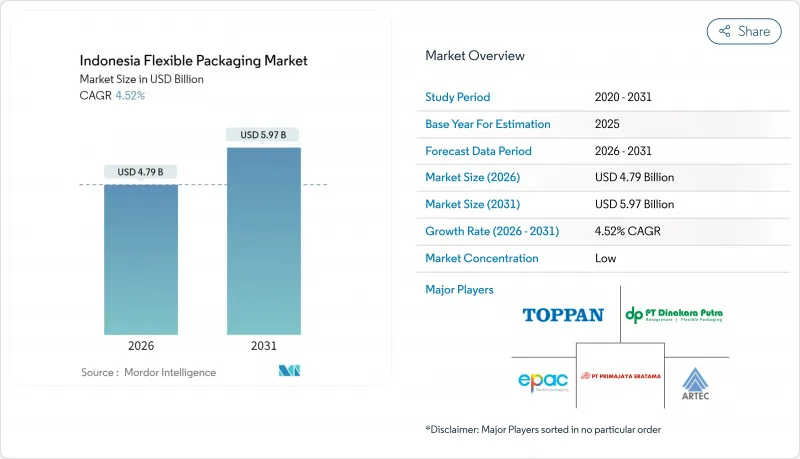

インドネシアのフレキシブル包装市場は、2025年に45億8,000万米ドルと評価され、2026年の47億9,000万米ドルから2031年までに59億7,000万米ドルに達すると予測されています。

予測期間(2026年~2031年)におけるCAGRは4.52%と見込まれています。

この成長軌跡は、東南アジア最大の経済規模を誇るインドネシアの立場を反映しており、都市化が進む人口が包装食品とオンライン小売へ着実に移行していることが背景にあります。いずれもフレキシブル包装形式への依存度が高い分野です。小分け包装への需要拡大、持続的な電子商取引活動、企業の持続可能性への取り組みが相まって、インドネシアのフレキシブル包装市場に有利な素材・製品・技術の変化を後押ししています。中国を中心とした輸入完成品は、国内コンバーターにとって依然としてコスト上の課題となっております。しかしながら、2025年に施行予定の拡大生産者責任(EPR)規制により、現地再生原料の需要加速が見込まれております。競合上の対応策は現在、垂直統合、バリアフィルムの革新、デジタル印刷能力に焦点が当てられており、これらはインドネシアの2,550万社に及ぶデジタル対応中小企業向けに、小ロット生産を可能にするものでございます。

インドネシアのフレキシブル包装市場の動向と洞察

包装食品・飲料消費の急増

包装食品は2024年に国内総生産(GDP)の6.47%を占め、インドネシア食品飲料起業家協会は、都市部の世帯が調理済み食品や高級スナックを好む傾向から、この割合がさらに上昇すると予測しております。2024年10月に導入された義務的なハラール表示には、明確で耐久性のある印刷が求められ、インドネシアの湿潤な多島嶼型サプライチェーンにおいて製品の品質を保持する高バリア性多層フィルムへの需要が高まっております。輸入された特殊食品や可処分所得の増加も、高級保護構造への需要をさらに後押ししています。こうした背景から、高度な酸素・湿気バリアフィルムを提供するコンバーターは、乳製品、肉製品、菓子加工業者からの受注を拡大しています。インドネシアのフレキシブル包装市場は、この着実な数量成長と、陳列に適したスタンドアップパウチを好む現代的な流通チャネルへの移行から直接的な恩恵を受けています。

持続可能な包装ソリューションへの需要加速

2025年に施行されるEPR規制では、生産者が2029年までに消費後プラスチック廃棄物を30%削減することが義務付けられており、リサイクル可能な単一素材フィルムや認証済み堆肥化可能素材への投資が促進されています。現地スタートアップのGreenhope社とBiopac社はPHA(ポリヒドロキシアルカン酸)および澱粉ベースのフィルムの量産化を進めており、一方、ダノン・インドネシアなどの多国籍企業は既にペットボトルに25%のリサイクル素材を使用しており、食品グレードの再生ポリエステル(rPET)の需要拡大につながっています。環境配慮をアピールしたいブランドは、バリア性能を維持しつつ廃棄処理を簡素化する代替基材を指定する傾向にあります。このためインドネシアのフレキシブル包装市場では、アジアおよび輸出市場向けリサイクル基準を満たすフィルムの受注が堅調に推移しております。

ポリオレフィン原料価格の変動性

2024年初頭、安価な輸入品により国内原料の競合力が低下した結果、国内上流部門の稼働率は55%を下回りました。コンバーター企業は、スポット樹脂価格が前月比15%以上変動するため、コストを確実にヘッジできず、固定価格包装契約の利益率が圧迫されています。提案されているアンチダンピング関税は国内供給を安定させる可能性がありますが、国内クラッカーの増産または輸入割当の引き締めが行われるまでは不確実性が残ります。このため、インドネシアのフレキシブル包装市場では、堅調な最終用途需要があるにもかかわらず、慎重な生産能力拡大が続いております。

セグメント分析

プラスチックは、コスト効率と優れた防湿特性により、2025年においても売上高シェア67.61%を維持し、インドネシアのフレキシブル包装市場を支えています。ポリエチレン(PE)およびポリプロピレン(PP)フィルムは、スナック菓子、冷凍食品、農業用途において不可欠な素材であり続けております。しかしながら、PE 60万5,000トン、PP 59万9,000トンに及ぶ輸入依存度が価格安定性を制限しております。バイオプラスチックおよび堆肥化可能素材は、ベースは小さいもの、EPR(生産者責任拡大)の期限が迫る中、7.45%という最速のCAGRを記録しております。

競合上の対応策として、グリーンホープ社のPHAベースフィルムやバイオパック社の堆肥化基準適合澱粉ブレンドフィルムが挙げられます。ブランドオーナーは機械的強度を維持しつつリサイクルを簡素化する単一素材PEラミネート試験を進めています。生分解性ポリマー工場への政府支援策により、現在のコストプレミアムにもかかわらず、代替基材向けインドネシアフレキシブル包装市場規模は2031年まで拡大を続ける見込みです。

2025年時点で、袋・パウチは食品、パーソナルケア、農薬製品ラインにおける汎用性から、インドネシアのフレキシブル包装市場規模の46.88%を占めました。スタンドアップ形式、ジッパー、注ぎ口は、現代の小売環境において利便性と店頭での訴求力を高めます。フィルムとラップは食肉加工業や園芸産業に、ラベルはプレミアムブランディング予算を獲得する用途で活用されています。

サシェおよびスティックパックはCAGR6.35%で拡大し、群島市場における手頃な価格と試供品ニーズに対応しています。デジタル印刷機により、金型を変更せずに地域固有の言語や祝祭日のデザインが可能となり、発売までのリードタイムを数日に短縮しています。使い捨てプラスチックに対する規制強化を受け、コンバーターは詰め替え用パウチやリサイクル可能なラミネート構造を提案し、小型フォーマットの利便性と環境規制遵守のバランスを図っています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 包装食品・飲料消費の急増

- 持続可能な包装ソリューションへの需要加速

- 電子商取引およびオンライン食料品配送の成長

- 都市部の中産階級増加が小型包装サイズの需要を牽引

- デジタル印刷およびフレキソ印刷による短納期印刷の急速な普及

- ベンチャー資本によるFMCGスタートアップの柔軟なフォーマット拡大

- 市場抑制要因

- ポリオレフィン原料価格の変動性

- 不十分なリサイクルインフラおよび回収システム

- 使い捨てプラスチックに対する環境規制の強化

- 島間物流コストの高さがバリアフィルムの普及を制限している

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- マクロ経済要因が市場に与える影響

- インドネシアにおける規制状況とリサイクル政策

- テクノロジーの展望

第5章 市場規模と成長予測

- 素材別

- 紙

- プラスチック

- 金属箔

- バイオプラスチックおよび堆肥化可能な素材

- 製品タイプ別

- 袋・パウチ

- フィルムおよびラップ

- 小袋およびスティックパック

- ラベル及びスリーブ

- エンドユーザー業界別

- 食品

- ベーカリー製品

- スナック

- 食肉・鶏肉・魚介類

- 菓子類

- ペットフード

- その他の食品製品

- 飲料

- 医療・医薬品

- パーソナルケア・化粧品

- 農業・園芸

- その他の最終用途産業

- 食品

- 印刷技術別

- フレキソ印刷

- グラビア印刷

- デジタル印刷

- その他の印刷技術

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Amcor plc

- Mondi plc

- PT Trias Sentosa Tbk

- PT Indopoly Swakarsa Industry Tbk

- PT Argha Prima Industry Tbk

- Sealed Air Corporation

- Huhtamaki Oyj

- PT Primajaya Eratama

- PT ePac Flexibles Indonesia

- PT Indonesia Toppan Printing

- PT Dinakara Putra

- PT Artec Package Indonesia

- PT Lotte Packaging

- PT Karuniatama Polypack

- PT Masplast Poly Film

- PT Polidayaguna Perkasa

- Constantia Flexibles Group GmbH

- UFlex Limited

- Sonoco Products Company