|

市場調査レポート

商品コード

1689783

屋上太陽光発電設備-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Rooftop Solar Photovoltaic Installation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 屋上太陽光発電設備-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

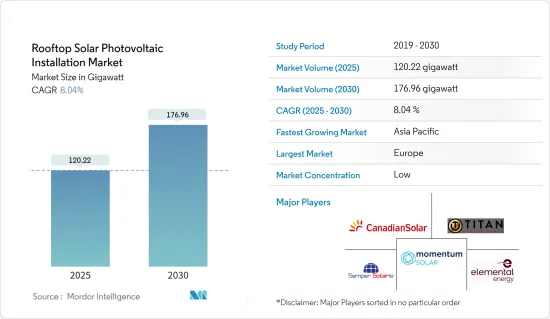

屋上太陽光発電設備市場規模は2025年に120.22ギガワットと推定され、予測期間(2025~2030年)のCAGRは8.04%で、2030年には176.96ギガワットに達すると予測されます。

市場は2020年のCOVID-19によってマイナスの影響を受けました。現在、市場はパンデミック以前のレベルに達しています。

長期的には、ソーラーパネル設備に対する優遇措置や税制優遇措置といった形で政府の支援施策が後押しし、PV設備コストの低下やパネル効率の上昇が予測期間中の市場を牽引するとみられます。

一方、初期設備投資が高額であることが、予測期間中の市場成長の妨げになると予想されます。

新技術の進歩やペロブスカイト太陽電池の市場開拓は、将来的に屋上太陽光発電設備市場にいくつかの機会をもたらすと予想されます。

2022年にはアジア太平洋が屋上設備型太陽光発電の最大市場となりました。同地域には中国やインドなど新興経済諸国がいくつか存在するため、予測期間中に最も急成長する市場になる可能性も高いです。

屋上太陽光発電設備市場の動向

住宅用屋上設備が市場を独占する見込み

- 住宅セグメントには、個人住宅や集合住宅が含まれます。住宅の屋上設備型システムは、業務用や産業用の屋上設備型システムに比べて小規模です。住宅用屋上太陽光発電システムの容量は通常50kWまでです。

- 住宅用屋上太陽光発電システムの導入は、コストの低下と政府の支援施策により、近年世界中で大幅に増加しています。住宅用屋根上太陽光発電設備は、ミニグリッドや個人使用向けに小型の構成にすることもできます。アクセスしやすく、手ごろな価格で信頼できる電力オプションを住民が必要としているさまざまな国から、住宅用屋上システムの需要が高まっています。多くの国では、太陽光発電で発電された電力は、送電網から電力を購入するよりも経済的に魅力的です。

- 例えば、米国ではここ数年、住宅用屋根上太陽光発電の設備容量が急速に増加しています。太陽エネルギー産業協会によると、住宅用屋根上太陽光発電の設備容量は2021~2022年にかけて約40%増加しました。2021年の年間設備容量は4.2GWであったのに対し、2022年には5.9GWとなりました。

- さらに2022年、米国の住宅用太陽光発電システムの平均コストは1ワット当たり3.21米ドルでした。住宅用太陽光発電の価格は過去3年間でわずかに上昇したが、それでも2010年に登録された平均コストの半分以下です。住宅用太陽光発電システムのコスト低下は、米国全土の一般家庭に設備される太陽光発電容量の大幅な増加に寄与しています。

- 欧州連合(EU)はソーラーパネルの国内生産を積極的に推進しており、エネル・グリーンパワー社が欧州連合(EU)と協力してイタリアにあるソーラーパネルのギガファクトリーを拡大したことなどがその例です。欧州連合(EU)の資金援助を受けて、エネル・グリーンパワー社は生産能力を既存の20万キロワットから15倍増の300万キロワットに拡大することを目指しています。2024年7月までに稼動が予定されているこの生産施設は、総額約6億3,000万米ドルの大規模な投資に相当し、欧州連合(EU)からは約1億2,400万米ドルの拠出が見込まれています。この協調的な取り組みにより、当面は屋上用ソーラーパネルのコストが下がり、欧州全域で住宅用屋上ソーラーシステムの需要が高まるとみられます。中国、インド、オーストラリアなどの国々では、住宅部門における太陽エネルギープロジェクトを促進し、設備コストを削減するための政府の取り組みにより、住宅用屋根のニーズがここ数年で高まっています。

- 例えば、インド政府は新・再生可能エネルギー省(MNRE)の系統連系屋根上太陽光発電プログラムの第2段階を開始しました。このプログラムの下、2022年4月、タミル・ナンドゥエネルギー開発庁は、タミル・ナンドゥ州に12MWの系統連系住宅用屋根上太陽光発電システムを設備する入札を実施しました。同様に、テランガナ州再生可能エネルギー局は、50MWの系統連系住宅用屋根上太陽光発電プロジェクトを建設する業者を指名する入札を募集しています。

- 以上のことから、住宅用屋根設備型太陽光発電市場は予測期間中に優位に立つと予想されます。

アジア太平洋が市場を独占する見込み

- アジア太平洋諸国では急速な都市化、人口増加、工業化が進み、電力消費量が大幅に増加しています。これに対応するため、政府や企業は環境問題に対処しつつエネルギー供給を増強する実行可能な手段として、屋上設備型太陽光発電への関心を高めています。

- さらに、アジア太平洋は日照量が豊富で、太陽光発電に非常に適しています。良好な気候条件とソーラーパネル効率の技術的進歩により、屋上設備による最適なエネルギー収量が確保されています。この自然の優位性が、この地域の魅力と太陽光発電設備の実現可能性を高めています。

- 中国には、世界最大の太陽光発電(PV)製造企業や施設がほぼすべてあり、世界の太陽光発電製造能力の70%近くが中国にあります。これらの企業はまた、ソーラーパネルのサプライチェーンに不可欠なポリシリコン、インゴット、ウエハー製造などの他の事業も支配しています。世界の太陽光発電サプライチェーンにおけるこの並外れた支配力により、中国メーカーは他国のソーラー機器メーカーと比べ、より大きな優位性を持っています。

- さらに、政府の積極的な施策とインセンティブは、アジア太平洋を屋上用太陽光発電市場の最前線に押し上げる上で極めて重要な役割を果たしています。同地域の各国政府は、固定価格買取制度、税額控除、屋根上太陽光発電システムの導入を奨励する規制枠組みなど、強力な支援メカニズムを導入しています。こうしたインセンティブは消費者や企業の経済的負担を軽減し、市場の急成長を促しています。

- 2022年6月、オーストラリア政府は新たな屋根上太陽光発電規制を発表しました。政府は2021~22年度予算でSRES(小規模再生可能エネルギー制度)の改革に1,920万米ドルを拠出しました。この改正規制は、消費者保護を強化し、屋上太陽光発電セグメントの健全性を向上させることを目的としています。改正内容は以下の通り:

- 設備業者、太陽光小売業者、製造業者に対する報告要件を合理化します。小規模技術認証の対象となる太陽光発電部材の条件設定において、規制当局がより直接的な役割を果たせるようにします。こうした義務化により、予測期間中に屋上太陽光発電の導入が大幅に増加するとみられます。

- 以上のことから、予測期間中、アジア太平洋が屋上太陽光発電設備市場を独占すると予想されます。

屋上太陽光発電設備産業概要

屋上太陽光発電設備市場は、その性質上、統合されています。市場の主要企業(順不同)には、Titan Solar Power NV Inc、Momentum Solar、Canadian Solar Inc、Elemental Energy Inc、Semper Solaris Construction Incなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 2029年までの屋上設備型太陽光発電(PV)市場(GWベース)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 太陽電池パネルのコスト低下

- 政府の支援施策

- 抑制要因

- 初期費用の高さ

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 導入場所

- 住宅用

- 商業・産業

- 地域(地域市場分析(2029年までの市場規模・需要予測(地域のみ)))

- 北米

- 米国

- カナダ

- その他の北米

- アジア太平洋

- 中国

- インド

- オーストラリア

- 日本

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 欧州

- ドイツ

- 英国

- スペイン

- イタリア

- フランス

- 北欧諸国

- トルコ

- ロシア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- エジプト

- ナイジェリア

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Titan Solar Power NV Inc.

- Momentum Solar

- Canadian Solar Inc.

- Elemental Energy Inc.

- Semper Solaris Construction Inc.

- Pink Energy

- ReVision Energy LLC

- ADT Solar

- Baker Electric Home Energy

- Infinity Energy Inc.

- 市場ランキング/シェア分析

第7章 市場機会と今後の動向

- 新技術の進歩とペロブスカイト太陽電池の開発

The Rooftop Solar Photovoltaic Installation Market size is estimated at 120.22 gigawatt in 2025, and is expected to reach 176.96 gigawatt by 2030, at a CAGR of 8.04% during the forecast period (2025-2030).

The market was negatively impacted by COVID-19 in 2020. Presently the market has now reached pre-pandemic levels.

Over the long term, supportive government policies in the form of incentives and tax benefits for solar panel installation, declining PV installation costs, and rising panel efficiencies are expected to drive the market during the forecast period.

On the other hand, high initial capital investment are expected to hinder the growth of the market during the forecasted period.

Nevertheless, new technological advancements and the development of perovskite solar cells are expected to create several opportunities for the rooftop solar PV installation market in the future.

Asia-Pacific was the largest market for rooftop solar PV installation in 2022. The region is also likely to be the fastest-growing market during the forecast period due to the presence of several developing economies, such as China and India.

Rooftop Solar Photovoltaic Installation Market Trends

Residential Rooftop Installation Expected to Dominate the Market

- The residential segment includes individual houses and residential building complexes. Residential rooftop-mounted systems are small compared to commercial and industrial rooftop systems. The residential rooftop solar PV system typically has a capacity range of up to 50 kW.

- The deployment of residential rooftop solar PV systems has increased significantly in recent years worldwide, owing to the declining costs and the government's supportive policies. Residential rooftop solar PV installations can be arranged in smaller configurations for mini-grids or personal use. There is a rise in demand for residential rooftop systems from various countries where residents need accessible, affordable, and reliable electricity options. In many countries, the electricity generated from solar PV is more economically attractive than buying electricity from the grid.

- For instance, in the past couple of years, the United States experienced rapid growth in residential rooftop solar installed capacity; according to the Solar Energy Industries Association, the residential rooftop solar PV installed capacity grew by around 40% between 2021 and 2022. In 2022, the annual installed capacity was 5.9 GW compared to 4.2 GW in 2021.

- Further, In 2022, the average cost of residential solar systems in the United States stood at USD 3.21 per watt. Although the price of residential solar has slightly increased in the last three years, it is still less than half the average cost registered in 2010. The decrease in the cost of residential solar systems has contributed to the significant increase in the solar capacity installed in United States households across the country.

- The European Union is actively promoting the domestic production of solar panels, exemplified by initiatives such as Enel Green Power's collaboration with the European Union to expand a solar panel Gigafactory located in Italy. Supported by European Union funding, Enel Green Power aims to increase its production capacity by a significant factor, specifically fifteen-fold, from the existing 200 MW to a substantial 3 GW. Anticipated to be operational by July 2024, this production facility represents a considerable investment totaling approximately USD 630 million, with an expected contribution from the European Union of around USD 124 million. This concerted effort is poised to drive down the cost of rooftop solar panels in the near term and to stimulate heightened demand for residential rooftop solar systems throughout Europe. The need for residential rooftops has increased in countries such as China, India, and Australia in the past couple of years due to government initiatives to promote solar energy projects in the residential sector and reduce installation costs.

- For instance, the Government of India initiated phase II of the Ministry of New and Renewable Energy's (MNRE) grid-connected rooftop solar program. Under this program, in April 2022, the Tamil Nandu Energy Development Agency issued a tender to install 12 MW of grid-connected residential rooftop solar systems in Tamil Nandu. Similarly, Telangana state's Renewable Energy Department Corporation invited bids to appoint suppliers to build 50 MW of grid-connected residential rooftop solar projects.

- Therefore, owing to the above points, the residential rooftop solar PV installation market is expected to dominate during the forecast period.

Asia-Pacific Expected to Dominate the Market

- Rapid urbanization, population growth, and industrialization across Asia-Pacific countries have fueled a substantial rise in electricity consumption. In response, governments and businesses are increasingly turning to rooftop solar PV installations as a viable means to augment energy supply while addressing environmental concerns.

- Moreover, the Asia-Pacific region offers an abundance of sunlight, making it exceptionally conducive to solar energy generation. The favorable climatic conditions and technological advancements in solar panel efficiency ensure optimal energy yield from rooftop installations. This natural advantage bolsters the region's attractiveness and viability of solar PV installations.

- China is home to nearly all the largest solar photovoltaic (PV) manufacturing companies and facilities globally, with almost 70% of the global solar PV manufacturing capacity in China. These companies also dominate other businesses, such as polysilicon, ingot, and wafer-making, which are integral to the solar panel supply chain. This extraordinary control of the global solar PV supply chain puts Chinese manufacturers at a more significant advantage when compared to solar equipment manufacturers from other countries.

- Furthermore, proactive government policies and incentives play a pivotal role in propelling Asia-Pacific to the forefront of the rooftop solar PV market. Governments across the region have implemented robust support mechanisms, including feed-in tariffs, tax credits, and regulatory frameworks that encourage the adoption of rooftop solar PV systems. These incentives reduce the financial burden on consumers and businesses, stimulating rapid market growth.

- In June 2022, the Australian government released new rooftop solar PV regulations. The government committed USD 19.2 million in the 2021-22 budget to reform the SRES (Small-scale Renewable Energy Scheme). The amendment regulations aim to protect consumers better and improve integrity in the rooftop solar sector. The amendments are as follows:

- Streamline reporting requirements for installers, solar retailers, and manufacturers. Allow the Regulator to take a more direct role in setting the conditions for solar PV components eligible for small-scale technology certificates. Such mandates are expected to see a massive rise in rooftop solar PV adoption during the forecast period.

- Therefore, owing to the above points, Asia-Pacific is expected to dominate the rooftop solar PV installation market during the forecast period.

Rooftop Solar Photovoltaic Installation Industry Overview

The rooftop solar installations market is consolidated in nature. Some of the key players in the market (in no particular order) include Titan Solar Power NV Inc, Momentum Solar, Canadian Solar Inc., Elemental Energy Inc., and Semper Solaris Construction Inc, and among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Rooftop Solar Photovoltaic (PV) Installed Market in GW, till 2029

- 4.4 Recent Trends and Developments

- 4.5 Government Policies and Regulations

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.1.1 Declining Solar Panel Costs

- 4.6.1.2 Supportive Government Policies

- 4.6.2 Restraints

- 4.6.2.1 High Upfront Cost

- 4.6.1 Drivers

- 4.7 Supply Chain Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products and Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Location of Deployment

- 5.1.1 Residential

- 5.1.2 Commercial and Industrial

- 5.2 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2029 (for regions only)})

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Asia-Pacific

- 5.2.2.1 China

- 5.2.2.2 India

- 5.2.2.3 Australia

- 5.2.2.4 Japan

- 5.2.2.5 Malaysia

- 5.2.2.6 Thailand

- 5.2.2.7 Indonesia

- 5.2.2.8 Vietnam

- 5.2.2.9 Rest of Asia-Pacific

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Spain

- 5.2.3.4 Italy

- 5.2.3.5 France

- 5.2.3.6 Nordic Countries

- 5.2.3.7 Turkey

- 5.2.3.8 Russia

- 5.2.3.9 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colombia

- 5.2.4.4 Rest of South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 Qatar

- 5.2.5.4 South Africa

- 5.2.5.5 Egypt

- 5.2.5.6 Nigeria

- 5.2.5.7 Rest of Middle-East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Titan Solar Power NV Inc.

- 6.3.2 Momentum Solar

- 6.3.3 Canadian Solar Inc.

- 6.3.4 Elemental Energy Inc.

- 6.3.5 Semper Solaris Construction Inc.

- 6.3.6 Pink Energy

- 6.3.7 ReVision Energy LLC

- 6.3.8 ADT Solar

- 6.3.9 Baker Electric Home Energy

- 6.3.10 Infinity Energy Inc.

- 6.4 Market Ranking/Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 New Technological Advancements and the Development of Perovskite Solar Cells