|

市場調査レポート

商品コード

1690139

インドの屋上ソーラー:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)India Rooftop Solar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドの屋上ソーラー:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 95 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

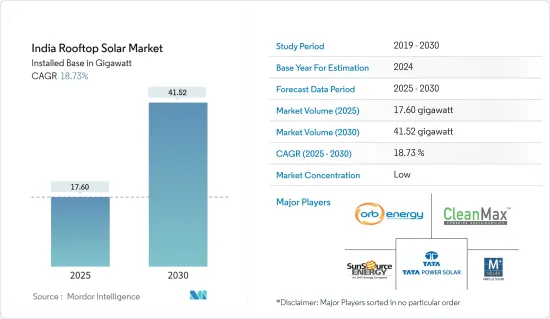

インドの屋上ソーラー市場規模は、設置ベースで2025年の17.60ギガワットから2030年には41.52ギガワットに成長し、予測期間中(2025~2030年)のCAGRは18.73%と予測されます。

主なハイライト

- 長期的には、商業・産業分野での需要増加や再生可能エネルギー統合に対する政府の重視といった要因が市場成長の大きな促進要因になると予想されます。

- その一方で、屋上プロジェクトの設置ペースが遅いことが、今後数年間のインド屋上ソーラー市場の成長を抑制する可能性があります。

- とはいえ、未開拓のソーラーポテンシャルと分散化の進展により、住宅および産業用顧客は中央送電網への依存度を下げることが可能になり、予測期間中の成長機会となることが期待されます。

インドの屋上ソーラー市場動向

オングリッドセグメントが市場を独占する見込み

- オングリッド屋根上システムでは、太陽光発電パネルやアレイがパワーインバーターユニットを介して電力会社の送電網に接続され、電力会社の送電網と並行して稼働します。消費者が発電した電力は、ネットメータリング方式によって中央送電網に供給されます。このような接続は、電気料金を削減するために、商業用、工業用、住宅用の消費者が一般的に利用しています。

- インドでは、政府の様々な政策や取り組みにより、系統連系型太陽光発電システムが近年大きく成長しています。これは、2030年の再生可能エネルギー国家目標達成を後押しするものと思われます。

- インドでは、州政府および中央政府による太陽光発電の屋上設置を促進するため、Grid Connected Solar Rooftop Schemeが導入されました。インドでは、2026年3月末までに系統連系屋上ソーラープロジェクトの累積設備容量約4万メガワットの達成を目指しています。

- 例えば、新・再生可能エネルギー省は、設定された目標を達成するため、2019年3月に屋上ソーラー・プログラム・フェーズIIスキームを開始しました。このスキームの下で、同省は消費者に対し、個人世帯または住民福祉協会/グループ住宅協会に屋上ソーラー(RTS)を設置するための中央資金援助(CFA)を提供する予定です。

- 2023年9月、消費者がRTSを設置するためのオンライン手続きを容易にするため、全国ポータルが開設されました。全国どの地域の住宅消費者も、屋上ソーラーパネルの設置を申請し、補助金を直接銀行口座に受け取ることができます。

- 新・再生可能エネルギー省(MNRE)によると、2023年から2024年の間に系統に接続された屋上ソーラーの累積設備容量は11.8GWに達し、2022年から2023年の8.9GWから33.86%増加しました。2023年中に複数の大規模太陽光発電プロジェクトが稼働し、送電網に接続されたことが、設置容量急増の主な要因となりました。

- グジャラート州、マハラシュトラ州、カルナータカ州は、送電網上の屋上ソーラー設備容量が最も多い州です。2024年3月までの発電量は、グジャラート州が345万kW、カルナータカ州が790万kW、ラジャスタン州が115万kWでした。

- 全体として、発電のための屋上ソーラーの採用が増加していること、支援政策、スキーム、野心的な再生可能エネルギー目標という形で政府の支援があることなどの要因から、予測期間中、インドの屋上ソーラー市場ではオングリッド部門が大きく成長すると予想されます。

再生可能エネルギー統合を重視する政府が市場を牽引する見通し

- 新・再生可能エネルギー省(MNRE)によると、インドは太陽光発電の導入において世界第5位の地位を確保しています。2023年6月30日現在、インドでは合計7,010万kWの太陽光発電プロジェクトが稼働しています。この容量は、地上設置型ソーラー・プロジェクトが5,722万kW、屋上設置型ソーラー・プロジェクトが1,037万kW、オフグリッド・ソーラー・プロジェクトが251万kWです。

- 2023年3月時点で、屋上ソーラー容量は8,877MWに増加した(2022年9月30日時点では7,520MW)。この成長の主な要因は、住宅消費者の意識の高まりと、住宅分野を対象とした政府の補助金です。

- 政府は、屋上ソーラーの導入を支援するための包括的な政策と政策を策定しました。政府はいくつかのネットメータリング・イニシアチブを実施し、屋上ソーラーの利用者が発電した余剰電力を送電網に売電できるようにし、経済的なメリットを提供するとともに送電網の安定を促進しました。

- 例えば、2024年3月、ラジャスタン電力規制委員会(RERC)は、屋上ソーラー設備のネットメータリングの上限を500kWから1MWに引き上げました。同委員会の決定は、ネットメータリング容量を拡大することで、屋上ソーラー設備の導入を促進することを目的としており、特別命令によって下されました。

- さらに2023年11月、タミル・ナードゥ電力規制委員会(TNERC)は、MSME部門の屋上ソーラーの消費者に対してネットワーク料金の50%を免除するという州政府の指示を支持する新たな命令を出しました。

- 2023年3月の時点で、MNREは2023年1月までの目標357.9MWに対して約40.4MWの屋上ソーラー容量が設置されたと発表しました。

- 2023年8月、マハラシュトラ電力規制委員会は、太陽光屋根上プロジェクトのネットメータリングの上限を1MWに引き上げる規制改正を提案しました。インドのほとんどの州では、MNREが義務付けている屋上ソーラー所のネットメータリング適用量は500kW程度でした。今回の改正案が承認されれば、大口消費者による屋上ソーラープロジェクトの導入が増えるかもしれないです。これはインドの屋上ソーラー市場の開拓にプラスになるかもしれないです。

- このような政府のインセンティブには通常、補助金、税額控除、助成金、融資制度、グリーンクレジットの追加などがあります。インド政府は、住宅用、商業用、産業用(C&I)太陽光発電システムに対して、財政的に魅力的な新たな優遇制度を展開しています。これが予測期間中の市場を牽引することになろう。

インド屋上ソーラー産業の概要

インドの屋上ソーラー市場は細分化されています。この市場の主要企業には、Clean Max Enviro Energy Solutions Pvt. Ltd、Tata Power Solar Systems Limited、Orb Energy Pvt. Ltd、Amplus Solar Power Private Limited、Sunsource Energy Pvt. Ltdなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 再生可能エネルギー統合に向けた政府の重視

- 商業・産業部門における需要の増加

- 抑制要因

- 屋上プロジェクトの設置ペースの遅れ

- 促進要因

- サプライチェーン分析

- PESTLE分析

第5章 市場セグメンテーション

- エンドユーザー

- 産業

- 商業(公共部門を含む)

- 住宅

- グリッドタイプ(定性分析のみ)

- オングリッド

- オフグリッド

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Cleantech Energy Corporation Pte Ltd

- Fourth Partner Energy Pvt. Ltd

- Amplus Solar Power Pvt. Ltd

- Clean Max Enviro Energy Solutions Pvt. Ltd

- Sunsource Energy Pvt. Ltd

- Orb Energy Pvt. Ltd.

- Tata Power Solar Systems Limited

- Mahindra Susten Pvt. Ltd

- Growatt New Energy Technology Co. Ltd

- Roofsol Energy Pvt. Ltd

- 市場ランキング分析

第7章 市場機会と今後の動向

- 未開拓のソーラーポテンシャルと分散化拡大への注力

目次

Product Code: 70202

The India Rooftop Solar Market size in terms of installed base is expected to grow from 17.60 gigawatt in 2025 to 41.52 gigawatt by 2030, at a CAGR of 18.73% during the forecast period (2025-2030).

Key Highlights

- Over the long term, factors such as increasing demand in the commercial and industrial sectors and government emphasis on renewable energy integration are expected to be significant drivers for the market's growth.

- On the other hand, slow-paced installation of rooftop projects may likely restrain the growth of the Indian rooftop solar market over the coming years.

- Nevertheless, the untapped solar potential and focus on increasing decentralization would enable residential and industrial customers to rely less on central grids, which is expected to be a growth opportunity during the forecast period.

India Rooftop Solar Market Trends

The On-grid Segment is Expected to Dominate the Market

- In the on-grid rooftop system, photovoltaic panels or arrays are connected to the utility grid through a power inverter unit, allowing them to operate in parallel with the electric utility grid. The electricity generated by consumers is fed into the central power grid through a net-metering scheme. Such kind of connection is commonly used by commercial, industrial, and residential consumers to reduce electricity bills.

- In India, on-grid or grid-connected solar PV systems have witnessed significant growth in recent years owing to the various government policies and initiatives. This is likely to support the country in achieving its 2030 national renewable energy target.

- The country introduced the Grid Connected Solar Rooftop Scheme to promote solar rooftop installation by the state and central government. India aims to achieve a cumulative installed capacity of about 40,000 MW from Grid Connected Rooftop solar projects by the end of March 2026.

- For instance, the Ministry of New and Renewable Energy launched the Rooftop Solar Programme Phase-II scheme in March 2019 to reach the set targets. Under the scheme, the ministry is expected to provide consumers with Central Financial Assistance (CFA) for installing Rooftop Solar (RTS) in individual households or Resident Welfare Associations/Group Housing Societies.

- In September 2023, the National Portal was launched to ease the online process for consumers to install RTS. Residential consumers from any part of the country are eligible to apply for the installation of rooftop solar panels and receive a subsidy directly in their bank accounts.

- According to the Ministry of New and Renewable Energy (MNRE), during the 2023-2024 period, the cumulative solar rooftop installed capacity connected to the grid reached 11.8 GW, representing an increase of 33.86% from 8.9 GW in the 2022-2023 period. Several large-scale solar energy projects were operational and connected to the grid during 2023, which was majorly responsible for the sharp increase in the installed capacity.

- Gujarat, Maharashtra, and Karnataka are the states with the highest on-grid rooftop solar PV installed capacity. Until March 2024, Gujarat generated 3.45 GW, while Karnataka and Rajasthan generated around 7.9 GW and 1.15 GW, respectively.

- Overall, factors including the increasing adoption of rooftop solar energy for power generation, government support in the form of supportive policies, schemes, and ambitious renewable targets are expected to witness significant growth of the on-grid segment in the Indian solar rooftop market during the forecast period.

Government Emphasis on Renewable Energy Integration is Expected to Drive the Market

- According to the Ministry of New and Renewable Energy (MNRE), India secured the fifth position globally in the deployment of solar power. As of June 30, 2023, the country commissioned solar projects with a total capacity of 70.10 GW. This capacity comprised 57.22 GW from ground-mounted solar projects, 10.37 GW from rooftop solar projects, and 2.51 GW from off-grid solar projects.

- As of March 2023, the rooftop solar capacity increased to 8,877 MW, compared to 7,520 MW as of September 30, 2022. The primary factors attributed to this growth included heightened awareness among residential consumers and government subsidies targeted toward the residential segment.

- The government has formulated comprehensive policies and regulations to support rooftop solar deployment. The government took several net metering initiatives, which allow rooftop solar users to sell excess electricity generated back to the grid, providing financial benefits and promoting grid stability.

- For instance, in March 2024, the Rajasthan Electricity Regulatory Commission (RERC) raised the limit for net metering from 500 kW to 1 MW for rooftop solar installations. The Commission's decision, made through a suo motu order, aims to promote the adoption of rooftop solar installations by expanding the net metering capacity.

- Further, in November 2023, the Tamil Nadu Electricity Regulatory Commission (TNERC) issued a new order endorsing the state government's directive to exempt 50% of network charges for rooftop solar consumers in the MSME sector.

- As of March 2023, the MNRE quoted that about 404 MW of rooftop solar capacity was installed against the target of 357.9 MW up to January 2023, a decline from 678 MW since the previous financial year.

- In August 2023, the Maharashtra Electricity Regulatory Commission proposed amendments in regulations to increase the capping of net metering to 1 MW for solar rooftop projects. The net-metering applicability stood around 500 kW for rooftop solar plants in most Indian states as mandated by MNRE. The approval of proposed amendments might lead to an increase in the adoption of rooftop solar projects by large consumers. This might benefit the development of the solar rooftop market in India.

- These government incentives usually include subsidies, tax credits, grants and loan programs, and additional green credits. The Indian government is rolling out new fiscally attractive incentive schemes for residential, commercial, and industrial (C&I) solar PV systems. This will likely drive the market during the forecast period.

India Rooftop Solar Industry Overview

The Indian rooftop solar market is fragmented. Some key players in this market include Clean Max Enviro Energy Solutions Pvt. Ltd, Tata Power Solar Systems Limited, Orb Energy Pvt. Ltd, Amplus Solar Power Private Limited, and Sunsource Energy Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Government Emphasis Towards Renewable Energy Integration

- 4.5.1.2 Increasing Demand in the Commercial and Industrial Sector

- 4.5.2 Restraints

- 4.5.2.1 Slow-Paced Installation of Rooftop Projects

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

5 MARKET SEGMENTATION

- 5.1 End-user

- 5.1.1 Industrial

- 5.1.2 Commercial (Including Public Sector)

- 5.1.3 Residential

- 5.2 Grid Type (Qualitative Analysis Only)

- 5.2.1 On-grid

- 5.2.2 Off-grid

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Cleantech Energy Corporation Pte Ltd

- 6.3.2 Fourth Partner Energy Pvt. Ltd

- 6.3.3 Amplus Solar Power Pvt. Ltd

- 6.3.4 Clean Max Enviro Energy Solutions Pvt. Ltd

- 6.3.5 Sunsource Energy Pvt. Ltd

- 6.3.6 Orb Energy Pvt. Ltd.

- 6.3.7 Tata Power Solar Systems Limited

- 6.3.8 Mahindra Susten Pvt. Ltd

- 6.3.9 Growatt New Energy Technology Co. Ltd

- 6.3.10 Roofsol Energy Pvt. Ltd

- 6.4 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Untapped Solar Potential and Focus to Increase Decentralization