|

市場調査レポート

商品コード

1687776

インドのエポキシ樹脂:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)India Epoxy Resins - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドのエポキシ樹脂:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

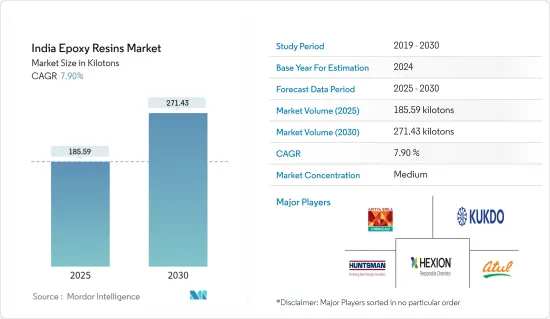

インドのエポキシ樹脂市場規模は2025年に185.59キロトンと推定され、予測期間(2025年~2030年)のCAGRは7.9%で、2030年には271.43キロトンに達すると予測されます。

COVID-19によるパンデミック期には、全国的な封鎖、厳しい社会的距離の義務付け、サプライチェーンの混乱により、市場は大きな影響を受けました。このため、エポキシ樹脂が必要とされる塗料やコーティング剤、接着剤、シーリング剤などのさまざまな製品の生産と製造が一時的に停止しました。しかし、パンデミック後の様々な製造業に対する政府の支援により、市場の成長は加速しています。

主なハイライト

- 建設産業の成長と自動車産業からの接着剤・シーラント需要の増加が市場成長の要因です。

- 反面、エポキシ樹脂の有害性が市場成長の妨げになると予想されます。

- リサイクル可能で改質可能なエポキシ樹脂の採用が増加していることは、予測期間において市場の好機となると思われます。

インドのエポキシ樹脂市場動向

DGBEA(ビスフェノールFとECH)の需要増加

- ビスフェノールA-エピクロロヒドリンをベースとするエポキシ樹脂は、依然として最も広く使用されているエポキシ樹脂です。エポキシ樹脂は、活性水素基を含む化合物をエピクロロヒドリンと反応させ、次いでデヒドロハロゲン化することによって調製されます。

- ビスフェノールAのジグリシジルエーテル(DGEBA)をベースとするエポキシ樹脂は、接着剤、コーティング剤、積層板、封止剤などの配合に最も一般的に使用されています。

- 現在、世界中のエポキシ樹脂材料のおよそ90%がビスフェノールAのジグリシジルエーテル(DGEBA)から作られています。この樹脂は、優れた機械的特性、耐薬品性、形状安定性などのユニークな特徴を備えています。

- ポリカーボネートとエポキシ樹脂は、BPFから派生した主要製品です。これらのエポキシ樹脂はDGEBAと同じ方法で製造されます。DGEBF(ビスフェノールF)エポキシ樹脂はDGEBAエポキシ樹脂よりも粘度が低く、機械的・化学的特性が優れています。

- ビスフェノールF型エポキシ樹脂は、コーティング、土木、接着剤、電気絶縁材料、反応中間体など幅広い用途に使用されています。特に液状樹脂は粘度が低いため、作業性や成形性に優れ、多くの用途に適しています。

市場を独占する塗料・コーティング剤セグメント

- インドのエポキシ樹脂業界では、建築、自動車、エネルギー、電子産業で広く使用されていることから、塗料・コーティング分野が最も急成長すると予想されています。

- エポキシ樹脂は、床や金属用途のコーティングの耐久性を高めるため、コーティング用途のバインダーとして使用されます。

- インドは製造業や機械産業が急成長している国のひとつであり、塗料やコーティング剤のニーズが高まっています。政府は、国内に製造部門を設置する企業に対してさまざまな便宜を図り、製造部門を後押しするためにさまざまな政策を打ち出しています。例えば、インドは2021年8月に製造品輸出額1兆米ドルという目標を達成するための計画の概要を発表しました。

- インドの塗料産業の売上高は約67億833万米ドルと推定されています。国内最大手のAsian Paintsは国内で10の生産施設を運営し、Berger paintsは12の生産施設を使用しています。

- OICAによると、2021年の自動車生産台数は約4,399万1,112台で、2020年の3,381万1,819台に比べ30%増加しました。

- 乗用車(BMW、メルセデス、タタ・モーターズ、ボルボ・オートを除く)、三輪車、二輪車、四輪車の自動車生産台数は、2021年10月までに221万4,745台となりました。

- IBEFによると、インド政府は自動車部門が国内外からの投資によって2023年までに80億~100億米ドルを生み出すと見込んでいます。

- このような要因によって、塗料やコーティングにおけるエポキシ樹脂の需要が促進され、予測期間中の市場の成長が高まると予想されます。

インドのエポキシ樹脂産業概要

インドのエポキシ樹脂市場は部分的に断片化されており、市場には様々な企業が存在しています。インドのエポキシ樹脂市場における主要企業(順不同)には、Aditya Birla Chemicals、Atul Ltd.、KUKDO CHEMICAL、Hexion、Huntsman International LLCなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 建設業界の力強い成長

- 自動車産業における接着剤とシーラントの需要増加

- 抑制要因

- エポキシ樹脂の危険な影響

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 原材料

- DGBEA(ビスフェノールAとECH)

- DGBEF(ビスフェノールFとECH)

- ノボラック(ホルムアルデヒドとフェノール類)

- 脂肪族(脂肪族アルコール)

- グリシジルアミン(芳香族アミン及びECH)

- その他の原材料

- 用途

- 塗料およびコーティング剤

- 接着剤およびシーラント

- 複合材料

- 電気・電子

- その他の用途

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場ランキング分析

- 主要企業の戦略

- 企業プロファイル(概要、財務、製品・サービス、最近の動向)

- 3M

- Aditya Birla Chemicals

- Atul Ltd

- BASF SE

- Daicel Corporation

- DuPont

- KUKDO CHEMICAL CO., LTD.

- Huntsman International LLC

- MACRO POLYMERS Pvt Ltd

- NAN YA PLASTICS CORPORATION

- Olin Corporation

- Westlake Corporation(Hexion)

第7章 市場機会と今後の動向

- リサイクル・改質可能なエポキシ樹脂の採用拡大

The India Epoxy Resins Market size is estimated at 185.59 kilotons in 2025, and is expected to reach 271.43 kilotons by 2030, at a CAGR of 7.9% during the forecast period (2025-2030).

During the pandemic period due to COVID-19, the market was deeply impacted because of nationwide lockdown, stringent social distancing mandates, and supply chain disruptions. This led to a temporary halt in the production and manufacturing of different products such as paints and coatings, adhesives and sealants, etc., in which epoxy resins are required. However, the market's growth is picking pace because of the government's support to various manufacturing industries in the post-pandemic period.

Key Highlights

- The growing construction industry and increasing demand for adhesives and sealants from the automotive industry are the factors driving the market growth.

- On the flip side, the hazardous impact of epoxy resins is expected to hinder the growth of the market.

- The growing adoption of recyclable and reformable epoxy resin will act as a market oppurtunity in the forecast period.

Epoxy Resin in India Market Trends

Increasing Demand for DGBEA (Bisphenol F and ECH)

- Epoxy resins based on bisphenol A-epichlorohydrin are still the most widely used epoxies. Epoxy resins are prepared by reacting compounds containing an active hydrogen group with epichlorohydrin, followed by dehydrohalogenation.

- Epoxy resins based on the diglycidylether of bisphenol A (DGEBA) are most commonly used in formulations for adhesives, coatings, laminates, and encapsulants.

- Nowadays, roughly 90% of epoxy resin materials worldwide are made from diglycidyl ether of bisphenol A (DGEBA). This resin offers unique features such as outstanding mechanical properties, chemical resistance, and shape stability.

- Polycarbonates and epoxy resins are the primary products derived from BPF. These epoxy resins are produced using the same method as performed for DGEBA. The DGEBF (Bisphenol F) epoxy resins have lower viscosity and better mechanical and chemical properties than the DGEBA ones.

- Bisphenol F epoxy resins are used in broad applications, including coatings, civil engineering, adhesives, electrical insulating materials, and reactive intermediates. In particular, the liquid resins have low viscosity, so they excel in workability and moldability, which makes them suited to many applications.

Paints and Coatings Segment to Dominate the Market

- The paints and coatings segment is expected to grow the fastest in the Indian epoxy resin industry, owing to its widespread use in the building, automotive, energy, and electronic industries.

- Epoxy resins are used as binders for coating applications to enhance the durability of coating for floor and metal applications.

- India is one of the fastest-growing countries in manufacturing sectors and machinery growth, giving rise to the need for paints and coatings. The government is providing various benefits to the companies setting their manufacturing units in the country and framing various policies to boost the manufacturing sector. For instance, India outlined a plan in August 2021 to reach its goal of USD 1 trillion in manufactured goods exports.

- The Indian paint industry is estimated to have a turnover of around USD 6708.33 million. Asian Paints, the largest domestic player in the market, operates ten production facilities in the country, while Berger paints use 12 production facilities.

- According to the OICA, around 43,99,112 units of vehicles were produced in 2021, which increased by 30% in comparison to 33,81,819 units manufactured in 2020.

- Automotive production for passenger vehicles (except for BMW, Mercedes, Tata Motors & Volvo Auto), three-wheelers, two-wheelers, and quadricycles witnessed 2,214,745 units by October 2021.

- According to the IBEF, the government of India expects the automobile sector to generate USD 8-10 billion by 2023 through local and foreign investment.

- Such factors are expected to drive the demand for epoxy resins in paints and coatings, thus increasing the market's growth during the forecast period.

Epoxy Resin in India Industry Overview

The Indian epoxy resins market is partially fragmented, with the presence of various players in the market. A few major companies in India's epoxy resins market (not in a particular order) include Aditya Birla Chemicals, Atul Ltd., KUKDO CHEMICAL Co. Ltd, Hexion, and Huntsman International LLC, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Strong Growth in the Construction Industry

- 4.1.2 Increasing Demand of Adhesives and Sealants in Automotive Industry

- 4.2 Restraints

- 4.2.1 Hazardous Impact of Epoxy Resins

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Raw Material

- 5.1.1 DGBEA (Bisphenol A and ECH)

- 5.1.2 DGBEF (Bisphenol F and ECH)

- 5.1.3 Novolac (Formaldehyde and Phenols)

- 5.1.4 Aliphatic (Aliphatic Alcohols)

- 5.1.5 Glycidylamine (Aromatic Amines and ECH)

- 5.1.6 Other Raw Materials

- 5.2 Application

- 5.2.1 Paints and Coatings

- 5.2.2 Adhesives and sealants

- 5.2.3 Composites

- 5.2.4 Electrical and Electronics

- 5.2.5 Other Applications

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles (Overview, Financials, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Aditya Birla Chemicals

- 6.4.3 Atul Ltd

- 6.4.4 BASF SE

- 6.4.5 Daicel Corporation

- 6.4.6 DuPont

- 6.4.7 KUKDO CHEMICAL CO., LTD.

- 6.4.8 Huntsman International LLC

- 6.4.9 MACRO POLYMERS Pvt Ltd

- 6.4.10 NAN YA PLASTICS CORPORATION

- 6.4.11 Olin Corporation

- 6.4.12 Westlake Corporation (Hexion)

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Adoption of Recyclable And Reformable Epoxy Resins