|

市場調査レポート

商品コード

1640679

エポキシ樹脂:市場シェア分析、産業動向と統計、成長予測(2025~2030年)Epoxy Resins - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| エポキシ樹脂:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

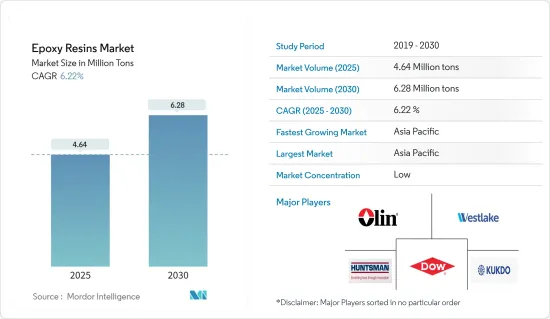

エポキシ樹脂市場規模は2025年に464万トンと推定され、予測期間(2025~2030年)のCAGRは6.22%で、2030年には628万トンに達すると予測されています。

2020年には、COVID-19の大流行と世界各地の厳しい規制がエポキシ樹脂市場に打撃を与えました。塗料・コーティング、接着剤、電気・電子などの産業が課題に直面し、サプライチェーンの混乱、作業停止、労働力不足に悩まされました。しかし、2021年には、塗料・コーティング、接着剤・シーラント、電気・電子セグメントからの需要の急増により、市場は回復しました。

主要ハイライト

- 短期的には、塗料・コーティングセグメントの需要増と電気・電子セグメントの需要増が、調査対象市場の需要を牽引する主要要因です。

- しかし、エポキシ樹脂の使用に関する厳しい規制が市場成長の妨げになると予想されます。

- バイオベースのエポキシ樹脂の開発と技術の進歩は、この市場に新たな機会をもたらすと予想されます。

- アジア太平洋は、中国とインドからの需要が大半を占め、世界の市場を独占すると予想されます。

エポキシ樹脂市場の動向

塗料・コーティングセグメントが市場を独占する見込み

- エポキシ樹脂はコーティング用途のバインダーであり、床や金属に使用されるコーティングの耐久性を強化します。

- これらの樹脂は、強度、耐久性、耐薬品性などの基本的な特性を塗料に付与します。速乾性、強靭性、優れた接着性、効果的な硬化性、耐摩耗性、優れた耐水性により、金属や様々な表面の保護に理想的です。

- 世界塗料・コーティング工業会(WPCIA)によると、世界の塗料・コーティング市場は2023年に1,855億米ドルの評価額を達成し、前年比3.2%増となりました。この上昇の主要要因は、建設、自動車、製造セクターにおける需要の高まりです。

- さらに、WPCIAのデータによると、アジア太平洋は世界最大の塗料・コーティング剤生産国で、2023年の世界生産量の54.7%を占め、次いで欧州(19.6%)、北米(15.6%)、ラテンアメリカ(6.4%)、中東・アフリカ(3.6%)となっています。このように、塗料・コーティング産業の拡大が市場を牽引する可能性が高いです。

- 米国は、世界最大かつ最も技術的に進んだ経済のひとつです。この圧倒的な地位により、同国は塗料・コーティング市場のホットスポットのひとつとなりました。米国は世界でもトップクラスの塗料・コーティング剤生産国で、1,400社以上の製造会社があります。

- 米国塗料協会によると、米国における塗料・コーティング産業の生産量は、2022年には約13億2,000万ガロンでした。さらに、2024年には13億4,000万ガロンを超えると予測されています。PPG、The Sherwin-Williams Company、Axalta Coating Systems、RPM Inc.、Diamond Paintsが米国の主要な塗料・コーティング剤メーカーとサプライヤーです。

- フランスの塗料・コーティング産業は最近の動向で開発が進んでおり、評価期間中にエポキシ樹脂の需要をかき立てることが予想されます。例えば、2023年12月、PPGはフランスのトゥールーズに1,700万米ドルの航空宇宙アプリケーションサポートセンター(ASC)を開設すると発表しました。この施設は、様々な航空機用のコーティング剤やシーラントを含む航空宇宙材料の充填包装機能を提供する予定です。

- こうした力学から、塗料・コーティングセグメントではエポキシ樹脂の需要が高まり、今後数年間の市場成長を牽引すると予想されます。

アジア太平洋が市場を独占する展望

- アジア太平洋が世界のエポキシ樹脂市場をリードする構えです。インド、中国、日本、韓国などの国々は、塗料、コーティング、電気・電子セグメントの急成長を目の当たりにしており、この地域におけるエポキシ樹脂の需要と消費を押し上げています。

- European Coatingsが報告しているように、世界の工業化の拠点である中国は、驚異的な1万社の塗料メーカーを誇っています。特に、Nippon Paint、AkzoNobel、PPG Industriesなどの大手企業が中国に製造拠点を設けています。

- 中国塗料工業協会の統計によると、2023年の中国の塗料生産量は357億7,200万トンに達し、前年比4.5%増となりました。輸出は19.6%増の26万2,000トンと急増し、国内消費は4.2%増の356億6,300万トンと、このセクターの力強い成長を裏付けています。

- メーカー各社は新工場を設立したり、既存設備の能力を増強したりしています。こうした戦略的な動きが塗料・コーティングの需要を押し上げ、市場全体の成長を下支えしています。

- 例えば、2024年1月、Berger Paints Indiaは、オディシャ州の新しいグリーンフィールド複合工場に100億インドルピー(約1億2,060万米ドル)以上を投入する計画を発表しました。この大胆な投資は、近い将来、塗料とコーティング剤の需要を喚起し、研究市場に利益をもたらすと考えられます。

- 中国のエレクトロニクス事情は活気に満ちており、スマートフォンやテレビなどの製品が著しい成長を遂げています。国内の電子機器需要を満たすだけでなく、輸出も盛んで、市場のさらなる拡大に拍車をかけています。

- 中国は世界最大のスマートフォン製造拠点です。中国国家統計局のデータによると、2023年11月、中国では約14億台の携帯電話が生産されました。モバイル製造において確立された実力により、中国の国内市場は世界最大級の規模に浮上しました。

- 新華社通信のデータによると、中国の電子機器製造業は2024年の年初4ヵ月間、生産台数の増加と国内と世界の需要の回復に支えられ、堅調な業績を示しました。工業情報化部の報告によると、2024年1月から4月までの中国のエレクトロニクスセグメントの主要企業の合計利益は前年同期比75.8%増の1,442億人民元(約203億米ドル)に達しました。

- 日本の電子情報技術産業協会のデータによると、2024年1月から6月までの日本のエレクトロニクス産業全体の生産額は5,452億5,600万円(約33億8,600万米ドル)で、前年同期比104.7%の成長率を記録しました。

- このような動きの中で、アジア太平洋は予測期間中にエポキシ樹脂の需要が急増する可能性があります。

エポキシ樹脂産業概要

エポキシ樹脂市場は細分化されています。主要企業(順不同)には、Olin Corporation、Huntsman International LLC、Dow、Kukdo Chemical、Westlake Corporationが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 塗料・コーティングセグメントからの需要増加

- 電気・電子セグメントからの需要増加

- その他の促進要因

- 抑制要因

- エポキシ樹脂の使用に関する厳しい規制

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(市場規模(数量ベース))

- 原料別

- DGBEA(ビスフェノールAとECH)

- DGBEF(ビスフェノールFとECH)

- ノボラック(ホルムアルデヒドとフェノール類)

- 脂肪族(脂肪族アルコール)

- グリシジルアミン(芳香族アミン及びECH)

- その他の原料

- 用途別

- 塗料とコーティング剤

- 接着剤とシーラント

- 複合材料

- 電気・電子

- 海洋

- 風力タービン

- その他

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- カタール

- アラブ首長国連邦

- ナイジェリア

- エジプト

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- 3M

- Aditya Birla Chemicals

- Atul Ltd

- BASF SE

- Chang Chun Group

- DIC Corporation

- Dow

- Huntsman International LLC

- Jiangsu Sanmu Group

- Kukdo Chemical Co. Ltd

- NAMA Chemicals

- Nan Ya Plastics Corporation

- Olin Corporation

- Robnor ResinLab

- Sika AG

- Sinochem Internation Corporation

- SPOLCHEMIE

- Westlake Corporation

第7章 市場機会と今後の動向

- バイオベースエポキシ樹脂の開発

- 成長機会を生み出す技術の進歩

- その他の機会

The Epoxy Resins Market size is estimated at 4.64 million tons in 2025, and is expected to reach 6.28 million tons by 2030, at a CAGR of 6.22% during the forecast period (2025-2030).

In 2020, the COVID-19 pandemic and stringent regulations across the globe took a toll on the epoxy resin market. Industries like paints and coatings, adhesives, and electrical and electronics faced challenges, grappling with supply chain disruptions, work stoppages, and labor shortages. However, in 2021, the market rebounded, driven by a surge in demand from the paints and coatings, adhesives and sealants, and electrical and electronics sectors.

Key Highlights

- Over the short term, the increasing demand from the paints and coatings sector and rising demand from electrical and electronics are the major factors driving the demand for the market studied.

- However, stringent regulations regarding the use of epoxy resin are expected to hinder the market's growth.

- Nevertheless, the development of bio-based epoxy resins and technological advancements are anticipated to create new opportunities for the market studied.

- Asia-Pacific is expected to dominate the market across the world, with the majority of demand coming from China and India.

Epoxy Resins Market Trends

Paints and Coatings Segment is Expected to Dominate the Market

- Epoxy resins are binders in coating applications, bolstering the durability of coatings used on floors and metals.

- These resins impart fundamental properties to coatings, including strength, durability, and chemical resistance. Their quick-drying nature, toughness, excellent adhesion, effective curing, abrasion resistance, and superior water resistivity make them ideal for safeguarding metals and various surfaces.

- According to the Worlds Paint and Coatings Industry Association (WPCIA), the global paint and coatings market achieved a valuation of USD 185.5 billion in 2023, marking a 3.2% increase from the prior year. This uptick was primarily fueled by heightened demand across the construction, automotive, and manufacturing sectors.

- Furthermore, the Asia-Pacific region is the largest producer of paint and coatings globally, accounting for 54.7% of global production in 2023, followed by Europe (19.6%), North America (15.6%), Latin America (6.4%), and the Middle East & Africa region (3.6%) as per the data from WPCIA. Thus, expansion in the paints and coatings industry is likely to drive the market.

- The United States represents one of the largest and most technologically advanced economies globally. This dominant position enabled the country to become one of the hotspots for the paints and coatings market. It is one of the top global paints and coatings producers, with more than 1,400 manufacturing companies.

- According to the American Coatings Association, the paint and coatings industry's production volume in the United States was approximately 1.32 billion gallons in 2022. Moreover, the industry's production is forecast to surpass 1.34 billion gallons in 2024. PPG, The Sherwin-Williams Company, Axalta Coating Systems, RPM Inc., and Diamond Paints are the major paints and coatings manufacturers and suppliers in the United States.

- The French paints and coating industry has witnessed development in recent years, which is expected to stir up the demand for epoxy resin over the assessment period. For instance, in December 2023, PPG announced the opening of a USD 17 million aerospace application support center (ASC) in Toulouse, France. The facility is set to offer filling and packaging capabilities for aerospace materials, including coatings and sealants for various aircraft.

- Given these dynamics, the paints and coatings sector is expected to see a rising demand for epoxy resins, driving the market's growth in the coming years.

Asia-Pacific Region is Expected to Dominate the Market

- Asia-Pacific is poised to lead the global epoxy resin market. Countries such as India, China, Japan, and South Korea are witnessing a surge in their paints, coatings, and electrical & electronics sectors, driving up the demand and consumption of epoxy resin in the region.

- China, a global hub for industrialization, boasts a staggering 10,000 coatings manufacturers, as reported by European Coatings. Notably, major players like Nippon Paint, AkzoNobel, and PPG Industries have established manufacturing bases in the country.

- Figures from the China Coatings Industry Association reveal that in 2023, China's coatings production hit 35,772 million tons, marking a 4.5% increase from the previous year. Exports surged by 19.6% to 262,000 tons, while domestic consumption rose by 4.2% to 35,663 million tons, underlining the sector's robust growth.

- Manufacturers are either setting up new plants or ramping up the capacities of their existing facilities. These strategic moves bolster the demand for paints and coatings and underpin the overall market growth.

- For instance, in January 2024, Berger Paints India announced plans to inject over INR 1,000 crore (~ USD 120.6 million) into a new greenfield composite plant in Odisha, focusing on decorative and industrial paints. This bold investment is poised to catalyze the demand for paints and coatings in the near future, thus benefiting the market studied.

- China's electronics landscape is vibrant, with products like smartphones and TVs witnessing significant growth. Not only does the nation cater to its domestic electronics appetite, but it also exports extensively, fueling further market expansion.

- China is the largest smartphone manufacturing base in the world. As per the National Bureau of Statistics of China data, in November 2023, the country produced nearly 1.4 billion cell phones. With its established prowess in mobile manufacturing, China's domestic market has emerged as one of the largest globally.

- As per the data from Xinhua News Agency, China's electronics manufacturing industry showcased robust performance in the initial four months of 2024, buoyed by rising production and a rebound in domestic and global demand. As reported by the Ministry of Industry and Information Technology, major companies in China's electronics sector saw their combined profits surge by 75.8% year-on-year, reaching CNY 144.2 billion (~USD 20.3 billion) from January to April 2024.

- The overall electronics production by the Japanese electronics industry was JPY 5,452,56 million (~USD 3,386 million) from January to June 2024, registering a growth rate of 104.7% compared to the previous year at the same period, as per the data from Japan's Electronics and Information Technology Industries Association.

- Given these dynamics, the Asia-Pacific region is poised for a surge in epoxy resin demand during the forecast period.

Epoxy Resins Industry Overview

The epoxy resin market is fragmented in nature. The major players (not in any particular order) include Olin Corporation, Huntsman International LLC, Dow, Kukdo Chemical Co. Ltd., and Westlake Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from Paints and Coatings Sector

- 4.1.2 Rising Demand from Electrical and Electronics

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Regulations Regarding the Use of Epoxy Resin

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 By Raw Material

- 5.1.1 DGBEA (Bisphenol A and ECH)

- 5.1.2 DGBEF (Bisphenol F and ECH)

- 5.1.3 Novolac (Formaldehyde and Phenols)

- 5.1.4 Aliphatic (Aliphatic Alcohols)

- 5.1.5 Glycidylamine (Aromatic Amines and ECH)

- 5.1.6 Other Raw Materials

- 5.2 By Application

- 5.2.1 Paints and Coatings

- 5.2.2 Adhesives and Sealants

- 5.2.3 Composites

- 5.2.4 Electrical and Electronics

- 5.2.5 Marine

- 5.2.6 Wind Turbines

- 5.2.7 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East & Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Aditya Birla Chemicals

- 6.4.3 Atul Ltd

- 6.4.4 BASF SE

- 6.4.5 Chang Chun Group

- 6.4.6 DIC Corporation

- 6.4.7 Dow

- 6.4.8 Huntsman International LLC

- 6.4.9 Jiangsu Sanmu Group

- 6.4.10 Kukdo Chemical Co. Ltd

- 6.4.11 NAMA Chemicals

- 6.4.12 Nan Ya Plastics Corporation

- 6.4.13 Olin Corporation

- 6.4.14 Robnor ResinLab

- 6.4.15 Sika AG

- 6.4.16 Sinochem Internation Corporation

- 6.4.17 SPOLCHEMIE

- 6.4.18 Westlake Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Bio-based Epoxy Resins

- 7.2 Technological Advancement to Create Growth Opportunities

- 7.3 Other Opportunities