|

|

市場調査レポート

商品コード

1687470

RF GaN-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)RF GaN - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| RF GaN-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 127 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

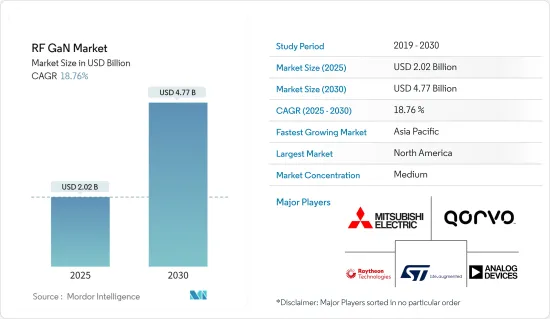

RF GaN市場規模は2025年に20億2,000万米ドルと推計され、2030年には47億7,000万米ドルに達すると予測され、市場推計・予測期間(2025年~2030年)のCAGRは18.76%です。

幅広いリアルタイム連動デバイスやアプリケーションでのRF GaN利用の利点により、モノのインターネット(IoT)技術を利用する産業が増えると予想され、市場成長の原動力となることが期待されます。GaN技術の継続的な進化により、GaNはフェーズドアレイ、レーダー、ケーブルテレビ(CATV)、超小型開口ターミナル(VSAT)、防衛通信のベーストランシーバー局など、より複雑なアプリケーションでより高い周波数を可能にします。

主なハイライト

- RF GaNはワイヤレスインフラで重要な役割を果たし、効率を向上させ、帯域幅を拡大することで、増え続けるデータトランスミッションをサポートしています。RF GaN市場は、主に5Gの採用拡大と無線通信の進歩によって牽引されます。電気通信事業者も、GaNパワートランジスタの使用増加から恩恵を受ける可能性があります。

- 電気自動車へのRF GaNの採用が増加していることも、この市場の需要を促進する主な要因の1つです。炭化ケイ素デバイスは、電気バス、タクシー、貨物車、乗用車の車載バッテリー充電器に使用されています。さらに、電気自動車市場を支持する政府の法律が増加していることも、RF GaN市場の需要を刺激しています。

- 自律走行車やドローンの開発に必要なインフラも、RF GaN技術の需要を高める要因の1つです。従って、様々な用途、特に軍事・防衛用途での自律走行車やドローンの採用・開発の増加は、予測期間中にRF GaNデバイスの採用をさらに増加させると予想されます。

- GaN固有の材料的な利点は、デバイス加工とパッケージングのコストと最適化を含む、いくつかの関連する製造上の課題を伴います。その他の問題には、電荷トラッピングや電流コラプスがあり、これらのデバイスの採用を増やすためには解決する必要があります。RF用GaNベースのデバイス(性能と歩留まり)は大幅に改善されましたが、GaN-on-SiC(炭化ケイ素上の窒化ガリウム)が主流アプリケーション(i.e.無線通信基地局やCATV)に参入するのを阻む障壁がまだいくつかあります。

- COVID-19の大流行は、供給ラインと電気通信業界に影響を与えました。COVID-19の大流行は、供給ラインと通信業界に影響を及ぼし、通信分野における5Gの普及を大幅に妨げました。この危機的な状況下でも、消費者は携帯電話を使い続けると予想されるが、その大半は、まだ黎明期にある技術にこれ以上の投資はできないかもしれないです。

- データ消費の急激な増加は商用ネットワークの成長をもたらし、ネットワーク・プロバイダーに4Gや5Gといった次世代ネットワークの採用を促しています。Cisco Visual Networking Indexによると、世界のモバイル・データ・トラフィックはCAGR46%を記録し、2022年には月間77.5エクサバイトに達すると予想されています。

- 世界中の組織が新製品を革新し、ビジネスを拡大しています。例えば、2022年6月、革新的なRFおよびマイクロ波パワー・ソリューションのプロバイダーであるIntegra社は、画期的な100V RF GaN技術を米国と欧州の顧客に出荷開始したと発表しました。同社はまた、航空電子工学、指向性エネルギー、電子戦、レーダー、科学市場セグメント向けに、単一トランジスタで最大5kWの電力レベルを実現する7つの新製品を発売し、100V RF GaN製品ポートフォリオを拡大すると発表しました。

高周波窒化ガリウムの市場動向

5G実装の進展に牽引される通信インフラ分野からの強い需要

- 世界のデジタル化の主要な促進要因であり、市場環境の包括的な変化下にある業界として、通信業界はデジタル変革技術の主要ユーザーとみなされています。通信業界の相互運用性とテクノロジーへの投資は、世界経済全体の資本と情報の流れにおけるパラダイムシフトを促進し、業界全体で全く新しいビジネスモデルの出現のためのビルディングブロックを提供しています。

- 5G技術は、さまざまなブロードバンド・サービスの領域を変革し、さまざまなエンドユーザーの垂直的な接続性を強化すると期待されています。GaNの市場シェアを押し上げる主な要因は、モバイル契約の増加、オンライン・ビデオ・コンテンツのストリーミング、5Gインフラ、5Gを利用したさまざまなIoTアプリケーションです。5Gは、複数のシナリオにわたってさまざまなサービスと関連するサービス要件をサポートすると予想されています。

- 現在、5Gモバイルの契約数は42万件と評価されており、2022年には4億件に達すると予想されています。5G技術の世界の展開の大幅な増加に伴い、RF GaN技術に対する需要は増加すると予想されます。

- 2022年5月、STマイクロエレクトロニクス(ST)と通信、産業、防衛、データセンター業界向け半導体製品のサプライヤであるMACOM Technology Solutions Holdings(MACOM)は、RF GaN on Silicon(RFガンオンシリコン)試作品の製造を発表しました。今回の成功により、STとMACOMは今後も協力関係を継続し、関係を拡大していきます。STとMACOMが開発中のGaN-on-Si技術は、標準的な半導体プロセス・フローへの統合により、競争力のある性能と大幅な規模の経済性を実現すると期待されています。

- Qorvoは、2G、3G、4G基地局メーカーにRFソリューションを提供するサプライヤーの1つです。Qorvoは、サブ6GHzおよびcmWave/mmWave無線インフラの開発をサポートする市場において、独自の地位を確立しています。Qorvoは、主に5Gを実現するために、3.5、4.8、28、39GHzなど、関連する5Gバンドをカバーする製品ソリューションに投資し、市場にサービスを提供しています。

- 5Gインフラでは高密度で小規模なアンテナアレイが必要とされるため、無線周波数(RF)システムの電力と熱管理に関する重要な課題が生じる。広帯域性能、効率、電力密度が改善されたGaNデバイスは、これらの課題に対処できる、よりコンパクトなソリューションの可能性を提供します。

アジア太平洋地域は大幅な成長が見込まれる

- アジア太平洋地域のディスクリート半導体産業は、中国、日本、台湾、韓国が牽引しており、世界のディスクリート半導体市場の約65%を占めています。これとは対照的に、ベトナム、タイ、マレーシア、シンガポールのような他の地域も、この地域の市場支配に貢献しています。

- インド電子・半導体協会によると、インドの半導体部品市場はCAGR 10.1%(2018-2025年)を記録し、2025年には323億5,000万米ドルに達します。同国は世界の研究開発拠点にとって重要な目的地です。そのため、インド政府による進行中の「Make in India」イニシアチブは、半導体市場に大きな投資をもたらすと予想されます。インド政府によるこのようなイニシアチブは、RF GaN市場にテコ入れをもたらすと思われます。

- 2022年2月、GaN集積回路(IC)のプロバイダーであるナビタスセミコンダクターは、China International Capital Corporation Limited(CICC)の投資家会議への参加を発表しました。同社独自のGaNパワーICは、GaNパワーとGaNドライブ、制御、保護を単一のSMTパッケージに統合したものです。このような市場参入企業は、この地域のGaN市場にテコ入れすることになります。

- 5G技術をサポートするインフラ開発に対する投資家の関心が高まっていることから、APAC地域全体のRF GaNに対する需要は増加すると予想されます。例えば、GSMAによると、アジア太平洋の携帯電話事業者は2025年までに4,000億米ドル以上を投じると予想されており、そのうち3,310億米ドルが5G展開に費やされます。

- 中国におけるRF GaN企業の成長は、中国が製造業主導から技術革新主導の経済へと移行する中で、より広範な傾向の一部となっています。中国市場では商用無線通信アプリケーションの需要が爆発的に伸びており、中国企業はすでに次世代通信ネットワークを開発しています。

- さらに2021年12月、インドのIIT Kanpurの研究者は、アルミニウムGaN(AlGaN)高電子移動度トランジスタ(HEMT)の高性能な業界標準モデルを開発しました。このモデルは、ハイパワーRF回路の製造に使用できるシンプルな設計手法を提供します。RF回路には、ワイヤレス・トランスミッションに使用される増幅器やスイッチなどがあり、航空宇宙や防衛用途に有用です。研究者による絶え間ない技術革新が、この地域のRF GaN市場成長の原動力となると思われます。

高周波窒化ガリウム産業概要

RF GaN市場の競争企業間の敵対関係は、以下のような主要企業の存在により高いです。 Raytheon Technologies, STM microelectronics, amongst others. 継続的なイノベーションによって、彼らは他社に対する競争優位性を獲得しています。研究開発、戦略的パートナーシップ、そして合併・買収を通じて、これらの企業は市場で強固な地位を築いてきました。

2022年6月、世界をつなぐ革新的なRFソリューションの著名なプロバイダーであるQorvoは、米国国防総省(DoD)により、国防次官研究技術局(OUSD R&E)のマイクロエレクトロニクスロードマップの一環として、STARRY NITEとしても知られる国産最先端(SOTA)RF GaNプログラム(Advanced Integration Interconnection and Fabrication Growth for Domestic State-of-the-Art(SOTA)RF GaN program)の推進企業に選定されました。このプログラムは、国防総省の先進パッケージング・エコシステムに合わせて、国内のオープンなSOTA RF GaN鋳造を開発し、成熟させることを目的としています。

2022年5月、STマイクロエレクトロニクスと、産業、通信、防衛、およびデータセンター業界向け半導体製品の重要なサプライヤであるMACOM Technology Solutions Holdings Inc.は、RF Gan on Silicon(RFガンオンSi)プロトタイプの製造に成功したと発表しました。この成果により、STとMACOMは引き続き協力し、関係を強化していきます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 技術スナップショット

- COVID-19の業界への影響評価

第5章 市場力学

- 市場促進要因

- 5G実装の進展に牽引される通信インフラ分野からの強い需要

- 高性能、小型フォームファクターなどの有利な特性

- 市場抑制要因

- コストと運用上の課題

第6章 市場セグメンテーション

- 用途別

- 軍事

- 通信インフラ(バックホール、RRH、Massive MIMO、スモールセル)

- 衛星通信

- 有線ブロードバンド

- 商用レーダーおよびアビオニクス

- RFエネルギー

- 材料タイプ別

- GaN-on-Si

- GaN-on-SiC

- その他の材料タイプ(GaN-on-GaN、GaN-on-Diamond)

- 地域別

- 北米

- 欧州

- アジア太平洋

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Aethercomm Inc.

- Analog Devices Inc.

- Wolfspeed Inc.(Cree Inc.)

- Integra Technologies Inc.

- MACOM Technology Solutions Holdings Inc.

- Microsemi Corporation(Microchip Technology Incorporated)

- Mitsubishi Electric Corporation

- NXP Semiconductors NV

- Qorvo Inc.

- STMicroelectronics NV

- Sumitomo Electric Device Innovations Inc.

- HRL Laboratories

- Raytheon Technologies

- Mercury Systems, Inc

第8章 投資分析

第9章 市場機会と今後の動向

The RF GaN Market size is estimated at USD 2.02 billion in 2025, and is expected to reach USD 4.77 billion by 2030, at a CAGR of 18.76% during the forecast period (2025-2030).

Due to the benefits of RF GaN usage across a wide range of real-time linked devices and applications, more industries are expected to use the Internet of Things (IoT) technology, which is expected to drive market growth. With the continuously evolving GaN technology, GaN enables higher frequencies in more complex applications, such as phased arrays, radar, and base transceiver stations for cable TV (CATV), very small aperture terminal (VSAT), and defense communications.

Key Highlights

- RF GaN plays a key role in wireless infrastructure, improving efficiency and expanding bandwidth to support ever-increasing data transmission speeds. The market for RF GaN is primarily driven by increasing 5G adoption and advances in wireless communications. Telecom operators could also benefit from increased use of GaN power transistors.

- The increasing adoption of RF GaN in electric automotive is also one of the major factors driving demand in this market. Silicon carbide devices are used in the onboard battery chargers of electric buses, taxis, lorries, and passenger cars. Further, increasing government laws favoring the electric vehicles market stimulates demand in the RF GaN market.

- The infrastructure needed to create autonomous vehicles and drones is another factor that increases demand for RF GaN technologies. Hence, growth in the adoption and development of autonomous vehicles and drones for various applications, especially military and defense, is expected to increase further the adoption of RF GaN devices over the forecast period.

- The inherent material advantages of GaN come with some associated manufacturing challenges that include the cost and optimization of device processing and packaging. Other issues include charge trapping and current collapse, which need to be resolved for increased adoption of these devices. Although significant improvements have been made in RF GaN-based devices (performance and yields), there are still some barriers preventing the gallium nitride on silicon carbide (GaN-on-SiC) from entering mainstream applications (i.e., in wireless telecom base-stations or CATV).

- The COVID-19 pandemic impacted supply lines and the telecoms industry. It considerably hindered the penetration of 5G in the telecommunications sector. In this critical situation, consumers are expected to continue using mobile phones, but most of them may not be able to invest more in a technology that is still in a nascent stage.

- Rapidly increasing data consumption has resulted in the growth of commercial networks and is encouraging network providers to adopt next-generation networks, such as 4G and 5G. According to the Cisco Visual Networking Index, global mobile data traffic is expected to register a CAGR of 46%, reaching 77.5 exabytes per month by 2022.

- Organizations across the world are innovating new products and expanding their business. For instance, in June 2022, Integra, a provider of innovative RF and microwave power solutions, announced that it had begun shipping its breakthrough 100V RF GaN technology to customers in the United States and Europe. The company also announced the expansion of its 100V RF GaN product portfolio with the launch of seven new products for the avionics, directed energy, electronic warfare, radar, and scientific market segments, delivering power levels of up to 5kW in a single transistor.

Radiofrequency Gallium Nitride Market Trends

Strong Demand from Telecom Infrastructure Segment Driven by Advancements in 5G Implementation

- As a primary driver of global digitization and an industry undergoing comprehensive changes in the market environment, the telecommunications industry is regarded as a major user of digital transformation technologies. The telecommunications industry's investment in interoperability and technology has facilitated a paradigm shift in the flow of capital and information throughout the global economy, providing the building blocks for the emergence of entirely new business models across the industry.

- The 5G technology is expected to revolutionize the domain of various broadband services and empower connectivity across different end-user verticals. The major factors boosting the market share of GaN are increasing mobile subscriptions, streaming of online video content, 5G infrastructure, and various IoT applications using 5G. 5G is anticipated to support different services and associated service requirements across multiple scenarios.

- Currently, the number of 5G mobile subscriptions is valued at 0.42 million, and it is expected to reach 400 million subscriptions by 2022. With the substantial growth in the rollouts of 5G technology globally, the demand for RF GaN technology is expected to increase.

- In May 2022, STMicroelectronics (ST) and MACOM Technology Solutions Holdings (MACOM), a supplier of semiconductor products for the telecommunications, industrial, defense, and data center industries, announced the production of RF GaN on silicon (RF Gan-on-Si) prototypes. With this success, ST and MACOM will continue to work together and expand their relationship. GaN-on-Si technology under development by ST and MACOM is anticipated to offer competitive performance and significant economies of scale enabled by integration into standard semiconductor process flows.

- Qorvo is one of the suppliers of RF solutions to the 2G, 3G, and 4G base station manufacturers. It is uniquely positioned in the market to support the development of sub-6 GHz and cmWave/mmWave wireless infrastructure. Qorvo has been investing in product solutions covering relevant 5G bands, such as 3.5, 4.8 and 28, and 39GHz, to service the market, mainly to enable 5G.

- The need for dense, small-scale antenna arrays in 5G infrastructure results in key challenges with power and thermal management in radio frequency (RF) systems. With their improved wideband performance, efficiency, and power density, GaN devices offer the potential for more compact solutions that can address these challenges.

Asia-Pacific is Expected to Experience Significant Growth

- The Asia-Pacific region's discrete semiconductor industry is driven by China, Japan, Taiwan, and South Korea, constituting around 65% of the global discrete semiconductor market. In contrast, others, like Vietnam, Thailand, Malaysia, and Singapore, contribute to the region's dominance in the market.

- According to the Electronics and Semiconductors Association of India,the Indian market for semiconductor components would register a 10.1% CAGR (2018-2025) to reach USD 32.35 billion by 2025. The country is a vital destination for global research and development centers. Therefore, the ongoing 'Make in India' initiative by the Government of India is expected to result in significant investment in the semiconductor market. Such initiatives by the government of India will leverage the RF GaN market.

- In February 2022, Navitas Semiconductor, a provider of GaN integrated circuits (ICs), announced its participation in the China International Capital Corporation Limited (CICC) Investor Conference. The company's proprietary GaN power IC integrates GaN power and GaN drive, control, and protection in a single SMT package. Such participation will leverage the GaN market in the region.

- Demand for RF GaN across the APAC region is expected to increase due to growing investor interest in developing infrastructure to support 5G technology. For instance, according to the GSMA, the Asia-Pacific mobile operator is expected to spend more than USD 400 billion by 2025, of which USD 331 billion will be expended on 5G deployments.

- The growth of RF GaN companies in China is part of a broader trend as the nation shifts from a manufacturing- to an innovation-driven economy. The Chinese market is witnessing an exploding demand for commercial wireless telecom applications, and Chinese companies are already developing next-gen telecom networks.

- Moreover, in December 2021, researchers from IIT Kanpur in India developed a high-performance, industry-standard model of aluminum GaN (AlGaN) high electron mobility transistor (HEMT). This model provides a simple design method that can be used to manufacture high-power RF circuits. RF circuits include amplifiers and switches used in wireless transmissions and are useful in aerospace and defense applications. Constant innovations by researchers will drive the market growth of RF GaN in the region.

Radiofrequency Gallium Nitride Industry Overview

The competitive rivalry among the players in the RF GaN market is high owing to the presence of some key players such as Raytheon Technologies, STM microelectronics, amongst others. Their ability to continually innovate their offerings has allowed them to gain a competitive advantage over other players. Through research and development, strategic partnerships, and mergers and acquisitions, these players have been able to gain a strong foothold in the market.

In June 2022, Qorvo, a prominent provider of innovative RF solutions that connect the world, was selected by the US Department of Defense (DoD) to proceed with the Advanced Integration Interconnection and Fabrication Growth for Domestic State-of-the-Art (SOTA) RF GaN program, also known as STARRY NITE, as part of the Office of Undersecretary of Defense Research & Engineering's (OUSD R&E) microelectronics roadmap. The program seeks to develop and mature domestic, open SOTA RF GaN foundries in alignment with the DoD's advanced packaging ecosystem.

In May 2022, STMicroelectronics and MACOM Technology Solutions Holdings Inc., a significant supplier of semiconductor products for the industrial, telecommunications, defense, and data center industries, announced the successful production of RF Gan on Silicon (RF Gan-on-Si) prototypes. With this achievement, ST and MACOM would continue to work together and enhance their relationship.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Technology Snapshot

- 4.5 Assessment of the Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Strong Demand from Telecom Infrastructure Segment Driven by Advancements in 5G Implementation

- 5.1.2 Favorable Attributes Such As High-performance and Small Form Factor to

- 5.2 Market Restraints

- 5.2.1 Cost & Operational Challenges

6 MARKET SEGMENTATION

- 6.1 By Application

- 6.1.1 Military

- 6.1.2 Telecom Infrastructure (Backhaul, RRH, Massive MIMO, Small Cells)

- 6.1.3 Satellite Communication

- 6.1.4 Wired Broadband

- 6.1.5 Commercial Radar and Avionics

- 6.1.6 RF Energy

- 6.2 By Material Type

- 6.2.1 GaN-on-Si

- 6.2.2 GaN-on-SiC

- 6.2.3 Other Material Types (GaN-on-GaN, GaN-on-Diamond)

- 6.3 Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Aethercomm Inc.

- 7.1.2 Analog Devices Inc.

- 7.1.3 Wolfspeed Inc. (Cree Inc.)

- 7.1.4 Integra Technologies Inc.

- 7.1.5 MACOM Technology Solutions Holdings Inc.

- 7.1.6 Microsemi Corporation (Microchip Technology Incorporated)

- 7.1.7 Mitsubishi Electric Corporation

- 7.1.8 NXP Semiconductors NV

- 7.1.9 Qorvo Inc.

- 7.1.10 STMicroelectronics NV

- 7.1.11 Sumitomo Electric Device Innovations Inc.

- 7.1.12 HRL Laboratories

- 7.1.13 Raytheon Technologies

- 7.1.14 Mercury Systems, Inc