|

市場調査レポート

商品コード

1850333

オレオレジン:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Oleoresin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| オレオレジン:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月30日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

概要

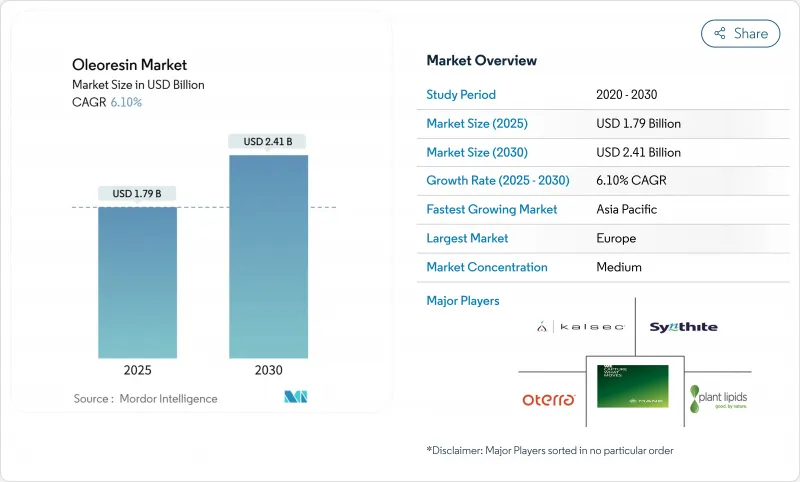

オレオレジン市場は、2025年に17億9,000万米ドルと評価され、予測期間中のCAGRは6.10%で、2030年には24億1,000万米ドルに達すると予測されています。

市場拡大の原動力となっているのは、各業界における天然素材やクリーンラベル素材に対する世界的な需要の高まりです。オレオレジンは、安定性、保存期間の長さ、濃縮された風味、抗酸化作用、抗菌作用、抗炎症作用などの健康上の利点から、合成添加物よりも好まれています。消費者の健康志向の高まりにより、栄養補助食品や機能性食品におけるターメリック、ブラックペッパー、ジンジャー、トウガラシのオレオレジンの使用が増加しています。市場の成長は、製品の品質と効率を高める超臨界CO2抽出や無溶媒抽出などの抽出方法の改良によってさらに支えられています。さらに、天然成分に対する有利な規制や研究開発投資の増加が、オレオレジンの用途を拡大しています。

世界のオレオレジン市場の動向と洞察

加工食品における天然着色料と天然香料の規制強化

2025年に食品医薬品局が3種類の天然着色料添加物を認可したことを受け、規制当局の動向はオレオレジン市場のダイナミクスに大きな影響を及ぼしています。認可された物質は、チョウマメ花エキス、ガルディエリアエキスブルー、食品用途のリン酸カルシウムです。この規制変更は、石油由来の合成染料からの体系的な移行を示すもので、天然代替物を専門とするオレオレジンメーカーに大きなビジネスチャンスをもたらすものです。欧州連合(EU)による規則1334/2008の施行は、すべての食品香料をEUの香料データベースに登録することを義務付けることにより、これらの要件を強化し、天然成分の調達を必要としています。さらに、欧州食品安全機関によるローズマリー抽出物およびパプリカオレオレジンの科学的評価は、複数の製品カテゴリーにわたる天然成分利用の包括的プロトコルを確立し、一貫した市場拡大を促進しています。

食品、飲食品、栄養補助食品におけるクリーンラベル需要の高まり

クリーンラベル製品に対する消費者の嗜好は原料の選択基準を変えつつあり、オレオレジンは機能性とラベルの透明性の両方を提供するソリューションとして浮上しています。クリーンラベルの動きには持続可能性の証明と加工方法が含まれ、倫理的な調達と環境に優しい抽出技術を提供するオレオレジンサプライヤーに機会を創出しています。国際食品情報評議会(IFIC)によると、2023年には、米国の回答者の約29%がクリーンな原材料を含むと表示された食品や飲食品を定期的に購入しており、これは食品用途における天然オレオレジンの需要に直接影響を与えています。欧州市場はクリーン・ラベルの採用率が最も高く、有機認証が市場参入の基本要件となっています。飲料メーカーはクリーンラベルの需要に対応し、製品の透明性と安定性を維持しながら天然の着色料と香味料を提供する水溶性のオレオレジン製剤を取り入れています。この動向は、消費者がクリーンラベルの証明のある製品により多くの対価を支払うことを望むため、プレミアム価格を可能にし、これらの要件を満たすオレオレジンサプライヤーに利幅拡大の可能性をもたらします。

原料価格の変動と複雑な抽出工程による高い生産コスト

原材料価格の変動は、オレオレジン市場の成長にとって大きな制約となります。気候の混乱や地政学的緊張によりスパイスの商品価格が変動するからです。ブラックペッパーの価格は、旺盛な国内需要と輸出需要により大幅に上昇し、オレオレジンメーカーにコスト圧力をもたらしています。経済顧問局によると、2024会計年度のインド全土における黒胡椒の卸売物価指数は185.4に達し、前年度より上昇しました。サプライチェーン全体の生産コストが上昇しており、インドのスパイス市場では肥料や労働力のコストが上昇しています。超臨界CO2システムは、従来の溶媒抽出法よりも収量と品質が高いにもかかわらず、多額の設備投資と専門的な知識を必要とするため、抽出技術コストがさらなる課題となっています。

セグメント分析

黒胡椒オレオレジンは2024年に25.41%の市場シェアを占め、食品、医薬品、化粧品産業への応用を通じて支配的地位を維持します。ウコンのオレオレジンは2030年までのCAGRが8.38%と最も高い成長率を示しているが、これは栄養補助食品における用途の拡大とクルクミンベースの製品に対する規制当局の承認の増加によるものです。これらのセグメント間の成長率の差は消費者の嗜好を反映しており、特に栄養補助食品や機能性食品において、抗炎症作用や抗酸化作用によりウコンが注目されるようになっています。パプリカオレオレジンは、着色料および香味料として機能することで市場での存在感を維持しており、特に食肉加工品ではクリーンラベル基準を満たしながら天然の着色料を提供します。

トウガラシオレオレジンは、標準化された辛さレベルを必要とする特定の用途に適しており、スパイシーな食品の人気の高まりや、業務用食品製造における一貫した辛味の必要性により需要が増加しています。超臨界CO2抽出技術は、従来の溶媒法と比較して、より高い純度レベルと生物活性化合物の優れた保存性を実現することで、すべてのセグメントにおいて製品の品質を向上させます。ジンジャーオレオレジンでは飲料や菓子類での使用が増加し、ガーリックオレオレジンとオニオンオレオレジンは本格的な風味を出すために硫黄化合物の保存を必要とする特定の市場に対応しています。ウコンが伝統的な香辛料から健康増進化合物として認知されるようになったことが示すように、このセグメントの動態は機能性成分への業界動向と一致しています。

地域分析

2024年の市場シェアは欧州が29.16%を占め、天然素材を支持する厳しい規制と、ドイツ、スペイン、オランダと世界のオレオレジンサプライヤーを結ぶ強固なサプライチェーンがその原動力となっています。この地域の成熟市場では、オーガニックや持続可能な方法で調達されたオレオレジンのプレミアム価格が標準要件として重視されています。サプライチェーンのトレーサビリティと環境責任は倫理的なサプライヤーに機会を創出する一方、確立された食品加工産業は用途を問わず一貫した需要を維持しています。

アジア太平洋は2030年までのCAGRが7.04%と最も高い成長率を示し、インドが世界最大のスパイス生産国の地位を占める。農業・農民福祉省の報告によると、インドのスパイス生産量は2024年度に1,180万トンに達し、同国のオレオレジン製造・輸出能力を支えています。中国のパプリカの輸入量は大きく、有機生産とトレーサビリティ基準を重視する貿易要件が市場力学に影響を与えます。

北米は、天然素材とクリーン・ラベルの需要を支える強力な規制枠組みを備えた成熟市場を示しています。食品メーカーの人工成分離れは、天然素材に代わるオレオレジンの機会を創出します。この地域は、パンデミックによる混乱後のサプライ・チェーンの回復力を優先し、国内調達と戦略的在庫管理に重点を置いています。先進的な食品加工産業、消費者の高い購買力、拡大する栄養補助食品部門が、プレミアムオレオレジン製品の成長を支えます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場促進要因

- 加工食品における天然着色料と香料の使用を求める規制の推進

- 食品、飲料、栄養補助食品におけるクリーンラベルの需要増加

- エスニック風味とスパイシー風味の世界の需要の高まり

- オレオレジンの長期保存性と物流上の利点

- パーソナルケア製品や化粧品への使用拡大

- 栄養補助食品業界における採用増加

- 市場抑制要因

- 原材料価格の変動と複雑な抽出プロセスによる高生産コスト

- 季節や気候条件により原材料の入手が制限される

- 合成代替品や代替香料との競合

- オレオレジンの繊細な性質による保管と取り扱いの課題

- サプライチェーン分析

- 規制の見通し

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力/消費者

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品タイプ別

- パプリカ

- 黒コショウ

- ターメリック

- トウガラシ

- ジンジャー

- ニンニク

- タマネギ

- その他

- 形態別

- 油溶性液体オレオレジン

- 水溶性液体オレオレジン

- 粉末オレオレジン

- 用途別

- 飲食品

- ベーカリー製品

- スパイスと調味料

- 肉類および魚介類

- 調理済み食事とスナック

- その他の飲食品

- 栄養補助食品

- 医薬品

- 化粧品・パーソナルケア

- 動物飼料およびペットフード

- 飲食品

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- その他アジア太平洋地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 戦略的動向

- 市場ランキング分析

- 企業プロファイル

- Synthite Industries Ltd

- Kalsec Inc.

- Mane SA

- Plant Lipids Private Limited

- Oterra A/S

- Olam Food Ingredients

- Silverline Chemicals Ltd

- Universal Oleoresins Private Limited

- Naturite Agro Products Ltd

- Givaudan SA

- McCormick and Company

- Sensient Technologies

- Lionel Hitchen Limited

- Natura Vitalis Industries Pvt. Ltd.

- Ozone Naturals

- AVT Group

- Mul Group

- Arjuna Natural Private Limited

- Rakesh Sandal Industries

- Natures Natural India Oils Private Limited