|

市場調査レポート

商品コード

1687250

石油・ガスEPC-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Oil & Gas EPC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 石油・ガスEPC-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 200 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

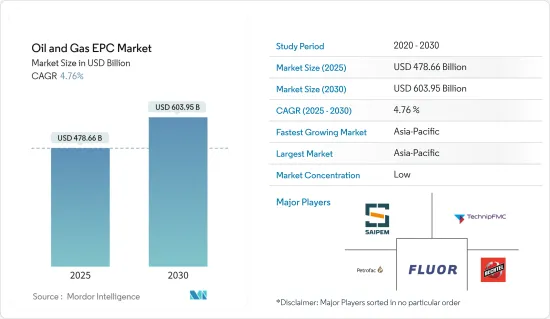

石油・ガスEPC市場規模は2025年に4,786億6,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは4.76%で、2030年には6,039億5,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、石油・ガス需要の増加と天然ガス消費量の増加により、天然ガスインフラ開発の必要性が高まっており、また、オフショア石油・ガス探査・生産(E& P)活動の増加も、調査対象市場の成長を促進すると予想されます。

- 一方、石油・ガス価格の高い変動は、石油・ガスEPC市場にとって大きな抑制要因の1つです。

- さまざまな国で新たな石油・ガス田が発見されていることから、予測期間中、上流・中流・下流のすべてのセグメントで石油・ガスEPC市場に十分な機会が生まれると予想されます。

- アジア太平洋が市場を独占しており、予測期間中も大きな成長が見込まれます。この成長は、天然ガス需要の増加と今後のLNG施設によるEPCサービスの大量需要に起因しています。

石油・ガスEPC市場の動向

上流セグメントが市場を独占する見込み

- 石油・ガス上流部門のEPCには、陸上と海上の探査・生産関連サービスが含まれます。従来、オンショアEPCへの投資総額はオフショアセグメントのそれを上回っていたが、これは主に、オフショアセグメントよりも投資要件が低く、複雑性が低く、アクセスしやすい立地であり、リスクが低いためです。しかし、陸上鉱区の成熟化により、オフショアセグメントへの投資は過去10年間で増加しています。

- 固定プラットフォーム、浮体式生産貯蔵積出設備(FPSO)、浅海、深海、超深海用の浮体式生産設備の設計、製作、据付、試運転、始動を含む据付などのオフショア向けEPCサービスが人気を集めています。

- 海洋構造物のEPCに関しては、固定構造物であれ浮体構造物であれ、海洋施設の開発オプションを特定し評価することが極めて重要です。浅海で使用される固定プラットホームのEPCサービスには、ジャケット、三脚、統合トップサイド、コンプレッションプラットフォームなどの建設と配備が含まれ、固定プラットホームの安定性と風や水の動きに対する弾力性を確保します。浮体式プラットフォームサービスは、一般に深海向けであり、半潜水式プラットフォーム用の船体やデッキ、FPSO用のモジュールやタレット、係留システムやブイの建設や配備が含まれます。

- 浮体式プラットフォームは一般に、生産施設から陸上ターミナルまで高価な長距離パイプラインを敷設する必要性を排除します。浮体式プラットフォームは、固定式石油プラットフォームとパイプラインの設置費用が高すぎる小規模油田でも経済的です。油田が劣化後は、固定プラットフォームを廃止する代わりに、FPSOを移動して新たな場所で使用することもできます。

- BP Statistical Review of World Energy 2023によると、2022年の世界の原油生産量は約44億トンでした。この数字は2018年にピークを迎え、世界の原油生産量は約45億トンに達しました。原油生産量は前年比約4.2%増となりました。

- アフリカでは、事業者が多くの新規探鉱・生産契約を締結しています。例えば、2022年1月、イタリアに本社を置く石油・ガス会社エニが、エジプトの5つの鉱区で探鉱契約を締結しました。これらの鉱区は、東地中海、西部砂漠、スエズ湾に位置しています。東部砂漠と西部砂漠では、他の企業によって7つの石油・ガス生産契約が結ばれました。

- このような開発により、石油・ガスEPC市場は今後急速に拡大するとみられます。

アジア太平洋が市場を独占する見込み

- アジア諸国の高い都市化率によるエネルギー需要の増加が、この地域の石油・ガス生産率の高さにつながっています。中国のような国々の存在が、この地域のEPC市場成長の主要原動力となっています。

- 中国はアジア最大の石油・天然ガス生産国です。2020年には、天然ガス総生産量の約30%を占めます。同国は、天然ガスの需給均衡を達成するため、さらに多くの上流・中流プロジェクトを計画しています。中国は、産業・商業部門の両方で天然ガス需要の急増を目の当たりにしています。

- 多くの企業が陸上・海上での探鉱・生産活動の青写真を描いています。2021年2月、中国海洋石油(CNOOC)は、南シナ海の深海埋蔵量や中国国内の非在来型資源を含む天然ガスの探鉱・開発を加速する計画を表明しました。同社は2021年に約139億3,000万~154億8,000万米ドルの資本支出を計画し、2025年までにポートフォリオの30%をガスに、2035年までに50%をガスにするとしています。

- インドはアジア太平洋で第2位の原油生産国です。BP Statistical Review of World Energy 2023によると、2022年の同地域の原油生産量の9.5%を占めています。インドの石油・ガス産業は、掘削リグ、生産プラットフォーム、精製所、パイプライン、ターミナルなどさまざまな設備があります。

- 2022年6月現在、インドには77基の稼働中のリグがあります。同国の石油生産量は、油田の老朽化と大きな発見の不在により、ほぼ10年間減少し続けています。国営企業も民間企業も、古い油田からの回収率を上げるための投資計画に取り組んでいます。

- 例えば、2022年4月、Indian Oil Corp(IOCL)は、北東地域にグリーンフィールド施設を設置するなど、石油・石油・潤滑油(POL)の貯蔵能力に1,020億米ドルを投資する計画を発表しました。

- こうした開発により、同地域は今後数年間、石油・ガスEPC市場の豊かな成長を示すことになりそうです。

石油・ガスEPC産業概要

石油・ガスEPC市場は細分化されています。同市場の主要企業(順不同)には、Saipem SpA、TechnipFmc PLC、Petrofac Limited、Fluor Corporation、Bechtel Corporationなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2028年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 天然ガスインフラ開発需要の高まり

- オフショア石油・ガス探査・生産(E& P)活動の増加

- 抑制要因

- 石油・ガス価格の高い変動性

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- セクター

- 上流

- 下流

- 中流

- 市場分析:地域別(2028年までの市場規模・需要予測(地域によるみ))

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- フランス

- 英国

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- その他の中東・アフリカ

- 北米

第6章 競争情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- National Petroleum Construction Company

- Petrofac Limited

- Tecnicas Reunidas SA

- Daewoo Engineering & Construction Co. Ltd

- Fluor Corporation

- Samsung Engineering Co. Ltd

- Korea Shipbuilding & Offshore Engineering Co. Ltd

- Hyundai Engineering & Construction Co. Ltd

- John Wood Group PLC

- TechnipFMC PLC

- Bechtel Corporation

- Saipem SpA

- McDermott International Ltd

- KBR Inc.

- Sinopec Engineering(Group)Co. Ltd

第7章 市場機会と今後の動向

- 世界の新規石油・ガス田の発見

目次

Product Code: 57107

The Oil & Gas EPC Market size is estimated at USD 478.66 billion in 2025, and is expected to reach USD 603.95 billion by 2030, at a CAGR of 4.76% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the growing demand for oil & gas and the rising consumption of natural gas, which is creating a need to develop the natural gas infrastructure, and an increase in offshore oil and gas exploration and production (E&P) activities are also expected to drive the growth of the market studied.

- On the other hand, the high volatility of oil and gas prices is one of the major restraints for the oil and gas EPC market.

- Nevertheless, the discovry of new oil and gas fields in various countries are exoected to create ample opportunities for the oil and gas EPC market for all the upstream, midstream, and downstream sectors during the forecast period.

- The Asia-Pacific region dominates the market and is also likely to witness significant growth during the forecast period. This growth is attributed to the increasing demand for natural gas and upcoming LNG facilities resulting in massive demand for EPC services.

Oil and Gas EPC Market Trends

Upstream Segment Expected to Dominate the Market

- The EPC in the upstream oil and gas sector includes onshore and offshore exploration and production-related services. Traditionally, the total investments in onshore EPC are more than that of the offshore segment, mainly due to lower investment requirements, lesser complexity, more accessible sites, and lower risk than the offshore segment. However, investment in the offshore segment has risen during the last decade due to maturing onshore fields.

- The EPC services for offshore, such as installations, including design, fabrication, installation, commissioning, and start-up of a fixed platform, floating production storage and offloading (FPSO) units, and floating production facilities for shallow, deep water, and ultradeep waters, are gaining traction.

- Concerning the EPC for offshore structures, identifying and assessing development options for offshore facilities, whether based on fixed or floating structures, is crucial. The EPC services for fixed platforms used for shallow waters include constructing and deploying jackets, tripods, integrated topsides, compression platforms, etc., to ensure that fixed platforms are stable and resilient to wind and water movements. The floating platform services, generally for deepwater, include constructing and deploying hulls and decks for semi-submersible platforms, modules and turrets for FPSOs, and mooring systems and buoys.

- Floating platforms generally eliminate the need for laying expensive long-distance pipelines from the production facility to an onshore terminal. Floating platforms are also economical in smaller oil fields, where the expense of installing a fixed oil platform and pipeline is too high. Once the field is depleted, FPSOs may be moved and used at a new location instead of decommissioning a fixed platform.

- According to BP Statistical Review of World Energy 2023, in 2022, global crude oil production amounted to about 4.4 billion metric tons. The figure peaked in 2018 when oil production worldwide reached nearly 4.5 billion metric tons. The crude oil production witness about 4.2% growth compared to previous year.

- In Africa, the operators have signed many new exploration and production contracts. For example, in January 2022, Eni, the Italy-based oil and gas company, clinched an exploration contract in five blocks in Egypt. The blocks are located in the Eastern Mediterranean Sea, Western Desert, and Gulf of Suez. Seven oil and gas production agreements were signed for the Eastern and Western deserts by other companies in the country.

- Such developments are likely to propel the oil and gas EPC market rapidly in the future.

Asia-Pacific Expected to Dominate the Market

- The growing energy demand due to the high urbanization rate in Asian countries has led to the region's high oil and gas production rate. The presence of countries like China is the main driver of the region's EPC market's growth.

- China is the largest crude oil and natural gas producer in Asia-Pacifi. In 2020, the country accounted for around 30% of the total natural gas production. The country has planned even more upstream and midstream projects to achieve an equilibrium in the demand-supply situation of natural gas in the country. China has witnessed an upsurge in the natural gas demand in both the industrial and commercial sectors.

- Many companies have blueprints for exploration and production activities onshore and offshore. In February 2021, CNOOC Ltd stated its plans to accelerate the exploration and development of natural gas, including deepwater reserves in the South China Sea and unconventional resources onshore in China. The company planned a capital spending of around USD 13.93-USD 15.48 billion in 2021 to make gas part of 30% of its portfolio by 2025 and 50% by 2035.

- India is the second-largest crude oil producer in the Asia-Pacific region. It accounted for 9.5% of the regional crude oil production in 2022, according to the BP Statistical Review of World Energy 2023. Although the country has a relatively less complex and new oil and gas infrastructure than China, India's oil and gas industry includes various installations, including drilling rigs, production platforms, refineries, pipelines, and terminals.

- As of June 2022, India has 77 active rigs. The country's oil production has been falling for almost a decade due to aging fields and the absence of major discoveries. Both state-owned and private players have been working on investment plans to raise recovery from older fields.

- For instance, in April 2022, Indian Oil Corporation Limited (IOCL) announced its plans to invest USD 102 billion in petroleum, oil, and lubricant (POL) storage capacities, including setting up a greenfield facility in the northeast region.

- Owing to such developments, the region is likely to witness rich growth in the oil and gas EPC market in the coming years.

Oil and Gas EPC Industry Overview

The oil and gas EPC market is fragmented. Some of the major players in the market (in no particular order) include Saipem SpA, TechnipFmc PLC, Petrofac Limited, Fluor Corporation, and Bechtel Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Demand to Develop the Natural Gas Infrastructure

- 4.5.1.2 Increase in Offshore Oil and Gas Exploration and Production (E&P) Activities

- 4.5.2 Restraints

- 4.5.2.1 High Volatility of Oil and Gas Prices

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Sector

- 5.1.1 Upstream

- 5.1.2 Downstream

- 5.1.3 Midstream

- 5.2 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)})

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 France

- 5.2.2.3 United Kingdom

- 5.2.2.4 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 South Africa

- 5.2.5.4 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 National Petroleum Construction Company

- 6.3.2 Petrofac Limited

- 6.3.3 Tecnicas Reunidas SA

- 6.3.4 Daewoo Engineering & Construction Co. Ltd

- 6.3.5 Fluor Corporation

- 6.3.6 Samsung Engineering Co. Ltd

- 6.3.7 Korea Shipbuilding & Offshore Engineering Co. Ltd

- 6.3.8 Hyundai Engineering & Construction Co. Ltd

- 6.3.9 John Wood Group PLC

- 6.3.10 TechnipFMC PLC

- 6.3.11 Bechtel Corporation

- 6.3.12 Saipem SpA

- 6.3.13 McDermott International Ltd

- 6.3.14 KBR Inc.

- 6.3.15 Sinopec Engineering (Group) Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Discovery of New Oil and Gas Fields Worldwide