|

市場調査レポート

商品コード

1907322

小麦:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Wheat - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 小麦:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

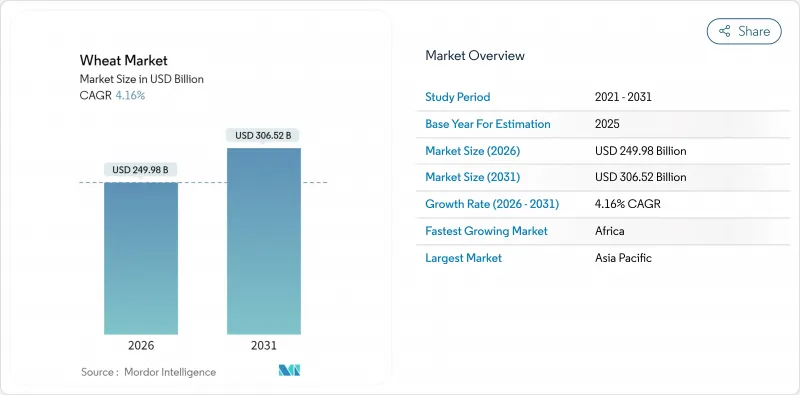

小麦市場は、2025年の2,400億米ドルから2026年には2,499億8,000万米ドルへ成長し、2026年から2031年にかけてCAGR4.16%で推移し、2031年までに3,065億2,000万米ドルに達すると予測されています。

世界の記録的な収穫量の増加が続く一方、小麦が世界のカロリー摂取量の20%を占めることで安定した需要基盤が確保されています。アジア太平洋地域の製粉能力拡大、干ばつ耐性品種の商業化、バイオ燃料義務化の拡大が相まって、輸出業者の利益基盤を拡大しています。ハイブリッド小麦、AIを活用した農業技術、可変施肥率といった供給側のイノベーションは生産リスクを低減しますが、資本要件を増大させます。市場の今後の展開は技術革新の導入によって支えられており、主要生産地域で人工知能を活用した収量予測プラットフォームが普及し、精密農業技術が資源最適化を促進しています。政府のバイオ燃料混合義務は追加的な需要源を生み出し、輸出制限による一時的な後退はあるもの、貿易自由化への取り組みは引き続き世界市場の統合と価格発見メカニズムを促進しています。

世界の小麦市場の動向と展望

強化小麦食品への需要増加

機能性栄養への消費者関心の高まりにより、鉄分・亜鉛・プロバイオティクス強化のパン、麺類、シリアル類のプレミアム価格が上昇しています。臨床試験では、プロバイオティクス強化が焼成後も生存菌数を維持することが確認され、健康表示の有効性が裏付けられました。アジア及び北米の大手小売業者は2024年以降、強化小麦製品の棚スペースを倍増させており、小麦市場における特殊粉の需要拡大を促進しています。米国大学では化学改良剤を使用せずに適切なパンの膨張性を実現するソフトホワイト小麦品種を開発し、生産1万トン当たり30万米ドルの製パン添加物コスト削減を実現しました。インドとフィリピンの政府栄養プログラムでは現在、微量栄養素を豊富に含む小麦粉への補助金を支給しており、普及が加速しています。

小麦ベースの即席製品の拡大

都市部の所得向上に伴い、消費者はインスタント麺、即食フラットブレッド、冷凍ベーカリー製品へと移行しており、これらはいずれも安定した小麦粉品質に依存しています。パプアニューギニアとスウェーデンに新設された製粉工場は年間120万トンの製粉能力を追加し、AI制御室を導入することでエネルギー消費量を12%削減しています。スナックメーカーは価格変動リスクをヘッジするため複数年の供給契約を締結しており、これにより加工業者は厳しい欠陥許容値を満たす光学選別機への投資を促進されています。電子商取引の食料品プラットフォームは、半焼きパンの当日配送サービスを提供することで需要をさらに拡大し、小麦市場における製粉業者の再発注サイクルを短縮しています。

肥料価格の変動性

天然ガス価格の変動により、2022年から2024年にかけて尿素価格は2倍に跳ね上がり、小麦生産者の利益率は1ヘクタールあたり最大65米ドル減少しました。ロシアとベラルーシの供給途絶によりリン酸塩市場はさらに逼迫し、東アフリカのDAP在庫は43日分まで減少しました。エチオピアとバングラデシュの信用制約を受けた小規模農家は肥料施用量を15%削減したため、小麦産業全体で収量低下と品質割引の増加につながりました。これに対し多国籍農業資材企業はモロッコで硫酸カリ混合の拡大で対応しましたが、価格転嫁のタイムラグが地域的な価格歪みを生じさせました。グリーンアンモニアプロジェクトは窒素コストを化石エネルギーから切り離す可能性を秘めていますが、2030年までの実用規模化は不透明であり、小麦市場への中期的緩和効果は限定的です。

地域別分析

2025年における小麦市場シェアは、アジア太平洋地域が37.40%を占めました。北米は近代的な貯蔵施設、鉄道、河川ネットワークを背景に、輸出基盤の強靭さを維持しています。米ドル安と豊富な在庫を追い風に、米国からの出荷量は2025/26年に2,700万トンに達すると予測されています。遺伝子編集作物に関する政策の明確化によりハイブリッド品種の導入が加速する一方、ハイプレインズ地域での断続的な干ばつが生産の変動性と保険請求を増加させています。カナダ・プレーリー地方は水分不足の影響を受けやすいもの、高タンパク春小麦のプレミアム価格を活用し収益変動を緩和しています。31億米ドル規模の気候適応型商品助成金は、亜酸化窒素排出削減につながる分割施肥などの再生農業手法を促進しています。

アフリカでは2031年までのCAGR5.22%が人口増加を上回り、都市部の食生活が小麦ベースのパンやパスタへ移行しています。欧州は降雨量の不安定さによる収量変動があるもの、北アフリカ・中東地域への主要供給源としての地位を維持しております。ウクライナ産穀物は食料安全保障の強化に寄与すると同時に、価格下落を懸念する加盟国生産者の不安を和らげております。厳格なマイコトキシン許容基準や「農場から食卓まで」といった持続可能性スキームはコンプライアンスコストを増加させますが、欧州輸出業者が品質プレミアムを獲得することを可能にしております。リモートセンシングプラットフォームへの投資により、協同組合は収穫前の圃場単位でのタンパク質含有量を予測できるようになり、選別戦略の最適化が進んでおります。

アジア太平洋地域では、中国北部の大規模集約農場から南アジアの小規模農家中心の耕作地まで、最も多様な生産システムが見られます。オーストラリアでは保全耕作を背景に降雨減少動向を相殺し、2025年には3,060万メートルトンの生産が見込まれています。中国各省における精密散布機の導入により除草剤使用量が18%削減され、収益性と環境評価が向上しました。一方、インドネシアとフィリピンはほぼ完全な輸入依存状態が続いており、消費者は世界の価格変動の影響を受けやすい状況です。地域自由貿易協定により関税障壁は低下したもの、衛生検疫プロトコルなどの非関税障壁が依然として越境流通を阻んでいます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 強化小麦食品の需要増加

- 小麦ベースの便利製品の拡大

- 政府のバイオ燃料混合義務化

- 耐熱性小麦品種の商業化

- 貿易自由化

- AIを活用した収量予測プラットフォームの導入

- 市場抑制要因

- 肥料価格の変動性

- 地政学的な輸出制限

- マイコトキシン汚染事例

- 水ストレスによる収量減少

- 規制情勢

- テクノロジーの展望

- 価値/バリューチェーン分析

- PESTEL分析

第5章 市場規模と成長予測(金額および数量)

- 地域別(生産分析、消費分析(数量と金額)、輸入分析(数量と金額)、輸出分析(数量と金額)、価格動向分析)

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- チリ

- 欧州

- ドイツ

- フランス

- イタリア

- 英国

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 中東

- トルコ

- サウジアラビア

- アフリカ

- 南アフリカ

- ケニア

- エジプト

- 北米

第6章 競合情勢

- List of Stakeholders