|

市場調査レポート

商品コード

1850077

加工デンプン:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Modified Starch - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 加工デンプン:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月18日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

概要

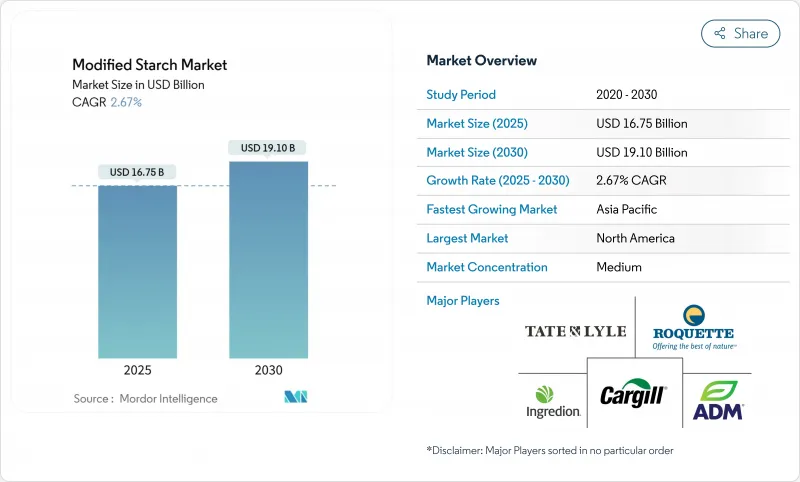

加工デンプンの世界市場は、2025年に167億5,000万米ドルと評価され、予測期間中のCAGRは2.67%を記録し、2030年には191億米ドルに達すると予測されています。

同市場は、都市化、人口増加、食生活の変化(特に新興国市場)により変貌を遂げつつあります。市場参入企業は、戦略的提携や地理的拡大を通じて市場での存在感を高めています。加工食品や簡便食品への需要の高まりは澱粉メーカーに新たな機会を生み出し、生産技術の向上は業務効率を高めています。市場の成長は、飲食品、製紙、繊維、製薬業界における用途の増加によってさらに支えられています。さらに、クリーンラベル製品や天然成分に対する消費者の嗜好の高まりが、メーカーに革新的な加工デンプンソリューションの開発を促しています。アジア太平洋地域は、中国やインドのような新興経済国からの大きな需要により、依然として主要な促進要因となっています。環境規制や持続可能性への懸念も、加工デンプン業界の製品開発や製造プロセスに影響を与えています。

世界の加工デンプン市場の動向と洞察

クリーンラベル原料への需要の高まりが加工デンプン消費を促進

クリーンラベルの動きは、ニッチセグメントから主要な市場促進要因へと発展しています。化学的処理の代わりに物理的処理を施した改質澱粉は、機能性の向上を達成しながらクリーンラベルのステータスを維持できるため、脚光を浴びています。食品メーカーは、化学添加物を使用せずにデンプンの機能性を向上させるコールド・プラズマ処理やパルス電界技術を導入し、食感や安定性を向上させながらクリーン・ラベルの表示を維持する製品を実現しています。これらの技術により、メーカーは天然成分の状態を損なうことなく、ゲル化温度、粘度、凍結融解安定性などのデンプン特性を変更することができます。

この動向は産業用途にも拡大しており、製紙メーカーは性能基準を維持しながら持続可能性を高めるため、合成添加物を改質デンプンに置き換えています。製紙メーカーが合成澱粉を改質澱粉に置き換えることで、性能基準を維持しながら持続可能性を高めています。このような市場の進化は、加工方法がより単純であるにもかかわらず、物理的に改質された澱粉がより高い価格で取引されるという、原料市場における従来の価格パターンを逆転させるような、明確な価格構造を生み出しました。プレミアム価格は、クリーンラベル製品に対する消費者の需要と、物理的改質処理に必要な特殊設備の両方を反映しています。

ビーガンおよび植物性食品における加工デンプンの使用拡大

植物由来の食品セクターの爆発的成長により、動物由来製品の官能特性を再現できる機能性素材に対するかつてない需要が生まれています。米国農務省の2023年のデータによると、ドイツでは158万人が植物ベースの食生活を送っています。改質デンプン、特にゲル化および水結合特性を強化したデンプンは、説得力のある食感と口当たりを持つ食肉類似物の調合に不可欠な成分となっています。澱粉改質技術における最近の技術革新は、植物ベースの用途に特に最適化された変種を生み出し、植物性タンパク質と組み合わせたときに筋肉組織の繊維状構造を模倣することができるようになりました。

こうした特殊なデンプンの戦略的重要性は、技術的な機能性だけでなく、サプライチェーンの弾力性にも及んでいます。メーカー各社は、気候関連の混乱を緩和するために、多様な農業投入物から調達できる原料を求めているからです。このような用途に特化した開発アプローチは、加工デンプン市場に新たな価値プールを生み出し、植物由来の製剤に特有の課題に対するオーダーメイドのソリューションを提供できるプレーヤーに報いることになります。

原材料価格の変動が利益率に影響

2024年の加工デンプン市場は、異常気象や地政学的混乱によりトウモロコシ価格が変動し、大きな変動に直面しました。米国農務省の最新データによれば、2024年のトウモロコシ価格は大幅に変動し、メーカーの一貫した価格維持能力に影響を与えました。この価格変動は主に、主要なトウモロコシ生産地域における深刻な干ばつと、世界的な穀物移動に影響を及ぼす貿易制限の継続によるものです。この変動は加工デンプン生産者の利益率を低下させ、生産者は競争の激しい消費市場でコスト増を顧客に転嫁するのに苦労しました。加工デンプンの生産者は、トウモロコシ以外の原料ソースを拡大し、ジャガイモやタピオカを代替原料として取り入れることで、作物特有の供給障害に対応しました。

代替原料へのシフトは、加工設備や研究開発に多額の投資を必要としました。このような多様化によって供給リスクは軽減されたもの、植物由来の原料が異なると、同様の機能性を実現するために特定の改良プロセスが必要になるため、技術的課題も生じた。温度管理、化学処理、加工時間のバリエーションを含むこうした技術的要件により、サプライヤーの迅速な変更が制限され、複数の澱粉源を加工できる生産者の価格決定力が強化されました。複数の澱粉ソースを管理することの複雑さは運営コストの増加につながったが、多様な加工能力を持つメーカーにとっては市場の安定性を高めることになりました。

セグメント分析

酸化デンプンは加工デンプン市場で最も急成長しているセグメントとして浮上しており、2025年から2030年までのCAGRは5.54%と予測され、市場全体の成長率を上回っています。その他」のカテゴリーは、レジスタントスターチやデュアルモディファイドバリアントなどの特殊な改良品で構成され、2024年のシェアは53.44%で市場を独占しています。これは、市場が標準的な改質タイプよりも用途に特化したソリューションにシフトしていることを示しています。

プレゼラチン化デンプンは、主に冷水溶解性により、インスタント食品用途で堅調な需要を維持しています。酸変性タイプは、正確なゲル強度のコントロールが不可欠な菓子類で存在感を増しています。カチオン澱粉は、その正電荷特性を利用して凝集効率を改善し、製紙産業から水処理へと用途を拡大しています。こうした技術開発により、メーカーは用途に特化したソリューションを生み出すことができ、競合の焦点は価格から性能へと移っています。

トウモロコシ(とうもろこし)は、その豊富な入手可能性、確立された加工インフラ、汎用性の高い改質の可能性により、2024年の市場の70.84%を占め、依然として加工デンプンの主要原料となっています。ジャガイモデンプンは、2025年から2030年までのCAGRが3.00%と予測され、最も急成長している代替品として浮上しています。

小麦澱粉は、特に地元での農業生産と確立された加工施設の恩恵を受けている欧州で、重要な地位を維持しています。タピオカ澱粉は、そのニュートラルな風味プロファイルと非遺伝子組み換えのステータスにより、クリーンラベル用途で牽引力を増しており、米やキャッサバのような他の供給源は特殊用途でニッチを見出しつつあります。市場のプレーヤーは、需要の高まりに対応するため、市場に新しい澱粉を投入しています。例えば、Roquette Freres社は2024年8月、調理用タピオカ澱粉「Clearem」シリーズを発売しました。これらはベーカリーのフィリング、デザート、乳製品に使用されます。

地域分析

北米は2024年に33.98%のシェアで加工デンプン市場をリードしており、その原動力は先進的な食品加工部門と医薬品製造能力です。この地域の優位性は、特にトウモロコシ生産などの強力な農業基盤によって強化されており、地元メーカーにコスト面での利点をもたらしています。2024年以降のコーンスターチの取り扱いに関する米国農務省の技術報告書を含む最近の規制動向は、非遺伝子組み換えや有機栽培の品種の重要性を浮き彫りにし、より広範な市場内にプレミアムセグメントを生み出しています。この地域の技術革新の焦点は持続可能性とクリーンラベル・ソリューションに移っており、メーカーは機能性を高めながら天然成分の状態を維持する物理的改良技術に投資しています。このような規制主導のイノベーションが新たな競合力学を生み出し、非化学的改質における技術力が、規模の経済性よりもむしろ重要な差別化要因になりつつあります。

アジア太平洋は、急速な工業化、食品加工能力の拡大、医薬品製造の増加に牽引され、2025年から2030年までのCAGRが3.32%と予測される急成長地域と位置づけられています。2023年のインド農業研究評議会のデータによると、中国では澱粉加工技術への多額の投資がこの地域の生産能力を高めており、インドでは製薬セクターの成長が特殊な賦形剤グレードの改質澱粉の需要を生み出しています。東南アジアのキャッサバや中国のジャガイモなど、この地域の多様な農業基盤は、トウモロコシに依存しない原料多様化の機会を提供しています。

欧州の市場力学欧州の市場力学は、厳しい規制の枠組みと先進的な持続可能性への取り組みによって特徴付けられ、他の地域とは異なる競争力学を生み出しています。EUの澱粉産業脱炭素化ロードマップは、澱粉生産の環境フットプリントを削減する野心的な目標を設定し、エネルギー効率の高い加工技術や循環型経済アプローチへの投資を促進しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- クリーンラベル原料の需要増加が消費を押し上げる

- ビーガン・植物性食品における加工デンプンの利用拡大

- 乳製品の主要安定剤としての加工デンプン

- 紙と繊維の産業用途を拡大し、市場へのリーチを拡大

- 低カロリー製品における脂肪代替物としての加工デンプンの機能性

- 有機食品配合における天然乳化剤としての加工デンプン

- 市場抑制要因

- 原材料価格の変動が利益率に影響を与える

- 食品中の化学的に加工された澱粉に対する規制圧力

- 架橋または酸化デンプン誘導体に関する健康への懸念

- 小麦由来の化工デンプンに関する潜在的なアレルギーの懸念

- サプライチェーン分析

- 規制の見通し

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力/消費者

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- タイプ別

- アルファ化デンプン

- 酸変性

- 酸化デンプン

- カチオンデンプン

- アセチル化デンプン

- その他

- 原料別

- トウモロコシ

- 小麦

- じゃがいも

- タピオカ

- その他

- 形態別

- 粉

- 液体

- 用途別

- 食品・飲料

- 医薬品

- パーソナルケア&化粧品

- 動物飼料

- テキスタイル

- 紙と段ボール

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- 英国

- ドイツ

- スペイン

- フランス

- イタリア

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場ランキング分析

- 企業プロファイル

- Cargill Inc.

- Archer Daniels Midland Company

- Ingredion Inc.

- Tate & Lyle PLC

- Roquette Freres

- Sudzucker AG(Beneo)

- Emsland-Starke GmbH

- AGRANA Beteiligungs-AG

- Avebe U.A.

- Tereos Group

- Grain Processing Corp.

- Universal Starch-Chem Allied Ltd.

- Sunar Misir

- China Starch Holdings Ltd.

- Global Bio-Chem Technology Group

- Spac Starch Products(India)Ltd.

- Thai Flour Industry Co.

- Visco Starch

- PT Sorini Agro Asia Corporindo Tbk

- Qingdao CBH Co.