|

市場調査レポート

商品コード

1686540

インドネシアの不動産:市場シェア分析、産業動向、成長予測(2025年~2030年)Real Estate In Indonesia - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドネシアの不動産:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

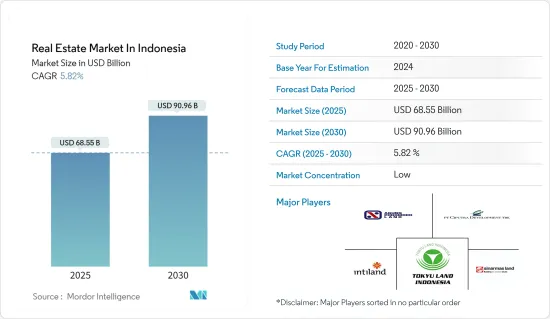

インドネシアの不動産市場2025年の市場規模は685億5,000万米ドルと推定、2030年には909億6,000万米ドルに達すると予測、予測期間(2025年~2030年)のCAGRは5.82%。

主なハイライト

- インドネシアは過去15年間、マクロ経済政策と構造政策を改善してきました。力強く安定した成長率により、同国経済は域内の他国に追いつきつつあり、インドネシアは開発課題に集中することができます。

- 急速な人口増加と高い都市化によって不動産需要と価格が上昇するなか、インドネシアの不動産市場はこの地域で最も重要なセクターのひとつとなっています。同国におけるCOVID-19危機の影響を大きく受けなかった数少ないセクターのひとつです。

- インドネシア統計局の公式数字によると、インドネシアの不動産活動によるGDPは2022年に488兆3,100億IDR(310億米ドル)に達しました。不動産活動に由来するインドネシアのGDPは、この10年間で徐々に増加しています。

- インドネシアでは、政府、外国投資家、世界銀行などの団体が支援する手頃な価格の住宅プロジェクトが、予測期間中の不動産市場の成長を高めると予想されます。

- インドネシア政府は、少なくとも年間100万戸を建設する「100万戸(OMH)」プログラムを導入しました。公共事業・公共住宅省(PUPR)によると、同プログラムにより2023年8月までに約63万4,132戸の住宅が建設されました。

- 経済が好転し、成長が刺激されたため、インドネシアにおけるプロテックの第一波は、中産階級の人々の住宅需要の増加から始まりました。検索ポータル企業での販売、購入、リースが集中し、プロテック分野は人気を博しています。

インドネシアの不動産市場動向

優良賃貸市場として台頭するジャカルタ

ジャカルタのサービスアパートメントは、規制完全撤廃後のビジネス活動の正常化や、日本、韓国、インドなどアジア諸国を中心とした外国人駐在員の需要増加を反映して、2023年第3四半期も平均入居率の改善が続いた。

2023年第3四半期現在の入居率は前四半期比約3.5%増の60.5%でした。CBDエリアのすべてのサービスアパートメントは安定した賃料を維持しました。これとは対照的に、新規サービスアパートメントプロジェクト(Citadines Gatot SubrotoとGrand Mansion Menteng by The Crest Collection)による新規供給が、非CBDエリアの賃料を押し上げました。登録された平均賃料は、CBDと南ジャカルタ(非一等地を含む)でそれぞれIDR445,986/平方メートル/月(USD28.85)とIDR410,707/平方メートル/月(USD26.57)でした。

専門家は、市場よりも高い賃貸料を提供する新しい高級サービスアパートメント・プロジェクトの参入が控えていることから、平均賃貸料がある程度上昇すると予想しています。

インドネシアにおける住宅販売の増加

- 業界専門家によると、インドネシアの住宅不動産市場は依然として低迷しており、2022年第3四半期の不動産価格指数は1.53%しか上昇していないです。インフレ調整後の不動産価格は3.48%下落しました。インフレを考慮すると、2022年第3四半期に住宅価格の上昇を記録したのはインドネシアの主要18都市のうち1都市のみでした。

- 市場は最近改善を見せたもの、依然として金融危機前の水準をはるかに下回っています。2018年から2023年まで、インドネシアの住宅価格指数は平均103.04ポイントで、2023年第2四半期には過去最高の107.26ポイントに達し、2018年第1四半期には過去最低の99.32ポイントを記録しました。

- 国内法では、非市民が不動産を完全に自由に所有することを事実上禁止しており、その権利は最長80年から100年の借地権に制限され、住宅ローン金融を利用することはできないです。さらに政府は、外国人投資家が購入できる不動産の最低価格を設定しており、スマトラ島北部のアパートの約6万5,000米ドルから、バリ島、ジャカルタ、ジャワ島の一部の一軒家の32万5,000米ドルまでの幅があります。

インドネシアの不動産業界の概要

インドネシアの不動産市場は、住宅用、商業用ともに競争が激しく、細分化されています。同市場は予測期間中に成長機会をもたらします。市場競争激化が販売価格や地価に影響を与え、市場の供給過剰を招いています。市場に参入している主な企業には、Agung Podomoro Land、Sinar Mas Land、Ciptura Group、東急不動産インドネシアなどがあります。また、インターネット普及率の上昇やeコマースの拡大により、各プレイヤーは技術動向に適応しつつあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の規制と政策

- 一般経済と不動産融資の金利レジームに関する洞察

- 不動産テックと不動産分野で活躍する新興企業に関する洞察

- 住宅不動産における資本市場の浸透とREITの存在に関する洞察

- 不動産購入動向-社会経済的・人口統計的洞察

- COVID-19の市場への影響

- バリューチェーン/サプライチェーン分析

第5章 市場力学

- 市場促進要因

- 人口の増加

- 住宅不動産需要の増加

- 市場抑制要因

- コスト増

- 市場機会

- 観光関連不動産

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第6章 市場セグメンテーション

- 物件タイプ別

- 住宅

- オフィス

- 商業施設

- ホスピタリティ

- 工業

- 都市別

- ジャカルタ

- バリ島

- インドネシア

第7章 競合情勢

- 市場集中度の概要

- 企業プロファイル

- PT Intiland Development Tbk

- Tokyu Land Indonesia

- Agung Podomoro Land

- Ciptura Group

- Sinar Mas Land

- PP Properti

- Lippo Group

- Trans Property

- Agung Sedayu Group

- PT. Pakuwon Jati Tbk*

- その他の企業

第8章 市場機会と今後の動向

第9章 付録

The Real Estate Market In Indonesia Market size is estimated at USD 68.55 billion in 2025, and is expected to reach USD 90.96 billion by 2030, at a CAGR of 5.82% during the forecast period (2025-2030).

Key Highlights

- Indonesia has improved its macroeconomic and structural policies over the last 15 years. With a strong and stable growth rate, its economy is catching up with other countries in the region, allowing Indonesia to focus on its development agenda.

- As property demand and prices rise due to rapid population growth and high urbanization, the real estate market in Indonesia is one of the most vital sectors in the region. It was one of the few sectors not significantly affected by the COVID-19 crisis in the country.

- The official figures from Statistics Indonesia reflected that the GDP from real estate activities in Indonesia amounted to IDR 488.31 trillion (USD 31 billion) in 2022. Indonesian GDP derived from real estate activities has gradually increased over the decade.

- The affordable housing projects in Indonesia supported by the government, foreign investors, and associations such as the World Bank are anticipated to enhance the real estate market's growth during the forecast period.

- The Indonesian government introduced the 'One Million Houses' (OMH) program to construct at least 1 million units annually. According to the Ministry of Public Works and Public Housing (PUPR), about 634,132 housing units were recorded until August 2023 under the program.

- Due to a better, growth-stimulating economy, the first wave of Proptech in Indonesia began with increased demand for homes from the middle-class populace. With a large concentration of selling, purchasing, and leasing on search portal firms, the proptech segment is gaining popularity.

Indonesia Real Estate Market Trends

Jakarta Emerging as a Prime Rental Market

In Jakarta, serviced apartments showed a continued improvement in average occupancy rate during 3Q 2023, reflecting the normalcy of business activities after the complete lifting of restrictions and increased demand from expatriates, especially from Asian countries, including Japan, South Korea, and India.

As of Q3 2023, the occupancy rate increased by about 3.5% QOQ to 60.5%. All serviced apartments in the CBD area maintained steady rental rates. In contrast, new supply in the form of new serviced apartment projects (Citadines Gatot Subroto and Grand Mansion Menteng by The Crest Collection) pushed rents up in the non-CBD area. The average rental rates registered were IDR 445,986/sq m/month (USD 28.85) and IDR410,707/sq m/month (USD 26.57) in the CBD and South Jakarta (including non-prime areas), respectively.

Experts expect some increment in the average rental rate given the forthcoming entry of new upscale serviced apartment projects that offer higher rental rates compared to the market.

Rising Residential Property Sales In Indonesia

- According to industry experts, Indonesia's residential property market remains slow, with the composite-16 property price index growing only by 1.53% in Q3 2022. When adjusted for inflation, property prices declined by 3.48%. When inflation is considered, only one of the eighteen major Indonesian cities recorded house price increases in Q3 2022.

- While the market showed improvements recently, it remains far below its pre-crisis levels. From 2018 to 2023, Indonesia's house price index averaged 103.04 points, reaching an all-time high of 107.26 points in Q2 of 2023 and a record low of 99.32 points in the first quarter of 2018.

- National laws effectively ban non-citizens from complete freehold ownership of the property, limiting their rights to a leasehold of a maximum of 80 to 100 years with no access to mortgage finance. In addition, the government has set a minimum price for real estate that can be bought by foreign investors, ranging from around USD 65,000 for an apartment in northern Sumatra to USD 325,000 for a house in Bali, Jakarta, and parts of Java.

Indonesia Real Estate Industry Overview

The Indonesian real estate market, including both residential and commercial, is highly competitive and fragmented. The market presents opportunities for growth during the forecast period. Higher competition among market players is impacting selling and land prices, further leading to oversupply in the market. Some of the major players present in the market include Agung Podomoro Land, Sinar Mas Land, Ciptura Group, and Tokyu Land Indonesia. The players are also adapting to technological trends, owing to the rising internet penetration and expansion of e-commerce.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Policies and Regulations

- 4.3 Insights into Interest Rate Regime for General Economy, and Real Estate Lending

- 4.4 Insights into Real Estate Tech and Startups Active in the Real Estate Segment

- 4.5 Insights into Capital Market Penetration and REIT Presence in Residential Real Estate

- 4.6 Real Estate Buying Trends - Socioeconomic and Demographic Insights

- 4.7 Impact of COVID-19 on the Market

- 4.8 Value Chain/Supply Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Population

- 5.1.2 Increase in Demand for Residential Real Estate

- 5.2 Market Restraints

- 5.2.1 Increase in Costs

- 5.3 Market Opportunities

- 5.3.1 Tourism-related Real Estate

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Threat of New Entrants

- 5.4.2 Bargaining Power of Buyers/Consumers

- 5.4.3 Bargaining Power of Suppliers

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Property Type

- 6.1.1 Residential

- 6.1.2 Office

- 6.1.3 Retail

- 6.1.4 Hospitality

- 6.1.5 Industrial

- 6.2 By City

- 6.2.1 Jakarta

- 6.2.2 Bali

- 6.2.3 Rest of Indonesia

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 PT Intiland Development Tbk

- 7.2.2 Tokyu Land Indonesia

- 7.2.3 Agung Podomoro Land

- 7.2.4 Ciptura Group

- 7.2.5 Sinar Mas Land

- 7.2.6 PP Properti

- 7.2.7 Lippo Group

- 7.2.8 Trans Property

- 7.2.9 Agung Sedayu Group

- 7.2.10 PT. Pakuwon Jati Tbk*

- 7.3 Other Companies