|

市場調査レポート

商品コード

1849968

シンガポール不動産:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Singapore Real Estate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| シンガポール不動産:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月24日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

概要

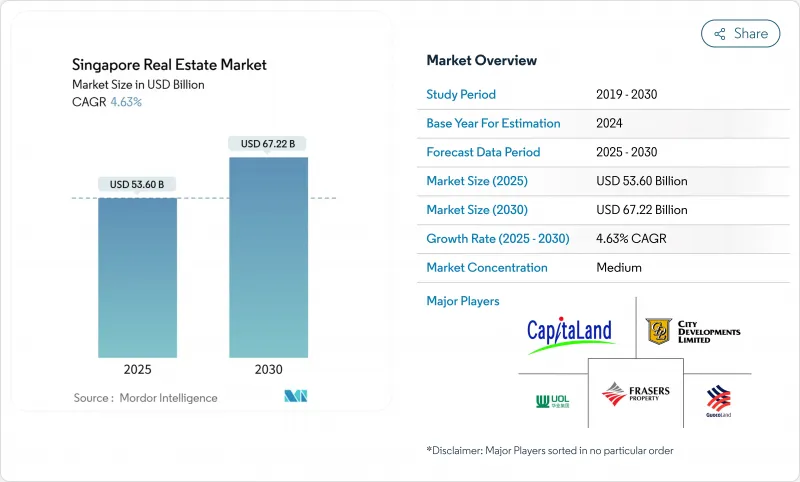

シンガポール不動産の市場規模は2025年に536億米ドル、2030年には672億2,000万米ドルに達すると推定・予測され、予測期間(2025~2030年)のCAGRは4.63%です。

安定したガバナンス、透明性の高い規制、政府主導の都市建設計画の活発なパイプラインは、引き続き幅広い投資家を惹きつけています。高級住宅は世界的な魅力を維持しており、近代的な物流施設、データセンター、複合施設に対する需要は、eコマースの成長、高度製造業、シンガポールの地域本社機能の拡大によって高まっています。供給が逼迫していること、土地の埋立容量が限られていること、融資額の規制が厳しくなっていることなどが投機的な動きを抑制しているが、長期的な資金の流れに狂いは生じていないです。開発業者は、PropTechの採用、プレハブ建設、グリーンマーク2021の要件に沿った新世代の低炭素設計によって差別化を図っています。

シンガポール不動産市場動向と洞察

政治的安定と強力な法的枠組みが後押しする外国人投資家の強い関心

外国資本は、契約執行可能性、明確な税制、効率的な紛争解決により、シンガポールを低リスクの拠点と見なし続けています。経済開発委員会は2024年中に100億米ドルの固定資産コミットメントを登録し、間接的に一等地のオフィスや産業の吸収を拡大する半導体、バイオ医薬品、AIプロジェクトに資金を誘導しています。2023年に導入された海外ネットワーク&エキスパート・パスは、グローバル人材の流入を維持し、プレミアム賃貸需要を下支えします。これらの力が相まって、シンガポール不動産市場の長期的な魅力が強化されます。

長期的開発に拍車をかける政府の都市計画

都市再開発局のマスタープラン2025草案は、今後10年間にわたりシンガポール不動産市場を再構築する、気候変動に強い統合的な青写真を定めています。旗艦プロジェクトには、2,000エーカーのグレーター・サザン・ウォーターフロントと800ヘクタールのロングアイランド埋立地が含まれ、海岸防衛を強化しながら、混合住宅、商業クラスター、20キロメートルのウォーターフロント・レクリエーションを追加します。テンガ線やセレター線といったMRTの延伸計画は、40万世帯以上を結びつけ、以前は十分なサービスを受けられなかった地区への価値移動を促進します。

厳しい冷房対策と印紙税が投機的な住宅投資を抑制

印紙税の引き上げ、融資額の上限規制の強化、民間からHDBへの転入者に対する15カ月の待機期間が、取引の速度を鈍化させています。2024年の政策パッケージを受けて、2025年第1四半期のHDB再販価格の伸びは1.6%に緩和しました。民間の新築住宅販売戸数は2025年5月に350戸を下回り、政策の有効性が浮き彫りになったが、賃金上昇と移民のおかげで構造的需要は維持されています。

セグメント分析

住宅部門は2024年の売上高の53.1%を占め、シンガポールの不動産市場規模が人中心の開発で主導権を握っていることを裏付けています。2025年から2027年にかけて、政府が5万戸以上の注文住宅を供給する計画であり、持ち家の安定的な基盤が強化されています。スタンダード、プラス、プライム・フラットの分類は、補助金と立地価値をリンクさせ、タウンシップ全体でバランスの取れた需要を促します。民間プロジェクトでは現在、商業施設やコミュニティ施設の上に住宅を配置する統合型が好まれており、弾力的なパイプラインの吸収を支えています。

経済のデジタル化に伴い、商業施設は2030年までCAGR 5.13%で最も急速に拡大します。ロジスティクスと工業用資産は、半導体とeコマースのサプライチェーンにおけるシンガポールの役割から恩恵を受ける。一方、投資家はデータセンター・キャンパスや、環境に配慮した分散型オフィスをターゲットにしており、伝統的な小売業やシングルテナント・オフィスにあまり縛られない収益源への軸足を移していることを示しています。このような方向転換が、シンガポール不動産市場の今後の軌跡を支えています。

シンガポール不動産市場レポートは、物件タイプ別(住宅・商業施設)、ビジネスモデル別(販売・賃貸)、エンドユーザー別(個人・一般家庭、法人・中小企業、その他)、地域別(中心地域(CCR)、中心地域以外(RCR)、中心地域以外(OCR))に分類しています。本レポートでは、上記のすべてのセグメントについて、市場規模および予測(米ドル)を提供しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場の洞察と動向

- 市場概要

- 商業用不動産購入動向-社会経済・人口動態に関する洞察

- 賃貸利回り分析

- 資本市場への浸透とREITの存在

- 規制の見通し

- テクノロジーの展望

- 不動産テックと不動産分野で活躍するスタートアップ企業に関する洞察

- 既存および今後のプロジェクトに関する洞察

- 市場促進要因

- 政治的安定と強力な法的枠組みによって推進される外国投資家の強い関心

- 政府主導の都市計画(マスタープラン、グレーターサザンウォーターフロントなど)が長期的な開発を促進している

- 世界の超富裕層からの高級住宅セグメントにおける持続的な需要

- オフィス、コワーキング、複合利用の成長をサポートする地域ビジネスハブとしての戦略的ポジショニング

- 急成長するeコマースと先進製造業が物流と産業用不動産の需要を牽引

- 政府の奨励策により、スマートで持続可能な建築技術の導入が増加

- 市場抑制要因

- 厳しい冷却措置と印紙税が住宅投機投資を抑制する

- 土地供給の制限と土地取得コストの高さが新規開発を制限している

- 地政学的および経済的な逆風が外国資本の流入とテナント需要に影響

- 特定の資産クラスにおける需給の不均衡(例:郊外の小売店や郊外のオフィスビルの供給過剰)

- バリュー/サプライチェーン分析

- 概要

- 不動産開発業者と建設業者- 主要な定量的および定性的な洞察

- 不動産ブローカーとエージェント- 主要な定量的および定性的な洞察

- 不動産管理会社- 主要な定量的および定性的な洞察

- 評価アドバイザリーおよびその他の不動産サービスに関する洞察

- 建築資材業界の現状と主要開発業者とのパートナーシップ

- 市場における主要な戦略的不動産投資家/購入者に関する洞察

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力/占拠者たち

- 供給企業の交渉力(開発者/ビルダー)

- 代替品の脅威

- 競争企業間の敵対関係さ

第5章 市場規模と成長予測(米ドルでの値)

- 物件タイプ別

- 住宅用

- アパートとコンドミニアム

- ヴィラと戸建て住宅

- 商業用

- オフィス

- 小売り

- ロジスティクス

- その他(産業用不動産、ホスピタリティ用不動産など)

- 住宅用

- ビジネスモデル別

- 販売

- レンタル

- エンドユーザー別

- 個人/ 世帯

- 企業・中小企業

- その他

- 地域別

- コアセントラルリージョン(CCR)

- 中央地域の残り(RCR)

- 中部地域外(OCR)

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 企業プロファイル

- CapitaLand

- City Developments Limited

- UOL Group Limited

- Frasers Property Limited

- GuocoLand Limited

- Far East Organization

- Keppel Land

- Mapletree Investments

- Oxley Holdings

- Wing Tai Holdings

- Bukit Sembawang Estates

- Allgreen Properties

- Sim Lian Group

- Hoi Hup Realty

- Tuan Sing Holdings

- Ascendas REIT

- ESR-LOGOS REIT

- Capitaland Integrated Commercial Trust(CICT)

- Frasers Centrepoint Trust

- GLP(Global Logistics Properties)