|

市場調査レポート

商品コード

1938981

マレーシアの不動産:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Malaysia Real Estate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| マレーシアの不動産:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

概要

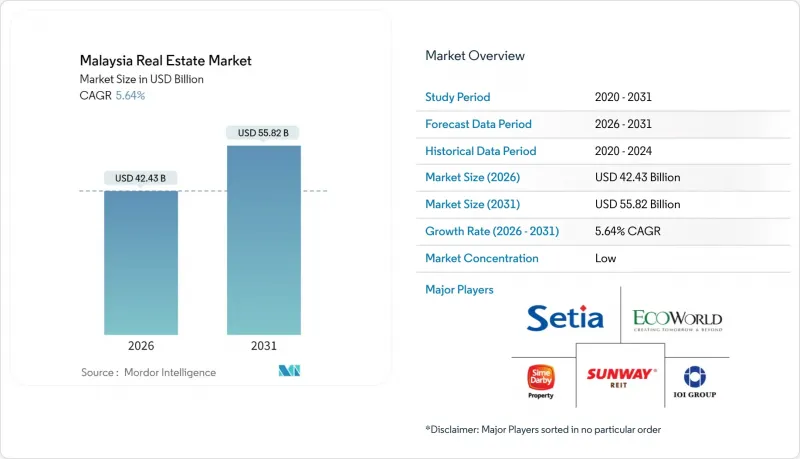

マレーシアの不動産市場は、2025年に401億6,000万米ドルと評価され、2026年の424億3,000万米ドルから2031年までに558億2,000万米ドルに達すると予測されています。

予測期間(2026年~2031年)におけるCAGRは5.64%と見込まれています。

鉄道、高速道路、港湾インフラへの政府支出の継続により、住宅および商業需要が新たに接続された回廊へと向かっています。インテルの70億米ドル規模の工場を筆頭とする半導体設備投資は、工業団地や高スペック物流ハブの着実な吸収につながっています。住宅市場はパンデミック後の軟調さから回復の兆しを見せており、初回購入者向け政策インセンティブや、より広大な土地付き住宅への継続的な移行がこれを支えています。同時に、AIデータセンターや再生可能エネルギープロジェクトへの外国直接投資が商業用資産の需要を拡大しています。交通結節点、港湾後背地、国境ゲートウェイ付近に早期に土地を確保した開発業者は、マレーシアの不動産市場の次の成長波に乗るのに最適な立場にあります。

マレーシアの不動産市場の動向と洞察

インフラ投資が新たな不動産回廊を開拓

インフラ整備がマレーシアの不動産市場に大きな変化をもたらしています。予算111億6,000万米ドルを投じたMRT3サークルラインは、51キロメートル・31駅を延伸し、クアラルンプールを環状に結ぶ路線を確立します。この鉄道拡張と並行し、ウェストポート社は88億米ドルを投資し、ポートクランの取扱能力を2,700万TEUに拡大。これによりクラン物流ベルト沿いの倉庫需要が急増しています。一方、パンボルネオ高速道路と東海岸鉄道リンクは東西軸の接続性を強化し、地方州にまで到達しています。これにより地価上昇を見越した積極的な土地取得が進み、開発業者は2027年以降に開通予定のインターチェンジ拠点周辺で戦略的なタウンシップ開発を計画中です。こうした新たなアクセス環境は、特に注目度が高まる郊外地域を中心に、マレーシアの不動産市場の資産価値上昇を牽引する見込みです。

クランバレー、ペナン、ジョホールにおける都市成長が住宅需要を持続

都市化がマレーシアの不動産市場、特にクランバレー、ペナン、ジョホールにおいて大きな変化をもたらしています。都市化が進むにつれ、経済活動はクランバレー、ペナン、ジョホールにおける公共交通回廊に沿って集中する傾向が強まっています。衛星都市とクアラルンプールの主要就業地域を結ぶMRT2路線は、通勤時間の短縮によりバンダル・スリ・ダマンサラやケポン地区の不動産価値を顕著に向上させました。ペナンでは、バトゥカワン地区に半導体工場の新規進出を背景に、1戸あたり20万9,000米ドルの戸建住宅704戸が供給されました。ジョホールでは、シンガポールとの国境を越えた通勤者を対象とした総額5億8,200万米ドルのブキット・チャガル開発など、ジョホール・シンガポール特別経済区が景観を形成しています。こうした動向は、住宅・小売・物流機能をシームレスに統合した開発への需要が高まっていることを示しています。不動産業者によれば、交通機関の駅より半径500メートル圏内の物件は、最大30%の転売プレミアムが付く可能性があります。こうした動向は、マレーシアの不動産市場において、交通機関を軸とした住宅開発が主要な投資対象として顕著にシフトしていることを示しています。

高層セグメントにおける供給過剰の課題

マレーシアの不動産市場の高層住宅セグメントは、深刻な供給過剰課題に直面しています。2023年第3四半期時点で、未販売在庫は25,311戸、総額38億7,000万米ドルに達しました。特にクアラルンプールでは3,111戸が未販売となり、全体の19.07%を占めています。この問題は価格設定の不一致に起因しています。開発業者は主に11万1,000米ドル以上の物件に注力している一方、実際の需要は6万7,000米ドルから11万1,000米ドルの範囲に集中しているのです。さらに、銀行が投機的プロジェクトへの最終融資を制限したことで、販売の鈍化とマーケティング費用の増加を招いています。パンデミック後の嗜好の変化に対応し、一部企業は土地付き住宅形式へ回帰し、2024年第1四半期に3,127戸を発売しました。しかしながら、在庫消化率が改善するまでは、供給過剰がマレーシアの不動産市場のキャピタルゲインに引き続き重くのしかかると予想されます。

セグメント分析

2025年、マレーシアの不動産市場において分譲住宅は59.45%のシェアを占め、国民の住宅所有意識を反映しました。同年の取引量は311,211戸、取引額は362億1,000万米ドルに達し、このセグメントの規模を裏付けています。固定金利住宅ローンや初回購入者向け印紙税免除の支援を受け、新規分譲物件は堅調な予約実績を維持しています。サイム・ダービー・プロパティなどの開発業者は、2023年以降デジタル予約システムを通じて2,700戸以上(5億7,800万米ドル相当)を販売しました。

賃貸物件は規模こそ小さいもの、2031年までにCAGR6.32%を記録しており、マレーシアの不動産市場で最も高い伸び率を示しています。若年層の専門職は柔軟性を重視し、MRTやLRT駅周辺に集住。交通機関直結型アパートメントでは車不要の生活が実現しています。これらの拠点に拠点を置くコワーキング事業者によれば、通勤時間の短縮によりテナントは年間7,000時間の節約効果を得ていると推定されています。ジョホール州はシンガポールに近接しているため、賃貸利回りがさらに向上しており、国境を越えて通勤する労働者を対象としたサービスアパートメント「Gen Rise」(総開発価値1億2,500万米ドル)は、事前賃貸契約で成功を収めています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察と市場力学

- 市場概要

- 不動産購入動向- 社会経済的・人口統計学的洞察

- 賃貸利回り分析

- 資本市場への浸透とREITの存在感

- 規制の見通し

- テクノロジーの展望

- 不動産セグメントで活動する不動産テックおよびスタートアップ企業に関する洞察

- 既存および今後のプロジェクトに関する洞察

- 市場促進要因

- クランバレー、ペナン、ジョホールにおける都市成長が住宅および複合用途需要を持続

- インフラ投資(MRT/LRT、高速道路、国境を越えた連絡路)による新たな回廊の開拓

- 工業・物流分野の拡大(電気電子産業、ニアショアリング)が土地・倉庫需要を支える

- 外国資本の参入経路とREIT市場による投資参加の支援

- 持続可能で公共交通指向型、スマートな開発への移行が資産の魅力を向上

- 市場抑制要因

- 特定の高層ビルサブマーケットにおける供給過剰と未販売在庫が価格を圧迫

- 政策変更(例:外国人購入者に対する購入制限額/MM2H制度の変更)による投資家の不確実性の生じ方

- 世帯収入の制約と銀行の選択的融資が吸収を抑制

- バリュー/サプライチェーン分析

- 概要

- 不動産開発業者および建設業者- 主要な定量的・定性的洞察

- 不動産ブローカー及びエージェント- 主要な定量的・定性的洞察

- 不動産管理会社- 主要な定量的・定性的洞察

- 評価アドバイザリー及びその他の不動産サービスに関する洞察

- 建材業界の現状と主要デベロッパーとの提携関係

- 市場における主要戦略的不動産投資家・購入者に関する洞察

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力(開発業者/建設業者)

- 代替品の脅威

- 競争企業間の敵対関係の激しさ

第5章 不動産市場規模と成長予測(金額:10億米ドル)

- ビジネスモデル別

- 販売

- 賃貸

第6章 不動産市場(販売モデル)規模及び成長予測(金額:10億米ドル)

- 物件タイプ別

- 住宅

- アパートメント・分譲マンション

- 戸建住宅・土地付き住宅

- 商業

- オフィス

- 小売り

- 物流

- その他(工業用不動産、ホスピタリティ不動産など)

- 住宅

- エンドユーザー別

- 個人/世帯

- 法人・中小企業

- その他

- 主要都市別

- クアラルンプール

- ペナン(ジョージタウン)

- ジョホールバル

- ペタリンジャヤ

- その他のマレーシア

第7章 競合情勢

- 市場集中度

- 戦略的動向

- 企業プロファイル

- Sime Darby Property Berhad

- SP Setia Berhad

- Sunway Berhad(Property Division)

- Eco World Development Group Berhad

- IOI Properties Group Berhad

- UEM Sunrise Berhad

- Mah Sing Group Berhad

- Gamuda Land

- Tropicana Corporation Berhad

- LBS Bina Group Berhad

- GuocoLand(Malaysia)Berhad

- Eastern & Oriental Berhad

- Matrix Concepts Holdings Berhad

- TA Global Berhad

- MK Land Holdings Berhad

- Country Garden Malaysia

- IJM Land Berhad

- Kuala Lumpur Kepong Berhad(Property)

- YTL Land & Development Berhad