|

市場調査レポート

商品コード

1907006

フレキシブル包装:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Flexible Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| フレキシブル包装:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 197 Pages

納期: 2~3営業日

|

概要

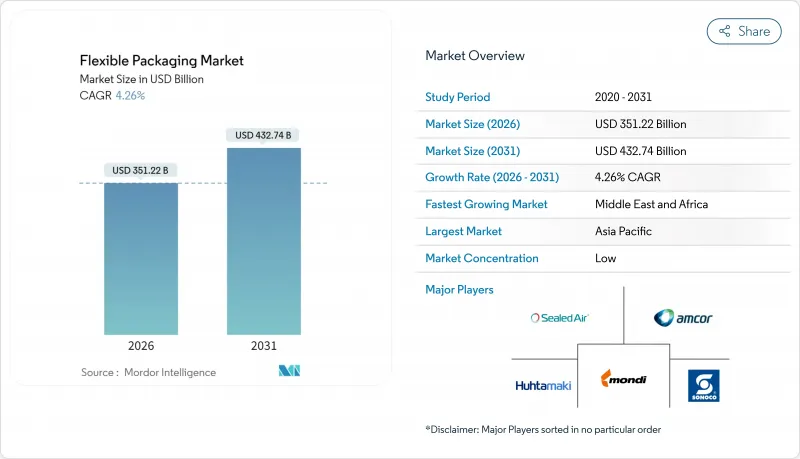

フレキシブル包装市場は、2025年の3,368億7,000万米ドルから2026年には3,512億2,000万米ドルへ成長し、2026年から2031年にかけてCAGR 4.26%で推移し、2031年までに4,327億4,000万米ドルに達すると予測されております。

持続可能性への要求の高まり、電子商取引の急速な拡大、軽量で高バリア性のあるフォーマットに対するブランド側の需要が、フレキシブル包装業界の機会を拡大しています。材料科学の進歩、特に単一素材構造における革新は、埋立地の負担を軽減し、加工業者にとって新たな循環型収益源を開拓しています。デジタル印刷はニッチ製品の発売サイクルを短縮し、ジャストインタイムのワークフローはポリオレフィン価格変動による収益の変動を緩和します。地域別では、アジア太平洋地域の中産階級の拡大と製造規模の拡大がその主導的地位を支えており、一方、中東・アフリカ地域の包装インフラ整備の急成長は、同地域の追い上げ成長を加速させています。

世界のフレキシブル包装市場の動向と洞察

軽量保護用メール便袋に対するEC需要の急増

北米のオンライン販売は2024年に15.4%拡大し、小売業者は容積重量料金を最大30%削減できるフレキシブル気泡緩衝封筒の採用を推進しています。アマゾンがインドで9,100メートルトンのプラスチック削減を実現し、再生紙製クッション袋の普及を拡大している事例は、企業のカーボン削減公約が調達を繊維とフィルムのハイブリッド製品へ導いていることを示しています。コンバーター各社の受注状況は現在、高再生プラスチック含有フィルムを使用した家庭ごみとして回収可能なメール袋を優先しており、米国とメキシコ全域で生産能力の増強が進んでいます。欧州でも適正サイズ化規制の強化に伴い需要が拡大し、アジアの小包ネットワークも同様のコスト効率型フォーマットを導入しています。この相乗効果により、ポリコーティング封筒の需要は持続的に増加し、フレキシブル包装業界は従来のFMCG用途を超えた成長を遂げています。

アジアのFMCGブランドにおける単一素材リサイクル可能フィルムへの移行

インドの2025年度プラスチック廃棄物管理規則では、ブランドオーナーが包装資材の定量的なリサイクル実績を証明することが義務付けられており、主要食品・口腔ケア企業は多層ラミネートからポリオレフィン単一素材フィルムへの切り替えを迫られています。Wipf AGのPPベース「WICOFILM」のようなソリューションは、酸素・香気バリア性を維持しつつ、既存のリサイクル工程に円滑に組み込まれます。ASEAN地域のパーソナルケアブランドも同様の転換を進めており、単一素材のパウチを活用することで小売店の回収制度を満たしつつ、店頭での訴求力を確保しています。供給側のイノベーションはアジア太平洋地域全体に広がり、同地域がフレキシブル包装業界で45.24%のシェアを維持する一助となっています。EPR(拡大生産者責任)費用の大半が年々上昇する中、単一素材の生産能力を拡大するコンバーターは、高収益契約の獲得と利益率の安定化を図れる立場にあります。

変動するポリオレフィン価格がコンバーターの利益率を圧迫

原料価格の変動幅は2024年に二桁に達し、四半期ごとの価格契約に縛られたコンバーターのEBITDAを圧迫しています。アジアにおけるPE・PPの供給過剰と輸送障害が変動幅を拡大させています。利益率への衝撃を和らげるため、主要コンバーターは薄肉フィルムの採用、在庫計画のデジタル化、バイオマス由来ナフサ契約の検討を通じてリスク分散を図っています。この抑制策は一時的なものですが、価格安定性と再生材含有率の高い素材への移行を加速させ、間接的にフレキシブル包装業界の供給基盤を近代化しています。

セグメント分析

ポリエチレンは2025年時点でフレキシブル包装業界の34.12%を占め、低コスト性と防湿特性により食品包装の基幹用途を支えています。樹脂の入手容易性と確立されたリサイクルシステムにより、シリアル用ライナー、冷凍食品用フィルム、洗剤用パウチにおける標準素材としての地位を維持しています。しかしながら、小売業者が家庭用堆肥化可能なプライベートブランド製品を導入し、自治体では有機廃棄物処理プログラムを拡充する中、生分解性・堆肥化可能ポリマーは2026年から2031年にかけて7.65%という最速のCAGRを示しています。この勢いにより、研究開発予算はLDPEの強度を模倣しつつ産業用堆肥化サイクル内で分解されるPLA(ポリ乳酸)およびPHA(ポリヒドロキシアルカン酸)ベースの共押出技術へ再配分されています。紙ラミネートは水蒸気透過性が中程度で求められる分野で再興し、アルミ箔は酸素透過性がほぼゼロであることが要求されるニッチな役割を維持します。EVOHはマイクロレイヤー形態での使用に留まりますが、無菌培養液や栄養補助食品用ゲルには依然として不可欠です。総合的に、素材ポートフォリオは加工性を損なわずにスコープ3排出量を削減するソリューションへ転換しており、フレキシブル包装市場の循環型経済への移行を強化しています。

生分解性素材のフレキシブル包装市場規模は、FMCG(日用消費財)の脱炭素化ロードマップや埋立処分回避費用を背景に、2026年の336億米ドルから2031年には486億米ドルへ拡大が見込まれます。ポリエチレンは依然として使用量で首位を維持していますが、消費者向けカテゴリーで再生材含有量の最低基準が設定されるにつれ、その優位性は徐々に低下すると予想されます。BOPPの透明性と剛性はスナック食品分野での存在感を維持し、CPPのヒートシール信頼性はレトルト包装やツイストラップ包装での採用を保証しています。樹脂メーカーは化学的リサイクル技術への投資を拡大し、ポリプロピレン(PP)やポリエチレン(PE)の単量体を回収。これにより材料性能を維持する真のポリマー・トゥ・ポリマー循環を実現しています。こうした取り組みが拡大する中、加工業者は機械的・化学的・生分解的リサイクル経路が共存する混合ポートフォリオを予測します。各手法がフレキシブル包装業界内の異なるチャネルニーズに対応する見込みです。

パウチは2025年の収益の46.05%を占め、ガラス瓶や缶を70%軽量な形態で代替し、輸送時の排出量を削減する能力が注目されています。スタンドアップパウチは広告スペースを拡大し、調味料やペットフードにおける衝動買いを促進します。高精細インクジェット印刷機の登場により、準備工程の廃棄物が大幅に削減され、季節限定フレーバーのSKU拡充が可能となりました。これによりD2Cブランドやプライベートブランドのリニューアルが支援されています。フィルムやラップは店頭での存在感は低いもの、耐穿刺性を損なわずに厚みを削減したことで、5.61%という最も高いCAGRを記録しています。ナノクレイや酸化ケイ素バリアコーティングがアルミ層に代わり、選別性とリサイクル性を向上させています。

一方、袋・サック分野のフレキシブル包装市場規模は、肥料・セメント・ドッグフード需要に支えられ安定を維持。サシェやスティックパックは、特に外出先での消費が増加する東南アジアを中心に、単回用栄養補助食品やインスタント飲料市場への浸透を続けております。今後5年間において、デジタル印刷機の稼働時間、無溶剤ラミネーション、電子ビーム硬化技術の相互作用により、リードタイムが数週間から数日に短縮されると予想されます。これによりコンバーターは工場レイアウトの再考を迫られるでしょう。最終的には、大規模な外食産業向け生産とインフルエンサーとのコラボレーション向け小ロット生産を柔軟に切り替えられる、俊敏なオペレーションを可能にする製品構成が求められます。

フレキシブル包装市場レポートは、素材タイプ(プラスチック、紙、アルミ箔、生分解性素材)、製品タイプ(パウチ、袋、フィルム、その他)、最終用途産業(食品、飲料、医薬品、化粧品、工業、その他)、流通チャネル(直接、間接)、地域(北米、欧州、アジア太平洋、南米、中東・アフリカ)別に分類されています。市場予測は金額(米ドル)で記載されています。

地域別分析

アジア太平洋地域は、都市化、可処分所得の増加、製造業支援政策により、2025年においてもフレキシブル包装業界の44.70%という圧倒的なシェアを維持しました。中国のスマート工場投資とインドの食品加工向け生産連動型奨励制度(PLI)が、国内の樹脂・フィルム生産能力を支えています。UFlex社はポリエステルチップの生産量を倍増させ、使用済み原料を統合するPCRプラントを稼働させ、循環型供給提案を強化しました。地域のコンバーター各社も、今後導入されるEPR(拡大生産者責任)制度に伴う費用負担に備え、単一素材製品の展開を主導しており、この地域の成長軌道をさらに強化しています。一方、東南アジア諸国は免税貿易クラスターを活用し、スタンドアップパウチの輸出を拡大しており、域内貿易の流れを活発化させています。

北米は第二の重要拠点であり、電子商取引用封筒の採用拡大と医薬品コールドチェーンの成長に牽引されています。小売業者はHow2Recycle認証済みパウチの採用を推進し、PEフィルムのリサイクル性向上を促しています。OEMメーカーはデジタル検査を統合し、FDA基準のトレーサビリティを保証することで市場の健全性を強化しています。欧州はEUプラスチック廃棄物指令(PPWR)を戦略の核とし、化学的リサイクル試験プラントや繊維系フレキシブル包装への資金投入を進めています。モンディ社とフッタマキ社はそれぞれ、リサイクル可能なレトルトラインとブルーループ社のポートフォリオを拡大し、大規模なリサイクル設計原則の組み込みを推進しています。

中東・アフリカ地域は2031年までにCAGR6.03%と最も高い伸びが予測され、サウジアラビアやエジプトにおける外国直接投資(FDI)支援の食品ハブがこれを後押しします。アフリカの包装市場は2031年までに560億2,000万米ドル規模に達する見込みで、うちフレキシブル包装は2033年までに33億8,000万米ドルを超える可能性があります。乾燥気候下での長期保存を可能とするパウチが現代小売チェーンに求められており、高バリアフィルムの輸入を促進しています。南米におけるスペシャルティコーヒーブームは脱気弁付きパウチの需要を強化する一方、通貨変動により軽量なフレキシブル包装産業が硬質ガラスや金属よりも魅力的に映っています。地域を問わず共通する傾向として、規制主導のリサイクル目標がコンバーターの研究開発を統一し、単一素材化に向けたロードマップを推進しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストサポート(3ヶ月間)

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 北米における軽量保護用メール便袋の電子商取引需要急増

- アジアのFMCGブランドがEPR義務対応のため単一素材リサイクル可能フィルムへ移行

- 欧州におけるレトルトパウチの即席食品への急速な普及

- 南米におけるコーヒーおよびスペシャルティ飲料ブランドの高バリアフィルムへの移行

- 化粧品パッケージ向け大量カスタマイズを可能とするデジタル印刷への投資

- コールドチェーン生物製剤ブリスター需要の成長が医薬品フレキシブル包装を促進

- 市場抑制要因

- 変動するポリオレフィン価格がコンバーターの利益率を圧迫

- EUおよび米国における多層ラミネート材のリサイクルインフラの断片化

- 主要新興経済国(例:インド、ケニア)における使い捨てプラスチック規制の強化

- 中東の炭酸飲料セグメントにおけるスタンドアップパウチの普及を阻む硬質PETボトル

- サプライチェーン分析

- 規制の見通し

- テクノロジーの展望

- 貿易シナリオ(関連HSコード別)

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- リサイクルと持続可能性の動向

第5章 市場規模と成長予測

- 材料タイプ別

- プラスチック

- ポリエチレン(PE)

- 二軸延伸ポリプロピレン(BOPP)

- キャスティングポリプロピレン(CPP)

- ポリ塩化ビニル(PVC)

- エチレン・ビニルアルコール(EVOH)

- その他の軟質プラスチック

- 紙

- アルミ箔

- 生分解性および堆肥化可能な材料

- プラスチック

- 製品タイプ別

- パウチ

- バッグおよび袋

- フィルムおよびラップ

- その他の製品タイプ

- 最終用途産業別

- 食品

- 冷凍食品

- 乳製品ベースの商品

- 肉類および魚介類

- 焼き菓子および菓子類

- 生鮮食品

- その他の食品製品

- 飲料

- ジュースおよびネクター

- 乳製品ベースの飲料

- その他の飲料

- 医薬品

- 化粧品およびパーソナルケア

- 産業

- その他の最終用途産業

- 食品

- 流通チャネル別

- 直接販売チャネル

- 間接販売チャネル

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- 北欧諸国

- アジア太平洋地域

- 中国

- 日本

- インド

- ASEAN

- 韓国

- オーストラリア

- ニュージーランド

- 南米

- ブラジル

- アルゼンチン

- チリ

- 中東・アフリカ

- 中東

- アラブ首長国連邦

- サウジアラビア

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ケニア

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 市場シェア分析

- 企業プロファイル

- Amcor plc

- Sealed Air Corporation

- Mondi plc

- Huhtamaki Oyj

- Constantia Flexibles Group GmbH

- Sonoco Products Company

- ProAmpac LLC

- Coveris Management GmbH

- Uflex Ltd.

- Sigma Plastics Group

- Schur Flexibles Holding

- Wipf AG

- Glenroy Inc.

- Printpack Inc.

- Clondalkin Flexible Packaging

- American Packaging Corporation

- FlexPak Services LLC

- Arabian Flexible Packaging LLC

- Gulf East Paper & Plastic Industries LLC

- Plastipak Packaging Inc.