|

市場調査レポート

商品コード

1939069

ベトナムのプラスチック:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Vietnam Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ベトナムのプラスチック:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

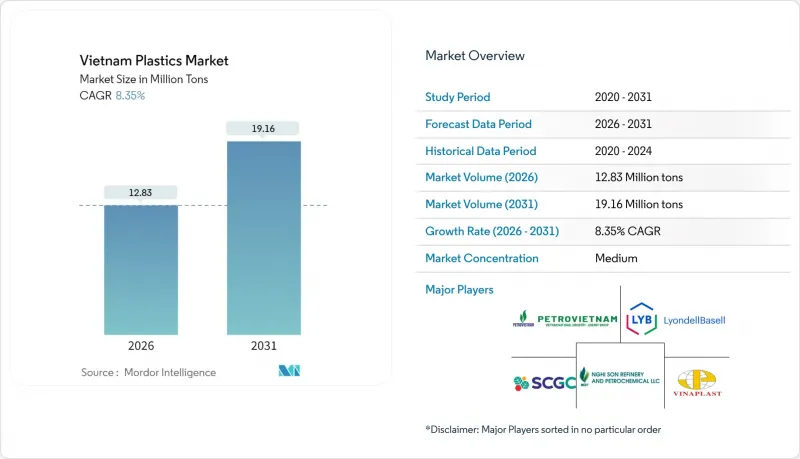

2026年のベトナムプラスチック市場規模は1,283万トンと推定され、2025年の1,184万トンから成長が見込まれます。

2031年までの予測では1,916万トンに達し、2026年から2031年にかけてCAGR8.35%で拡大する見通しです。

堅調な外国直接投資、積極的なインフラ支出、そして断固たる規制の近代化が相まって、ベトナムは東南アジアで最も成長著しいプラスチック産業の拠点としての地位を確立しています。中国からの製造業移転は下流消費を拡大し続けており、建設投資(2025年上半期で前年比40%増)はパイプ、プロファイル、断熱材への安定した需要を生み出しています。現地の加工業者は実験よりも生産量を優先し、急増する受注に対応するため押出ラインの規模拡大を進めています。同時に、持続可能性への要請がバイオプラスチックの採用を加速させ、樹脂サプライヤーは原料の多様化やリサイクル素材の採用を推進しています。ただし、輸入ナフサやプロピレンは依然としてコストに敏感な原料です。

ベトナムプラスチック市場の動向と展望

国内建設プロジェクトの堅調な成長

インフラ支出は、資金執行期間が数週間から1~3日に短縮されたことを受け、2025年上半期に前年比40%増加しました。PVCパイプ、断熱ボード、難燃性ケーブルトレイの需要が急増しており、ベトナムがシンガポール水準より60~65%低いコスト競争力を持つ建設拠点であることを反映しています。工場建設を上回るデータセンタープロジェクトの増加により、ハロゲンフリー化合物や耐熱性エンジニアリング樹脂の需要が高まっています。通達10/2024/TT-BXDにより輸入建材の品質検査が義務付けられ、適合性を証明できる現地コンバーターに有利な政策となっています。これらの動向が相まって、ベトナムプラスチック市場には数量・金額ともに成長がもたらされています。

食品グレード・Eコマース包装需要の急拡大

2024年、ベトナムの食品加工生産高は793億米ドル(前年比7.4%増)に達し、都市部では電子商取引の普及が急拡大しました。この結果、加工メーカーは保存期間を延長するバリアフィルムと、輸送コストを削減する軽量メール便袋という二つの要求に同時に対応する必要があります。電子機器向け保護緩衝材(2025年3月までの部品輸入量は29.3%増加)は、緩衝フォームや成形インサートの需要をさらに押し上げています。国内製造包装材を重視する政府の優遇政策は、調達を国内サプライヤーに誘導し、印刷、ラミネート、多層押出ラインにおける設備投資の促進につながっています。

輸入ナフサ・プロピレンへの高い依存度

ベトナムは2025年1~7月期に550万トン超のプラスチック原料を輸入し、その大半は中国、韓国、台湾からのものでした。SCGのロンソン複合施設は2025年8月に稼働を開始し、140万トンの生産能力を有しますが、それでも国内需要の一部にしか対応できていません。原料費は生産コストの60~70%を占め、原油価格の変動に左右され続けるため、原油価格が急騰すると価格競争力が損なわれます。計画中の7億米ドル規模のエタンアップグレードにより格差は縮小する見込みですが、ガス優位性を持つ湾岸生産者とのコスト競争力確保は依然として困難です。

セグメント分析

2025年時点で、ベトナムプラスチック市場における従来型プラスチックのシェアは51.10%を維持しております。日常的な包装材、パイプ、成形部品に使用されるポリエチレンおよびポリプロピレングレードが中核を成しております。これらの製品は成熟したサプライチェーンと低単価の利点を活かし、継続的な数量面での優位性を確保しております。ポリカーボネートやポリアミドを含むエンジニアリングプラスチックは、高輝度有機EL(有機発光ダイオード)ディスプレイや光学モジュールを輸送する電子機器ラインで需要が拡大しています。ポリウレタンは建設ブームに支えられ、サンドイッチパネルや家具用クッション材として活用されています。

バイオプラスチックは依然としてニッチ市場ではありますが、ブランドオーナーが持続可能性目標を追求し、新規規制が需要を喚起する中、2031年までCAGR12.55%で成長が見込まれます。農業残渣は潜在的な澱粉原料を供給しますが、認証の障壁やプレミアム価格設定により規模拡大は依然として困難です。しかしながら、国際的なアパレルグループ主導のパイロットプログラムは、ベトナムが将来のバイオポリマー生産拠点となる可能性を示しており、2027年以降の転換点を示唆しています。

ベトナムプラスチック市場レポートは、種類別(従来型プラスチック、エンジニアリングプラスチック、バイオプラスチック)、技術別(ブロー成形、押出成形、射出成形、その他技術)、用途別(包装、電気・電子機器、建築・建設、自動車・輸送機器、家庭用品、家具・寝具、その他用途)に分類されています。市場予測は数量(トン)単位で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 国内建設プロジェクトの堅調な成長

- 食品用及び電子商取引包装需要の急増

- 下流樹脂転換分野における外国直接投資の増加

- 自動車・電子機器産業のベトナム移転急増

- 再生樹脂に対する政府の優遇措置

- 市場抑制要因

- 輸入ナフサおよびプロピレンへの依存度の高さ

- 使い捨てプラスチックに対する環境保護活動の活発化

- FMCG分野におけるバイオベース代替品からの競合激化

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替製品・サービスの脅威

- 競合の程度

- 原材料分析

第5章 市場規模と成長予測

- タイプ別

- 従来型プラスチック

- ポリエチレン

- ポリプロピレン

- ポリスチレン

- ポリ塩化ビニル

- エンジニアリングプラスチック

- ポリウレタン

- フッ素樹脂

- ポリアミド

- ポリカーボネート

- スチレン共重合体(ABSおよびSAN)

- 熱可塑性ポリエステル

- その他のエンジニアリングプラスチック

- バイオプラスチック

- 従来型プラスチック

- 技術別

- ブロー成形

- 押出成形

- 射出成形

- その他の技術

- 用途別

- 包装

- 電気・電子

- 建築・建設

- 自動車・輸送機器

- 家庭用品

- 家具・寝具

- その他の用途

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)**/順位分析

- 企業プロファイル

- AGC Inc.

- Billion Industrial Holding Limited

- Far Eastern New Century Corporation

- Hyosung Chemical

- LyondellBasell Industries Holdings B.V.

- NAN YA PLASTICS CORPORATION

- NSRP LLC

- SCG Chemicals Public Company Limited

- SKC

- Toray Industries Inc.

- Vietnam 石油・ガス Group

- Vietnam Polystyrene Co. Ltd

- Vinaplast