|

市場調査レポート

商品コード

1685878

欧州の液体肥料:市場シェア分析、産業動向、成長予測(2025年~2030年)Europe Liquid Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の液体肥料:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

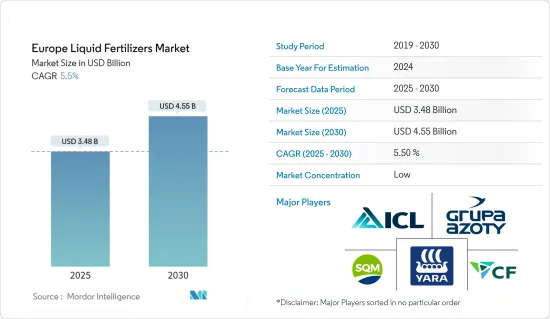

欧州の液体肥料市場規模は2025年に34億8,000万米ドルと推定・予測され、予測期間中(2025年~2030年)のCAGRは5.5%で、2030年には45億5,000万米ドルに達すると予測されています。

欧州の液体肥料市場は、効率的で持続可能な農業への需要の高まりに後押しされ、着実な成長を遂げています。液体肥料は、施用が容易で養分の吸収が速いことが評価され、この地域の農家にとって好ましい選択肢となっています。作物の収量を高め、土壌の肥沃度を向上させ、人口増加による食糧需要の増加に対応する必要性が、こうした肥料の採用をさらに加速させています。国連経済社会局によると、ドイツの人口は2022年の8,410万人から2023年には8,460万人に増加し、生産性を高めて消費者の需要を満たすために液体肥料の大きなニーズが生まれています。その他の特典として、精密農業の技術的進歩により、液体肥料の正確な施用が促進され、無駄の削減と環境への影響の軽減が図られています。

ウクライナ、ドイツ、フランス、英国といった国々は、先進的な農業セクターと近代的農業技術の導入率が高いことから、欧州の液体肥料市場を独占しています。例えば、FAOSTATのデータによると、フランスの硝酸尿素アンモニウム肥料消費量は2022年に190万トンに達し、前年比5.5%増となりました。市場需要に貢献している主な作物には、穀物、油糧種子、果物、野菜などがあり、いずれも液体肥料による栄養効率の恩恵を受けています。

さらに、2022年11月に実施された調査では、ジャガイモ栽培に液体窒素肥料である硝酸尿素アンモニウム(UAN)を施用すると、ロシアでは市場流通可能なジャガイモ収量が6.4%増加し、総収量が最大12.2%増加することが実証されました。2023年、Eurostatは、小規模農家が欧州地域の全農場の70%近くを占めていると報告し、欧州の農業風景において極めて重要な役割を担っていることを強調しました。一般的に10ヘクタール以下の農場は、農村の起業家精神を育み、伝統的な農法を維持するために不可欠です。そのため、これらの農家にとって、液体肥料は収量を向上させるための最も効果的な選択肢となっています。

持続可能性が欧州農業セクターの中心的な焦点となり、液体肥料市場の成長に影響を与えています。環境規制の強化や欧州連合(EU)のグリーン・ディール構想により、二酸化炭素排出量を抑えた環境に優しい肥料の使用が奨励されています。多くの液体肥料は現在、こうした目標に合わせて開発されており、持続可能な農業を支援するためにバイオベースや有機成分を配合しています。この転換は、規制要件を満たすだけでなく、環境に優しい農法を求める消費者の需要にも応えるものです。そのため、環境への有害な影響を最小限に抑えながら生産量を増加させる高効率肥料への継続的な需要に加え、企業の積極的な参加と関与により、このセグメントは予測期間中に徐々に成長すると予想されます。

欧州液体肥料市場の動向

精密農業の重要性の高まりと消費者需要

欧州では、技術革新や精密農業技術などの要因の影響を受けて、液体肥料市場が大きく進化しています。気候条件の変化、人口の増加、耕作可能地の減少による食糧安全保障への懸念の高まりが、同地域における精密農業の導入を後押しする主な要因となっています。液体肥料は現代の農家にさまざまな利点をもたらし、養分の利用可能性に対する作物の反応を改善し、生産性を向上させるためです。

硝酸尿素アンモニウム(UAN)肥料は、植物栄養の液体パワーハウスで、尿素と硝酸アンモニウムを水溶液に混合し、効率的な植物栄養管理に正確に使用されます。国際植物栄養研究所(International Plant Nutrition Institute)は、UANの窒素効力は通常28%から32%であることから、この地域の精密農業で使用される重要な液体肥料であると強調しています。さらに、欧州の尿素硝酸アンモニウム肥料市場では、市場参入企業が市場競争力を維持するために、戦略的パートナーシップを含む様々な戦略を実施しています。2022年、グレート・ヤーマスに本社を置く液体肥料メーカーのブリネフローは、ドイツの著名な肥料メーカーであるHELM AGと戦略的合弁会社を設立しました。トリニダードに液体窒素(UAN)の製造能力を持つHEML AGは、この協力関係を通じて、英国への肥料供給の安全性を高めることを目指しています。このパートナーシップは、サプライチェーンを強化し、欧州市場での競争力を維持しようとする業界の努力を示すものです。

さらに、欧州では都市化によって耕地が徐々に減少しています。この動向により、農家は減少する面積で作物の収量を維持または増加させなければならなくなり、生産性を最適化するための肥料への依存度が高まっています。FAOSTATSのデータによると、欧州における穀物の収穫面積は1億1,670万ヘクタールに達し、前年から3.42%減少しました。トルコは、都市化や工業化によって悪化した耕地面積の減少により、食料安全保障を維持する上で大きな課題に直面しています。こうした問題を軽減するため、トルコ農林省によると、2023年、トルコでは化学肥料の使用量が史上最高を記録し、全国で1,400万トン近くが施用されました。この増加は、利用可能な農地の減少に対抗し、十分な食糧生産を確保するための広範な努力の一環です。

農産物の輸入が増加していることは、この地域における需要の増大と生産量の不足を示しています。例えば、ITC Trade Mapによると、ドイツでは2023年の小麦の輸入量は513万トンに達し、2022年には410万トンでした。耕地面積の減少、輸入の増加、精密農業の採用拡大、農業生産性向上の必要性が、予測期間中の液体肥料市場を牽引すると予想されます。

ロシアが欧州液体肥料市場を独占

ロシアは強力な農業基盤と肥料の大規模生産により、欧州液体肥料市場で重要な役割を果たしています。同国は、尿素硝酸アンモニウム(UAN)溶液を含む窒素ベースの液体肥料の主要生産国であり、これらは欧州の農業生産性にとって不可欠です。例えば、ロシアの大手肥料メーカーであるPhosAgro社のデータによると、同国は6,000万トンの肥料を生産しており、PhosAgro社は2023年に1,100万トンの貢献をしています。

また、ロシアのLife Force LLCは、植物活性成分の革新的な配合を特徴とする液体肥料Life Force Acti Grow Fe/B/Zn/Mnを提供しています。ロシアの農地は都市化や環境問題への取り組みによって減少の一途をたどっており、液体肥料の役割はますます重要になっています。例えば、2022年のロシアにおける稲の収穫面積は16万9,600ヘクタールで、前年に比べ8.94%減少しました。正確な栄養施用が可能な液体肥料を使用することで、ロシアは限られた土地で作物の収量を増やすことを目指しています。

ロシアの農業輸出能力、特に肥料の輸出能力は、国内と欧州の両方のニーズに応えることを可能にしています。欧州の農家が縮小する土地で作物の収量を向上させようとしている中、ロシアの輸出志向戦略は、同国を地域および世界の肥料市場における重要な企業として位置づけています。例えば、ITC貿易地図によると、2023年のロシアからの尿素と硝酸アンモニウムの液体混合物の輸出量は202万5,979トンであり、これは世界で30.9%の金額シェアでした。Rosstatによると、EUにおけるロシアの肥料の最大の買い手はポーランド、フランス、ドイツです。ポーランドは前年比2.7倍、フランスは2023年に輸入量を18%増加させました。

しかし、他国との紛争が続いているため、国内外のサプライチェーンが混乱し、肥料の入手に不確実性が生じています。こうした課題にもかかわらず、ロシアは欧州の液体肥料市場の最前線に立ち続け、革新性と持続可能性に重点を置いて、増大する欧州の農業需要に供給する重要な役割を維持しています。

欧州の液体肥料産業の概要

欧州の液体肥料市場は断片化されており、安定した顧客基盤を維持し、大きな市場シェアを獲得するために、大手企業間の競争が激化しています。市場で最も注目されている企業には、Yara International ASA、ICL Group Ltd.、Grupa Azoty S.A.、CF Industries Holdings, Inc.、Sociedad Quimica y Minera de Chile SA(SQM)などがあります。各社は、欧州液体肥料市場におけるポートフォリオの充実と戦略的地位確立のため、施設の拡張や新製品の開発に注力しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 精密農業の重要性の高まり

- 耕作地の減少

- 政府の支援とイニシアチブの拡大

- 市場抑制要因

- 有機農業の採用増加

- 比較的な高コスト

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 複合型

- ストレート

- 微量栄養素

- 窒素系

- リン酸系

- カリウム

- 二次微量栄養素

- 施用方法

- 施肥

- 葉面散布

- タイプ

- 畑作物

- 園芸作物

- 芝および観賞用作物

- 地域

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- 英国

- ウクライナ

- その他の欧州

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- Yara International ASA

- ICL Group Ltd

- Grupa Azoty S.A.

- BMS Micro-nutrients NV

- CF Industries Holdings, Inc.

- Nordfert

- YILDIRIM Group

- Sociedad Quimica y Minera de Chile SA(SQM)

第7章 市場機会と今後の動向

The Europe Liquid Fertilizers Market size is estimated at USD 3.48 billion in 2025, and is expected to reach USD 4.55 billion by 2030, at a CAGR of 5.5% during the forecast period (2025-2030).

The European liquid fertilizer market has experienced steady growth, propelled by the increasing demand for efficient and sustainable agricultural practices. Liquid fertilizers, valued for their ease of application and rapid nutrient absorption, are becoming a preferred choice for farmers in the region. The need to enhance crop yields, improve soil fertility, and meet the rising food demand of the growing population has further accelerated the adoption of these fertilizers. According to the United Nations, Department of Economic and Social Affairs, Germany's population increased to 84.6 million in 2023 from 84.1 million in 2022, creating a significant need for liquid fertilizers to boost productivity and satisfy consumer demand. Additionally, the market benefits from technological advancements in precision agriculture, which promote the precise application of liquid fertilizers, reducing wastage and environmental impact.

Countries such as Ukraine, Germany, France, and the United Kingdom dominate the European liquid fertilizer market due to their advanced agricultural sectors and higher adoption rates of modern farming techniques. For instance, according to FAOSTAT data, France's urea ammonium nitrate fertilizer consumption reached 1.9 million metric tons in 2022, an increase of 5.5% from the previous year. Key crops contributing to the market demand include cereals, oilseeds, fruits, and vegetables, all of which benefit from the nutrient efficiency offered by liquid fertilizers.

Furthermore, a research study conducted in November 2022 demonstrated that the application of Urea Ammonium Nitrate (UAN), a liquid nitrogenous fertilizer in potato cultivation resulted in a 6.4% increase in marketable potato yield and up to a 12.2% increase in total yield in Russia. In 2023, Eurostat reported that small-scale farmers constituted nearly 70% of all farms in the European region, underscoring their pivotal role in Europe's agricultural landscape. Typically spanning under 10 hectares, these farms are essential for fostering rural entrepreneurship and upholding traditional farming practices. Hence, liquid fertilizer is the most effective option for better yield for these farmers.

Sustainability has become a central focus in the European agricultural sector, influencing the growth of the liquid fertilizer market. Stricter environmental regulations and the European Union's Green Deal initiatives encourage the use of environmentally friendly fertilizers with reduced carbon footprints. Many liquid fertilizers are now developed to align with these goals, incorporating bio-based or organic ingredients to support sustainable farming. This shift not only meets regulatory requirements but also addresses consumer demand for eco-friendly farming practices. Therefore, due to the continued demand for high-efficiency fertilizers to boost production while minimizing harmful impacts on the environment, coupled with the active participation and involvement of players, the segment is anticipated to grow gradually during the forecast period.

Europe Liquid Fertilizer Market Trends

Rising Importance of Precision Farming and Consumer Demand

In Europe, the liquid fertilizers market is evolving significantly, influenced by factors such as technological innovations, and precision agriculture techniques. Rising food security concerns due to changing climatic conditions, increasing population, and decreasing arable land availability are the primary factors bolstering the adoption of precision farming practices in the region. This, in turn, drives the market for liquid fertilizers as they provide an array of benefits to modern farmers that lead to improved crop response to the availability of nutrients and better productivity.

Urea ammonium nitrate (UAN) fertilizer, a liquid powerhouse of plant nutrition, blends urea and ammonium nitrate in an aqueous solution used precisely for efficient plant nutrient management. The International Plant Nutrition Institute highlights its nitrogen potency, typically ranging from 28% to 32%, hence it is an important liquid fertilizer used in precision farming in the region. Moreover, the European urea ammonium nitrate fertilizer market has witnessed the implementation of various strategies by industry participants, including strategic partnerships, to maintain market competitiveness. In 2022, Brineflow, a liquid fertilizer manufacturer headquartered in Great Yarmouth, established a strategic joint venture with HELM AG, a prominent German fertilizer producer. HEML AG, which possesses substantial liquid nitrogen (UAN) manufacturing capabilities in Trinidad, aims to enhance the security of fertilizer supply for the United Kingdom through this collaborative arrangement. This partnership exemplifies the industry's efforts to strengthen supply chains and maintain a competitive edge in the European market.

Furthermore, Europe has experienced a gradual reduction in arable land due to urbanization. This trend compels farmers to maintain or increase crop yields from a diminishing area, thereby increasing their reliance on fertilizers to optimize productivity. According to FAOSTATS data, the harvested area of cereal grains in Europe has reached 116.7 million hectares, a reduction of 3.42% from the previous year. Turkey has faced significant challenges in maintaining food security due to a decrease in arable land, exacerbated by urbanization, and industrialization. To mitigate these issues, in 2023, Turkey recorded the highest usage of chemical fertilizers in its history, with nearly 14 million metric tons applied across the country, according to the Ministry of Agriculture and Forestry, Turkey. This increase is part of a broader effort to counteract the decline in available agricultural land and ensure sufficient food production.

The growing import of agricultural produce further shows the growing demand and insufficient production in the region. For instance, according to the ITC Trade Map, in Germany, the import of wheat in 2023 reached 5.13 million metric tons which was 4.10 million metric tons in 2022. The reduction in arable land, increasing import, and growing adoption of precision agriculture, coupled with the need for increased agricultural productivity, is anticipated to drive the liquid fertilizer market in the forecast period.

Russia Dominates the European Liquid Fertilizers Market

Russia plays a critical role in the European liquid fertilizer market, driven by its strong agricultural base and extensive production of fertilizers. The country is a major producer of nitrogen-based liquid fertilizers, including urea ammonium nitrate (UAN) solutions, which are essential for European agricultural productivity. For instance, according to the data of PhosAgro, a leading fertilizer producer in Russia, the country has produced 60 million metric tons of fertilizers, with PhosAgro contributing 11 million metric tons in 2023.

Additionally, another Russian company Life Force LLC offers Life Force Acti Grow Fe/B/Zn/Mn, a liquid fertilizer featuring an innovative formula of active phytocomponents. As agricultural land in Russia continues to decrease due to urbanization and environmental initiatives, liquid fertilizers' role becomes even more significant. For instance, in 2022 the harvested area for rice was 169.6 thousand hectares in Russia with a reduction of 8.94% compared to the previous year. Using liquid fertilizer, that enables precise nutrient application, the country is aiming to boost crop yields on limited land.

Russia's agricultural export capacity, particularly in fertilizers, allows it to cater to both domestic and European needs. As European farmers seek to improve their crop yields with shrinking land, Russia's export-oriented strategy positions the country as a critical player in the regional and global fertilizer market. For instance, the export quantity of the liquid mixture of urea and ammonium nitrate in 2023 from Russia was 2,025,979 metric tons which was 30.9% value share worldwide according to the ITC trade map. According to Rosstat, the largest buyers of Russian fertilizers in the EU were Poland, France, and Germany. Poland increased its imports 2.7-fold year-on-year, and France increased its imports by 18% in 2023.

However, the ongoing conflict with other nations has disrupted both domestic and international supply chains, creating uncertainty in the availability of fertilizers. Despite these challenges, Russia continues to remain at the forefront of the European liquid fertilizer market, focusing on innovation and sustainability to maintain its critical role in feeding Europe's growing agricultural demands.

Europe Liquid Fertilizer Industry Overview

The European liquid fertilizer market is fragmented, intensifying competition among major players to maintain a stable customer base and capture significant market shares. Some of the most notable companies in the market are Yara International ASA, ICL Group Ltd., Grupa Azoty S.A., CF Industries Holdings, Inc., and Sociedad Quimica y Minera de Chile SA (SQM) among others. The companies have focused on facility expansions and developing new products to enhance their portfolio and strategize their hold in the European liquid fertilizer market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Importance of Precision Farming

- 4.2.2 Decreasing Arable Land

- 4.2.3 Growing Government Support and Initiative

- 4.3 Market Restraints

- 4.3.1 Increase in Adoption of Oragnic Farming

- 4.3.2 Comparative High Cost

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Complex

- 5.2 Straight

- 5.2.1 Micronutrients

- 5.2.2 Nitrogenous

- 5.2.3 Phosphatic

- 5.2.4 Potassic

- 5.2.5 Secondary Macronutrients

- 5.3 Mode of Application

- 5.3.1 Fertigation

- 5.3.2 Foliar Application

- 5.4 Cop Type

- 5.4.1 Field Crops

- 5.4.2 Horticultural Crops

- 5.4.3 Turf and Ornamental Crops

- 5.5 Geography

- 5.5.1 France

- 5.5.2 Germany

- 5.5.3 Italy

- 5.5.4 Netherlands

- 5.5.5 Russia

- 5.5.6 Spain

- 5.5.7 United Kingdom

- 5.5.8 Ukraine

- 5.5.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Yara International ASA

- 6.3.2 ICL Group Ltd

- 6.3.3 Grupa Azoty S.A.

- 6.3.4 BMS Micro-nutrients NV

- 6.3.5 CF Industries Holdings, Inc.

- 6.3.6 Nordfert

- 6.3.7 YILDIRIM Group

- 6.3.8 Sociedad Quimica y Minera de Chile SA (SQM)