|

市場調査レポート

商品コード

1686264

北米の液体肥料:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)North America Liquid Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の液体肥料:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 126 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

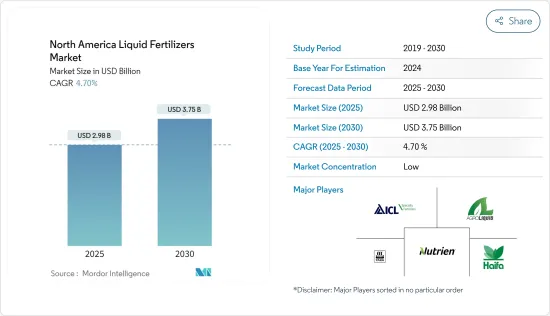

北米の液体肥料の市場規模は2025年に29億8,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは4.7%で、2030年には37億5,000万米ドルに達すると予測されています。

北米地域では、COVID-19の大流行が液体肥料市場に大きな影響を与えています。その結果、北米全域でCOVID-19のパンデミックが蔓延し、労働力不足、原材料の調達、サプライチェーンの混乱をもたらす貿易の制限など、業界のさまざまな側面に影響を与えました。さらに、パンデミックは肥料店を通じて液体肥料業界の流通経路を遮断し、消費者が肥料製品を購入するためにオンライン販売チャネルにシフトする原因となりました。

北米は液体肥料の第2位の消費国と推定されます。同地域では、米国、カナダ、メキシコが液体肥料の最大市場であり、米国が市場を独占しています。北米地域では土地が酸性であり、窒素肥料を使用することで土壌の望ましいpHレベルを維持することができ、これが液体窒素ベース肥料市場の成長を促進する大きな要因の一つとなっています。

北米全域で高効率肥料の需要が増加しており、液体肥料の需要とともに、同地域では今後数年間に増加すると予想されます。高栄養ベースの液体肥料の最近の増加は、生産者の間で作物収量と生産性の増加とともに、市場の主要な促進要因であることが証明されています。

尿素はこの地域で最も広く使用されている液体窒素肥料です。北米液体肥料市場の液体微量栄養素セグメントは急速なペースで成長しており、この成長は食用穀物需要の増加と土壌欠乏症の増加に起因しています。

北米の液体肥料市場動向

持続可能な農業慣行の採用

農業生産の管理は現在、環境の持続可能性への取り組みに重点が置かれており、そのために北米地域では慣行農業に代わるものとして受け入れられている有機農業の採用が増加しており、鉱物肥料が健康問題や環境汚染の原因となっていることから、環境に優しい栽培システムであると考えられています。ファーティライザー・カナダによると、2019年、カナダのトウモロコシ、ダイズ、カノーラ作物専用の土壌サンプルにおいて、生産者による窒素とリンの栄養素の使用率は、高収量カテゴリーで65.8%、次いで中収量で55.6%、低収量で54.8%となっており、作物におけるあらゆる適用モードをカバーする液体肥料の需要を押し上げると思われます。

2020年8月、米国の全米有機プログラム(NOP)は、サプライチェーンに沿った有機原則の監督と遵守を強化することを目的とした米国農務省(USDA)の有機規制の変更を提案し、これは有機製品の生産、取り扱い、マーケティングに影響を与え、それによってこの地域の液体肥料市場における有機成分の成長を促進します。

米国が市場を独占

液体肥料は、北米地域の中で米国での消費量が最大のシェアを占めています。米国で使用されている肥料の4分の1以上が液体肥料です。

米国で液体肥料市場を牽引すると予想される要因は、施肥が容易であることと、液体肥料を充填するための大型ワゴンが利用可能であることです。加えて、精密農業技術の採用率が高いことも市場成長を後押ししています。可変レート技術(VRT)の使用には液体肥料の使用が必要だからです。VRT農法の約77%が肥料を使用しています。しかし、農薬と種子に対するVRT農業の採用率はかなり低く、それぞれ11%と7%と推定されます。VRTで使用される肥料のうち、石灰系肥料のシェアが最も高く、次いで単肥、多肥と続きます。こうした要因から、米国における液体肥料の消費量は予測期間中に高率で増加する可能性があります。

米国ではここ数年、作物生産においてトウモロコシや大豆への液体肥料散布が一般的になっています。2017年にSoybean Management and Research Technology(SMaRT)プロジェクトが実施した調査によると、処方箋に基づく葉面肥料の混合により、20地点中3地点(15%)で大豆収量が増加しました。

北米の液体肥料業界の概要

北米市場はやや統合されており、主要企業が39.7%、その他が60.3%のシェアを占めています。Yara International、Nutrien Ltd、ICL Group、Agro Liquidが調査対象市場の主要企業です。調査期間中に観察された主な発展として、製品の発売と提携が市場の支配的なプレーヤーが最も採用した戦略であり、M&Aがそれに続いています。調査対象市場の主要プレイヤーは、市場での地位を維持するために、地域の他のプレイヤーと提携することで製品ポートフォリオを増やしています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 栄養タイプ

- 窒素

- カリウム

- リン酸塩

- 微量栄養素

- 成分タイプ

- 有機

- 合成

- 使用方法

- スターター液

- 葉面散布

- 施肥

- 土壌への注入

- 空中散布

- 施肥

- 穀物

- 豆類および油糧種子

- 商業作物

- 果物・野菜

- 芝・観葉植物

- 地域

- 米国

- カナダ

- メキシコ

- その他北米地域

第6章 競合情勢

- Most Adopted Competitor Strategies

- 市場シェア分析

- 企業プロファイル

- AgroLiquid

- FoxFarm Soil & Fertilizer Company

- Haifa Group

- Kugler Company

- Nutrien Ltd.

- Planet Natural

- Plant Food Company Inc.

- Sociedad Quimica y Minera(SQM SA)

- Triangle C. C.

- Yara International ASA

第7章 市場機会と今後の動向

第8章 COVID-19の市場への影響評価

The North America Liquid Fertilizers Market size is estimated at USD 2.98 billion in 2025, and is expected to reach USD 3.75 billion by 2030, at a CAGR of 4.7% during the forecast period (2025-2030).

In the North American region, the outbreak of the COVID-19 pandemic has had a significant effect on the liquid fertilizer market. Consequently, the widespread COVID-19 pandemic across North America has impacted various aspects of the industry, such as labor shortages, procurement of raw materials, and restrictions on trade resulting in supply chain disruptions. Further, the pandemic interrupted the distribution channel of the liquid fertilizer industry through fertilizer stores, which caused a shift of consumers toward online sales channels to buy fertilizer products.

North America is estimated to be the second-largest consumer of liquid fertilizers. Within the region, the US, Canada, and Mexico are the largest markets for liquid fertilizer, with the US dominating the market. In the North American region, the lands are acidic, and using nitrogen fertilizers helps maintain the desirable pH level of the soil, which is one of the major drivers for the growth of the liquid nitrogen-based fertilizer market.

The increasing demand for highly efficient fertilizers across North America, along with the demand for liquid fertilizer, is expected to increase during the coming years in the region. The recent rise in high nutrient-based liquid fertilizers, wherein with growing crop yield and productivity among the growers, is proving to be a major driver for the market.

Urea is the most widely used liquid nitrogenous fertilizer in the region. The liquid micronutrient segment of the North American liquid fertilizer market is growing at a rapid pace, and the growth can be attributed to the rising demand for food grains and increasing soil deficiency.

North America Liquid Fertilizer Market Trends

Adoption of Sustainable Agriculture Practices

The management of agricultural production is presently focused on a greater commitment to environmental sustainability, for which the rising adoption of organic agriculture, accepted by the North American region as an alternative to conventional agriculture, appears to be an environmentally friendly growing system since mineral fertilizers are responsible for health problems and environmental pollution. According to Fertilizer Canada, in 2019, the usage of nitrogen and phosphorus nutrients by the growers in the high yield categories for which utilization of 65.8% is used in the high yield category, followed by 55.6% for moderate yield, and 54.8% for low yield in the soil samples exclusively for corn, soybean, and canola crops in Canada, which will boost the demand of the liquid fertilizer for covering all modes of applications in the crops.

In August 2020, the United States of America's National Organic Program (NOP) proposed changes to the US Department of Agriculture (USDA) organic regulation aiming to strengthen oversight and compliance to the organic principles along the supply chain, which will impact the production, handling, and marketing of organic products, thereby, in turn, enhance the growth of the organic ingredients in the liquid fertilizer market in the region.

United States Dominates The Market

Liquid fertilizers hold the largest share of consumption in the United States within the North American region. More than one-fourth of the fertilizers used in the United States are liquid fertilizers.

The factors that are expected to drive the liquid fertilizer market in the United States are the easy application and the availability of large wagons to fill the liquid fertilizers. Additionally, the high adoption of precision agriculture technology is driving market growth, as the use of variable rate technology (VRT) requires the use of liquid fertilizers. Around 77% of VRT farming use fertilizers. However, the adoption of VRT farming for pesticides and seeds is quite low, estimated to be 11% and 7%, respectively. Among the fertilizers used in VRT, lime-based fertilizers have the largest share, followed by single nutrient and multiple nutrient fertilizers. Owing to these factors, the consumption of liquid fertilizers in the United States may increase at a high rate during the forecast period.

Liquid fertilizer applications to corn and soybean plants have become a common practice in crop production during the past few years in the United States. According to the research conducted by the Soybean Management and Research Technology (SMaRT) project in 2017, the prescription-based foliar fertilizer mixture increased soybean yields at three of the 20 sites (15% of the time).

North America Liquid Fertilizer Industry Overview

The North American market is Slightly consolidated, with major players occupying a share of 39.7% and others accounting for 60.3% of the total shares. Yara International, Nutrien Ltd, ICL Group, and Agro Liquid are the key players in the market studied. As per the key developments observed during the review period, product launches and partnerships are the most adopted strategies by the dominant players in the market, followed by mergers and acquisitions. The major players in the market studied are increasing their product portfolio by partnering with other players in the region to maintain their position in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Nutrient Type

- 5.1.1 Nitrogen

- 5.1.2 Potassium

- 5.1.3 Phosphate

- 5.1.4 Micronutrients

- 5.2 Ingredient Type

- 5.2.1 Organic

- 5.2.2 Synthetic

- 5.3 Mode of Application

- 5.3.1 Starter Solution

- 5.3.2 Foliar Application

- 5.3.3 Fertigation

- 5.3.4 Injection into Soil

- 5.3.5 Aerial Application

- 5.4 Application

- 5.4.1 Grains & Cereals

- 5.4.2 Pulses & Oilseeds

- 5.4.3 Commercial Crops

- 5.4.4 Fruits & Vegetables

- 5.4.5 Turf & Ornamentals

- 5.5 Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

- 5.5.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Competitor Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 AgroLiquid

- 6.3.2 FoxFarm Soil & Fertilizer Company

- 6.3.3 Haifa Group

- 6.3.4 Kugler Company

- 6.3.5 Nutrien Ltd.

- 6.3.6 Planet Natural

- 6.3.7 Plant Food Company Inc.

- 6.3.8 Sociedad Quimica y Minera (SQM SA)

- 6.3.9 Triangle C. C.

- 6.3.10 Yara International ASA