欧州の飼料用酸味料:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Europe Feed Acidifiers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 230 Pages

- 納期

- 2~3営業日

- 商品コード

- 1685850

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

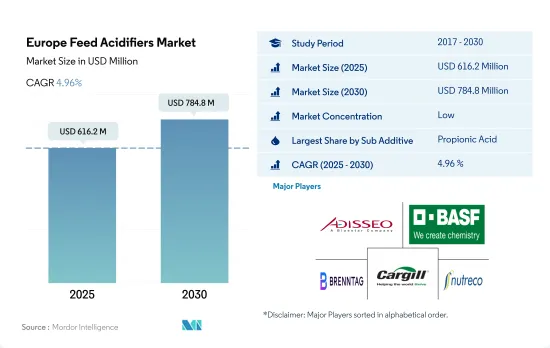

欧州の飼料用酸味料市場規模は2025年に6億1,620万米ドルと推定され、2030年には7億8,480万米ドルに達すると予測され、予測期間(2025年~2030年)のCAGRは4.96%で成長する見込みです。

- 酸味料は飼料の性能を高め、病原性生物や有毒代謝物の取り込みを抑えるため、動物栄養の重要な要素です。欧州では、2022年に酸性化剤市場は飼料添加物市場全体で7.0%のシェアを占め、2017年から2022年の間に市場額は12.9%増加しました。

- この地域で最も広く使用されている酸味料はプロピオン酸で、2022年の市場価値は1億8,270万米ドルであり、このセグメントは予測期間中にCAGR 5%を記録すると予測されています。栄養吸収を改善し、病原性微生物を減少させるため、動物飼料に最適です。

- 家禽は欧州の飼料用酸味料市場で最大の動物種セグメントであり、2022年の市場シェア値の35.4%を占めています。このセグメントは予測期間中にCAGR 5.0%を記録すると予測されています。飼料用酸味料は、成長を促進し、代謝を高め、飼料摂取量を増加させ、有害な病原体に対する抵抗力を与えるために、家禽類に広く使用されています。

- 乳酸とフマル酸は、予測期間中にCAGR 5.1%を記録し、この地域で最も急成長する分野と予想されます。乳酸は、配合飼料に添加することで、動物の消化管の健康、消化率、高い栄養利用率の改善に役立ちます。

- スペイン、ドイツ、フランスは欧州の主要市場であり、2022年の市場シェアは合わせて45.3%でした。スペインのシェアが高いのは、同国の飼料生産量が多いためで、2022年の同地域の飼料生産量全体の12.1%を占めています。飼料生産量の増加と動物栄養における飼料用酸味料の重要性に基づき、予測期間中に同市場のCAGRは4.9%を記録すると予測されています。

- 欧州地域は飼料用酸味料の主要市場の1つであり、飼料用酸味料は動物栄養における飼料性能を向上させ、病原性生物や有毒代謝物の取り込みを減少させる上で重要な役割を果たすからです。2022年現在、飼料用酸味料は金額ベースで欧州飼料添加物市場の7.0%を占め、2017年から2022年の間に12.9%増加しました。

- 欧州地域ではスペイン、ドイツ、フランス、ロシアが飼料用酸味料の主要市場であり、特にスペインは2022年に8,180万米ドルという大きな市場価値を持っています。スペインのシェアが高いのは、2022年の飼料生産量が前年比2.5%増加したためです。スペインの市場価値は2029年に1億1,640万米ドルに達すると予測され、予測期間中のCAGRは5.2%です。

- ドイツも飼料用酸味料の主要市場で、2022年の市場価値は8,140万米ドルです。これは予測期間中にCAGR 4.6%を記録すると予測されています。この成長は、ドイツにおける飼料生産が2020年から2022年の間に0.9%増加することに起因しています。

- 予測期間中、欧州地域の飼料用酸味料市場では英国がCAGR 5.8%で最も急成長すると予測されています。これは同国における家畜人口と飼料生産の増加によるもので、2017年から2022年にかけて飼料総生産量は4.7%増加します。

- 飼料生産と家畜人口の増加が欧州地域の市場促進要因です。2022年現在、欧州の飼料総生産量は2億6,290万トンで、2017年から2.0%増加しました。その結果、同市場は予測期間中にCAGR 4.9%を記録すると予測されます。

欧州の飼料用酸味料市場動向

欧州は第3位の家禽肉輸出国であり、ブロイラー肉生産は家禽肉生産の82.6%を占め、これが家禽肉生産の需要を促進すると予想される

- 欧州は世界有数の鶏肉生産・輸出国であり、2021年の年間鶏肉生産量は約1,340万トンと推定されています。一人当たり年間26.9kgと、同地域で2番目に食肉が消費されているにもかかわらず、欧州の鶏肉生産量は世界の需要増に追いついていないです。欧州地域で最大の鶏肉生産国は、ポーランド(生産量の19.2%、250万トン)、フランス(12.5%、160万トン)、スペイン(12.3%)、ドイツ(12%)、イタリア(10.4%)です。

- EU域内では、ブロイラー肉生産が2021年の家禽肉生産全体の大半(82.6%)を占め、次いでアヒル肉が3.3%でした。2021年の欧州の鶏群数は約24億5,000万羽で、ロシア、フランス、オランダ、ウクライナ、ポーランド、英国が合計で50%以上を占める。レイヤーのサブセグメントは、卵消費の増加により欧州全域で成長を遂げており、2017年の5,864トンから2021年には613万5,000トンに増加します。

- 家禽肉の第4位の輸入国、第3位の輸出国である欧州は、世界の家禽肉市場における重要な参入企業です。2021年、欧州連合はおよそ225万2,000トン(枝肉重量)の家禽肉を英国、ガーナ、ウクライナなど様々な国に輸出しました。家禽類の生産量の増加、家禽製品の需要の増加、卵の消費量の増加が欧州の市場成長の主な促進要因になると予想されます。

82%を占める養魚用飼料の高い需要と水産物の輸入急増が養殖用配合飼料にマイナスの影響

- 2022年には、欧州は世界の養殖用配合飼料生産において8.0%という大きなシェアを占め、生産量は450万トンに達しました。配合飼料生産量は2018年から2022年にかけて15%の顕著な増加を見たが、これは疾病リスクを低減し飼料効率を向上させるための栄養バランス飼料に対する需要の高まりによるものです。しかし、養殖飼料生産は2018年に21.2%の減少を観測し、これは水産物輸入の急増と輸入水産物価格が比較的低いことが影響したと考えられ、2018年の欧州配合飼料市場に影響を与えました。

- 欧州の主要養殖飼料生産国は、トルコ、英国、オランダ、スペイン、イタリア、フランスであり、この地域の2021年の養殖種の生産量は1,740万トンで、2018年から1.7%の成長を示しています。この成長は、人口と一人当たりの水産物消費量の増加によるもので、これが同地域の養殖生産を牽引しています。このことは、ひいては配合飼料の需要を促進し、予測期間(2023年~2029年)中に18.2%増加する見込みです。

- 水産養殖飼料生産は魚類飼料が圧倒的に多く、2022年のシェアは82%を占め、次いでエビ飼料が4.3%、その他の水生種飼料が13.7%でした。魚の餌は、この地域で最も消費されている水産食品であり、他の水産種に比べて生産量が多いです。水産養殖産業の拡大、水産物および水産養殖製品への需要の高まり、食肉の品質に関する意識の高まりが、調査した市場の成長を増大させる主な要因です。

欧州の飼料用酸味料産業の概要

欧州の飼料用酸味料市場は細分化されており、上位5社で37.31%を占めています。この市場の主要企業は以下の通りです。 Adisseo, BASF SE, Brenntag SE, Cargill Inc. and SHV(Nutreco NV).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 動物頭数

- 家禽

- 反芻動物

- 豚

- 飼料生産

- 水産養殖

- 家禽

- 反芻動物

- 養豚

- 規制の枠組み

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- トルコ

- 英国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- サブ添加物

- フマル酸

- 乳酸

- プロピオン酸

- その他の酸味料

- 動物

- 水産養殖

- サブアニマル別

- 魚類

- エビ

- その他の養殖種

- 家禽類

- 小動物別

- ブロイラー

- レイヤー

- その他の鳥類

- 反芻動物

- 小動物別

- 肉牛

- 乳牛

- その他の反芻動物

- 豚

- その他の動物

- 水産養殖

- 国名

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- トルコ

- 英国

- その他の欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- Adisseo

- Alltech, Inc.

- BASF SE

- Borregaard AS

- Brenntag SE

- Cargill Inc.

- Kemin Industries

- MIAVIT Stefan Niemeyer GmbH

- SHV(Nutreco NV)

- Yara International ASA

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要洞察

- データパック

- 用語集

目次

Product Code: 48525

The Europe Feed Acidifiers Market size is estimated at 616.2 million USD in 2025, and is expected to reach 784.8 million USD by 2030, growing at a CAGR of 4.96% during the forecast period (2025-2030).

- Acidifiers are a crucial component of animal nutrition as they enhance feed performance and reduce the uptake of pathogenic organisms and toxic metabolites. In Europe, the acidifiers market held a share of 7.0% in the total feed additives market in 2022, with a market value increase of 12.9% between 2017 and 2022.

- Propionic acid was the most widely used acidifier in the region, with a market value of USD 182.7 million in 2022, and the segment is projected to record a CAGR of 5% during the forecast period. It improves nutrient absorption and reduces pathogenic microbes, making it an ideal choice for animal feed.

- Poultry is the largest animal type segment in the European feed acidifiers market, and it accounted for 35.4% of the market share value in 2022. The segment is projected to register a CAGR of 5.0% during the forecast period. Feed acidifiers are extensively used in poultry birds to promote growth, increase metabolism, increase feed intake, and provide resistance to harmful pathogens.

- Lactic acid and fumaric acid are expected to be the fastest-growing segments in the region, recording a CAGR of 5.1% during the forecast period. Lactic acid helps improve gastrointestinal tract health in animals, digestibility, and high nutrient utilization when added to the compound feed.

- Spain, Germany, and France are the major markets in Europe, and they together held a market share of 45.3% in 2022. Spain's higher share was attributed to the country's higher feed production, with 12.1% of the total feed production in the region in 2022. Based on increased feed production and the importance of feed acidifiers in animal nutrition, the market is projected to record a CAGR of 4.9% during the forecast period.

- The European region is one of the key markets for feed acidifiers, as it plays a crucial role in improving feed performance in animal nutrition and reducing the uptake of pathogenic organisms and toxic metabolites. As of 2022, feed acidifiers accounted for 7.0% of the European feed additives market in terms of value, and they increased by 12.9% between 2017 and 2022.

- Spain, Germany, France, and Russia are the major markets for feed acidifiers in the European region, with Spain, in particular, holding a significant market value of USD 81.8 million in 2022. The high share of Spain was due to the increased feed production by 2.5% in 2022 compared to the previous year. Spain's market value is anticipated to reach USD 116.4 million in 2029, with a CAGR of 5.2% during the forecast period.

- Germany is also a major market for feed acidifiers, with a market value of USD 81.4 million in 2022. This is projected to register a CAGR of 4.6% during the forecast period. This growth is attributed to the increased feed production in Germany by 0.9% between 2020 and 2022.

- The United Kingdom is expected to be the fastest-growing country in the feed acidifiers market in the European region during the forecast period, with a CAGR of 5.8%. This is due to the increased livestock population and feed production in the country, with total feed production increasing by 4.7% between 2017 and 2022.

- The increased feed production and livestock population are the key drivers for the market in the European region. As of 2022, the total feed production in Europe was 262.9 million metric tons, which increased by 2.0% from 2017. Consequently, the market is anticipated to register a CAGR of 4.9% during the forecast period.

Europe Feed Acidifiers Market Trends

Europe is 3rd largest exporter of poultry meat and broiler meat production accounted for 82.6% of poultry meat production which is expected to drive the demand for poultry production

- Europe is a prominent global poultry meat producer and exporter, and it had an estimated annual poultry meat production of approximately 13.4 million metric tons in 2021. Despite being the second-most consumed meat in the region at 26.9 kg per capita per year, European poultry production has not kept pace with rising global demand. The largest poultry meat producers in the European region include Poland (accounting for 19.2% of production, or 2.5 million metric tons), France (12.5%, or 1.6 million metric tons), Spain (12.3%), Germany (12%), and Italy (10.4%).

- Within the European Union, broiler meat production constituted the majority (82.6%) of total poultry meat production in 2021, followed by duck meat at 3.3%. Europe's poultry flock numbered approximately 2.45 billion birds in 2021, with Russia, France, the Netherlands, Ukraine, Poland, and the United Kingdom collectively comprising more than 50% of the population. The layer sub-segment is experiencing growth across Europe due to increased egg consumption, which rose to 6,135 thousand metric tons in 2021 from 5,864 metric tons in 2017.

- As the fourth-largest importer and the third-largest exporter of poultry meat, Europe is a significant participant in the global poultry meat market. In 2021, the European Union exported roughly 2,252 thousand metric tons (carcass weight) of poultry meat to various countries, including the United Kingdom, Ghana, and Ukraine. The rising production of poultry birds, increasing demand for poultry products, and growing consumption of eggs are expected to be the key drivers of market growth in Europe.

High demand for fish feed which accounted for 82% and surge in seafood imports had a negative impact on compound feed for aquaculture

- In 2022, Europe held a significant share of 8.0% in the global aquaculture compound feed production, with a production volume of 4.5 million metric tons. Compound feed production saw a notable increase of 15% between 2018 and 2022, driven by the growing demand for nutrient-balanced feed to reduce disease risk and improve feed efficiency. However, aquaculture feed production observed a decline of 21.2% in 2018, which may have been influenced by the surge in seafood imports and the relatively low prices of imported seafood, impacting the European compound feed market in 2018.

- The major aquaculture feed producers in Europe are Turkey, the United Kingdom, the Netherlands, Spain, Italy, and France, and the region produced 17.4 million metric tons of aquaculture species in 2021, indicating a growth of 1.7% since 2018. The growth was attributed to the rise in population and per capita seafood consumption, which is driving aquaculture production in the region. This, in turn, propels the demand for compound feed, which is expected to increase by 18.2% during the forecast period (2023-2029).

- Fish feed dominated aquaculture feed production, accounting for 82% share in 2022, followed by shrimp feed and other aquatic species feed, with shares of 4.3% and 13.7%, respectively, in the region. Fish food is the most consumed aquatic food across the region, and it is highly produced in comparison to other aquatic species. The expanding aquaculture industry, the rising demand for seafood and aquaculture products, and the growing awareness regarding quality meat are the major factors augmenting the growth of the market studied.

Europe Feed Acidifiers Industry Overview

The Europe Feed Acidifiers Market is fragmented, with the top five companies occupying 37.31%. The major players in this market are Adisseo, BASF SE, Brenntag SE, Cargill Inc. and SHV (Nutreco NV) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Animal Headcount

- 4.1.1 Poultry

- 4.1.2 Ruminants

- 4.1.3 Swine

- 4.2 Feed Production

- 4.2.1 Aquaculture

- 4.2.2 Poultry

- 4.2.3 Ruminants

- 4.2.4 Swine

- 4.3 Regulatory Framework

- 4.3.1 France

- 4.3.2 Germany

- 4.3.3 Italy

- 4.3.4 Netherlands

- 4.3.5 Russia

- 4.3.6 Spain

- 4.3.7 Turkey

- 4.3.8 United Kingdom

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Sub Additive

- 5.1.1 Fumaric Acid

- 5.1.2 Lactic Acid

- 5.1.3 Propionic Acid

- 5.1.4 Other Acidifiers

- 5.2 Animal

- 5.2.1 Aquaculture

- 5.2.1.1 By Sub Animal

- 5.2.1.1.1 Fish

- 5.2.1.1.2 Shrimp

- 5.2.1.1.3 Other Aquaculture Species

- 5.2.2 Poultry

- 5.2.2.1 By Sub Animal

- 5.2.2.1.1 Broiler

- 5.2.2.1.2 Layer

- 5.2.2.1.3 Other Poultry Birds

- 5.2.3 Ruminants

- 5.2.3.1 By Sub Animal

- 5.2.3.1.1 Beef Cattle

- 5.2.3.1.2 Dairy Cattle

- 5.2.3.1.3 Other Ruminants

- 5.2.4 Swine

- 5.2.5 Other Animals

- 5.2.1 Aquaculture

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Netherlands

- 5.3.5 Russia

- 5.3.6 Spain

- 5.3.7 Turkey

- 5.3.8 United Kingdom

- 5.3.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Adisseo

- 6.4.2 Alltech, Inc.

- 6.4.3 BASF SE

- 6.4.4 Borregaard AS

- 6.4.5 Brenntag SE

- 6.4.6 Cargill Inc.

- 6.4.7 Kemin Industries

- 6.4.8 MIAVIT Stefan Niemeyer GmbH

- 6.4.9 SHV (Nutreco NV)

- 6.4.10 Yara International ASA

7 KEY STRATEGIC QUESTIONS FOR FEED ADDITIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

欧州の飼料用酸味料:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 230 Pages

- 納期

- 2~3営業日