飼料用酵母:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Feed Yeast - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 386 Pages

- 納期

- 2~3営業日

- 商品コード

- 1685841

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

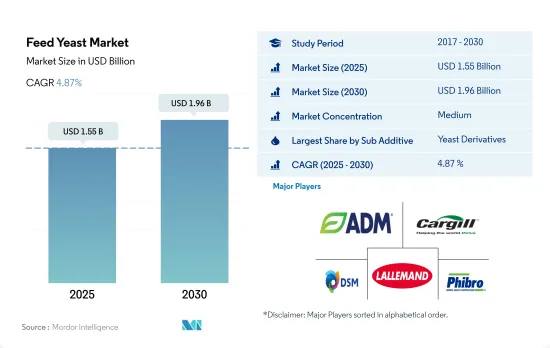

飼料用酵母の市場規模は2025年に15億5,000万米ドルと推計され、2030年には19億6,000万米ドルに達し、予測期間(2025-2030年)のCAGRは4.87%で成長すると予測されています。

- 世界の飼料用酵母市場は、飼料用酵母培養物が動物の健康と生産性に好影響を与えることから、近年著しい成長を遂げています。飼料用酵母は2022年に世界の飼料添加物市場の3.1%を占めました。飼料用酵母の主な利点の1つは、セルロースを分解し消化を改善する胃内の有用細菌の増殖を促進することです。

- アジア太平洋地域は世界最大の飼料用酵母市場で、2022年の市場シェアの31.4%を占めました。次いで北米が25.4%、欧州が23.5%を占めています。アジア太平洋のシェアが高いのは、添加物の普及率が高いことと、動物人口が多いことによる。

- 酵母誘導体は動物が最もよく消費する飼料用酵母であり、2022年には4億9,000万米ドルを占めました。使用済み酵母は市場で第2位のシェアを占めています。酵母は体重と飼料効率を改善し、健康と免疫力の維持に役立ちます。

- 家禽類は飼料用酵母を消費する最大の動物タイプであり、2022年に世界の飼料用酵母市場の45.1%を占めました。家禽類の成長と生産性において酵母は重要な役割を果たすからです。

- 予測期間中、ホエイイーストはCAGR 5.2%で最も急成長する飼料用酵母になると予想されます。ホエー酵母はルーメン発酵を変化させるために使用され、栄養消化を改善し、ルーメンアシドーシスのリスクを低減し、動物の成績を向上させる。

- 世界の飼料用酵母市場は成長を続け、予測期間中にCAGR 4.8%を記録すると予想されます。この成長の原動力は動物飼料産業の成長です。動物の健康と生産性に対する飼料用酵母の利点は、今後もその需要を牽引し続けると予想されます。

- 飼料酵母セグメントは世界の飼料添加物市場において重要なセグメントであり、腸内細菌叢を改善することで腸の抗菌活性を高め、動物の成長を促進する上で重要な役割を果たしています。2022年、飼料用酵母セグメントは世界の飼料添加物市場の4.1%を占めました。

- アジア太平洋は2022年に4億米ドルの市場価値を持つ最大の飼料用酵母市場であり、その高い普及率と2022年に5億トンとなった飼料生産に牽引されました。米国は、広範な商業的畜産と同国の畜産農場における新しい生産慣行の採用により、2022年の市場規模が2億5,000万米ドルとなり、市場の18.9%を占める最大国に浮上しました。中国とブラジルは、配合飼料生産量が多いため、2022年の世界の飼料用酵母市場のそれぞれ14.5%と6.6%を占めています。

- 米国は世界の飼料用酵母市場で最も急成長している国です。抗生物質の代替品としての酵母の需要の増加と飼料効率を高める能力により、予測期間中にCAGR 6.3%を記録すると予想されます。

- 腸内の毒素に対する酵母の抗菌性能により、腸の健康が増進され、飼料効率が向上するため、2022年の世界の飼料用酵母市場では、家禽が45.2%、豚が25%を占め、最大の動物種でした。

- 世界の飼料用酵母市場は、抗生物質の代替としての酵母の能力と飼料効率を高める能力により、予測期間中に4.8%のCAGRで推移すると予想され、それによりコストを削減し、動物の成長率を向上させる。

世界の飼料用酵母市場動向

動物性タンパク質や卵などの家禽製品への高い需要と家禽セクターへの投資の増加により家禽人口が増加しています。

- 家禽の飼育頭数は近年大幅に増加しており、その主な理由は毎日の食事における鶏肉と卵の需要の高まりです。鶏肉製品へのシフトは、米国における豚肉など他の食肉の価格上昇によってもたらされました。欧州の鶏卵消費量は2017年から2021年にかけて4.6%増加し、2021年には6,135トンを占める。

- アジア太平洋は最大の家禽類生産国で、2022年の生産量は2017年比で6.6%増加します。家禽生産量の増加は、アフリカ豚熱の発生により豚肉の供給が減少したことに伴う動物性タンパク質への需要の高まりによるものです。中国は世界の生産量の40%を占め、9億羽以上の採卵鶏を飼養しており、最大のレイヤー養鶏センターでは年間6,000万羽のヒナを孵化させることができます。

- 中東は予測期間中(2023~2029年)、鶏肉生産の成長が見込まれます。サウジアラビアのAlmaraiのような企業はこのセクターに多額の投資を行っており、生産拡大のための新農場設立に11億2,000万米ドルを投じています。

- 鶏肉製品の需要増は、鶏肉セクターへの投資増と相まって、飼料生産の成長を強化すると予想されます。この成長は、予測期間中の世界市場における飼料添加物の需要を促進すると予想されます。全体として、鶏肉業界は、鶏肉製品へのシフトと同部門への投資の増加により、今後数年間で大きく成長する構えです。

アジア太平洋と南米における水産物の消費需要の増加と政府の取り組みにより、養殖種用の飼料生産が増加しています。

- 養殖業の拡大により飼料需要が急増しており、これが配合飼料生産の成長を牽引しています。2022年、配合飼料生産量は前年比13.1%増、養魚飼料生産量は2017年から2022年にかけて46.3%増。魚用飼料の消費増は、水産物の需要増に対応するため、水産動物の性能を維持・向上させ、生産性を高める必要性が背景にあります。

- アジア太平洋地域では魚の消費と生産が盛んであるため、2022年には魚用飼料が世界市場の73.2%を占めました。世界市場におけるシェアでは、魚類に次いでエビとその他の水生種が続きます。エビは欧米諸国が他地域から大量に輸入しています。増大する水産物の需要を満たすため、各国は養殖生産の拡大に力を入れています。インドは漁業省への予算配分を2020年の1億1,410万米ドルから2021年には1億6,880万米ドルに増やし、生産量を増やしており、予測期間中に飼料需要を押し上げると予想されます。

- 南米でも飼料生産が増加しており、養殖の拡大により2022年には2017年から46.4%増の510万トンに達します。同地域は主要な水産物消費地域の1つであり、水産物需要の増加が養殖生産の成長を促進しています。

- 増大する需要に対応するために養殖が拡大し続ける中、業界の開発とその拡大に注力することが、飼料生産の成長を促進すると予想されます。このような水生種向けの飼料生産の増加は、予測期間中の水生セグメントの成長を助けると予想されます。

飼料用酵母産業の概要

飼料用酵母市場は適度に統合されており、上位5社で44.35%を占めています。この市場の主要企業は以下の通りです。Archer Daniel Midland Co., Cargill Inc., DSM Nutritional Products AG, Lallemand Inc. and Phibro Animal Health Corporation(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 動物頭数

- 家禽

- 反芻動物

- 豚

- 飼料生産

- 水産養殖

- 家禽

- 反芻動物

- 養豚

- 規制の枠組み

- オーストラリア

- ブラジル

- カナダ

- 中国

- フランス

- ドイツ

- インド

- イタリア

- 日本

- メキシコ

- オランダ

- フィリピン

- ロシア

- 南アフリカ

- スペイン

- タイ

- トルコ

- 英国

- 米国

- ベトナム

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- サブ添加物

- 生酵母

- セレン酵母

- 使用済み酵母

- トルラ乾燥酵母

- ホエイ酵母

- 酵母誘導体

- 動物

- 水産養殖

- サブ動物別

- 魚類

- エビ

- その他の養殖種

- 家禽類

- サブ動物別

- ブロイラー

- レイヤー

- その他の鳥類

- 反芻動物

- サブ動物別

- 肉牛

- 乳牛

- その他の反芻動物

- 豚

- その他の動物

- 水産養殖

- 地域

- アフリカ

- 国別

- エジプト

- ケニア

- 南アフリカ

- その他のアフリカ

- アジア太平洋

- 国別

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- フィリピン

- 韓国

- タイ

- ベトナム

- その他アジア太平洋地域

- 欧州

- 国別

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- トルコ

- 英国

- その他欧州

- 中東

- 国別

- イラン

- サウジアラビア

- その他中東

- 北米

- 国別

- カナダ

- メキシコ

- 米国

- その他北米地域

- 南米

- 国別

- アルゼンチン

- ブラジル

- チリ

- その他南米諸国

- アフリカ

第6章 競合情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- Alltech, Inc.

- Archer Daniel Midland Co.

- Associated British Foods plc

- Cargill Inc.

- DSM Nutritional Products AG

- Innov Ad NV/SA

- Kemin Industries

- Lallemand Inc.

- Novus International, Inc.

- Phibro Animal Health Corporation

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要洞察

- データパック

- 用語集

目次

The Feed Yeast Market size is estimated at 1.55 billion USD in 2025, and is expected to reach 1.96 billion USD by 2030, growing at a CAGR of 4.87% during the forecast period (2025-2030).

- The global feed yeast market has seen significant growth in recent years due to the positive impact of feed yeast cultures on animal health and productivity. Feed yeast accounted for 3.1% of the global feed additives market in 2022. One of the key benefits of feed yeast is that it enhances the growth of helpful bacteria in the stomach that break down cellulose and improve digestion.

- The Asia-Pacific region was the largest market for feed yeast in the world, accounting for 31.4% of the market share in 2022. This was followed by North America and Europe, which accounted for 25.4% and 23.5% of the market, respectively. The higher share of Asia-Pacific was due to the higher penetration rates of additives and a larger animal population.

- Yeast derivatives were the most commonly consumed feed yeast by animals, accounting for USD 0.49 billion in 2022. Spent yeast held the second-largest share in the market. Yeast improves body weight and feed efficiency and helps in the maintenance of health and immunity.

- Poultry birds were the largest animal type that consumed feed yeast, accounting for 45.1% of the global feed yeast market in 2022, as yeast plays a crucial role in the growth and productivity of poultry birds.

- During the forecast period, whey yeast is expected to be the fastest-growing feed yeast, with a CAGR of 5.2%. Whey yeast is used to alter rumen fermentation, which improves nutrient digestion, reduces the risk of rumen acidosis, and improves animal performance.

- The global feed yeast market is expected to continue growing, registering a CAGR of 4.8% during the forecast period. This growth is driven by growth in the animal feed industry. The benefits of feed yeast for animal health and productivity are expected to continue driving its demand in the future.

- The feed yeast segment is an important segment in the global feed additive market, as it plays a vital role in enhancing the antimicrobial activity of the gut and promoting animal growth by improving intestinal microbiota. In 2022, the feed yeast segment accounted for 4.1% of the global feed additive market.

- Asia-Pacific was the largest market for feed yeast in 2022, with a market value of USD 0.4 billion, driven by its higher penetration rate and feed production, which stood at 0.5 billion metric tons in 2022. The United States emerged as the largest country, accounting for 18.9% of the market in 2022, with a value of USD 0.25 billion due to extensive commercial animal cultivation and the country's adoption of new production practices in its animal farms. China and Brazil accounted for 14.5% and 6.6%, respectively, of the global feed yeast market in 2022, owing to their higher compound feed production.

- The United States is the fastest-growing country in the global feed yeast market. It is expected to record a CAGR of 6.3% during the forecast period due to the increasing demand for yeast as an antibiotic substitute and its ability to increase feed efficiency.

- Poultry birds and swine were the largest animal types in the global feed yeast market, accounting for 45.2% and 25%, respectively, in 2022 due to the antimicrobial performance of yeast on toxins in the gut, which enhances intestinal health and increases feed efficiency.

- The global feed yeast market is expected to record a CAGR of 4.8% during the forecast period due to the ability of yeast to serve as a substitute for antibiotics and its ability to increase feed efficiency, thereby reducing costs and improving animal growth rates.

Global Feed Yeast Market Trends

High demand for animal protein and poultry products such as eggs with increasing investment in poultry sector is increasing poultry population

- The poultry population has witnessed a significant increase in recent years, primarily due to the growing demand for chicken meat and eggs in daily diets. The shift toward poultry products has been driven by the increasing prices of other meat, such as pig meat, in the United States. The consumption of eggs in Europe increased by 4.6% between 2017 and 2021, accounting for 6,135 metric ton in 2021.

- Asia-Pacific is the largest producer of poultry birds, with production increasing by 6.6% in 2022 compared to 2017. The rise in poultry production is due to the growing demand for animal protein following the outbreak of African swine fever, which reduced the supply of pork meat. China accounts for 40% of global production and has more than 900 million stock-laying hens, and the largest layer poultry farming center can hatch 60 million chicks per year.

- The Middle East is expected to witness growth in poultry production during the forecast period (2023-2029). Companies such as Almarai in Saudi Arabia have invested heavily in the sector, with USD 1.12 billion spent on establishing new farms to expand production.

- The increasing demand for poultry products, coupled with rising investments in the poultry sector, is expected to strengthen the growth of feed production. This growth is expected to drive the demand for feed additives in the global market during the forecast period. Overall, the poultry industry is poised for significant growth in the coming years, driven by the shift toward poultry products and increasing investments in the sector.

The growing demand for seafood consumption in Asia-Pacific and South America, and government initiatives is increasing the feed production for aquaculture species

- The demand for feed is rapidly increasing due to the expansion of aquaculture, which is driving the growth of compound feed production. In 2022, compound feed production increased by 13.1% from the previous year, and fish feed production increased by 46.3% between 2017 and 2022. The rising consumption of fish feed is driven by the need to maintain and improve the performance of aquatic animals and increase productivity to meet the growing demand for seafood.

- Fish feed accounted for 73.2% of the global market in 2022, as fish is highly consumed and produced in the Asia-Pacific region. Fish is followed by shrimp and other aquatic species in terms of share in the global market. Shrimp is highly imported by countries in Europe and the United States from other regions. To meet the growing demand for seafood, countries are focusing on the expansion of aquaculture production. India increased its budget allocation to the Department of Fisheries from USD 114.1 million in 2020 to USD 168.8 million in 2021 to increase production, which is expected to boost the demand for feed during the forecast period.

- South America is also experiencing an increase in feed production, which rose by 46.4% in 2022 from 2017 to reach 5.1 million metric ton due to the expansion of aquaculture farming. The region is one of the major seafood-consuming regions, and the increasing demand for seafood is driving the growth of aquaculture production.

- As aquaculture continues to expand to meet the growing demand, the development of the industry and a focus on its expansion are expected to fuel the growth of feed production. This increase in feed production for aquatic species is expected to aid in the growth of the aquatic segment during the forecast period.

Feed Yeast Industry Overview

The Feed Yeast Market is moderately consolidated, with the top five companies occupying 44.35%. The major players in this market are Archer Daniel Midland Co., Cargill Inc., DSM Nutritional Products AG, Lallemand Inc. and Phibro Animal Health Corporation (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Animal Headcount

- 4.1.1 Poultry

- 4.1.2 Ruminants

- 4.1.3 Swine

- 4.2 Feed Production

- 4.2.1 Aquaculture

- 4.2.2 Poultry

- 4.2.3 Ruminants

- 4.2.4 Swine

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 Brazil

- 4.3.3 Canada

- 4.3.4 China

- 4.3.5 France

- 4.3.6 Germany

- 4.3.7 India

- 4.3.8 Italy

- 4.3.9 Japan

- 4.3.10 Mexico

- 4.3.11 Netherlands

- 4.3.12 Philippines

- 4.3.13 Russia

- 4.3.14 South Africa

- 4.3.15 Spain

- 4.3.16 Thailand

- 4.3.17 Turkey

- 4.3.18 United Kingdom

- 4.3.19 United States

- 4.3.20 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Sub Additive

- 5.1.1 Live Yeast

- 5.1.2 Selenium Yeast

- 5.1.3 Spent Yeast

- 5.1.4 Torula Dried Yeast

- 5.1.5 Whey Yeast

- 5.1.6 Yeast Derivatives

- 5.2 Animal

- 5.2.1 Aquaculture

- 5.2.1.1 By Sub Animal

- 5.2.1.1.1 Fish

- 5.2.1.1.2 Shrimp

- 5.2.1.1.3 Other Aquaculture Species

- 5.2.2 Poultry

- 5.2.2.1 By Sub Animal

- 5.2.2.1.1 Broiler

- 5.2.2.1.2 Layer

- 5.2.2.1.3 Other Poultry Birds

- 5.2.3 Ruminants

- 5.2.3.1 By Sub Animal

- 5.2.3.1.1 Beef Cattle

- 5.2.3.1.2 Dairy Cattle

- 5.2.3.1.3 Other Ruminants

- 5.2.4 Swine

- 5.2.5 Other Animals

- 5.2.1 Aquaculture

- 5.3 Region

- 5.3.1 Africa

- 5.3.1.1 By Country

- 5.3.1.1.1 Egypt

- 5.3.1.1.2 Kenya

- 5.3.1.1.3 South Africa

- 5.3.1.1.4 Rest of Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 By Country

- 5.3.2.1.1 Australia

- 5.3.2.1.2 China

- 5.3.2.1.3 India

- 5.3.2.1.4 Indonesia

- 5.3.2.1.5 Japan

- 5.3.2.1.6 Philippines

- 5.3.2.1.7 South Korea

- 5.3.2.1.8 Thailand

- 5.3.2.1.9 Vietnam

- 5.3.2.1.10 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 By Country

- 5.3.3.1.1 France

- 5.3.3.1.2 Germany

- 5.3.3.1.3 Italy

- 5.3.3.1.4 Netherlands

- 5.3.3.1.5 Russia

- 5.3.3.1.6 Spain

- 5.3.3.1.7 Turkey

- 5.3.3.1.8 United Kingdom

- 5.3.3.1.9 Rest of Europe

- 5.3.4 Middle East

- 5.3.4.1 By Country

- 5.3.4.1.1 Iran

- 5.3.4.1.2 Saudi Arabia

- 5.3.4.1.3 Rest of Middle East

- 5.3.5 North America

- 5.3.5.1 By Country

- 5.3.5.1.1 Canada

- 5.3.5.1.2 Mexico

- 5.3.5.1.3 United States

- 5.3.5.1.4 Rest of North America

- 5.3.6 South America

- 5.3.6.1 By Country

- 5.3.6.1.1 Argentina

- 5.3.6.1.2 Brazil

- 5.3.6.1.3 Chile

- 5.3.6.1.4 Rest of South America

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Alltech, Inc.

- 6.4.2 Archer Daniel Midland Co.

- 6.4.3 Associated British Foods plc

- 6.4.4 Cargill Inc.

- 6.4.5 DSM Nutritional Products AG

- 6.4.6 Innov Ad NV/SA

- 6.4.7 Kemin Industries

- 6.4.8 Lallemand Inc.

- 6.4.9 Novus International, Inc.

- 6.4.10 Phibro Animal Health Corporation

7 KEY STRATEGIC QUESTIONS FOR FEED ADDITIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 386 Pages

- 納期

- 2~3営業日