ベトナムの殺虫剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Vietnam Insecticide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 165 Pages

- 納期

- 2~3営業日

- 商品コード

- 1684009

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

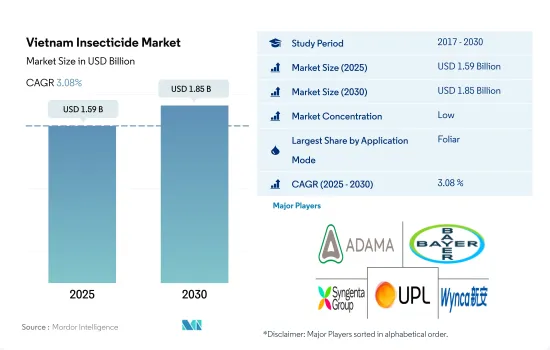

ベトナムの殺虫剤市場規模は2025年に15億9,000万米ドルと推定・予測され、2030年には18億5,000万米ドルに達し、予測期間(2025~2030年)のCAGRは3.08%で成長すると予測されます。

ステムボーラー、アーミーワーム、アブラムシによる作物の損失が頻発し、殺虫剤の使用量が増加

- ベトナムの農家は、主要作物に脅威を与える害虫と闘うために、主に殺虫剤に頼っています。特定の害虫や作物に応じて、農家は適切な散布方法を採用し、幅広い作物で害虫を効果的に駆除しています。このアプローチにより、害虫による被害を軽減し、農作物を保護することができます。

- 2022年の市場は、殺虫剤の葉面散布が57.7%と大きなシェアを占めていました。この優位性は、この方法に関連する数多くの利点に起因すると考えられます。殺虫剤を植物の葉に直接散布することで、狙った害虫に対して迅速かつ効率的に作用させることができます。さらに、イネやトウモロコシのようなこの国の主要作物は、イネ茎虫、アワノメイガ、アブラムシのような害虫に非常に弱いです。葉面殺虫剤の散布を利用することで、農家は害虫の個体数を効果的に駆除・管理することができます。この有利なアプローチが、国内での葉面散布の採用拡大に寄与しています。

- 2022年には、種子処理が殺虫剤散布のもう一つの重要な方法として浮上し、16.8%の市場シェアを占めました。この方法は種子を適切な殺虫剤で処理するもので、初期の段階で作物の成長に大きな影響を与える昆虫の幼虫や線虫を防除するのに有効です。この方法の採用が拡大しているのは、種子処理殺虫剤の最新の進歩により、地上と地下の両方で害虫を効果的に駆除できるようになったためです。

- 農家が使用するその他の散布方法には、化学灌漑、燻蒸、土壌処理などがあります。害虫蔓延の増加と生産性向上のニーズが、CAGR 3.3%で市場を牽引すると予想されます。

ベトナムの殺虫剤市場動向

害虫の発生増加、気象条件の変化、集約的農法の採用により殺虫剤の消費が増加する見込み

- ベトナムでは、気象条件の変化や従来の害虫駆除方法に耐性を持つ害虫の出現により害虫の発生が増加しているため、農作物用殺虫剤の消費量が増加すると予想されます。これら両方の要因が、増大する害虫問題に対処するための殺虫剤需要を押し上げています。

- 2019年のFAWの全国的な急速な広がりは農業セクターに大きな影響を与え、農作物にかなりの被害をもたらしました。この年、40県で35,000ヘクタール以上のトウモロコシがFAWの被害を受けました。その結果、農家が農作物を守るために殺虫剤の使用を増やしたため、この期間に除草剤の消費量が顕著に増加しました。

- 食料需要の高まりを受けて、農業活動は大幅に拡大しています。この拡大により、農作物を被害から守るための害虫駆除対策の強化が必要になる可能性があります。その結果、特に集約的な農法が採用されている地域では、殺虫剤の使用量が増加すると予想されます。

- ベトナムでも遺伝子組み換えトウモロコシの栽培が大幅に増加しています。2020年現在、耐虫性品種を含むGEトウモロコシの作付面積は約92,000ヘクタールで、全作付面積の約10%を占めています。ベトナムにおけるこのGEトウモロコシ栽培の増加は、殺虫剤の消費に影響を与えました。

- したがって、害虫の発生の増加、気象条件の変化、集約的農法の採用が、ベトナムの農作物に対する殺虫剤の使用量を増加させると予想される主な要因です。

ベトナムは殺虫剤のほとんどを中国、インド、米国から輸入しており、殺虫剤の世界第3位の輸入国です。

- ベトナムは殺虫剤の有効成分を輸入に依存しており、ベトナム国内で殺虫剤の有効成分を生産している企業は限られています。ベトナムはシペルメトリンとイミダクロプリドの大半を中国、ドイツ、インドから輸入しています。これらの有効成分の価格は、害虫の発生率、為替レート、輸入関税などさまざまな要因に左右されます。

- シペルメトリンは合成ピレスロイド系殺虫剤で、2022年にはトン当たり2万1,100米ドルと評価されました。シペルメトリンは、ベトナムの穀物や豆類に影響を与える鱗翅目、鞘翅目、双翅目、半翅目など幅広い害虫を駆除します。同様に、イミダクロプリドは浸透性殺虫剤であり、2022年にはトン当たり1万7,200米ドルと評価されました。イミダクロプリドは様々な作物の吸汁性・咀嚼性昆虫の防除に用いられます。

- マラチオンは有機リン系殺虫剤で、2022年にはトン当たり1万2,500米ドルの値がつきました。マラチオンは南ベトナムの主要害虫であるゾウムシやミバエの駆除に用いられます。これらの害虫は、グアバ、サポタ、サワーソップ、パパイヤ、ドラゴンフルーツなどの作物において、年間30.0%もの収量損失をもたらしています。

- ベトナムは殺虫剤のほとんどを中国、インド、米国から輸入しています。世界的に見て、ベトナムは第3位の殺虫剤輸入国です。2018年には国内で洪水が発生し、国内外を問わずサプライチェーンが寸断されました。その結果、輸送ルートが影響を受け、需要の増加と有効成分の限られた供給につながりました。そのため、2018年には有効成分の価格が上昇しました。

ベトナムの殺虫剤産業概要

ベトナムの殺虫剤市場は断片化されており、上位5社で12.07%を占めています。この市場の主要企業は以下の通りです。ADAMA Agricultural Solutions Ltd., Bayer AG, Syngenta Group, UPL Limited and Wynca Group(Wynca Chemicals)(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- ベトナム

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 使用方法

- 薬剤散布

- 葉面散布

- 燻蒸

- 種子処理

- 土壌処理

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- ADAMA Agricultural Solutions Ltd.

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- PI Industries

- Syngenta Group

- UPL Limited

- Wynca Group(Wynca Chemicals)

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50001711

The Vietnam Insecticide Market size is estimated at 1.59 billion USD in 2025, and is expected to reach 1.85 billion USD by 2030, growing at a CAGR of 3.08% during the forecast period (2025-2030).

Frequent crop losses due to stem borers, armyworms, and aphids increase the usage of insecticides

- Vietnamese farmers primarily rely on insecticides to combat insect pests that pose a threat to major crops. Depending on the specific pests and crops, farmers adopt suitable application methods to control the pests effectively across a wide range of crops. This approach allows them to mitigate the damage caused by pests and protect their agricultural produce.

- In 2022, the market was largely dominated by the foliar application of insecticides, which held a significant share of 57.7%. This dominance could be attributed to the numerous benefits associated with this method. Directly applying insecticides to the leaves of plants enables rapid and efficient action against targeted pests. Moreover, the country's prominent crops, such as rice and maize, are highly susceptible to insect pests like rice stem borers, armyworms, and aphids. Through the utilization of foliar insecticide applications, farmers can effectively control and manage pest populations. This advantageous approach has contributed to the growing adoption of foliar applications in the country.

- In 2022, seed treatment emerged as another significant mode of applying insecticides, representing a market share of 16.8%. This method involves treating seeds with suitable insecticides, which proves effective in controlling insect larvae and nematodes that significantly impact crop growth during the early stages. The growing adoption of this approach can be attributed to the latest advancements in seed treatment insecticides, enabling effective control of pests both above and below the ground.

- Other application modes used by the farmers include chemigation, fumigation, and soil treatment. Increasing pest infestations and the need for higher productivity are expected to drive the market at a CAGR of 3.3%.

Vietnam Insecticide Market Trends

The increasing occurrence of pests, changes in weather conditions, and the adoption of intensive farming practices are expected to increase the consumption of insecticides

- In Vietnam, the consumption of pesticides for crops is expected to increase due to the increasing prevalence of pests as a result of changing weather conditions and the emergence of pest populations that are resistant to conventional control methods. Both these factors have driven demand for insecticides to combat the growing pest issues.

- The rapid spread of FAW across the country in 2019 significantly impacted the agricultural sector, causing considerable damage to crops. Over 35,000 hectares of corn were affected by FAW in 40 provinces during that year. As a consequence, the consumption of herbicides witnessed a notable increase during this period as farmers increased their usage of insecticides to safeguard their crops.

- Agricultural activities have expanded significantly in response to the rising demand for food. This expansion may necessitate enhanced pest control measures to protect crops from damage. Consequently, the usage of insecticides is expected to increase, particularly in regions where intensive farming practices are employed.

- Vietnam has also witnessed a substantial rise in the cultivation of GE corn varieties. As of 2020, approximately 92,000 hectares of GE corn were planted, including insect-resistant varieties, which accounted for approximately 10% of the total crop area. This increase in GE corn cultivation in Vietnam impacted insecticide consumption.

- Therefore, the increasing occurrence of pests, changes in weather conditions, and the adoption of intensive farming practices are the primary factors that are expected to increase the utilization of insecticides for crops in Vietnam.

Vietnam imports most of its insecticides from China, India, and the United States and is the third-largest importer of insecticides in the world

- Vietnam is an import-dependent country in terms of active ingredients for insecticides; there are limited companies in Vietnam that produce active ingredients for pesticides. Vietnam imports the majority of Cypermethrin and Imidacloprid from China, Germany, and India. The prices of these active ingredients depend on various factors such as pest incidence, currency exchange rates, and import tariffs.

- Cypermethrin is a synthetic pyrethroid insecticide, which was valued at USD 21.1 thousand per metric ton in 2022. Cypermethrin controls a wide range of pests, including Lepidoptera, Coleoptera, Diptera, and Hemipteran, that affect cereals and pulses in Vietnam. Similarly, Imidacloprid is a systemic insecticide, which was valued at USD 17.2 thousand per metric ton in 2022. Imidacloprid is used to control sucking and chewing insects in various crops.

- Malathion is an organophosphate insecticide, which was valued at USD 12.5 thousand per metric ton. Malathion is used to control weevils and fruit flies, which are major pests in South Vietnam. These pests cause up to 30.0% annual yield losses in crops such as guava, sapota, soursop, papaya, and dragon fruit.

- Vietnam imports most of its insecticides from China, India, and the United States. Globally, Vietnam is the third-largest importer of insecticides. In 2018, there was a flood in the country that disrupted supply chains, both domestically and internationally. As a result, transportation routes were affected, leading to increased demand and a limited supply of active ingredients. Owing to that, the prices of active ingredients increased in 2018.

Vietnam Insecticide Industry Overview

The Vietnam Insecticide Market is fragmented, with the top five companies occupying 12.07%. The major players in this market are ADAMA Agricultural Solutions Ltd., Bayer AG, Syngenta Group, UPL Limited and Wynca Group (Wynca Chemicals) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd.

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 PI Industries

- 6.4.7 Syngenta Group

- 6.4.8 UPL Limited

- 6.4.9 Wynca Group (Wynca Chemicals)

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

ベトナムの殺虫剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 165 Pages

- 納期

- 2~3営業日