|

市場調査レポート

商品コード

1683980

アジア太平洋地域の殺虫剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Asia Pacific Insecticide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域の殺虫剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 224 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

アジア太平洋地域の殺虫剤市場規模は2025年に126億4,000万米ドルと推定され、2030年には151億3,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは3.66%で成長すると予測されます。

市場を牽引しているのは、病害虫の蔓延による収量減の増大です。

- この地域のほとんどの国で、農業は重要な役割を担っており、GDPに大きく貢献しています。それにもかかわらず、害虫の蔓延による農作物生産へのリスクは大きく、収量の減少、農家の経済的損失、食糧安全保障への懸念につながっています。アジア太平洋地域は気候や土壌が多様なため、さまざまな作物を栽培することができます。

- この地域では、虫害を管理するために様々な散布方法が採用されています。2022年には、葉面散布法が金額ベースで57.0%と最も高いシェアを占めました。この地域では、総合的害虫管理戦略の一環として、クロラントラニリプロール、エマメクチン安息香酸塩、スピネトラムによる葉面散布がかなり効果的であることが確認されています。

- 土壌治療法は2022年に金額ベースで9.9%と3番目に高いシェアを占めました。土壌への殺虫剤散布は、昆虫を防除する最も簡単で安全かつ効率的な方法であることが確認されています。農業害虫の場合、約95%が一生のうち何度かは土の中で過ごしているため、すでに述べたように、土の中に閉じ込めておくことが不可欠です。

- とはいえ、葉面散布農薬の使用には、消費者、労働者、環境の健康にとっていくつかの欠点があります。化学灌漑は、点滴灌漑システムを用いて土壌中の農薬を使用するもので、葉面散布殺虫剤に共通するいくつかの欠点を取り除くことができるかもしれないです。化学灌漑は2022年に金額ベースで7.4%のシェアを占めました。

- 最も安全で効果的な散布方法を生み出すことを目的とした研究と技術革新の増加により、市場は予測期間(2023~2029年)にCAGR 3.9%を記録すると予想されます。

気候の変化に伴う害虫の脅威の高まりが市場の成長に寄与している

- 2022年の殺虫剤世界市場シェアは、アジア太平洋地域が34.8%を占める。アジア太平洋地域地域は農業部門が大きく、害虫が多いことから、殺虫剤の重要な市場の一つとなっています。同地域では、殺虫剤は昆虫や害虫から作物を守り、より高い収量を確保するために広く使用されています。

- インド、中国、日本、オーストラリアなどの国々は、農作物を保護するために殺虫剤を広く採用していること、また、作物の収量や生産性に対する昆虫の影響についての認識が高まっていることから、市場で大きなシェアを占めています。

- 近代的な農業慣行の導入や耕作面積の増加など、農業活動の拡大が市場の成長に寄与しています。同地域の耕作面積は、2019年の6億2,450万ヘクタールから2022年には6億6,220万ヘクタールに増加します。農業の増加に伴い、作物を害虫から守るための効果的なソリューションが必要とされています。

- 気候の変化は、作物に被害を与える害虫の蔓延につながっています。このため、殺虫剤の需要は今後数年間で増加する可能性があります。

- 中国は、害虫の脅威の高まりと農作物の損失増加により、同国の農家が殺虫剤の使用量を増やすと予想されるため、予測期間(2023~2029年)のCAGRは5.7%で、同地域で最も急成長が見込まれています。

- アジア太平洋地域の殺虫剤市場は、農業セクターの拡大、作物を保護するニーズの高まり、気候の変化による殺虫剤需要の増加により、2023年から2029年にかけてCAGR 3.9%を記録すると予測されます。

アジア太平洋地域の殺虫剤市場動向

気温の上昇はカメムシのような様々な害虫の成長を促し、ヘクタール当たりの殺虫剤消費量を増加させる

- アジア太平洋地域では、日本の1ヘクタール当たりの殺虫剤消費量が高く、2017年から2022年にかけて約7%増加しました。この増加は、害虫の個体数の大幅な増加に起因すると考えられます。農林水産省の報告によると、農作物に重大な脅威をもたらすカメムシは近年ますます蔓延しています。専門家によると、カメムシをはじめとする害虫の増殖の主な要因は地球温暖化にあるといいます。カメムシやその他の害虫の蔓延を管理する主な方法は化学殺虫剤の使用であり、散布の頻度や量が増えていることが、ベトナムで1ヘクタール当たりの殺虫剤の消費量が増加している主な要因です。

- ヘクタール当たりの殺虫剤使用量では、ベトナムはこの地域で2番目の国です。ヘクタール当たりの殺虫剤使用量は、2017年の750gから2022年には1,200gへと大幅に増加しています。この増加は、生産性の向上と害虫駆除を目的とした集約的作物生産技術の採用に起因すると考えられます。高温、多湿、頻繁な降雨を特徴とするベトナムの熱帯気候は、農業に好条件を提供するが、同時に害虫の急速な増殖を促進します。その結果、同国では1ヘクタール当たりの殺虫剤消費量が増加しています。

- 全体として、アジア太平洋地域の他の国々でも、1ヘクタール当たりの殺虫剤消費量が前年比で増加しています。害虫の発生数の増加につながる気候変動が、この傾向の主な理由です。

サトウキビ、綿花、果物・野菜などの主要作物における殺虫剤需要の増加は、有効成分の価格上昇に有利です。

- 気候変動に加えて、害虫はこの地域の農業セクターに大きな脅威を与えており、平均で最大73%~100%の収量損失をもたらしています。こうした害虫と効果的に闘うため、農家は化学殺虫剤に大きく依存しています。

- この地域で最も広く使用されている殺虫剤はシペルメトリンで、鱗翅目、鞘翅目、双翅目、半翅目など様々な害虫を効果的に駆除する合成ピレスロイド系の特性で知られています。インド、中国、ベトナムなどの国々では、様々な作物の害虫駆除にシペルメトリンが主に使用されています。中国とベトナムはシペルメトリンの主要輸入国です。2022年現在、有効成分の価格は1トン当たり21,037.7米ドルに上昇し、2017年以降21.1%の大幅な上昇を反映しています。この顕著な価格上昇は主に、サトウキビ、綿花、果物・野菜などの作物におけるシペルメトリンの需要増に起因します。

- ネオニコチノイド系殺虫剤であるイミダクロプリドは、綿花、稲、油糧種子、果実、野菜、茶、コーヒー、カルダモンなどのプランテーション作物など、さまざまな作物の種子コーティング剤、土壌治療剤、葉面処理剤として使用されています。その主な目的は、吸汁性害虫の駆除です。中国はイミダクロプリドの主要輸出国であり、インドとベトナムはこの殺虫剤の主要輸入国です。有効成分の価格はトン当たり17,105.7米ドルで、2017年と比較して21.2%の大幅な上昇となりました。

- 需要の増加、輸入関税、為替レートの変動など様々な要因が有効成分の価格変動に寄与しています。

アジア太平洋地域殺虫剤産業の概要

アジア太平洋地域殺虫剤市場は細分化されており、上位5社で21.92%を占めています。この市場の主要企業は以下の通り。 ADAMA Agricultural Solutions Ltd, Corteva Agriscience, FMC Corporation, Syngenta Group and UPL Limited(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 使用方法

- 化学灌漑

- 葉面散布

- 燻蒸

- 種子処理

- 土壌処理

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

- 国

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- その他アジア太平洋地域地域

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- ADAMA Agricultural Solutions Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Jiangsu Yangnong Chemical Co. Ltd

- Nufarm Ltd

- Rainbow Agro

- Syngenta Group

- UPL Limited

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

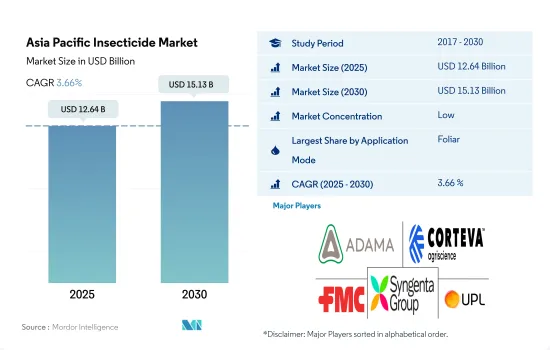

The Asia Pacific Insecticide Market size is estimated at 12.64 billion USD in 2025, and is expected to reach 15.13 billion USD by 2030, growing at a CAGR of 3.66% during the forecast period (2025-2030).

The market is being driven by growing yield losses due to increasing pest infestations

- In most of the countries in the region, agriculture has a key role to play and contributes substantially to GDP. Nevertheless, there is a significant risk to crop production due to the infestations of insects that result in reduced yields, financial losses for farmers, and concerns about food security. The diversity of climate and soil in Asia-Pacific allows for the cultivation of different crops.

- Various application methods are adopted in the region to manage insect infestation. The foliar application method occupied the highest share of 57.0% by value in 2022. It has been observed that the use of foliar spraying with chlorantraniliprole, emamectin benzoate, and spinetoram as part of an integrated pest management strategy has been quite effective in the region.

- The soil treatment method occupied the third highest share of 9.9% by value in 2022. It has been observed that insecticide application on soil appeared to be the easiest, safest, and most efficient way of controlling insects. In terms of agricultural pests, approximately 95% have passed some portion of their lives in the soil, and therefore, it is essential for them to be held underground, as already mentioned.

- Nevertheless, there are several drawbacks to the health of consumers, workers, and the environment from using foliar pesticides. Chemigation uses pesticides in soil with drip irrigation systems and may remove several drawbacks common to foliar insecticide applications. Chemigation occupied a share of 7.4% by value in 2022.

- Owing to the increase in research and innovation, which are aimed to bring out the safest and most effective method of application, the market is anticipated to register a CAGR of 3.9% during the forecast period (2023-2029).

The rising threat of pests with changing climate is contributing to the growth of the market

- Asia-Pacific accounted for 34.8% of the market share of the global insecticide market in 2022. Asia-Pacific is one of the important markets for insecticides due to its large agricultural sector and the prevalence of pests in the region. Insecticides are widely used in the region to protect crops from insects and pests, ensuring higher yields.

- Countries such as India, China, Japan, and Australia hold a substantial share of the market due to the wide adoption of insecticides to protect crops and the rise in awareness about the effects of insects on crop yield and productivity.

- The expansion of agriculture activities, such as adapting modern agriculture practices and increasing the area under agricultural cultivation, contributes to the market's growth. The region witnessed an increase in acreage under cultivation to 662.2 million hectares in 2022 from 624.5 million hectares in 2019. As agriculture increases, effective solutions are needed to protect crops from pests.

- The changing climate is leading to the spread of insect pests that can damage crops. Due to this, the demand for insecticides may increase in the coming years.

- China is expected to grow fastest in the region at a CAGR of 5.7% during the forecast period (2023-2029) because the farmers in the country are expected to increase the usage of insecticide owing to the rising threat of pests and increasing crop losses.

- The Asia-Pacific insecticide market is forecasted to record a CAGR of 3.9% during 2023-2029 due to the increasing demand for insecticides due to the expansion of the agriculture sector, the rising need to protect crops, and the changing climate.

Asia Pacific Insecticide Market Trends

The rise in climate temperatures favors various insect pests like stink bugs to grow, increasing insecticide consumption per hectare

- In Asia-Pacific, Japan exhibits higher per-hectare consumption of insecticide, which witnessed approximately a 7% increase from 2017 to 2022. This rise may be attributed to the substantial growth in the population of insect pests. The Ministry of Agriculture, Forestry, and Fisheries reports that stink bugs, which pose significant threats to agricultural crops, have been increasingly prevalent in recent years. According to experts, the primary factor driving the proliferation of stink bugs and other pests is attributed to global warming. The principal approach to managing infestations of stink bugs and other pests involves the use of chemical insecticides, with the intensified frequency and dosages of the application being the primary factors contributing to the augmented consumption of insecticides per hectare in the country.

- Vietnam is the second country in the region in terms of insecticide usage per hectare. The amount of insecticide used per hectare significantly increased from 750 g in 2017 to 1,200 g in 2022. This rise may be attributed to the adoption of intensive crop production techniques aimed at improving productivity and pest control. Vietnam's tropical climate, characterized by high temperatures, humidity, and frequent rainfall, provides favorable conditions for agriculture but also promotes the rapid proliferation of insect pests. As a result, insecticide consumption per hectare has increased in the country.

- In overall, other countries in Asia-Pacific are also experiencing a YoY increase in insecticide consumption per hectare. Climate changes leading to an increase in the population of insect pests' infestations are primary reasons for this trend.

Increased demand for insecticides in major crops like sugarcane, cotton, and fruits and vegetables favors the active ingredient price growth

- In addition to climate changes, insect pests present a significant threat to the agriculture sector in the region, causing average yield losses of up to 73% to 100%. To combat these insect pests effectively, farmers are heavily relying on chemical insecticides.

- Cypermethrin holds a dominant position as the most widely used insecticide in the region, known for its synthetic pyrethroid properties that effectively control various insect pests, including Lepidoptera, Coleoptera, Diptera, and Hemiptera. Countries like India, China, and Vietnam predominantly rely on cypermethrin for pest control across various crops. China and Vietnam are the primary importers of cypermethrin. As of 2022, the price of the active ingredient increased to USD 21,037.7 per metric ton, reflecting a significant rise of 21.1% since 2017. This notable price increase was primarily attributed to the escalating demand for cypermethrin in crops such as sugarcane, cotton, and fruits and vegetables.

- Imidacloprid, a neonicotinoid insecticide, finds application as a seed dressing, soil treatment, and foliar treatment in various crops, including cotton, rice, oilseeds, fruits, and vegetables, and plantation crops like tea, coffee, and cardamom. Its primary purpose is to control sucking insect pests. China serves as the major exporter of Imidacloprid, while India and Vietnam are the main importing countries for this insecticide. The price of the active ingredient stood at USD 17,105.7 per metric ton, representing a significant increase of 21.2% compared to 2017.

- Various factors, such as rising demand, import tariffs, and fluctuations in exchange rates, contribute to the fluctuation in the price of the active ingredients.

Asia Pacific Insecticide Industry Overview

The Asia Pacific Insecticide Market is fragmented, with the top five companies occupying 21.92%. The major players in this market are ADAMA Agricultural Solutions Ltd, Corteva Agriscience, FMC Corporation, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 India

- 4.3.4 Indonesia

- 4.3.5 Japan

- 4.3.6 Myanmar

- 4.3.7 Pakistan

- 4.3.8 Philippines

- 4.3.9 Thailand

- 4.3.10 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Myanmar

- 5.3.7 Pakistan

- 5.3.8 Philippines

- 5.3.9 Thailand

- 5.3.10 Vietnam

- 5.3.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Jiangsu Yangnong Chemical Co. Ltd

- 6.4.7 Nufarm Ltd

- 6.4.8 Rainbow Agro

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms