|

市場調査レポート

商品コード

1683997

北米の殺虫剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)North America Insecticide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の殺虫剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

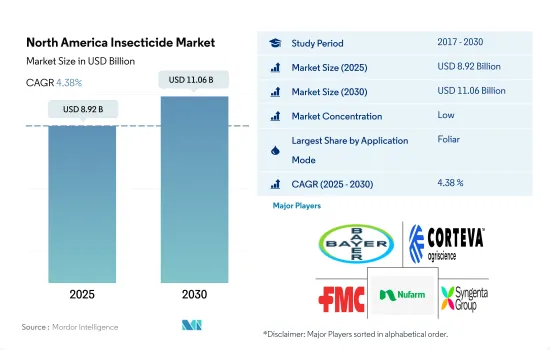

北米の殺虫剤市場規模は2025年に89億2,000万米ドルと推定・予測され、2030年には110億6,000万米ドルに達し、予測期間(2025~2030年)のCAGRは4.38%で成長すると予測されます。

害虫問題の高まりが市場成長を促進する見込み

- 北米の殺虫剤市場は、2022年の世界の殺虫剤市場の市場価値の25.2%を占める。北米の殺虫剤市場は、すべてのセグメントで成長が見込まれています。作物保護に対する需要の高まりと農業生産性の向上により、2023~2029年のCAGRは4.8%を記録すると予測されます。

- 北米の殺虫剤市場では、害虫駆除効果の高さから葉面散布剤が大きなシェアを占め、2022年には41.2%を占めました。

- 化学灌漑分野は、2022年に北米の殺虫剤市場の14.4%を占めました。ケミゲーション分野の殺虫剤市場は、殺虫剤の正確で均一な散布、人件費の削減、害虫駆除効果の向上など、その潜在的なメリットによって牽引されています。

- 種子処理法はこの地域で人気を集めており、予測期間(2023~2029年)の殺虫剤市場のCAGRは4.8%で、最も急成長しているセグメントの1つになると予想されます。種子処理は、植え付け前に種子を殺虫剤でコーティングすることで、初期の害虫の圧力や病気から新興の苗を保護します。害虫管理に的を絞った効率的なアプローチであるため、農家にとって魅力的な選択肢となっています。

- 土壌処理分野の殺虫剤市場は、2023~2029年にCAGR 4.8%を記録すると予測されています。土壌処理の成長は、特定の害虫から長期間保護し、ライフサイクルのさまざまな段階にある害虫を対象とすることで、より優れた害虫管理を促進するなどの利点があるためと考えられます。

害虫圧力の増加、栽培の拡大、高品質の農産物への需要の高まりが市場の成長を促進しています。

- 北米は、2022年の殺虫剤世界市場の24.0%のシェアを占めました。同地域は、作物保護ソリューションの需要増加により著しい成長を遂げています。人口の増加、食糧需要の増加、農業活動の拡大、害虫から作物を保護するニーズの高まりなどの要因が市場を牽引しています。

- 米国は北米殺虫剤市場の支配的プレイヤーです。同国は世界最大かつ最も技術的に進んだ農業セクターのひとつであり、さまざまな作物や商品を生産しています。その結果、有害な害虫や害獣から作物を守るための殺虫剤に対する米国の需要は大きいです。

- メキシコは予測期間中(2023~2029年)にCAGR 6.2%を記録する見込みで、北米の殺虫剤市場で最も急成長している国です。農業活動の拡大、多様な作物、気候条件の変化が、作物を保護し最適な収量を確保するためにメキシコでの殺虫剤の使用を促進しています。

- カナダは予測期間中(2023~2029年)にCAGR 3.0%を記録すると予測されています。大規模栽培作物における害虫圧力の上昇と、害虫から作物を保護する必要性の高まりが、カナダの殺虫剤市場の成長を促進すると予測されます。

- その他北米地域の殺虫剤市場は、2022年に6,550万米ドルと評価されました。果物・野菜作物分野が市場を独占し、同年の市場シェアは4.3%でした。この地域セグメントの市場は、作物を害虫から守ることによる経済的利益に対する意識の高まりによって牽引されています。その結果、北米以外の地域の殺虫剤市場は、予測期間中(2023~2029年)にCAGR 4.7%を記録すると予測されます。

北米の殺虫剤市場動向

害虫から作物を守ることで収穫量を向上させるニーズが殺虫剤需要を押し上げると予測

- 北米諸国の中では米国が1ヘクタール当たりの殺虫剤消費量が最も多く、2022年には791.7 gとなりました。これは、作物の栽培面積が広く、地球温暖化などの要因によって気候条件が絶えず変化するため、害虫の侵入にさらされる機会が増えていることに起因しています。気温の上昇により、冬季の害虫の生存率が高まっており、これは主に米国におけるトウモロコシの穂いもちや綿ボルワームの事例で観察されています。

- この現象は作物の収量に顕著なリスクをもたらし、特に米国で基本的に栽培されている食用作物であるトウモロコシ栽培において、これらの害虫を管理する上で重要な課題となっています。このような状況により、農地1ヘクタールあたりの殺虫剤消費量が増加しています。

- メキシコは北米で2番目に殺虫剤を消費する国で、2022年には1ヘクタール当たり606gの殺虫剤を消費しました。同国における殺虫剤使用量の増加は、害虫の侵入増加による収穫作物収量の減少に起因すると考えられます。FAO統計局が提供したデータによると、メキシコで最も多く栽培されている作物のひとつであるナスの収量は、2019年の1ヘクタールあたり793.0kgから2021年には785.0kgに減少し、殺虫剤の消費量の減少につながりました。農作物の収穫量を増やすことが、同国における殺虫剤使用の大きな原動力となっています。

- 米国とカナダで生産されたトウモロコシ全体の収量ロスの87.6%は無脊椎動物害虫の侵入によるものだと報告されています。これらの要因が北米における殺虫剤の使用を促進すると予想されます。

殺虫剤の価格は原料価格の変動によって影響を受ける可能性があります。

- 2022年、シペルメトリンは1トン当たり2万1,100米ドルと評価されました。シペルメトリンが農業で広く利用されているのは、アブラムシ、カイガラムシ、斑点玉虫、ピンク玉虫、早期斑点螟虫、毛虫など、多様な昆虫を管理する能力が高いためです。その効果は実証済みで、農作物を害虫から守り、実りある収量を確保しようとする農家の間で人気が高まっています。

- イミダクロプリドは強力なネオニコチノイド系殺虫剤であり、効果的な浸透性と持続性を持っています。アブラムシ、サシガメ、アザミウマ、カメムシ、イナゴ、その他作物に害を与える害虫の一群など、幅広い昆虫を駆除する能力を誇る。また種子処理剤としても使用され、特に発芽・生育中の植物を脅かす地中性害虫に対して、幼苗を害から守る。イミダクロプリド製品は濃縮液や固形など、さまざまな形態で入手できます。植物との相溶性がよく、散布の必要性が少ないことから、農家の間で人気を博しています。この活性化合物の価格は2022年にはトン当たり1万7,200米ドルと記録されています。

- マラチオンは有機リン系殺虫剤で、アブラムシ、ノミ、オオヨコバイ、コナカイガラムシ、その他多くの作物の害虫駆除に使用されます。米国で広く栽培され、マラチオンを頻繁に使用する作物は、ミニトマト、ブロッコリー、クワ、クランベリー、イチジクの5種類です。2022年の価格は1トン当たり1万2,600米ドルと評価されています。

北米の殺虫剤産業概要

北米殺虫剤市場は細分化されており、上位5社で39.62%を占めています。この市場の主要企業は以下の通りです。 Bayer AG, Corteva Agriscience, FMC Corporation, Nufarm Ltd and Syngenta Group(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- カナダ

- メキシコ

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 使用方法

- 化学灌漑

- 葉面散布

- 燻蒸

- 種子処理

- 土壌処理

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

- 生産国

- カナダ

- メキシコ

- 米国

- その他北米地域

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- ADAMA Agricultural Solutions Ltd.

- American Vanguard Corporation

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Nufarm Ltd

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50001699

The North America Insecticide Market size is estimated at 8.92 billion USD in 2025, and is expected to reach 11.06 billion USD by 2030, growing at a CAGR of 4.38% during the forecast period (2025-2030).

The rising pest challenges are expected to propel the growth of the market

- The North American insecticide market accounted for 25.2% of the market value of the global insecticide market in 2022. The North American insecticide market is expected to witness growth in all segments. It is anticipated to register a CAGR of 4.8% during 2023-2029 due to the rising demand for crop protection and improved agriculture productivity.

- Foliar applications held a significant value share in the insecticide market of North America, accounting for 41.2% in 2022 due to their effectiveness in controlling insect pests.

- The chemigation segment accounted for 14.4% of North America's insecticide market value in 2022. The insecticide market in the chemigation segment is driven by its potential benefits, including the precise and uniform application of insecticides, reduced labor costs, and enhanced pest control efficacy.

- The seed treatment method has been gaining popularity in the region, and it is expected to be one of the fastest-growing segments at a CAGR of 4.8% in the insecticide market during the forecast period (2023-2029). Seed treatment involves coating seeds with insecticides before planting, which provides protection to emerging seedlings from early pest pressures and diseases. It has become an attractive option for farmers due to its targeted and efficient approach to pest management.

- The insecticide market in the soil treatment segment is anticipated to register a CAGR of 4.8% during 2023-2029. The growth in soil treatment can be attributed to its advantages, such as providing long-lasting protection against certain pests and promoting better pest management by targeting insects at different stages of their life cycles.

Increasing pest pressure, expansion of cultivation, and rising demand for quality produce are driving the growth of the market

- North America accounted for a 24.0% share in 2022 of the global insecticide market. The region is witnessing significant growth due to the increasing demand for crop protection solutions. Factors such as growing population, rising food demand, expanding agricultural activities, and the increasing need to protect crops from insect pests are driving the market.

- The United States is a dominant player in the North American insecticide market. It has one of the largest and most technologically advanced agricultural sectors in the world, producing a wide range of crops and commodities. As a result, the US demand for insecticides to protect crops from damaging pests and insects has been substantial.

- Mexico is expected to register a CAGR of 6.2% during the forecast period (2023-2029), making it the fastest-growing country in the North American insecticide market. The growing agricultural activities, a diverse range of crops, and changing climatic conditions are driving the use of insecticides in Mexico to protect crops and ensure optimal yields.

- Canada is anticipated to register a CAGR of 3.0% during the forecast period (2023-2029). The rising pest pressure in significantly cultivated crops and the growing need to protect crops from insect pests are anticipated to fuel the growth of the Canadian insecticide market.

- The insecticide market in the Rest of North America was valued at USD 65.5 million in 2022. The fruit and vegetable crops segment dominated the market, with a 4.3% market share in the same year. The market in this regional segment is being driven by the growing awareness of the economic benefits of protecting crops from insect pests. As a result, the Rest of North America insecticide market is expected to register a CAGR of 4.7% during the forecast period (2023-2029).

North America Insecticide Market Trends

The need for improved yield by protecting the crops from pests is anticipated to boost the demand for insecticides

- Among the North American countries, the United States witnessed the largest consumption of insecticides per hectare, with 791.7 g in 2022, attributed to the large area under the cultivation of crops and increased exposure to insect pest infestations due to constantly changing climatic conditions due to factors like global warming. Rising temperatures have caused the increased survival of insect pests during the winter seasons, which is mainly observed in cases of corn earworm and cotton bollworm in the United States.

- This phenomenon has posed a notable risk to crop yields and presented a significant challenge in managing these pests, particularly in corn cultivation, which is a fundamentally grown food crop in the United States. These kinds of circumstances have increased the need for heavy insecticide consumption per hectare of cropland.

- Mexico is the second-largest consumer of insecticides in North America, and in 2022, the country consumed 606 g of insecticides per hectare. The increased usage of insecticides in the country may be attributed to the reduction in the harvested crop yield due to increased infestation of insect pests. According to the data provided by the FAO Statistics, the yield of eggplant, which is one of the most largely grown crops in Mexico, decreased from 793.0 kg per hectare in 2019 to 785.0 kg per hectare in 2021, leading to reduced insecticide consumption. The aim to increase the yield of the crops is majorly driving the usage of insecticides in the country.

- It was reported that 87.6% of the yield loss from the total corn produced in the United States and Canada was due to invertebrate pest infestation. These factors are anticipated to drive the usage of insecticides in North America.

The prices of insecticides may be impacted by the fluctuation of raw material prices

- In 2022, cypermethrin was valued at USD 21.1 thousand per metric ton. Its widespread utilization in agriculture owes to its proficiency in managing diverse insect varieties, such as aphids, beetles, spotted ball worms, pink ball worms, early spot borers, and hairy caterpillars. Its proven efficacy has elevated its popularity among farmers aiming to protect their crops from pests and secure a fruitful yield.

- Imidacloprid stands as a potent neonicotinoid insecticide, displaying effective systemic and enduring characteristics. It boasts the ability to manage a broad spectrum of insects, such as aphids, cane beetles, thrips, stink bugs, locusts, and an array of other crop-damaging pests. It is also used as a seed treatment that shields young plants from harm, especially against subterranean pests that can threaten germinating and growing plants. Imidacloprid products are available in various forms, such as liquid concentrates and solids. Owing to its compatibility with plants and minimal application needs, it has gained popularity among farmers. The pricing of this active compound was recorded at USD 17.2 thousand per metric ton in 2022.

- Malathion is an organophosphate insecticide that is used to control a wide variety of food and feed crops to control many types of insects such as aphids, fleas, leafhoppers, Japanese beetles, and other insect pests on a number of crops. Five crops that are extensively grown in the United States that use malathion frequently are cherry tomato, broccoli, mulberry, cranberry, and fig. It is valued at a price of USD 12.6 thousand per metric ton in 2022.

North America Insecticide Industry Overview

The North America Insecticide Market is fragmented, with the top five companies occupying 39.62%. The major players in this market are Bayer AG, Corteva Agriscience, FMC Corporation, Nufarm Ltd and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Canada

- 4.3.2 Mexico

- 4.3.3 United States

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd.

- 6.4.2 American Vanguard Corporation

- 6.4.3 BASF SE

- 6.4.4 Bayer AG

- 6.4.5 Corteva Agriscience

- 6.4.6 FMC Corporation

- 6.4.7 Nufarm Ltd

- 6.4.8 Sumitomo Chemical Co. Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms