|

市場調査レポート

商品コード

1683890

電気バス用バッテリーパック:市場シェア分析、産業動向・統計、成長予測(2025年~2029年)Electric Bus Battery Pack - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 電気バス用バッテリーパック:市場シェア分析、産業動向・統計、成長予測(2025年~2029年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 356 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

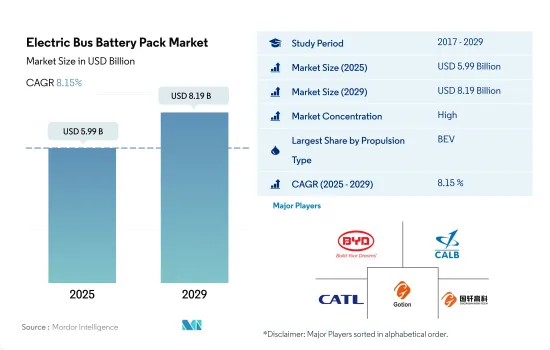

電気バス用バッテリーパックの市場規模は2025年に59億9,000万米ドルと推定され、2029年には81億9,000万米ドルに達すると予測され、予測期間(2025-2029年)のCAGRは8.15%で成長する見込みです。

環境問題への関心の高まりと政府の取り組みが世界の電気バス市場の成長を牽引、バッテリー製造の拡大が後押し

- バスは依然として世界的に人気のある交通手段ですが、環境に対する懸念の高まりや、ディーゼルバスやガソリンバスのような従来型車両を段階的に廃止する政府の動きが、電気バスの需要に拍車をかけています。しかし、COVID-19の大流行などの要因により、2020年のEバス需要は落ち込みました。EV市場が回復すると、2021年にはEバスの販売台数が32%急増し、同年にはバッテリーパックの販売台数が30.9%増加しました。

- 公共輸送サービスの拡大による電気バスの需要増は、バッテリー電気バスとプラグインハイブリッドバスの両方で多様なタイプのバッテリーの必要性に拍車をかけています。特に米国では、2022年の輸送用電気バスの販売台数が前年比66%増と顕著に急増しました。カリフォルニア州のような州は、野心的なゼロ・エミッション目標を設定し、2030年までにゼロ・エミッション・バスのみを販売することを目指しています。これらの開発により、2022年のバス用バッテリーの世界需要は2021年比で15%増加しました。

- 2023年4月、カナダの電池会社ライオン・エレクトリックは、バスを含む中型・大型車用電池に特化した新しい製造施設を落成させました。同社は2023年末までに1.7GWhの生産能力を目指していました。カナダだけでなく世界的に見られるこのような取り組みは、今後数年間、電気バス用バッテリーの需要を強化する構えです。

中国が牽引するアジア太平洋が著しい成長で世界の電気バス用バッテリーパック市場を独占

- 世界の電気バスバッテリーパック市場は、歴史的期間(2017-2021年)に大きな成長が見られましたが、これは世界のいくつかの国で電気バスの採用が増加していることが要因です。電気バスの採用は、大気汚染や温室効果ガス排出に対抗するため、クリーンでグリーンな公共交通機関へのニーズの高まりが原動力となっています。また、大手電池メーカーによる継続的な研究開発活動により、高エネルギー密度で長寿命の先進的な電気バス用電池パックが開発され、従来の化石燃料を使用するバスの理想的な代替品となっています。

- 2022年から2023年を基準年として、世界の電気バス用バッテリーパック市場は、環境に優しい公共交通機関へのニーズの高まり、電気自動車への需要の高まり、クリーンエネルギーの導入を促進する政府の取り組みなど、いくつかの要因によって、着実な成長が見込まれています。さらに、再生可能エネルギーと持続可能なインフラへの注目の高まりは、世界中の様々な地域で電気バスの需要を押し上げると予想されています。

- 世界の電気バス用バッテリーパック市場は、予測期間中(2023-2029年)、電気バスの採用増加、クリーンでグリーンな公共交通機関へのニーズの高まり、電気自動車市場の拡大により、大きな成長が見込まれています。さらに、大手OEMやバッテリーメーカーは、より優れた性能と効率を提供する新しく高度な技術を生み出すために研究開発に多額の投資を行っており、これが市場の成長をさらに押し上げると予想されます。

電気バス用バッテリーパック市場の動向

BYDとテスラがEV市場をリードし、未来を形作る

- 2022年、BYDは電気自動車販売で市場をリードし、13.3%のシェアを占めました。BYDの主導的地位にはいくつかの要因があります。BYDは、電気自動車と関連技術の生産に重点を置き、EV業界で早くから有力なプレーヤーとして活躍してきました。BYDは早くから市場に参入していたため、確固たる基盤を築き、消費者の間で認知されるようになりました。BYDはまた、積極的に世界に事業を拡大し、パートナーシップを結び、研究開発に投資しており、これらすべてが主導的地位に貢献しています。

- テスラは電気自動車の技術革新の最前線に立ち、EVの世界の普及に重要な役割を果たしてきました。テスラは2022年のEV業界において、12.2%の市場シェアを持つ重要なプレーヤーでした。テスラの強力なブランドイメージ、最先端技術、広範なスーパーチャージャー・ネットワークがその成功に寄与しています。

- EV市場のその他の主要企業の中にも、大きな市場シェアを持つ企業がいくつかあります。BMWは、サブブランド「BMW i」による電動モビリティへのコミットメントと相まって、自動車業界における定評を確立しており、市場での存在感を高めています。同様に、2022年に3.9%の市場シェアを占めたフォルクスワーゲンは、「フォルクスワーゲン・グループ」傘下で電動モビリティに積極的に投資しています。これらの企業は、メルセデス・ベンツ、起亜自動車、現代自動車といった他の企業とともに、既存のブランド認知度を活用し、魅力的な電気自動車モデルを投入し、電気自動車の航続距離と性能を向上させる技術に投資することで、EV業界を再植民地化しています。

テスラとBYDが2022年のベストセラーEVモデルを独占

- 2022年に最も売れたEVモデルは、2つの主要OEMが独占した:テスラとBYDです。テスラはModel YとModel 3の2モデルでそれぞれ1位と3位を獲得し、市場で確固たる地位を築いた。テスラのモデルYは最も人気のあるプラグイン電気自動車で、2022年の世界販売台数は約77万1,300台でした。同年、テスラのモデル3とモデルYの販売台数は120万台を突破し、テスラのベストセラーモデルは前年比36.77%増となりました。プラグイン電気自動車(PEV)のベストセラー5モデルのうち2モデルはテスラブランドだったが、バッテリー電気自動車メーカーは2022年にアジアブランドとの競争に直面しました。中国を拠点とするBYDは、プラグイン・ハイブリッド電気自動車モデルの豊富なラインアップを武器に、2022年にテスラを抜いてPEVのベストセラー・ブランドとなりました。テスラ・モデルYに僅差で続いたのは、BYDソング・プラス(BEV+PHEV)で、販売台数は47万7,090台に達し、2位の座を確保しました。BYDは中国市場で確固たる地位を確立しており、信頼性が高く技術的に先進的な電気自動車を生産しているという評判が、Song Plusモデルの好調な販売実績に貢献したと思われます。

- フォルクスワーゲンID.4は、欧州のPEV(プラグイン電気自動車)の中で唯一トップ10に入り、ベストセラーEVモデルの中で際立っていました。2022年の販売台数は17万4,090台で、ID.4はフォルクスワーゲンの電動モビリティに対するコミットメントと、EV市場におけるプレゼンスの高まりを実証しました。

- 全体として、TeslaとBYDのこれらのトップクラスのEVモデル、およびWuling Hong Guang MINI EVやVolkswagen ID.4などの他の注目すべき競合モデルは、電気自動車に対する消費者の需要が高まっていることを示しています。

電気バス用バッテリーパック業界の概要

電気バス用バッテリーパック市場はかなり統合されており、上位5社で88.11%を占めています。この市場の主要企業は以下の通りです。BYD Company Ltd., China Aviation Battery(CALB), Contemporary Amperex Technology(CATL), Gotion High-Tech and Guoxuan High-tech(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 電気バス販売台数

- OEM別電気バス販売台数

- 売れ筋EVモデル

- 選好されるバッテリーケミストリーのOEM

- バッテリーパック価格

- 電池材料コスト

- 異なるバッテリーケミストリーの価格表

- 誰が誰に供給するか

- EVバッテリーの容量と効率

- EVの発売モデル数

- 規制の枠組み

- ベルギー

- ブラジル

- カナダ

- 中国

- コロンビア

- フランス

- ドイツ

- ハンガリー

- インド

- インドネシア

- 日本

- メキシコ

- ポーランド

- タイ

- 英国

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 推進タイプ

- BEV

- PHEV

- バッテリーケミストリー

- LFP

- NCA

- NCM

- NMC

- その他

- 容量

- 15 kWh~40 kWh

- 40 kWh~80 kWh

- 80kWh以上

- 15kWh未満

- バッテリー形状

- 円筒形

- パウチ

- 角型

- 方式

- レーザー

- ワイヤー

- コンポーネント

- アノード

- カソード

- 電解液

- セパレーター

- 材料タイプ

- コバルト

- リチウム

- マンガン

- 天然黒鉛

- ニッケル

- その他の材料

- 地域

- アジア太平洋

- 国別

- 中国

- インド

- 日本

- 韓国

- タイ

- その他アジア太平洋地域

- 欧州

- 国別

- フランス

- ドイツ

- ハンガリー

- イタリア

- ポーランド

- スウェーデン

- 英国

- その他欧州

- 中東&アフリカ

- 北米

- 国別

- カナダ

- 米国

- 南米

- アジア太平洋

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- BMZ Batterien-Montage-Zentrum GmbH

- BYD Company Ltd.

- China Aviation Battery Co. Ltd.(CALB)

- Contemporary Amperex Technology Co. Ltd.(CATL)

- Farasis Energy(Ganzhou)Co. Ltd.

- Gotion High-Tech Co. Ltd.

- Guoxuan High-tech Co. Ltd.

- Leclanche SA

- LG Energy Solution Ltd.

- NFI Group Inc.

- Panasonic Holdings Corporation

- Proterra Operating Company Inc.

- Samsung SDI Co. Ltd.

- Sunwoda Electric Vehicle Battery Co. Ltd.(Sunwoda)

- Tata Autocomp Systems Ltd.

- TOSHIBA Corp.

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Electric Bus Battery Pack Market size is estimated at 5.99 billion USD in 2025, and is expected to reach 8.19 billion USD by 2029, growing at a CAGR of 8.15% during the forecast period (2025-2029).

Rising environmental concerns and governmental initiatives are driving the growth of the global electric bus market, supported by expansions in battery manufacturing

- Buses remain a popular mode of transportation globally, but rising environmental concerns and governmental moves to phase out conventional vehicles, like diesel and petrol buses, are fueling the demand for e-buses. However, factors like the COVID-19 pandemic led to a dip in e-bus demand in 2020. As the EV market rebounded, e-bus sales surged by 32% in 2021, propelling battery pack sales up by 30.9% in the same year.

- The growing demand for electric buses, driven by expanding public transportation services, is spurring the need for diverse battery types in both battery electric and plug-in hybrid buses. Notably, the US witnessed a remarkable 66% surge in transit electric bus sales in 2022 compared to the previous year. States like California are setting ambitious zero-emission targets, aiming to sell only zero-emission buses by 2030. These developments collectively pushed the global demand for bus batteries up by 15% in 2022 over 2021.

- In April 2023, Lion Electric, a Canada-based battery company, inaugurated a new manufacturing facility dedicated to batteries for medium- and heavy-duty vehicles, including buses. The company was eyeing a production capacity of 1.7 GWh by the close of 2023. Such initiatives, seen not only in Canada but globally, are poised to bolster the demand for electric bus batteries in the coming years.

Asia-Pacific, led by China, dominates the global EV battery pack market with remarkable growth

- The global electric bus battery pack market witnessed significant growth during the historical period (2017-2021), driven by the increasing adoption of electric buses in several countries worldwide. The adoption of electric buses is driven by the growing need for clean and green public transportation to combat air pollution and greenhouse gas emissions. Additionally, the continuous research and development activities undertaken by leading battery manufacturers have resulted in the development of advanced electric bus battery packs with high energy density and longer lifespan, which are an ideal replacement for traditional fossil fuel-based buses.

- In the base year of 2022-2023, the global electric bus battery pack market is expected to witness steady growth, driven by several factors such as the increasing need for eco-friendly public transportation, the rising demand for electric vehicles, and the government initiatives to promote the adoption of clean energy. Furthermore, the growing focus on renewable energy and sustainable infrastructure is expected to boost the demand for electric buses in various regions across the world.

- The global electric bus battery pack market is expected to witness significant growth, driven by the increasing adoption of electric buses, the rising need for clean and green public transportation, and the expanding electric vehicle market during the forecast (2023-2029). Furthermore, leading OEMs and battery manufacturers are investing heavily in research and development to create new and advanced technologies that offer better performance and efficiency, which is expected to further boost the growth of the market.

Electric Bus Battery Pack Market Trends

BYD AND TESLA ARE LEADING THE CHARGE IN THE EV MARKET AND SHAPING THE FUTURE

- In 2022, BYD was the market leader in electric vehicle sales and held a share of 13.3%. BYD's leading position can be attributed to several factors. It has been an early and prominent player in the EV industry, with a strong focus on producing electric vehicles and related technologies. The company's early entry into the market allowed it to establish a solid foundation and gain recognition among consumers. BYD has also been actively expanding its operations globally, forging partnerships, and investing in research and development, all of which contribute to its leading position.

- Tesla has been at the forefront of electric vehicle innovation and has played a crucial role in popularizing EVs worldwide. Tesla was a significant player in the EV industry in 2022, with a market share of 12.2%. Tesla's strong brand image, cutting-edge technology, and extensive Supercharger network have contributed to its success.

- Among the other players in the EV market, there are several notable companies that hold significant market shares. BMW's established reputation in the automotive industry, coupled with its commitment to electric mobility through its "BMW i" sub-brand, has contributed to its market presence. Similarly, Volkswagen, which held a market share of 3.9% in 2022, has been actively investing in electric mobility under its "Volkswagen Group" umbrella. These companies, along with others like Mercedes-Benz, Kia, and Hyundai, are recolonizing the EV industry by leveraging their existing brand recognition, introducing compelling electric vehicle models, and investing in technology to enhance the range and performance of their electric offerings.

TESLA AND BYD DOMINATED THE BEST-SELLING EV MODELS OF 2022

- The best-selling EV models in 2022 were dominated by two key OEMs: Tesla and BYD. Tesla held a strong market position with two of its models, the Model Y and Model 3, capturing the first and third spots, respectively. The Tesla Model Y was the most popular plug-in electric vehicle, with global unit sales of roughly 771,300 in 2022. That year, deliveries of Tesla's Model 3 and Model Y surpassed 1.2 million, a Y-o-Y increase of 36.77% for Tesla's best-selling models. While two of the five best-selling plug-in electric vehicle (PEV) models were Tesla-branded, the battery electric vehicle manufacturer faced competition from Asian brands in 2022. China-based BYD overtook Tesla as the best-selling PEV brand in 2022, relying on a large offering of plug-in hybrid electric models. Following closely behind the Tesla Model Y, the BYD Song Plus (BEV + PHEV) secured the second spot, with sales reaching 477,090 units. BYD's established presence in the Chinese market, along with its reputation for producing reliable and technologically advanced electric vehicles, likely contributed to the strong sales performance of the Song Plus models.

- The Volkswagen ID.4 stood out among the best-selling EV models as the only European PEV (Plug-in Electric Vehicle) in the top ten. With a sales volume of 174,090 units in 2022, the ID.4 demonstrated Volkswagen's commitment to electric mobility and its growing presence in the EV market.

- Overall, these top-performing EV models from Tesla and BYD, along with other notable contenders like the Wuling Hong Guang MINI EV and Volkswagen ID.4, demonstrate the increasing consumer demand for electric vehicles.

Electric Bus Battery Pack Industry Overview

The Electric Bus Battery Pack Market is fairly consolidated, with the top five companies occupying 88.11%. The major players in this market are BYD Company Ltd., China Aviation Battery Co. Ltd. (CALB), Contemporary Amperex Technology Co. Ltd. (CATL), Gotion High-Tech Co. Ltd. and Guoxuan High-tech Co. Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Electric Bus Sales

- 4.2 Electric Bus Sales By OEMs

- 4.3 Best-selling EV Models

- 4.4 OEMs With Preferable Battery Chemistry

- 4.5 Battery Pack Price

- 4.6 Battery Material Cost

- 4.7 Price Chart Of Different Battery Chemistry

- 4.8 Who Supply Whom

- 4.9 EV Battery Capacity And Efficiency

- 4.10 Number Of EV Models Launched

- 4.11 Regulatory Framework

- 4.11.1 Belgium

- 4.11.2 Brazil

- 4.11.3 Canada

- 4.11.4 China

- 4.11.5 Colombia

- 4.11.6 France

- 4.11.7 Germany

- 4.11.8 Hungary

- 4.11.9 India

- 4.11.10 Indonesia

- 4.11.11 Japan

- 4.11.12 Mexico

- 4.11.13 Poland

- 4.11.14 Thailand

- 4.11.15 UK

- 4.11.16 US

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Propulsion Type

- 5.1.1 BEV

- 5.1.2 PHEV

- 5.2 Battery Chemistry

- 5.2.1 LFP

- 5.2.2 NCA

- 5.2.3 NCM

- 5.2.4 NMC

- 5.2.5 Others

- 5.3 Capacity

- 5.3.1 15 kWh to 40 kWh

- 5.3.2 40 kWh to 80 kWh

- 5.3.3 Above 80 kWh

- 5.3.4 Less than 15 kWh

- 5.4 Battery Form

- 5.4.1 Cylindrical

- 5.4.2 Pouch

- 5.4.3 Prismatic

- 5.5 Method

- 5.5.1 Laser

- 5.5.2 Wire

- 5.6 Component

- 5.6.1 Anode

- 5.6.2 Cathode

- 5.6.3 Electrolyte

- 5.6.4 Separator

- 5.7 Material Type

- 5.7.1 Cobalt

- 5.7.2 Lithium

- 5.7.3 Manganese

- 5.7.4 Natural Graphite

- 5.7.5 Nickel

- 5.7.6 Other Materials

- 5.8 Region

- 5.8.1 Asia-Pacific

- 5.8.1.1 By Country

- 5.8.1.1.1 China

- 5.8.1.1.2 India

- 5.8.1.1.3 Japan

- 5.8.1.1.4 South Korea

- 5.8.1.1.5 Thailand

- 5.8.1.1.6 Rest-of-Asia-Pacific

- 5.8.2 Europe

- 5.8.2.1 By Country

- 5.8.2.1.1 France

- 5.8.2.1.2 Germany

- 5.8.2.1.3 Hungary

- 5.8.2.1.4 Italy

- 5.8.2.1.5 Poland

- 5.8.2.1.6 Sweden

- 5.8.2.1.7 UK

- 5.8.2.1.8 Rest-of-Europe

- 5.8.3 Middle East & Africa

- 5.8.4 North America

- 5.8.4.1 By Country

- 5.8.4.1.1 Canada

- 5.8.4.1.2 US

- 5.8.5 South America

- 5.8.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 BMZ Batterien-Montage-Zentrum GmbH

- 6.4.2 BYD Company Ltd.

- 6.4.3 China Aviation Battery Co. Ltd. (CALB)

- 6.4.4 Contemporary Amperex Technology Co. Ltd. (CATL)

- 6.4.5 Farasis Energy (Ganzhou) Co. Ltd.

- 6.4.6 Gotion High-Tech Co. Ltd.

- 6.4.7 Guoxuan High-tech Co. Ltd.

- 6.4.8 Leclanche SA

- 6.4.9 LG Energy Solution Ltd.

- 6.4.10 NFI Group Inc.

- 6.4.11 Panasonic Holdings Corporation

- 6.4.12 Proterra Operating Company Inc.

- 6.4.13 Samsung SDI Co. Ltd.

- 6.4.14 Sunwoda Electric Vehicle Battery Co. Ltd. (Sunwoda)

- 6.4.15 Tata Autocomp Systems Ltd.

- 6.4.16 TOSHIBA Corp.

7 KEY STRATEGIC QUESTIONS FOR EV BATTERY PACK CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms