|

市場調査レポート

商品コード

1683522

セキュアアクセスサービスエッジ(SASE)-市場シェア分析、産業動向、成長予測(2025年~2030年)Secure Access Service Edge (SASE) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| セキュアアクセスサービスエッジ(SASE)-市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

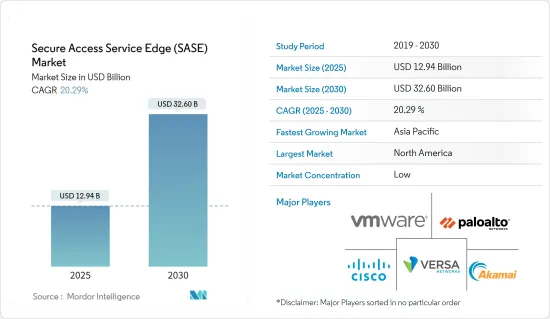

セキュアアクセスサービスエッジ市場規模は、2025年に129億4,000万米ドルと推定され、予測期間(2025年~2030年)のCAGRは20.29%で、2030年には326億米ドルに達すると予測されます。

SASEは、ネットワーク・アクセス・セキュリティのパラダイム・シフトを意味します。これは、Firewall-as-a-service(FWaaS)やSD-WANのようなネットワークとセキュリティ機能を統合し、さらにnetwork-as-a-service(NaaS)を単一のクラウドネイティブサービスに統合したものです。この統合により、分散したワークフォースとクラウドベースのアプリケーションは、スケーラブルで柔軟かつセキュアな方法で保護され、接続されます。

主なハイライト

- SASEはSDN環境のセキュリティを向上させ、Software-Defined Networking(SDN)システムを完成させる。ダイナミックなネットワーク構成はSDNによって可能になり、SASEは変化する要件に対応するために変化するネットワークの安全性を保証します。SASEは、モノのインターネット(IoT)の発展に伴い、IoTデバイスとそれらが生成するデータを保護します。IoTの文脈では、安全な通信とデータ保護が不可欠です。

- さらに、クラウドベースのSASEは採用が急増する可能性があります。例えば、2024年2月、ファーウェイはIP Club Carnivalで新しいHiSec SASEソリューションの発表を行いました。新たに発表されたこのソリューションには、クラウド-ネットワーク-エッジ-エンドポイントの統合インテリジェント・プロテクションが搭載されており、企業の本社と支社に一貫したセキュリティ保証を提供します。

- パブリック・クラウドの利用が増加するにつれ、あらゆる種類の企業でクラウドへの支出が増加しています。クラウドへの支出はすでにIT予算の中で重要な位置を占めており、約77%の企業が年間クラウド支出額が1,200万米ドルを超え、80%の企業が120万米ドルを超えると回答しています。中小企業はワークロードの数が少なく、規模も小さいため、クラウドの全体的なコストは安くなります。

- 市場関係者は、顧客にSASEサービスを提供しながら適切な規制コンプライアンスを維持し、経費を執行することに懸念を抱いています。ベンダーは、自社のテクノロジーを保護し、円滑に稼働させ、適用されるすべての法律や規制を遵守することが困難な場合があります。ベンダーが規則や基準を遵守しないことは、彼らのサービスに悪影響を及ぼし、クライアントの事業運営を危険にさらす可能性があります。ベンダーは、一般に認められた基準やサービス提供のベストプラクティスを遵守することで、それらを優先するプログラムやサービスを提供しています。ベンダーは、進化する技術や政府の規制に対応するための支援を必要としています。

- 世界的により多くの企業における投資戦略の拡大は、ビジネスの成長を支えるセキュア・アクセス・サービス・エッジの採用を加速させると思われます。COVID-19以降の時代には、シングルベンダでSASEを提供するベンダの数が大幅に増加すると思われます。COVID-19以降の時代におけるSD-WANの新規購入は、シングルベンダのSASEオファリングの一部となると思われます。

セキュアアクセスサービスエッジ(SASE)の市場動向

大企業が大きな市場シェアを占める

- エッジコンピューティングの採用拡大、クラウドインフラへの移行、リモートワークの急増により、従来のネットワークアーキテクチャやセキュリティモデルが大きく変化しています。大規模なIT予算と熟練した従業員を利用できる大企業は、この市場の現実に急速に適応しつつあります。

- 分散型ワークフォースモデルを採用する大企業は、VPNアグリゲーション容量が厳格に制限された従来のWANアーキテクチャでは、ほとんどのWFA(Work-From-Anywhere)ワークフローに対応できないことに気づいています。既存のセキュリティ・モデルと固定的なデジタル・トランスフォーメーションへの投資が、ここ数年、大企業におけるSASEの採用を遅らせています。

- 世界市場では、新たなITインフラが拡大しています。セキュリティとネットワークを単一のクラウドプラットフォームに統合する大企業が急増しています。その結果、マルウェア・アズ・ア・サービスは、病院、石油・ガス田、電力網、輸送サービス、企業ネットワークなど、露出したIoTやOTに対する大規模な運用に移行しています。脅威行為者は、動作環境や組み込まれたIoTやOTデバイスの構成を明らかにし、それを悪用するために、多大な調査努力を必要としています。

- マイクロソフトのデジタルディフェンスレポート2023によると、世界的に攻撃が増加しており、中でもID攻撃が最も多く、全体の42%がID攻撃のみだといいます。また、サイバー攻撃は年々増加しており、ランサムウェア関連の被害額は世界的に増加しています。マイクロソフトが2024年に発表した報告書によると、パスワード攻撃の試みは、1カ月あたり約30億件から300億件以上に急増しています。

- 接続されたデジタル世界では、デバイスが大規模なシステムとオンラインで通信し、大量のデータを収集し、大企業にビジネスチャンスをもたらす可視性を生み出しています。この状況はまた、サイバー脅威への扉を開き、サイバー犯罪ビジネスを数十億米ドル規模にします。コンピューター、ルーター、プリンター、ウェブカメラ、遠隔管理デバイスなどのIoTデバイスは、セキュリティ・リスクにさらされています。これらのデバイスは多くの組織の業務にとって重要であるため、すぐに責任やセキュリティ・リスクになりかねないです。あらゆる業界でIoTソリューションが急速に採用されるようになったことで、攻撃のベクトルが増え、組織がリスクにさらされる機会が増えています。リモート管理デバイスへの攻撃、ウェブ経由の攻撃、データベースへの攻撃は、大企業で最も多く発生しています。

- 前述のインシデントは、他のセキュアなネットワーキング戦略とは一線を画す能力を持つことから、大企業におけるネットワーク・アズ・ア・サービス(NaaS)の採用を後押しする可能性が高いです。SASEはデータセンターのセキュリティに依存するのではなく、ユーザーのデバイスからの全体的なトラフィックが最終目的地に送信される前に、近くに存在するポイントで検査されるため、直接的なアプローチを採用しています。そのため、クラウド上の分散したワークフォースやデータを保護するための理想的な選択肢となります。現代のクラウド中心の大企業では、ユーザー、デバイス、アプリケーションは、どこからでも作業できる安全なアクセスを必要としています。レガシーシステムは、この柔軟性を提供するために必要な帯域幅に耐えることができません。しかし、SASEは、ユーザーやデバイスの場所を問わず、企業レベルのセキュリティを維持しながらアクセスできるため、このセグメントの需要を強化しています。

北米が大きなシェアを占める

- 米国は先進経済圏であり、先進技術の導入と受容、ネットワーク自動化の開発、クラウドベースのサービスの急増がセキュアアクセスサービスエッジ市場に大きく貢献しています。エンドユーザー業界のデジタル化の進展や、シスコシステムズ、ヴイエムウェア、パロアルトネットワークス、バーサネットワークス、アカマイ・テクノロジーズといった著名ベンダーの存在が、市場の成長に寄与しています。

- 企業のデジタルトランスフォーメーションが急速に加速しているため、セキュリティはクラウドコンピューティングへと移行しています。複数のエンドユーザー産業でクラウドサービスが大幅に採用されているため、ネットワークインフラの安全性を確保し、複雑さを減らしてスピードと俊敏性を向上させる必要があります。このことは、今後数年間、市場ベンダーに大きな成長機会をもたらすと予想されます。

- 米国には3つの主要クラウドサービスプロバイダーが存在する:アマゾン・ウェブ・サービス(Amazon Web Services)、マイクロソフトのアジュール(Azure)、グーグル・クラウド(Google Cloud)です。また、5G、自律走行、IoT、ブロックチェーン、人工知能、ゲームといった主要な技術革新の拠点とも考えられています。SASEの機能を統合することで、ゼロトラスト・セキュリティ機能を企業アーキテクチャに収束させることができ、これは信頼されたネットワーク・セキュリティ体制を実現する上で最も重要です。このように、SASEソリューションはエンドユーザーのネットワークとセキュリティ・アーキテクチャを変革し、サイバーリスク、コスト、複雑さを軽減すると分析されています。

- Orange Business、パロアルトネットワークス、Orange Cyberdefenseは2023年8月に提携し、クラウドネイティブなマネージドセキュリティアクセスサービスエッジ(SASE)ソリューションを世界中の企業に提供しています。企業がハイブリッド業務に対応し、顧客に最新の製品やサービスを提供するためにクラウドの導入を加速させているため、デジタル攻撃対象領域は拡大しています。このパートナーシップは、業界で最も完全なAIを活用したSASEソリューション、アドバイザリーおよびコンサルタント・サービス、世界なマネージド・ネットワーク、セキュリティ、デジタル・サービスを提供します。このサービスを利用する組織は、SASEによる変革の投資収益率(ROI)を最大化することができます。

- カナダはクラウド導入の最前線にあります。多くの組織がパブリック、プライベート、エッジクラウドを組み合わせて導入しています。ハイブリッドワークとクラウド変革の台頭により、ネットワーク境界を越えて拡張するセキュリティサービスの需要が高まっており、カナダ市場の成長にプラスの影響を与えています。さらに、同国ではデータ保護と規制に関する法規制が厳しく、エンドユーザー業界におけるSASEソリューションの需要をさらに押し上げています。

- 自動化の進展と接続機器の導入により、市場の需要は大幅に増加すると予想されます。Network-as-a-Service(NaaS)モデルは、日々の機器メンテナンスの負荷を軽減し、顧客サービスなどのタスクに集中することで、中小企業に利益をもたらします。カナダでは小規模企業が多いため、NaaSは今後数年で大きな動向になると予想されます。

セキュアアクセスサービスエッジ(SASE)市場概要

セキュアアクセスサービスエッジ市場のベンダーは、さまざまなサービスを提供し、適度に統合されています。しかし、VMware、Palo Alto Networks、Versa Networks Inc.、Cisco Systems Inc.などの主要ベンダーは、様々な地域の様々なエンドユーザーに非常に好まれているネットワーク・サービス・プロバイダーです。

- 2024年1月-キンドリルは、顧客がセキュリティ管理を改善し、サイバーインシデントにプロアクティブに対処・対応できるよう、シスコと提携して2つの新しいセキュリティ・エッジ・サービスを開始すると発表しました。KyndrylとCiscoの利用可能なSD-WANサービスと共に新たに開始されたセキュリティエッジサービスは、企業がセキュアアクセスサービスエッジ(SASE)アーキテクチャに移行するための強固な基盤を構築することを可能にします。

- 2024年1月-AI/MLを活用した統合セキュアアクセスサービスエッジ(SASE)ソリューションのリーディングプロバイダーであるバーサネットワークスは、統合SASEゲートウェイの新シリーズを発表しました。これらのゲートウェイは、100Gbpsを超える驚異的なスループットを提供し、強化されたコンピューティング機能に対する需要の高まりに対応するよう設計されています。この需要は、ネットワーキングとセキュリティ機能の統合が進む業界によって牽引されています。Versaの新しいゲートウェイは、高性能ハードウェアとVersaオペレーティングシステム(VOS)を統合し、シングルパスアーキテクチャを特徴とする同社の統合SASEソフトウェアスタックです。このパフォーマンスの向上により、企業は初めてセキュリティ機能と複数のネットワーキングを単一のゲートウェイに統合することができます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

- 市場に影響を与えるマクロ経済要因の評価

第5章 市場力学

- 市場促進要因

- SD-WAN、FWaaS、SWG、CASB、ZTNA機能を組み合わせた単一ネットワークアーキテクチャへのニーズの高まり

- セキュリティ手順とツールの欠如

- データ保護と規制法へのコンプライアンスの義務化

- 市場抑制要因

- クラウドリソース、クラウドセキュリティアーキテクチャ、SD-WAN戦略に関する知識の不足

- 高い初期導入コストとSASEアーキテクチャとそのコンポーネントの標準化の欠如

第6章 市場セグメンテーション

- 提供タイプ別

- サービスとしてのネットワーク

- サービスとしてのセキュリティ

- 組織規模別

- 大企業

- 中小企業

- エンドユーザー産業別

- BFSI

- IT・通信

- 小売

- ヘルスケア

- 政府機関

- 製造業

- その他エンドユーザー産業別

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- ベルギー

- オランダ

- ルクセンブルク

- デンマーク

- フィンランド

- ノルウェー

- スウェーデン

- アイスランド

- アジア

- インド

- 中国

- 日本

- 台湾

- 韓国

- マレーシア

- 香港

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Cisco Systems Inc.

- VMWare Inc.

- Palo Alto Networks.

- Versa Networks Inc.

- Akamai Technologies Inc.

- Cato Networks

- Fortinet Inc.

- Check Point Software Technologies Ltd

- Cloudflare Inc.

- Forcepoint

第8章 投資分析

第9章 市場の将来展望

The Secure Access Service Edge Market size is estimated at USD 12.94 billion in 2025, and is expected to reach USD 32.60 billion by 2030, at a CAGR of 20.29% during the forecast period (2025-2030).

SASE signifies a paradigm shift in network access security. It combines network and security features, like Firewall-as-a-service (FWaaS) and SD-WAN, further combining network-as-a-service (NaaS) into a single cloud-native service. With this convergence, distributed workforces and cloud-based applications will be protected and connected in a scalable, flexible, and secure manner.

Key Highlights

- SASE improves security in SDN environments, thereby completing software-defined networking (SDN) systems. Dynamic network configuration is made possible by SDN, and SASE guarantees that these networks are secure as they change in order to meet the changing requirements. SASE protects IoT devices and the data they generate as the Internet of Things (IoT) develops. In the context of the IoT, secure communications and data protection are essential.

- Furthermore, cloud-based SASE may witness a surge in adoption. For instance, in February 2024, Huawei announced the new HiSec SASE Solution launch at the IP Club Carnival. This newly launched solution comes with cloud-network-edge-endpoint integrated intelligent protection, providing consistent security assurance for the enterprise headquarters and branches.

- The increasing usage of the public cloud is boosting cloud spending for businesses of all kinds. Cloud spending is already a significant aspect of IT budgets, wherein about 77% of companies stated that their annual cloud spending value surpasses USD 12 million, and 80% of them stated that the value exceeds USD 1.2 million. As SMBs have fewer and smaller workloads, their overall cloud costs are cheaper.

- The market players are concerned about maintaining proper regulatory compliance while offering clients SASE services and executing expenses. Sometimes, vendors find it difficult to safeguard their technology, keep running smoothly, and comply with all applicable laws and regulations. Vendors' non-compliance with rules and standards can adversely affect their services and jeopardize clients' business operations. By adhering to the accepted standards and best service-delivery practices, they offer programs and services to prioritize them. Vendors need help keeping up with evolving technologies and government regulations.

- The growth in investment strategies in a larger share of businesses globally will accelerate the adoption of secure access service edge in supporting business growth. In the post-COVID-19 era, there will be a significant increase in the number of vendors with single-vendor SASE offerings. New SD-WAN purchases in the post-COVID-19 era will be part of a single-vendor SASE offering.

Secure Access Service Edge (SASE) Market Trends

Large Enterprises will Hold Major Market Shares

- Increased adoption of edge computing, the shift to cloud infrastructure, and a surge in remote work have challenged many traditional network architectures and security models. Large enterprises with access to larger IT budgets and skilled employees are rapidly adapting to this market reality.

- Large enterprises with a distributed workforce model find the traditional WAN architectures with rigidly limited VPN aggregation capacity inadequate for most work-from-anywhere (WFA) workflows. Existing security models and fixed digital transformation investments have slowed down the adoption of SASE among large enterprises over the last few years.

- The global market is witnessing an expansion in new IT infrastructure. Large enterprises that combine security and networks into a single cloud platform are proliferating. As a result, Malware-as-a-service has moved to large-scale operations against exposed IoT and OT in hospitals, oil and gas fields, electrical grids, transportation services, and corporate networks. Threat actors require significant research efforts to uncover and exploit the configuration of operating environments and embedded IoT and OT devices.

- According to the Microsoft Digital Defense Report 2023, Microsoft said that globally, there has been a growing number of attacks, of which identity attacks are the most common, and 42% of the total attacks are only identity attacks. Also, every year, there has been an increasing number of cyberattacks, and the cost of ransomware-related damage increases globally. As per the report published by Microsoft in 2024, attempted password attacks have soared to over 30 billion from around 3 billion per month.

- In a connected digital world, devices communicate online with larger systems, collecting voluminous data and creating visibility to bring business opportunities to large enterprises. This situation also opens the doors for cyber threats, making the cybercrime business worth multi-billion dollars. IoT devices such as computers, routers, printers, web cameras, and remote management devices are at a security risk. These devices are critical to many organizations' operations; hence, they can quickly become a liability and security risk. The rapid adoption of IoT solutions close to every industry has increased the number of attack vectors and organizations' risk exposure. Attacks against remote management devices, attacks via the web, and attacks on databases are most prevalent among large enterprises.

- The aforementioned incidents are likely to boost the adoption of the network-as-a-service (NaaS) in large enterprises due to its ability to stand out from other secure networking strategies. Rather than relying on data center security, SASE has a direct approach as the overall traffic from the users' devices is inspected at a nearby point of presence before being sent to its final destination. This makes it an ideal option for protecting distributed workforces and data in the cloud. In modern cloud-centric large enterprises, users, devices, and applications require secure access while working from anywhere. Legacy systems cannot tolerate the bandwidth needed to provide this flexibility. However, SASE can do so while maintaining enterprise-level security for users and devices at any location, which bolsters this segment's demand.

North America will Hold a Significant Share

- The United States is a developed economy with a significant inclination toward implementing and accepting advanced technology, development in network automation, and surge in cloud-based services, thereby contributing to the secure access service edge market. The growing digitization among end-user industries and the presence of prominent market vendors, like Cisco Systems Inc., Vmware Inc., Palo Alto Networks, Versa Networks Inc., and Akamai Technologies, are contributing to the market's growth.

- Security is moving toward cloud computation due to the fast acceleration of the digital transformation of businesses. The significant adoption of cloud services in several end-user industries necessitates securing the network infrastructure and reducing complexity to improve speed and agility. This is anticipated to create substantial growth opportunities for market vendors in the coming years.

- The United States is home to three major cloud service providers: Amazon Web Services, Microsoft's Azure, and Google Cloud. It is also considered to be the hub for major technological innovations such as 5G, autonomous driving, IoT, Blockchain, artificial intelligence, and gaming. Integrating SASE capabilities converges zero trust security capabilities into enterprise architectures, which is paramount in achieving a trusted network security posture. Thus, SASE solutions are analyzed to transform the end-users networks and security architectures to reduce cyber risks, costs, and complexities.

- Orange Business, Palo Alto Networks, and Orange Cyberdefense partnered in August 2023 to deliver a cloud-native managed security access service edge (SASE) solution to enterprises globally. The digital attack surface has expanded as organizations expedite cloud adoption to accommodate hybrid work and deliver the latest products and services to their customers. The partnership provides the industry's most complete AI-powered SASE solutions, advisory and consultant services, and global managed network, security, and digital services. Organizations using this offering can maximize their SASE transformation's return on investments (ROI).

- Canada is at the forefront of cloud adoption. Many organizations are deploying a mix of public, private, and edge clouds. With the rise of hybrid work and cloud transformation, the demand for security services to expand beyond the network perimeter is increasing, positively impacting the growth of the country's market. In addition, stringent data protection and regulatory legislation in the country further drive the demand for SASE solutions in end-user industries.

- The market demand is anticipated to rise significantly due to increasing automation and deploying connected devices. The network-as-a-service (NaaS) model benefits small businesses by offloading day-to-day equipment maintenance and focusing on tasks such as customer service. With a large base of small businesses in Canada, NaaS is expected to become a significant trend in the coming years.

Secure Access Service Edge (SASE) Market Overview

The secure access service edge market vendors are moderately consolidated with an array of services. However, major vendors like VMware, Palo Alto Networks, Versa Networks Inc., and Cisco Systems Inc. are highly preferred network service providers for various end users in various regions.

- January 2024 - Kyndryl announced that the company partnered with Cisco to launch two of its new security edge services in order to help customers improvise their security controls and address and respond to cyber incidents proactively. The newly launched security edge services along with Kyndryl and Cisco's available SD-WAN services, enable organizations to build a solid foundation to transition into a secure access service edge (SASE) architecture.

- January 2024-Versa Networks, a leading provider of AI/ML-powered Unified Secure Access Service Edge (SASE) solutions, has announced the launch of a new series of Unified SASE gateways. These gateways offer an impressive throughput exceeding 100 Gbps, designed to address the rising demand for enhanced computing capabilities. This demand is driven by the industry's increasing integration of networking and security functions. Versa's new gateways integrate high-performance hardware with the Versa Operating System (VOS), the company's unified SASE software stack, which features a single-pass architecture. This improved performance allows organizations to consolidate security functions and multiple networking into a single gateway for the first time.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products and Services

- 4.3 Assessment of Macro Economic Factors Impact on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Need for a Single Network Architecture that Combines SD-WAN, FWaaS, SWG, CASB, and ZTNA Capabilities

- 5.1.2 Lack of Security Procedures and Tools

- 5.1.3 Mandatory Compliance with Data Protection and Regulatory Legislation

- 5.2 Market Restraints

- 5.2.1 Lack of Knowledge of Cloud Resources, Cloud Security Architecture, and SD-WAN Strategy

- 5.2.2 High Upfront Implementation Costs and Lack of Standardization Around SASE Architecture and Its Components

6 MARKET SEGMENTATION

- 6.1 By Offering Type

- 6.1.1 Network as a Service

- 6.1.2 Security as a Service

- 6.2 By Organization Size

- 6.2.1 Large Enterprises

- 6.2.2 Small and Medium Enterprises

- 6.3 By End-user Vertical

- 6.3.1 BFSI

- 6.3.2 IT and Telecom

- 6.3.3 Retail

- 6.3.4 Healthcare

- 6.3.5 Government

- 6.3.6 Manufacturing

- 6.3.7 Other End-user Verticals

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 United Kingdom

- 6.4.2.3 France

- 6.4.2.4 Spain

- 6.4.2.5 Italy

- 6.4.2.6 Belgium

- 6.4.2.7 Netherlands

- 6.4.2.8 Luxembourg

- 6.4.2.9 Denmark

- 6.4.2.10 Finland

- 6.4.2.11 Norway

- 6.4.2.12 Sweden

- 6.4.2.13 Iceland

- 6.4.3 Asia

- 6.4.3.1 India

- 6.4.3.2 China

- 6.4.3.3 Japan

- 6.4.3.4 Taiwan

- 6.4.3.5 South Korea

- 6.4.3.6 Malaysia

- 6.4.3.7 Hong Kong

- 6.4.3.8 Australia and New Zealand

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Cisco Systems Inc.

- 7.1.2 VMWare Inc.

- 7.1.3 Palo Alto Networks.

- 7.1.4 Versa Networks Inc.

- 7.1.5 Akamai Technologies Inc.

- 7.1.6 Cato Networks

- 7.1.7 Fortinet Inc.

- 7.1.8 Check Point Software Technologies Ltd

- 7.1.9 Cloudflare Inc.

- 7.1.10 Forcepoint